Closing ESG gaps in the consumer industry

Many consumer companies make ESG progress despite challenges

Deloitte’s 2024 Sustainability Action Report surveyed executives to understand how many public and private companies across sectors—including retail and consumer products—are thinking about and addressing environmental, social, and governance (ESG) disclosures. Despite persisting data challenges, discover how many consumer companies are making strides in their ESG plans.

Consumer companies plan for evolving climate-related requirements

In the past few years, many US consumer companies have begun to implement frameworks such as the Task Force on Climate-Related Financial Disclosures (TCFD) (44%), the Global Reporting Initiative (GRI) (44%), and the International Sustainability Standards Board (ISSB)/Sustainability Accounting Standards Board (SASB) (50%) into their reporting process. Despite the current stay on the landmark March 6, 2024, US Securities and Exchange Commission's (SEC) climate rule1, there are other regulations (such as the Corporate Sustainability Reporting Directive [CSRD]) and California climate laws that are still in place. Considering how relevant these frameworks are to a company’s sustainability reporting, the stay on the SEC’s rule should not deter public companies from considering how climate reporting fits into their broader ESG strategies.

In January 2024, we asked 250 consumer industry executives within the retail and consumer products sectors to weigh in on the implications they’re observing for oversight, assurance, and other aspects of the transition toward a more sustainable future. Explore these detailed insights into ESG readiness among the consumer industry, the challenges they see themselves up against, and the potential impact of sustainability reporting regulations on their climate tracking and reporting practices.

ESG report insights

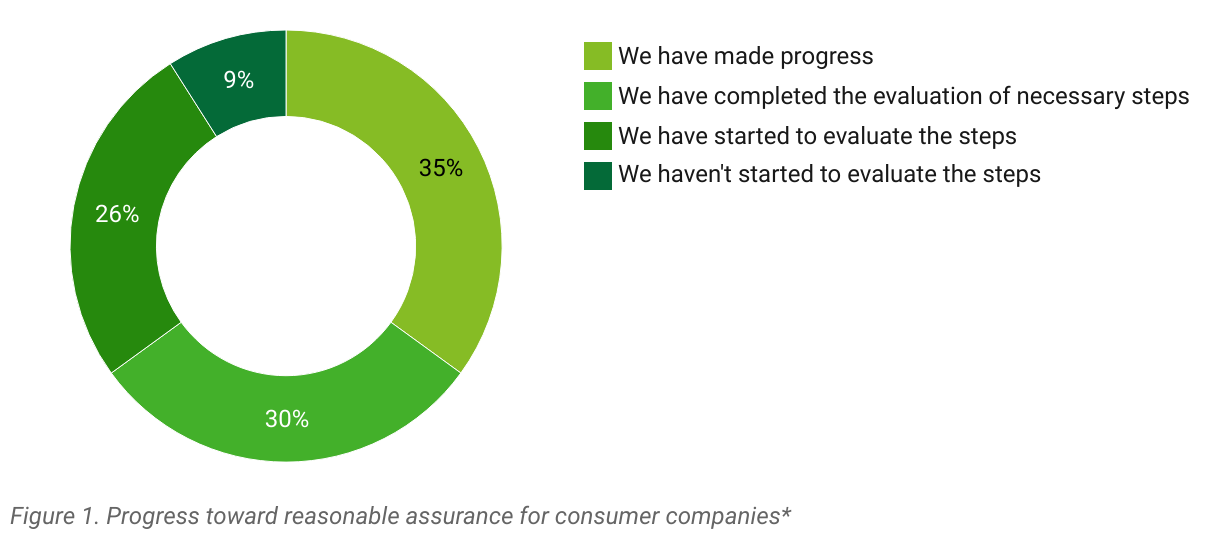

Slow but steady progress toward a reasonable level of assurance

Nearly a third (30%) of consumer executives' companies have already completed their evaluation of steps to move to a reasonable level of assurance; another 61% have at least started.

Consumer executives report making progress toward a reasonable level of assurance, however it is measured.

