Home office or business hub?

Tax Alert - December 2025

By Jayesh Dahya, Julian Bryant and Ben Tinsley

The global adoption of remote and flexible work arrangements, accelerated by the COVID-19 pandemic, has enabled employees to work from virtually anywhere, including countries outside their employer’s home jurisdiction. While this flexibility offers significant benefits, it also raises important tax considerations for businesses, particularly the risk that an employee’s home office could be deemed a “permanent establishment” (PE) under international tax treaties.

A PE can expose an employer to unexpected corporate tax liabilities and compliance obligations in the foreign country where the employee is based. To mitigate these risks, many organisations have imposed restrictions on the duration or nature of overseas remote work that they will allow the employee to undertake. However, the question of when a home office constitutes a PE has remained a grey area.

The OECD has updated Article 5 of the Model Tax Convention commentary to provide new guidance that introduces a two-part test: a 50% working-time threshold that, if passed, means there will be no permanent establishment based on the time the employee spends remote working in another country, and, if the working time test is not satisfied, a commercial reason test that looks at various factors to assess whether the business has a commercial reason for the employee’s presence in the other country.

This article summarises the key elements of the OECD’s update, illustrates how the rules apply in practice, and outlines steps employers should take to align their remote work policies with the latest guidance.

OECD’s 2025 update: Home Office Permanent Establishment Guidance

- 50% working-time threshold: If an employee works from their home (or another place, e.g., holiday home, the home of a relative or friend etc) in a foreign country for less than 50% of their total working time over any 12-month period, that location will generally not be considered a place of business of the employer. This safe harbour is designed to exclude sporadic or infrequent remote work from PE risk. If an employee is not able to meet this safe harbour then whether employer has a place of business at such a place will be determined by the facts and circumstances.

- “Commercial reason” test: If the employee works from the foreign home office for '50% or more' of their total working time, the arrangement is assessed based on whether there is a business-driven reason for the employee’s presence in that country. If the location provides a commercial advantage to the employer—such as serving local clients, accessing local resources, or enabling business expansion—it may be considered a PE. Conversely, if the arrangement is driven solely by the employee’s personal preference or a general flexible work policy, it is less likely to create a PE.

The OECD Commentary makes it clear that cost savings, such as reducing office rent, or simply accommodating an employee’s preferred place of residence do not, on their own, amount to a commercial reason for establishing business activities in a particular country. Likewise, having some customers or suppliers in the area, or the mere fact that the location is in a different time zone, does not automatically justify a business presence without additional context. For a foreign home office to be considered a PE, there must be a specific, business-driven rationale. Notably, if a company allows remote work solely to attract or retain a particular employee, this alone does not meet the threshold for a commercial reason.

In situations where only small amounts of profit would be attributed, the tests are aiming to limit situations of permanent establishments arising recognising that this creates increased compliance costs for businesses.

