Shareholder loans. Yeah, nah.

Tax Alert - December 2025

New Zealanders have long been known for having laid-back, casual attitude, with “she’ll be right” being a popular idiom. There are concerns that this casual approach has flowed into New Zealand’s businesses with a rather lackadaisical approach to managing interactions between businesses and shareholders in some cases leading to large shareholder loan balances which are unrecoverable when a business gets into trouble.

With increased funding to investigate taxpayers, it seems Inland Revenue have formed the view that more discipline is required in this area and a “no worries” approach is no longer fit for purpose. In early December Inland Revenue released a consultation document “Improving taxation of loans made by companies to shareholders – Officials’ issues paper” (the Paper).

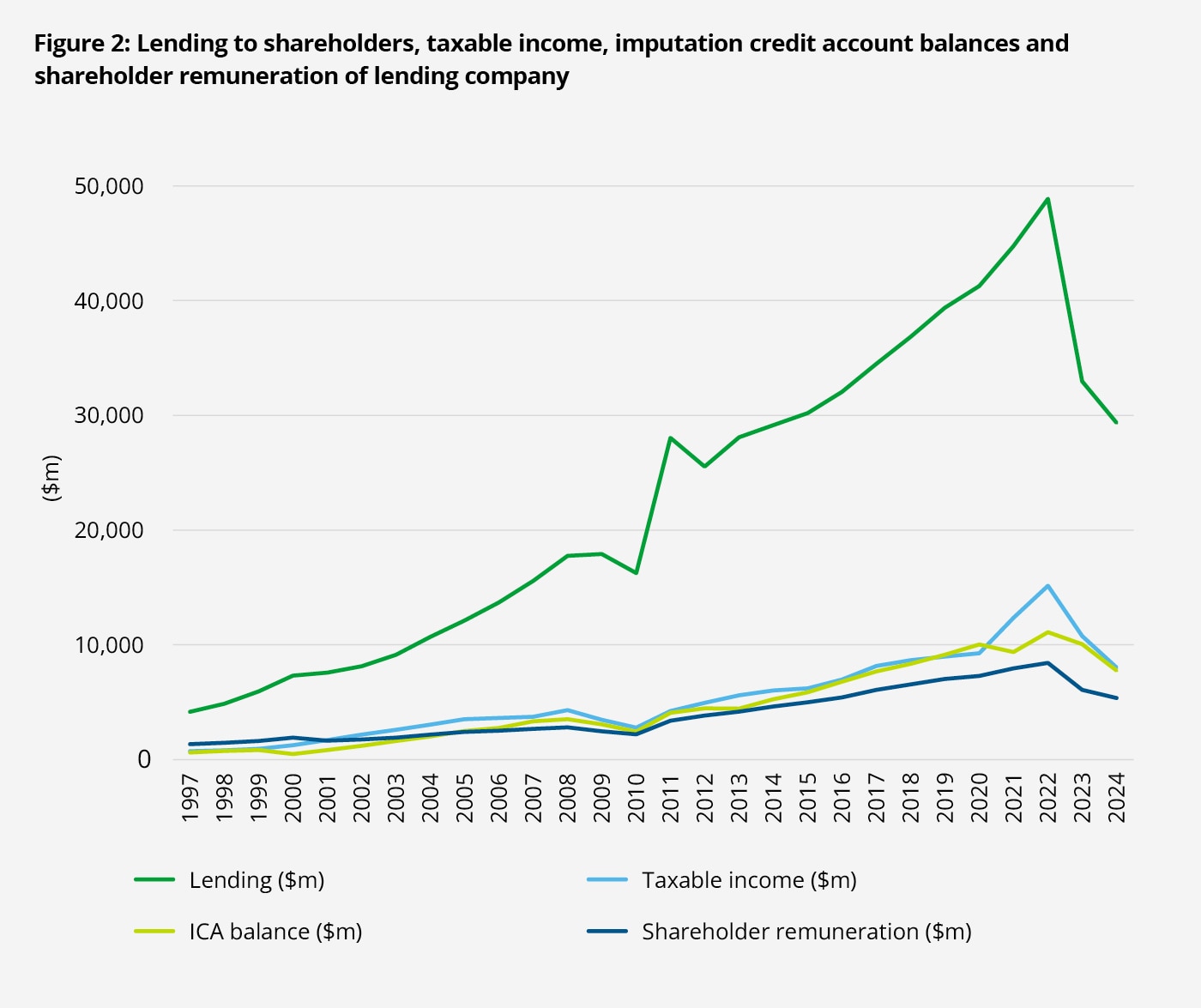

This Paper paints a sober picture of the current state of affairs. Of all the companies registered in New Zealand, 119,000 companies were owed nearly $29 billion by about 165,000 natural person or trustee shareholders. The average loan amount sits at over $245,000 per company.

The concern is not so much that there is shareholder lending, but the quantum of material lending. Of the companies reviewed, 5,500 had loan balances in excess of $1 million, and 540 had balances above $5 million. Many loan balances are going up, indicating that shareholders potentially have an inability to repay the loan and they are not just being used for working capital purposes within an income year.

