Future proof your tax governance framework: the Participating Advisor advantage

Tax Alert - December 2025

By Annamaria Maclean, Vicky Yen and Charlotte Mackenzie

Deloitte has collaborated with Inland Revenue to develop the Participating Advisor program, and since its official launch in April 2025, taxpayers have had great success from the benefits and protections of Participating Advisor reviews for GST, FBT and Payroll. Deloitte is also proud to now also be an approved Participating Advisor for Tax Governance reviews.

Tax governance is no longer a “nice to have”, it is a significant focus area for Inland Revenue and a key consideration in their questionnaires, risk assessment decisions, and audit procedures. If Inland Revenue becomes aware of governance weaknesses, it can lead to a thorough audit and little flexibility regarding penalties.

For taxpayers navigating today’s landscape of increased Inland Revenue scrutiny and expectations for tax governance, a Participating Advisor review provides an assessment of the existing tax control framework to identify gaps and opportunities, while demonstrating a proactive, governance focused mindset. Parameters of the Participating Advisor review have been agreed with Inland Revenue, providing clarity on expectations along with an additional level of protection that Inland Revenue should not separately undertake further testing on governance for a four-year period (provided there are no significant organisational or system changes). The review can also be undertaken in response to/as a defence to further Inland Revenue audit or risk review activity on governance matters. Deloitte, as an approved Participating Advisor, is here to help you move confidently toward best practice and future-proof your Tax Governance strategy.

What does the Tax Governance Participating Advisor review involve?

The Participating Advisor Tax Governance review focuses on testing the existence, design and operating effectiveness of documentation, processes and controls compared to Inland Revenue’s expectations and best practice.

Our review involves a desktop review of your documentation and evidence of controls. This is followed by a workshop to identify additional informal processes or controls which might be in place. We use our Tax Governance assessment model to work through a series of criteria and provide a gap analysis report which includes:

- Our Tax Cube risk heatmap on key aspects of governance per relevant tax type (including general, income tax, indirect tax, employment taxes and international considerations).

