The financial services industry’s (FSI) answer to ESG regulations and stakeholder demands

Financial sector executives state progress despite obstacles

Many FSI organizations are taking action to determine progress against sustainability goals and the continuously evolving reporting requirements surrounding them. Discover more from Deloitte’s Sustainability Action Report, which surveyed 250 executives to learn how many companies across various industries are thinking about and addressing environmental, social, and governance (ESG) disclosures.

Responsibility, expectation, and action: FSI sustainability progress

Financial services organizations play a significant role in progressing sustainability initiatives. Not only do they account for their own operations, but they also provide capital to other companies that can be used to advance their sustainability initiatives through financing, facilitating transactions, and insurance activities.

According to financial services executives responding to the survey, the most pressure for transparency and progress in ESG reporting and disclosure policy comes from many different angles, including the board of directors (53%); ESG rating agencies (49%); and customers, consumers, and clients (38%). High expectations from these different stakeholders, as well as evolving reporting obligations, have resulted in many financial services organizations closely monitoring the progress made toward their sustainability objectives, as well as the reporting obligations surrounding them.

Deloitte conducted a survey of 250 FSI executives about the status of their sustainability journeys. Among these participants were a mix of public and private companies representing a variety sectors, including banking and capital markets, insurance, investment management, and real estate. Among FSI respondents were sectors representing banking and capital markets, insurance, investment management, and real estate. Here’s what we learned about the FSI approach to ESG disclosures.

ESG report insights

FSI stands out in its progress toward sustainability goals

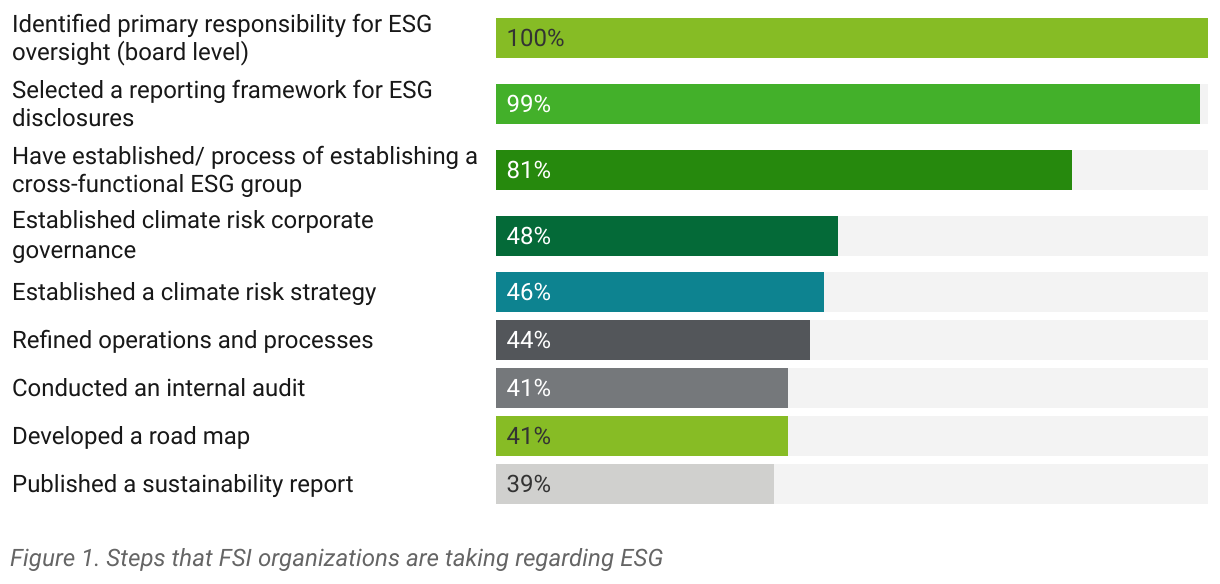

All FSI organization respondents identified responsibility for ESG oversight (100%) at the board level, 99% selected a reporting standard, and 81% have established, or are in the process of establishing, an ESG working group (figure 1).

Public FSI organizations have made progress on most ESG-related activities reflected in figure 1, a trend that aligns with various climate-related financial reporting requirements. However, it's important to note that private organizations in the financial services industry have shown less progress on certain other activities compared to public FSI organizations, displaying the potential need for better preparedness.

