Taxing Christmas

Tax Alert - December 2025

By Robyn Walker, Rose Basile and Katie Helm

Have Santa’s elves been busy bringing joy to your workplace?

While the work Christmas party and gift-giving bring joy, they can also bring confusion when it comes to understanding the tax implications for both employers and employees. Behind the sparkle of parties and presents lie three key tax regimes: FBT, PAYE, and entertainment expenditure, with each regime bringing its own festive twist, subtle enough to keep even the elves guessing. Whether you’re hosting a Christmas party, giving gifts to staff, or entertaining clients, chances are one of these regimes will apply, but which one isn’t always clear.

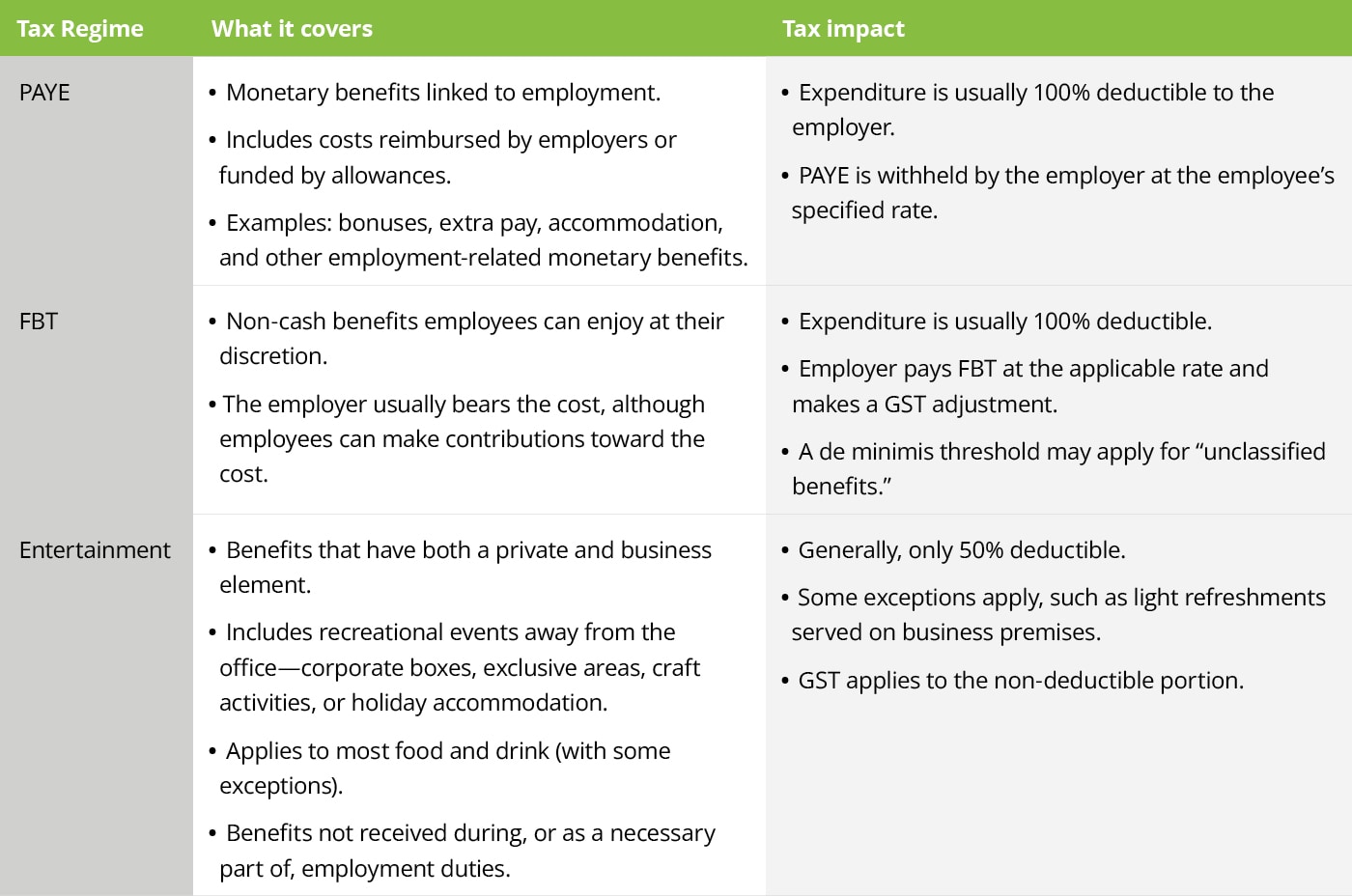

The PAYE rules will apply where any monetary compensation is provided to employees in connection with their employment, think of things like bonuses, and gratuities provided to employees. Accommodation is also taxed through PAYE.

The entertainment expenditure rules reduce income tax deductions by 50% for certain types of expenditure including corporate boxes, holiday accommodation, expenditure on yachts, food and drink at celebrations, and all connected incidental expenditure.

The FBT regime then comes in to capture non-cash benefits that are provided to employees in connection with their employment. While there is some overlap between the entertainment rules and FBT, the entertainment rules will generally override FBT, unless:

- the employee can choose when to enjoy the benefit or the benefit is enjoyed outside New Zealand

- the benefit is not received or used in the course of, or as a necessary consequence of, the employee’s employment duties.

For example, if you take your team out for a Christmas lunch the entertainment rules kick in. Swap that for a restaurant voucher they can use anytime, and you’re in FBT territory.

This table provides a quick summary of the three regimes:

Christmas party off-site

Planning a festive event away from the office? Costs for food, drinks, and venue hire fall under entertainment expenditure rules. Incidental expenses—such as crockery, glassware, utensils, waitstaff, or music—are also included.

Tax impact: Only 50% of these costs are deductible.

Staff cash bonuses

Cash bonuses paid to employees are taxable under PAYE rules. These payments relate to employment but are not part of regular salary or wages.

Tax impact: Bonuses should be taxed at the “extra pay” rate.

Christmas gifts for employees

Most gifts to employees are subject to FBT. If instead you allow employees to buy their own gift and provide a reimbursement the cost after the fact, it falls under PAYE.

Tip: Some benefits may qualify for an FBT exemption under the 'de minimis rule' if:

- Total unclassified benefits for all employees are under $22,500 in the past 12 months.

- No employee receives more than $300 per quarter ($1,200 annually).

Common examples: vouchers, gifts, flowers.

Gifts for clients and customers

Here’s an interesting twist: Inland Revenue treats any food and drink as entertainment expenditure, even when given as a gift.

Example: A gift basket with wine, cheese, towels, and soap.

Tax impact: Towels and soap are fully deductible, but wine and cheese are only 50% deductible.

We hope this clears up some common misunderstandings around employment tax regimes. If you have questions, contact your usual Deloitte advisor.

From us to you

Merry Christmas and Happy New Year!

The Tax Alert team wishes you a joyful festive season and a well-deserved break!

December 2025 - Tax Alerts

- Shareholder loans. Yeah, nah

- Bringing up the rear: final two shortfall penalty guidance documents published

- Employment Leave Act: a new era for leave entitlements in New Zealand

- Future proof your tax governance framework: the Participating Advisor advantage

- Software development and SaaS expenditure under the policy spotlight

- Five-year RDTI review confirms strong business backing and economic impact

- Home office or Business hub?

- Emissions Trading Scheme for non-forestry industries

- Snapshot of recent developments