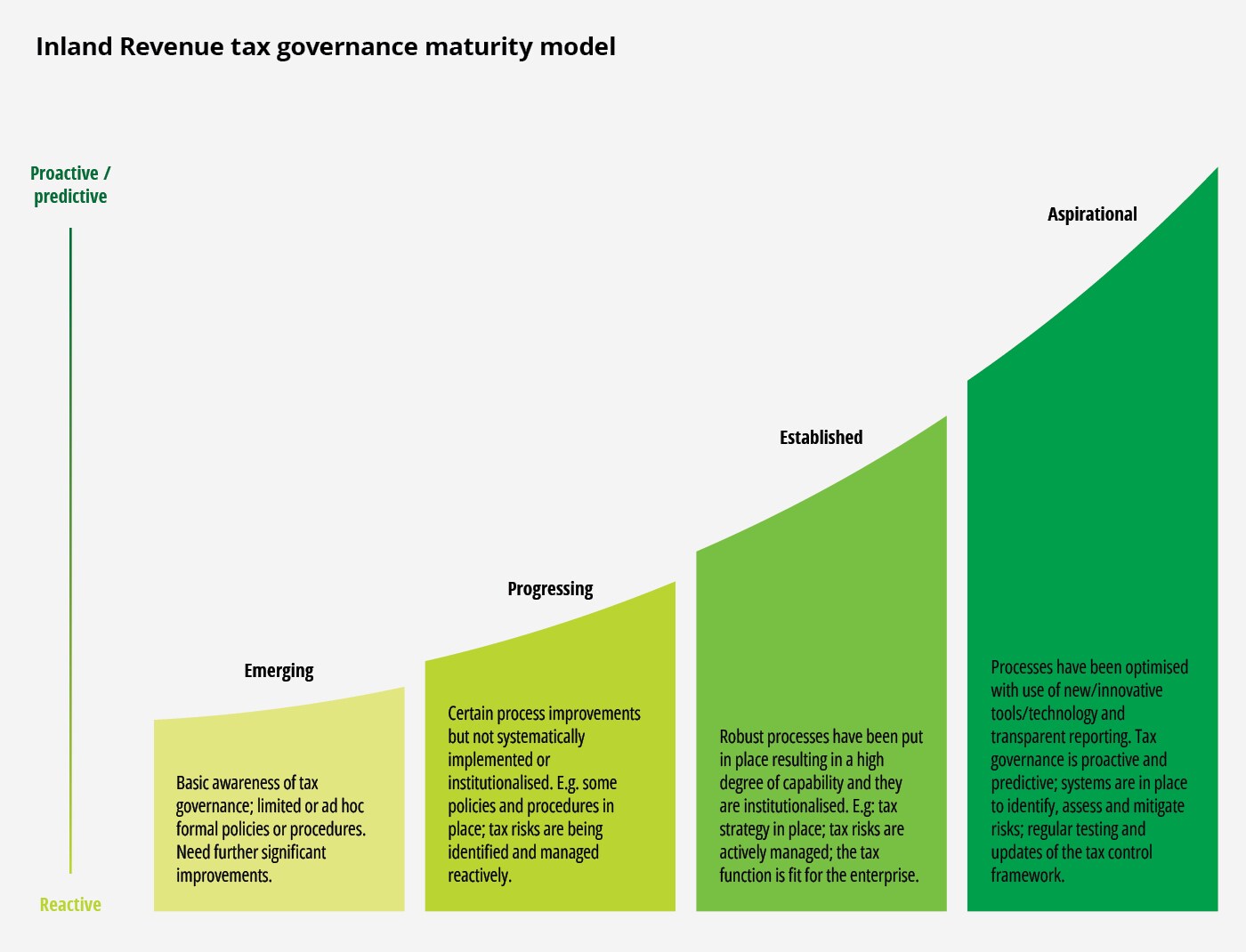

- An indication of where Deloitte believes the taxpayer is on the Inland Revenue tax governance maturity model.

- A summary of the key findings and recommendations (broken down by relevant tax type) to assist in strengthening the tax control framework and progress towards the aspirational and proactive/predictive end of the tax governance maturity model.

Why is tax governance so important?

A robust tax governance and tax control framework is fundamental to supporting compliance. Inland Revenue expects most enterprises to be near the ‘established’ level of their maturity model, with significant or multinational enterprises expected to already be at the ‘established’ level or higher. Our May 2025 Tax Alert article provides an explainer on what the Inland Revenue is looking for.

Taxpayers that receive the Basic Compliance Package (BCP) will see tax governance as a significant focus of the 2026 BCP questionnaire (for the 2025 income year). The BCP applies to New Zealand owned multinationals with a turnover of at least NZD 80 million or foreign owned multinationals with a turnover of at least NZD 30 million, it is intended to be issued to such taxpayers on a three-yearly basis.

The focus of the 2026 BCP questions will be on understanding the current state of tax governance within the New Zealand market and any existing/potential barriers to increasing tax governance. The proposed questions include:

- Whether there have been any significant changes to the Tax Governance control framework within the last three years.

- A self-assessment using the Tax Governance Maturity Model (included above) of which phase best describes the current maturity of the taxpayer.

- An indication of the key challenges taxpayers are facing in improving tax governance maturity.

Where to from here?

BCP questionnaires are released around March each year, giving taxpayers time to get their house in order. Deloitte can assist with conducting the Tax Governance Participating Advisor review to identify the gaps and opportunities within your current tax control framework. This will allow you to focus on improving the key risk areas and progressing through the Inland Revenue Maturity Model.

Please contact your Deloitte advisor to discuss how we can help you on your Tax Governance journey.

December 2025 - Tax Alerts

- Shareholder loans. Yeah, nah

- Bringing up the rear: final two shortfall penalty guidance documents published

- Employment Leave Act: a new era for leave entitlements in New Zealand

- Software development and SaaS expenditure under the policy spotlight

- Five-year RDTI review confirms strong business backing and economic impact

- Home office or Business hub?

- Emissions Trading Scheme for non-forestry industries

- Taxing Christmas

- Snapshot of recent developments