Technology, media, and telecommunications (TMT) enhances ESG reporting to meet new expectations

How many tech executives are prioritizing sustainability

In response to evolving regulations and increasing stakeholder interest surrounding environmental, social, and governance (ESG)-related financial reporting, many public and large private TMT companies are prioritizing enhanced ESG disclosure reporting capabilities to enable regulatory compliance and strategic communications. Explore how TMT executives are thinking about and addressing ESG disclosures in Deloitte's new Sustainability Action Report.

Flipping the script: TMT changes how it views ESG reporting

When many of the ESG rules and regulations affecting TMT companies were being developed and were still voluntary, a common sentiment among many “asset-light” organizations (such as software and media companies) was that their carbon footprint was minimal. At that time, a belief among many companies might have been that, because their direct emissions were seemingly insignificant, the emerging rules and regulations did not significantly affect their business. Rapidly approaching and expanding regulation, coupled with increasing stakeholder interest, may require that TMT companies (regardless of size or emissions) proactively work toward regulatory compliance that considers their global ESG regulatory environment and key stakeholder groups.

In January 2024, we asked 250 executives what they’ve noticed about ESG readiness, assurance, and other strategic initiatives that may lead to a more sustainable future. The result was a collection of responses that indicate a TMT industry that is more prepared for a complex global ESG regulatory environment. Explore detailed insights into the current position of TMT executives regarding ESG reporting readiness, the challenges companies face in the industry, and the impact of sustainability regulations and stakeholder expectations on their climate tracking and reporting practices.

ESG report insights

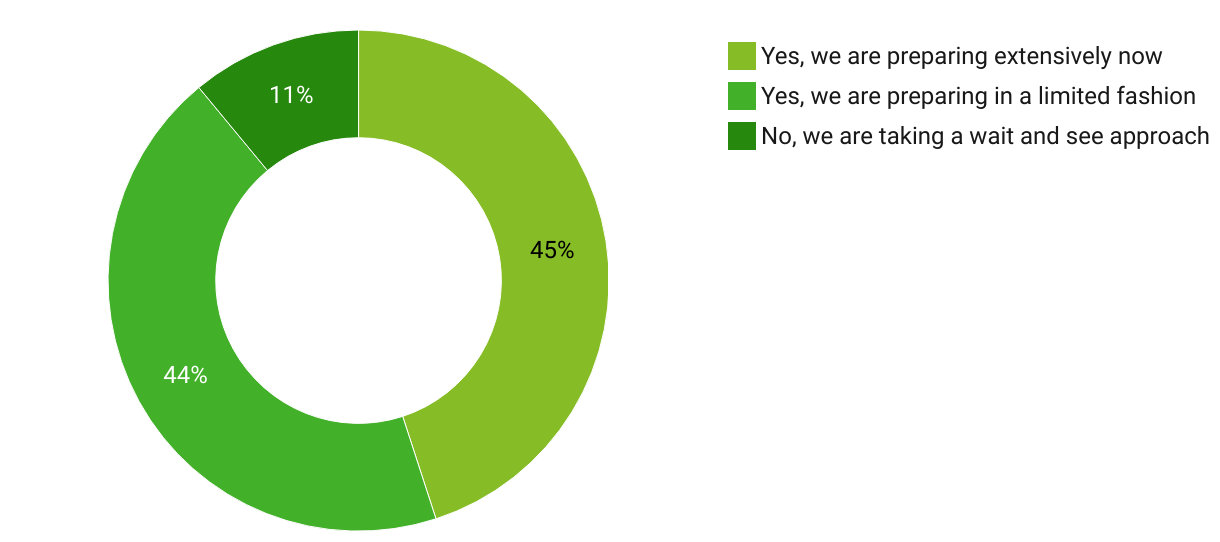

TMT showed progress toward increased ESG regulations readiness

TMT companies are split in how prepared they are for increased ESG regulatory requirements, with 45% reporting they are "preparing extensively", and 44% reporting they are "preparing in a limited fashion".

Figure 1. Are TMT companies actively preparing for evolving ESG requirements?

When asked how they're preparing for ESG requirements, 89% of respondents shared they are taking steps to prepare for the fast-approaching and ever-expanding ESG regulatory and disclosure requirements. While the US Securities and Exchange Commission's (SEC) final climate rule was issued March 6, 2024 (which has since been stayed)1, it's worth noting that a large part of what the SEC's final climate rule encompasses is similar to disclosures already present in other regulations and standards, which are likely driving many companies' readiness efforts. If companies focus on compliance with regulations like those set by the Corporate Sustainability Reporting Directive (CSRD), the California climate rules, or a jurisdiction that plans to adopt the International Sustainability Standards Board (ISSB) standards as a regulation, it's likely that they will, in turn, cover a significant portion of what's outlined by the SEC's requirements. This underscores the fact that the SEC's final climate rule is typically only one part of a company's broader ESG regulatory environment.

Some companies should carefully consider what is required by the SEC's final climate rule even if it means taking a step back, identifying data that is subject to reporting, and planning accordingly. However, they should not be bound only by its timeline when working toward their ESG goals but should also consider other applicable requirements.

Some TMT companies work to meet expanding ESG interest

About 38% of TMT companies have already established a cross-functional ESG council or working group, while 47% are in the process of doing so.