It is possible that the small percentage of companies that have yet to begin are apprehensive to adjust for regulations that might change in the future. However, despite the stay on the SEC's new climate-related reporting mandate, other regulations already in play suggest that starting sooner than later can be advantageous.

*The objective of a limited assurance engagement is for the service provider to express a conclusion about whether it is aware of any material modifications that a company should make for the subject matter to be in accordance with the relevant criteria. By contrast, the objective of a reasonable assurance engagement, which provides the same level of assurance as an audit of a company's financial statements, is to express an opinion on whether the subject matter is, in all material respects, in accordance with the relevant criteria.

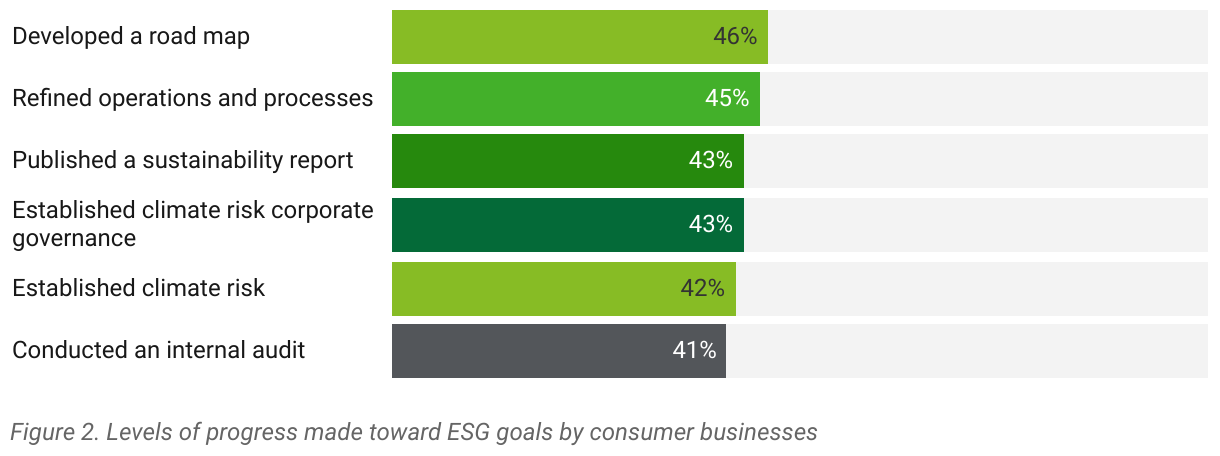

Concrete steps toward ESG goals

Consumer executives say their companies have already taken several steps toward their ESG goals; notably, they have developed a roadmap (46%), refined their operations and processes (45%), and published a sustainability report (43%).

Many companies have identified what is important to their ESG journey and are making significant progress toward their goals. However, there is still a considerable way to go for those who have not yet laid the foundation, and a proactive, sooner-than-later approach is suggested to keep pace with industry requirements.

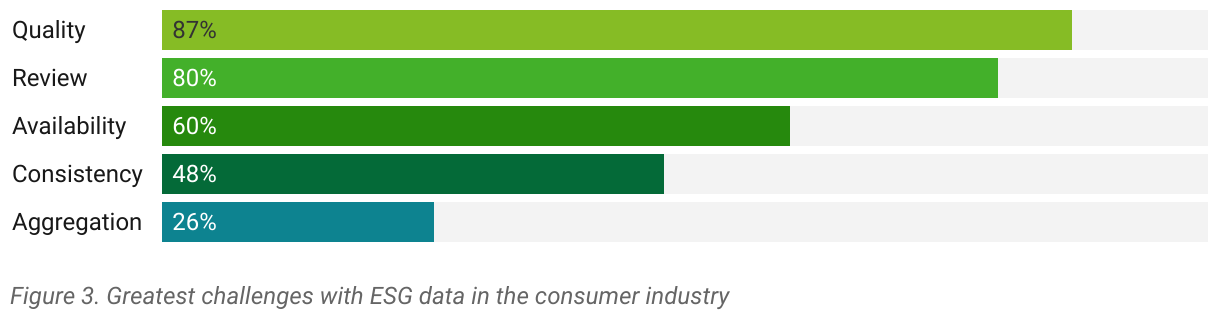

Similar to other industries, data quality remains a challenge

Most consumer executives cite ESG data quality as a top challenge (87%), followed by data review (80%).