Moving toward an adequate level of ESG reporting readiness is important for public and private organizations, as entities that require reporting will need to understand how to incorporate climate-related disclosures. If these steps have not been taken, it is becoming increasingly important to start taking a timely, proactive approach.

Most FSI organizations are proactive about sustainability

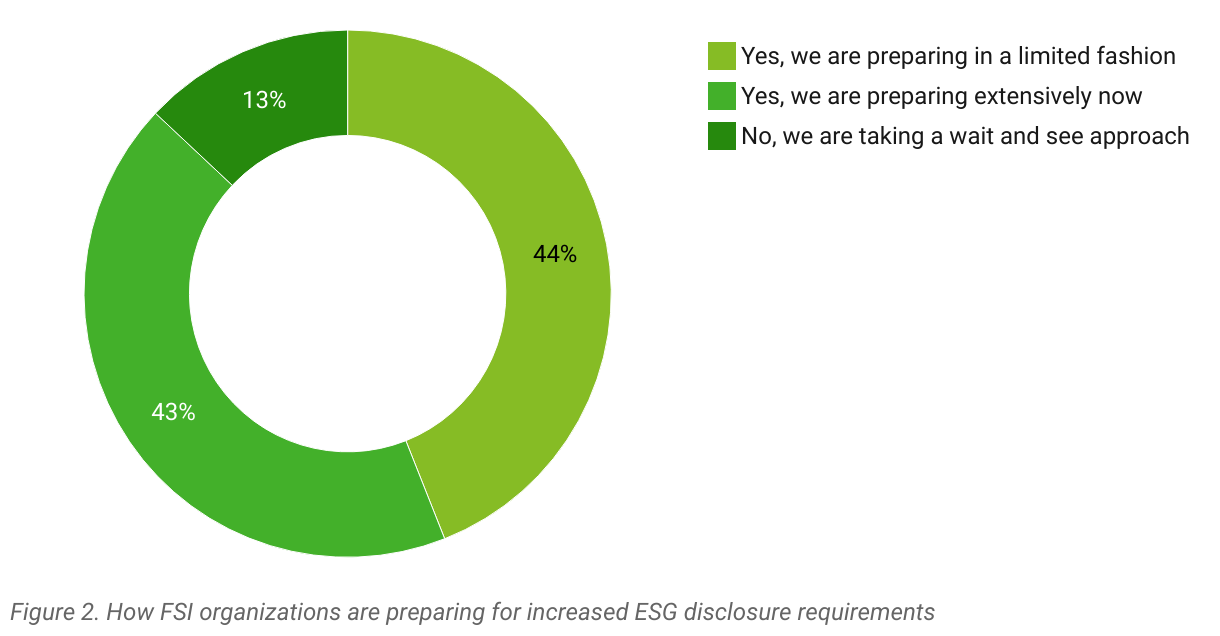

When asked if and how they're preparing, 87% of FSI executives indicated they are currently preparing for increased disclosure requirements. Meanwhile, 44% are preparing in a limited fashion for the potential increase in ESG regulatory or other disclosure requirements, while almost the same number (43%) are preparing extensively now. The remaining 13% of respondents are taking a “wait and see” approach (figure 2).