Source: Improving taxation of loans made by companies to shareholders – Officials’ issues paper

Is the party over?

The Paper makes it clear that there is no issue with shareholder debt (or overdrawn current accounts) per se; however, “Inland Revenue is concerned that the way shareholder loans are taxed, together with the differences in tax rates, means that the current tax system provides an unintended tax advantage when companies lend funds to shareholders, compared with paying taxable dividends,” The Paper goes on to note “We consider that the current tax treatment of shareholder loans results in a less efficient taxation system, lower revenue raised and creates horizontal and vertical inequities. The current rules are unfair to shareholders who receive dividends or salaries, partners, sole traders and employees, who will typically be taxed at a higher marginal tax rate (33% or 39%) at the time they receive the income.” The Paper expresses concern that the current tax rules provide little incentive to repay loans and makes comparisons to Australia, United Kingdom, Canada and Norway, who all have rules of varying severity to address such issues.

In response to these concerns the Paper has three main proposals:

- Treating shareholder loans as dividends if not repaid within set period of time: Inland Revenue propose to treat new loans by a company to a shareholder as a dividend if the loan is not repaid within a set period of time, subject to a de minimis threshold and other exceptions

- Treating outstanding shareholder loans as shareholder income when company removed from Companies Register: Inland Revenue propose that when a company is removed from the Companies Register with an outstanding shareholder loan, the amount of the loan will be treated as income at that time (if not already treated as a dividend by first proposal).

- Improving record-keeping and reporting requirements: Inland Revenue propose new record-keeping and reporting requirements for Available Subscribed Capital and Available Capital Distribution Amount.

The remainder of this article focuses on proposal 1.

Are loans still ‘sweet as’?

When a significant potential law change is announced, it’s necessary for Inland Revenue to think through how to make an announcement without causing bigger issues due to the time lag between the proposal and enacted law. In this case, if progressed, changes to shareholder loans are intended to take effect from the date the consultation document was released, 4 December 2025. The proposals will not apply to loan balances in place prior to this date, unless there is a material change to the loan.

For new shareholder loans, it is proposed that if the loan balance remains outstanding for a certain period, it will be converted into a taxable dividend. Subject to the outcomes of consultation, the likely features will be:

Application to: shareholder loans by New Zealand resident companies to any natural person or trustee shareholders.

Timeframe for loan repayment: the rules will apply if a loan is outstanding following two successive balance dates. This means, subject to when the loan was taken out, that the loan period could be between 12 to 24 months (for example, if a standard balance date taxpayer took out a loan on 31 March 2026, the loan would need to be repaid by 31 March 2027. If a loan were taken out on 1 April 2026 it would need to be repaid by 31 March 2028).

De minimis: the rules wouldn’t apply if total company loan balances are less than $50,000 at the end of any income year. It is estimated than this de minimis will remove about half of all companies from the rule.

Possible exceptions: the Paper raises four areas where exceptions could be considered, with two of them not expected to make the cut: (1) capital gains [officials do not think this should be an exception]; (2) loans on commercial terms with proper documentation [officials do not think this should be an exception]; (3) employee share scheme loans [officials consider an exception would be appropriate]; and (4) loans in the ordinary course of business [officials consider an exception would be appropriate].

Integrity measures: if this proposal goes ahead it’s likely there will be a series of integrity measures to ensure it is not possible to defeat the intention of the rules, for example by repaying and immediately redrawing a loan, temporary repayments, back-to-back loan structures, related party loans and lending to associates.

Implications of a dividend: it will be possible to attach imputation credits to a dividend but any withholding tax implications may fall squarely on the shareholder and not the company. The loan will only be treated as a dividend for tax purposes so will technically continue for other purposes and ultimately require repayment in some way. The need to still repay the loan essentially exists to knock the practice on the head and encourage taxpayers to avoid falling within the rules, as this may technically result in double taxation if the loan is repaid from post-tax income.

Nek minnit

With the potential for rule changes from 4 December, now is the time for businesses with shareholder loans to evaluate the current position and put in plans to ensure loan balances remain manageable. Consultation on the proposals remains open until 5 February 2026. So now is the right time to think around practical issues and to make submissions to ensure any rules work as intended and don't cause unnecessary disruption to vanilla business practices.

For more information or to talk through implications and alternatives approaches to shareholder transactions please get in touch with your usual Deloitte advisor.

December 2025 - Tax Alerts

- Bringing up the rear: final two shortfall penalty guidance documents published

- Employment Leave Act: a new era for leave entitlements in New Zealand

- Future proof your tax governance framework: the Participating Advisor advantage

- Software development and SaaS expenditure under the policy spotlight

- Five-year RDTI review confirms strong business backing and economic impact

- Home office or Business hub?

- Emissions Trading Scheme for non-forestry industries

- Taxing Christmas

- Snapshot of recent developments