For many consumer companies, gathering data from within the supply chain is particularly difficult. And for many, it's their first time gathering this data. This is consistent with other industries that participated in our Sustainability Action Report survey, with 88% of all total respondents citing data quality as one of their top three challenges.

This is associated with many questions, including “What data are we gathering?”, “What technology can we utilize to gather it?” and “How can we utilize automation technology to ensure that we gather it in a more efficient and effective way?” A more effective internal audit strategy can, in part, help answer these questions—shedding light on the data gaps that may be necessary to fill on the way to ESG reporting compliance.

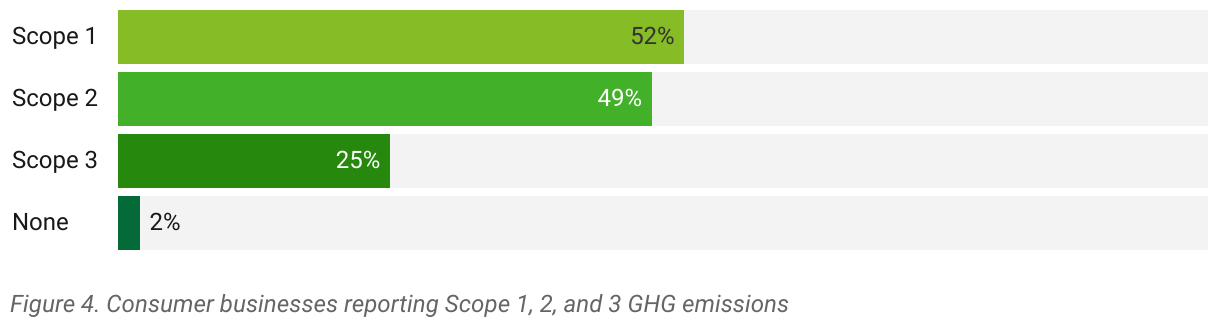

Disclosure of Scope 1 and Scope 2 GHG emissions under way, while Scope 3 lags behind

A roughly equal number of consumer executives say they are currently preparing and disclosing Scope 1 (52%) and Scope 2 (49%) GHG emissions; only a quarter (25%) are currently preparing and disclosing Scope 3 GHG emissions.

Regardless of where companies are on their ESG journey, Scope 1 and Scope 2 GHG emissions are important to disclose. And while the SEC’s March 6 ruling excludes Scope 3 from its reporting requirements, other stakeholders and reporting bodies, such as the CSRD, expect them to be reflected on their climate-related financial reports.