FSI organizations use a variety of reporting standards

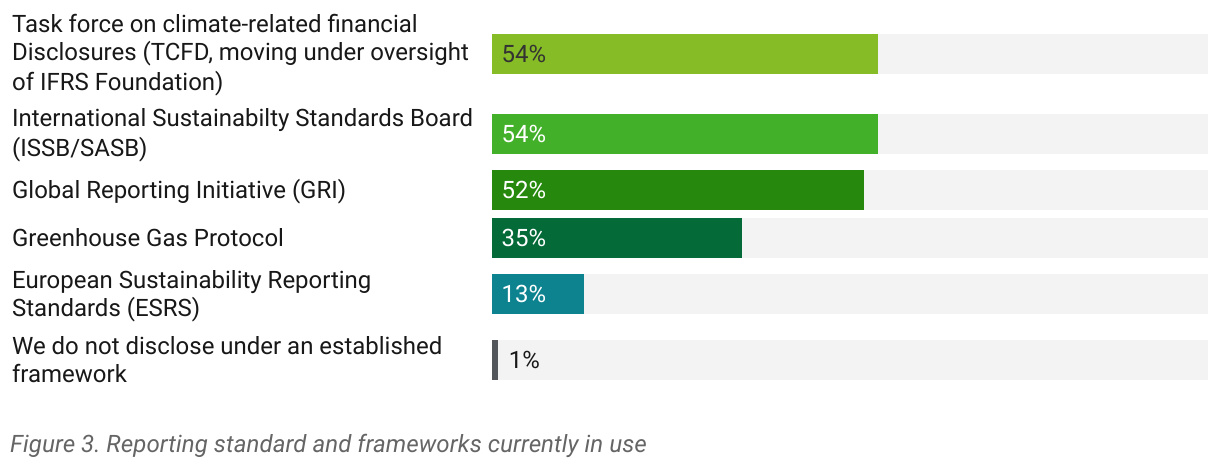

Three voluntary reporting standards are most prevalent and commonly used at financial services organizations (figure 3): 54% report using the Task Force on Climate-related Financial Disclosures (TCFD), 54% report using the International Sustainability Standards Board (ISSB) and Sustainability Accounting Standards Board (SASB), and 52% report using the Global Reporting Initiative (GRI).

Only 35% of respondents are using the industry standard Greenhouse Gas (GHG) Protocol. Public and private respondents alike reported that they are taking steps toward enhancing their financial reporting capabilities and controls around GHG emissions reporting; however, this suggests that there is still work to be done to comply with climate-related rules and regulations.

FSI organizations are enhancing their ESG reporting

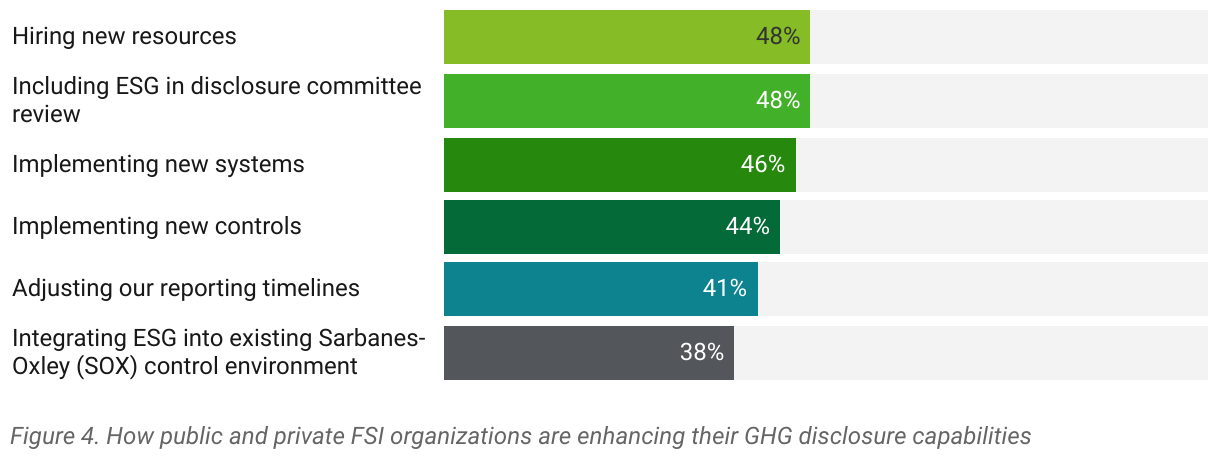

Many financial services executives reported they are taking steps toward enhancing their financial reporting capabilities and the controls around the GHG emissions measurement as well as other related financial reporting impacts of climate change (figure 4).

Public FSI executives report having made progress in enhancing their climate reporting-related capabilities and controls, with 55% of respondents having hired new resources and 50% having adjusted their reporting timelines. Meanwhile, 48% of private FSI organizations report having implemented new systems, and 44% have implemented new controls. Additionally, based on Deloitte's observations, we have seen the rise of ESG controllers taking on elevated responsibilities for disclosure in many organizations.