Application of the tests

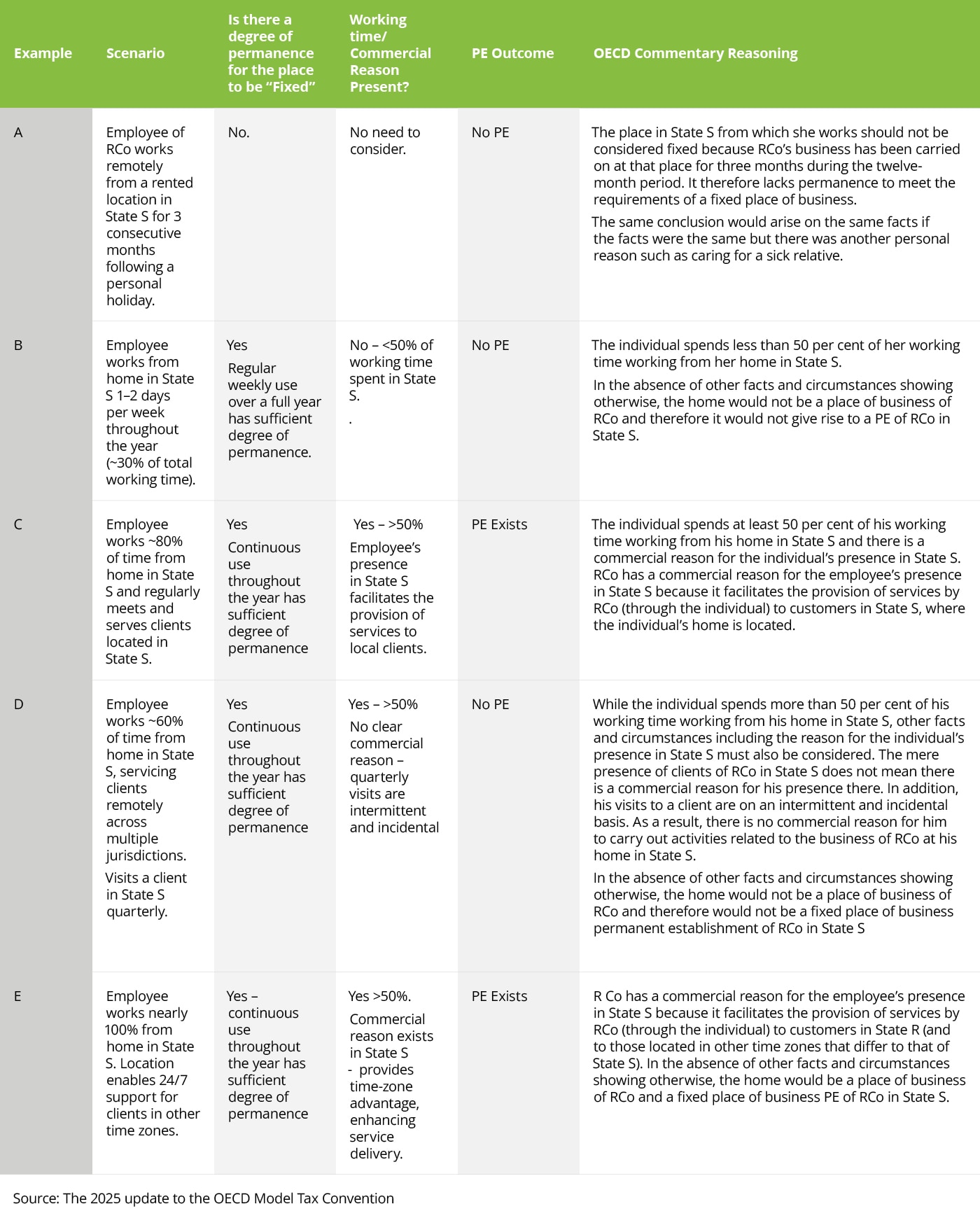

The OECD guidance includes five practical examples to illustrate how these criteria apply. Each example considers a scenario of an employee of “RCo” (resident in State R) working from a location in State S and considers whether that location in State S constitutes a PE for RCo.

The examples and conclusions are summarised in the table below:

Concluding comments

The OECD’s 2025 update provides much-needed clarity for employers managing international remote work arrangements. A home office is not automatically considered a PE; if the arrangement is not driven by business needs, it will generally not be treated as a fixed place of business. However, employers should remember that other aspects of the PE definition, such as the activities of dependent agents, may still apply. Furthermore, not all countries have double tax agreements in place with New Zealand based on the OECD model.

Recommended actions for employers include:

- Reviewing existing arrangements: Assess current home office setups to ensure alignment with the new OECD guidance.

- Updating remote work policies: Consider aligning internal policies with the 50% threshold and develop clear guidelines for handling long-term international remote work requests. Consider implementing systems to track where employees are working and for how long.

- Documenting commercial purpose: When approving an overseas remote work arrangement, document the rationale. If it’s approved to allow for an employee’s personal request or to retain their services (with no intent to expand business in that country), put that on record. Clear and contemporaneous documentation will be useful if you ever need to demonstrate the “commercial reason” for the arrangement.

- Educating and communicating to the teams: Ensure HR, legal, and business teams understand the tax implications of cross-border work and know when to involve tax specialists in decision-making.

As with any remote working arrangements there will be other considerations for the employer to consider that include for example payroll and immigration.

If you have any questions or would like to discuss these changes please contact your Deloitte advisor.

December 2025 - Tax Alerts

- Shareholder loans. Yeah, nah

- Bringing up the rear: final two shortfall penalty guidance documents published

- Employment Leave Act: a new era for leave entitlements in New Zealand

- Future proof your tax governance framework: the Participating Advisor advantage

- Software development and SaaS expenditure under the policy spotlight

- Five-year RDTI review confirms strong business backing and economic impact

- Emissions Trading Scheme for non-forestry industries

- Taxing Christmas

- Snapshot of recent developments