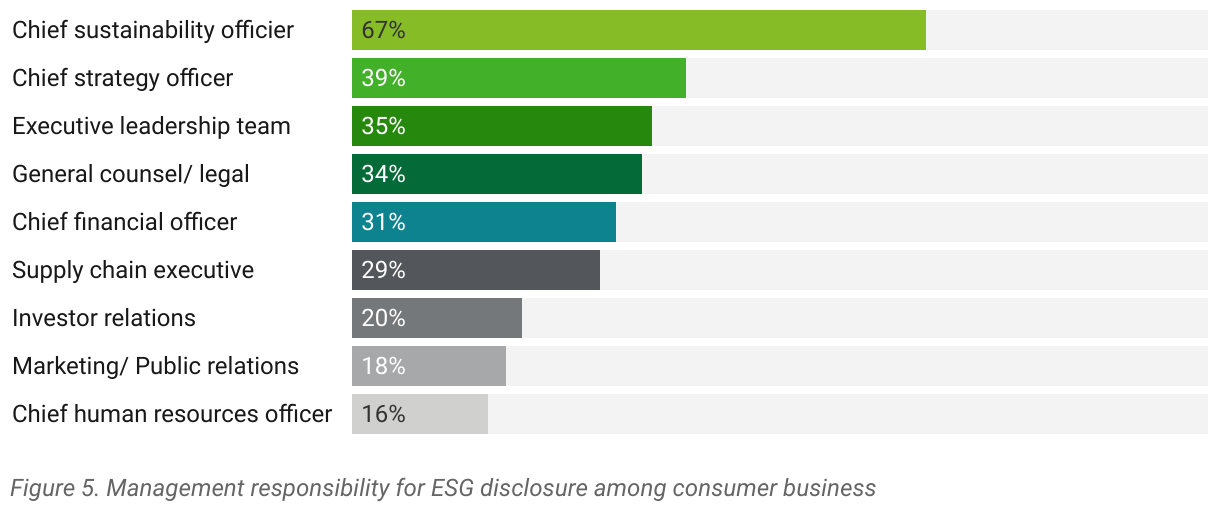

Evolving roles for ESG disclosure management

More than two-thirds (67%) of consumer respondents' companies have a chief sustainability officer with management responsibility over their ESG disclosures; if not that, a chief strategy officer is often involved (39%).

ESG capacity building has become a priority in the consumer industry, with 80% of respondents saying their company has created a new internal role or responsibility to prepare for increased ESG disclosure requirements. Those further along in their ESG journey (that have a plan in place and know what they need to move forward), might designate an ESG controller to be present for data collection, analysis, and management.

Despite where the overall responsibility lies, 85% of executives say their company has, or is in the process of establishing, an ESG council or working group inclusive of personnel from various functions (e.g., accounting, finance, legal, HR). These companies have a regular meeting cadence (49% of which meet quarterly) to address progress regarding ESG.

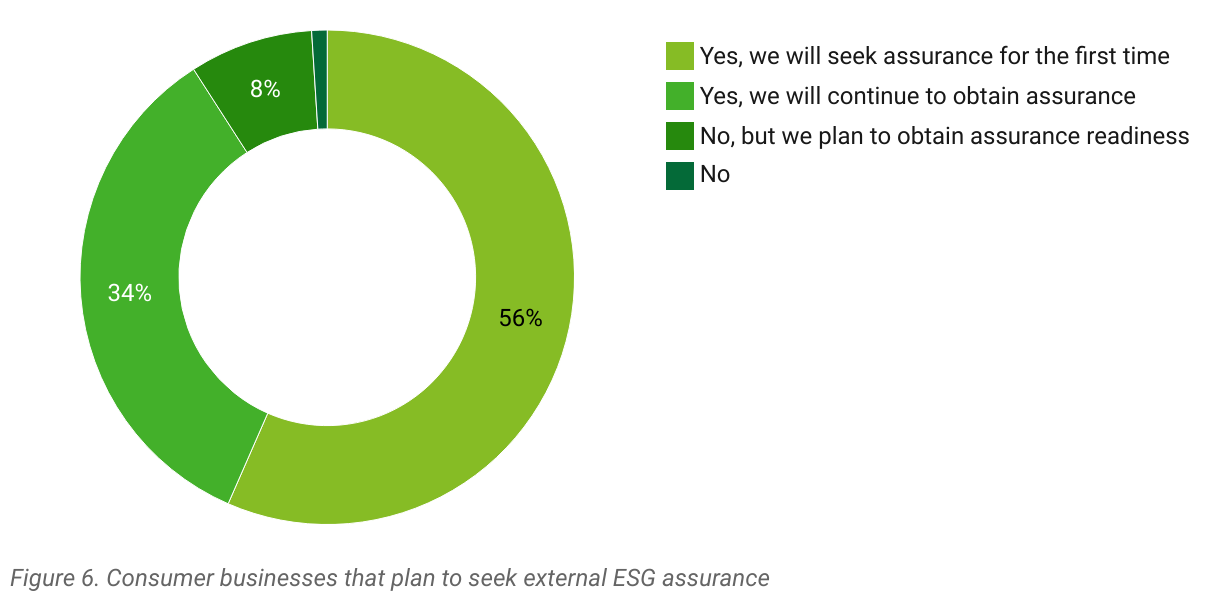

New objective to find external ESG assurance

More than half (56%) of consumer executives say they plan to seek external assurance over ESG disclosures for the first time in the next reporting cycle.