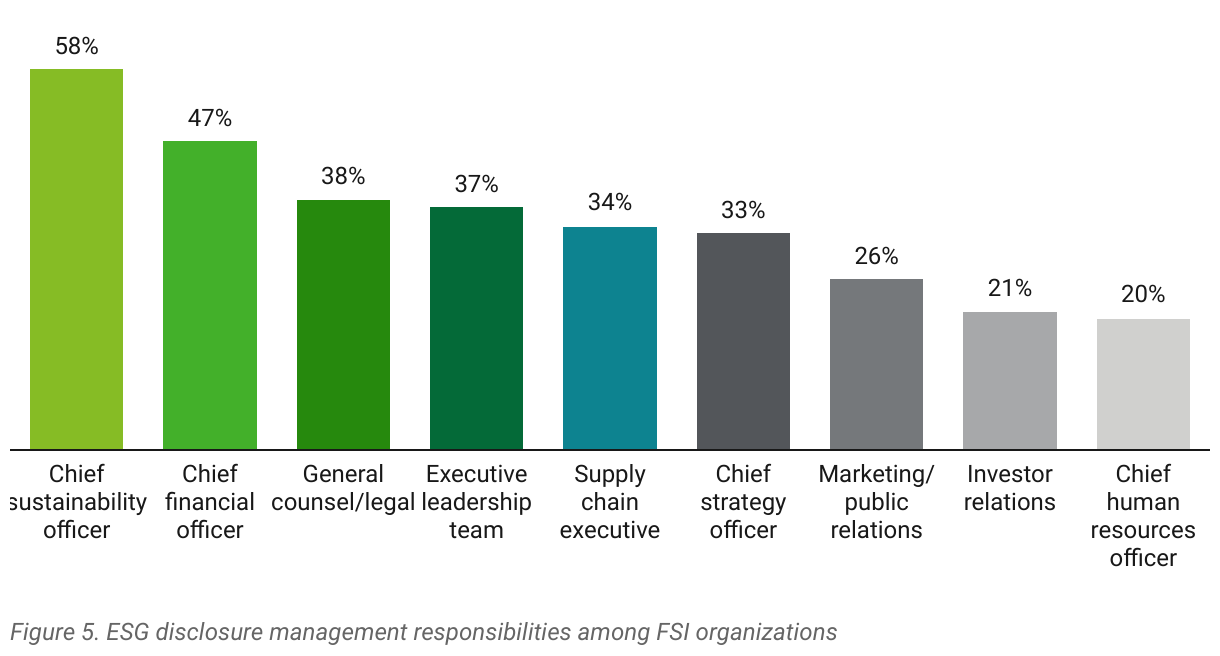

CSOs lead CFOs in most responsibilities over FSI ESG disclosures

Chief sustainability officers (CSOs) most commonly have management responsibility for ESG disclosures (58%), though for nearly half of FSIs (47%), joint responsibilities also lie with chief financial officers (CFOs). See figure 5.

The difference in ESG disclosure management responsibility between the CFO and CSO is less significant in public FSI organizations compared with private ones. According to private FSI organization executives, the CSO has more management responsibility (63%) at their organization compared to the CFO (44%). But for public FSI organizations, these two roles are considered to be more evenly weighted, with 53% of public respondents noting their CSO and 51% noting their CFO has management responsibility.

As regulatory requirements shift climate-related disclosures from voluntary to mandatory, we anticipate the CFO will become more involved in the organization's sustainability goals. The CSO's subject knowledge remains an important piece of the sustainability story, but regulation generally results in a CFO taking ownership of some controllership and finance activities.

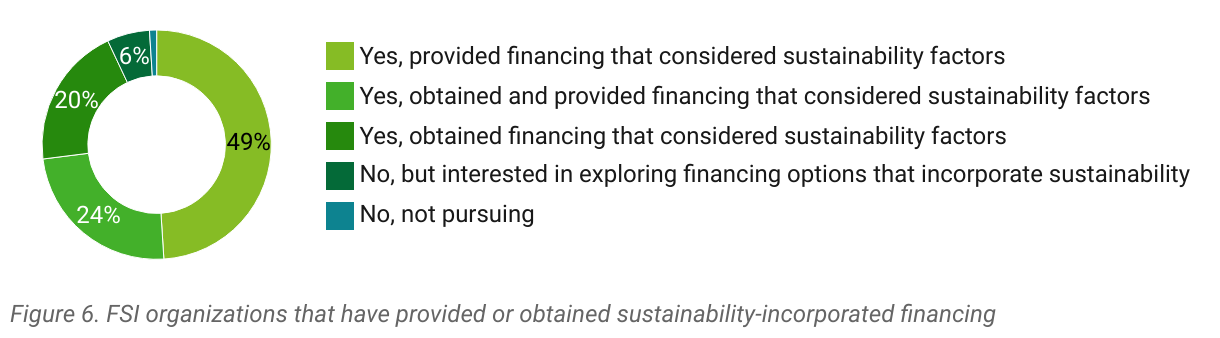

A large majority of FSI organizations have engaged in sustainability-related financing

Of the financial services executives surveyed (figure 6), 93% have either provided or obtained financing that incorporates sustainability considerations (e.g., Green Bonds).