For those planning to seek external assurance for their ESG disclosures, the time to start preparing is now. Not only is timeliness important for meeting stakeholder expectations for accurate and reliable information, but resources (external and internal) are typically limited. Being proactive allows for the opportunity to take advantage of the appropriate solutions for making progress toward ESG goals.

Telling your own ESG story

Deloitte's 2024 Sustainability Action Report highlights that consumer companies are making significant progress in their ESG efforts. Despite evolving ESG demands, many companies are starting their ESG journeys from square one.

You might require assistance in identifying the path forward and the necessary tools for the journey. Where can you start?

- Understand expectations

- Have a defined plan/structure

- Connect ESG efforts with value creation

- Plan a more effective internal audit strategy that incorporates ESG risk

More than half (54%) of consumer executives report that enhanced trust with stakeholders is one of the top three business outcomes most likely influenced by improved ESG reporting. The top stakeholders from those companies feel that the most pressure regarding their organization's ESG reporting and disclosure policy comes from the board of directors (56%) and ESG rating agencies (42%), followed by investors (39%) and customers (33%).

This implies that if your company isn't telling its ESG story, it's likely that someone else is. And while following regulations is an important chapter in that story, it's far from the only one important to the plot. Prioritizing ESG means prioritizing the sustainable and equitable future that many of your key stakeholders are eager to invest in.

Whether your company needs help understanding regulatory changes, assessing their impact on your greater ESG strategy, or defining an implementation plan, we invite you to contact us. Our breadth of knowledge, resources, and experience can advise your ESG story, demystify financial reporting requirements, and help you understand the importance of a materiality assessment. Reach out to one of our resources to learn more and get started.

Featured resources

Methodology

The Deloitte ESG Survey was conducted by Wakefield Research (www.wakefieldresearch.com) among 300 Executives at publicly owned companies with a minimum annual revenue requirement of $500 million or more. Executives are defined as Senior Finance, Accounting, Sustainability, and Legal Executives with a minimum seniority of director, or Chief Risk Officers, General Counsels, Chief Legal Officers or Chief Sustainability Officer. Oversample interviews were conducted to increase the total sample size to 250 public and private companies in each of the following industries: Life Science and Healthcare; Financial Services; Consumer Products; Technology, Media & Telecommunications; Energy & Utilities. The survey was fielded between January 4th and January 18th, 2024, using an email invitation and an online survey.

Data rounding

Percentages throughout survey may not sum to 100% due to rounding.

Endnote

1 On April 4, 2024, the SEC voluntarily stayed the effective date of the final rule pending judicial review of petitions challenging it, which have been consolidated for review by the US District Court of Appeals for the Eighth Circuit. The SEC stated that it “will continue vigorously defending the [climate rule's] validity in court” but issued the stay to “facilitate the orderly judicial resolution of” challenges presented against the climate rule and to avoid “potential regulatory uncertainty if registrants were to become subject to the [climate rule's] requirements” before the legal challenges were settled. The stay does not reverse or change any of the final rule's requirements nor does it affect the SEC's existing 2010 interpretive release on climate change disclosures. For additional details, read Deloitte's “Comprehensive Analysis of the SEC's Landmark Climate Disclosure Rule.”

The services described herein are illustrative in nature and are intended to demonstrate our experience and capabilities in these areas; however, due to independence restrictions that may apply to audit clients (including affiliates) of Deloitte & Touche LLP, we may be unable to provide certain services based on individual facts and circumstances.

This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.

As used in this document, Deloitte means Deloitte & Touche LLP, a subsidiary of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of our legal structure. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Copyright © 2024 Deloitte Development LLC. All rights reserved.