Financing that integrates sustainability considerations is becoming important in building public trust in an organization's sustainability strategy. The increasing number of FSI organizations providing sustainability-incorporated financing is evidence of a growing market demand. The surge in public FSI organizations seeking green financing signifies that many investors are prioritizing financing that accounts for green initiatives, viewing it as important for maintaining market capital. The bottom line? Sustainable financing matters in the financial services industry.

How can you get on board with other ESG-focused FSI leaders?

The successful implementation of ESG-related reporting typically begins with a well-devised plan and includes a thorough understanding of your organization's ESG reporting circumstances as well as the new requirements that might affect them. Through that thorough understanding, this preparation should also address any existing gaps.

According to this year's report, financial services organizations are making strides toward achieving their sustainability objectives. However, some FSI organizations report taking a “wait and see” approach, signaling room for progress that may necessitate a more proactive approach.

Figure 7. The ESG readiness journey

The message here is clear: Don't delay in getting prepared. Despite pending developments, the Securities and Exchange Commission (SEC) ruling on March 6, 20241, along with the standards applicable globally through the Corporate Sustainability Reporting Directive (CSRD) and those in California, could dramatically expand the scope and detail of what you're required to disclose. If your organization has been readying itself for broader ESG regulatory requirements, the good news is you're likely not starting from zero. The groundwork you've laid for ESG can be applied in a comprehensive manner to meet disclosure requirements, thereby fostering efficiency and allowing you to effectively manage risk.

Regardless of your specific goals or where you currently stand on your sustainability journey, our sustainability and transformation team is here to advise you as you work to speed up your progress toward integration maturity and disclosure readiness. To understand if your current financial reporting processes are in line with your ESG objectives, reach out to one of our experienced advisers.

Kevin Richards

Sarah Digirolamo

Featured resources

Methodology

The Deloitte ESG Survey was conducted by Wakefield Research (www.wakefieldresearch.com) among 300 Executives at publicly owned companies with a minimum annual revenue requirement of $500 million or more. Executives are defined as Senior Finance, Accounting, Sustainability, and Legal Executives with a minimum seniority of director, or Chief Risk Officers, General Counsels, Chief Legal Officers or Chief Sustainability Officer. Oversample interviews were conducted to increase the total sample size to 250 public and private companies in each of the following industries: Life Science and Healthcare; Financial Services; Consumer Products; Technology, Media & Telecommunications; Energy & Utilities. The survey was fielded between January 4th and January 18th, 2024, using an email invitation and an online survey.

Data rounding

Percentages throughout survey may not sum to 100% due to rounding.

Endnote

1 On April 4, 2024, the SEC voluntarily stayed the effective date of the final rule pending judicial review of petitions challenging it, which have been consolidated for review by the US District Court of Appeals for the Eighth Circuit. The SEC stated that it “will continue vigorously defending the [climate rule's] validity in court” but issued the stay to “facilitate the orderly judicial resolution of” challenges presented against the climate rule and to avoid “potential regulatory uncertainty if registrants were to become subject to the [climate rule's] requirements” before the legal challenges were settled. The stay does not reverse or change any of the final rule's requirements nor does it affect the SEC's existing 2010 interpretive release on climate change disclosures. For additional details, read Deloitte's “Comprehensive Analysis of the SEC's Landmark Climate Disclosure Rule.”

The services described herein are illustrative in nature and are intended to demonstrate our experience and capabilities in these areas; however, due to independence restrictions that may apply to audit clients (including affiliates) of Deloitte & Touche LLP, we may be unable to provide certain services based on individual facts and circumstances.

This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.

As used in this document, Deloitte means Deloitte & Touche LLP, a subsidiary of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of our legal structure. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Copyright © 2024 Deloitte Development LLC. All rights reserved.