Figure 2. Companies with established or in-progress ESG councils

*The 1% illustrated here was added due to rounding to 100%

Data from our TMT ESG report shows that 85% of surveyed companies have made some amount of progress when it comes to establishing a cross-functional ESG council and are most likely to prepare for various rules, regulations, and stakeholders.

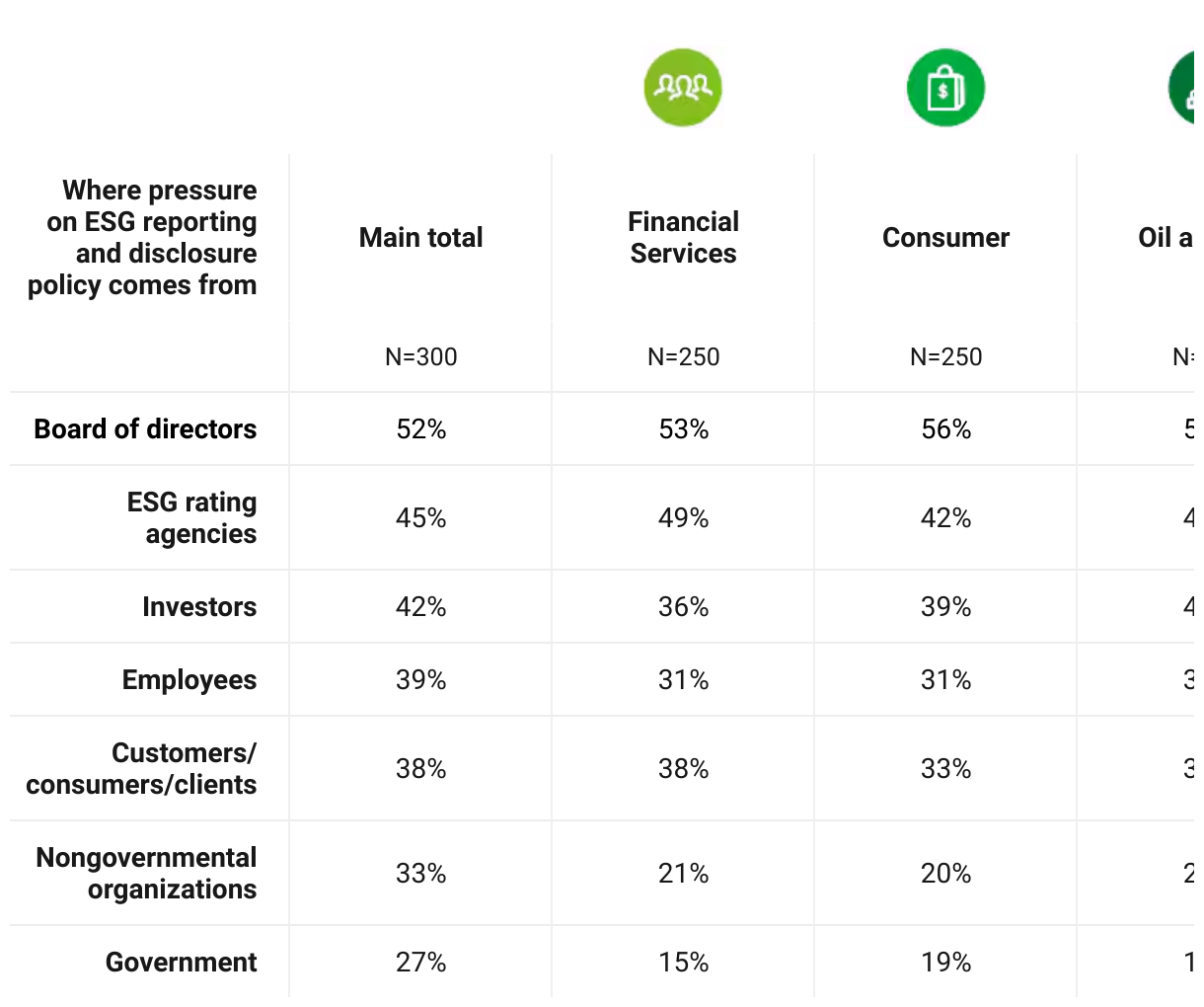

TMT company respondents report feeling pressure from consumers (40%), from nongovernmental organizations (NGOs) (30%), and from governments and their new regulations (25%). In addition to climate-related disclosures, the increased pressure might also be due to data privacy and concerns in the supply chain (e.g., labor rights pertaining to workers in various stages of the supply chain potentially facing low wages and excessive working hours).i Furthermore, in our experience, TMT companies typically handle vast amounts of personal data, and consumers expect them to protect this data from breaches. With the advancements in technology, consumers also have increasingly high expectations for seamless, innovative, and personalized experiences.

Figure 3. Sources of ESG reporting and disclosure policy pressure

*Each industry oversample surveyed a mix of public and private companies, with a minimum of at least 100 publicly owned companies. Which stakeholders do you feel the most pressure from regarding your organization's ESG reporting and disclosure policy?

While ESG regulatory and other disclosure requirements might be expanding, this data shows that expectations are not just being set by the regulators who establish them, but also by the consumers of TMT products, as well as affected NGOs, among others. More parties interested in ESG-related information can mean a heightened importance placed on the data and the potential need for teams dedicated to helping analyze, collect, and report it.

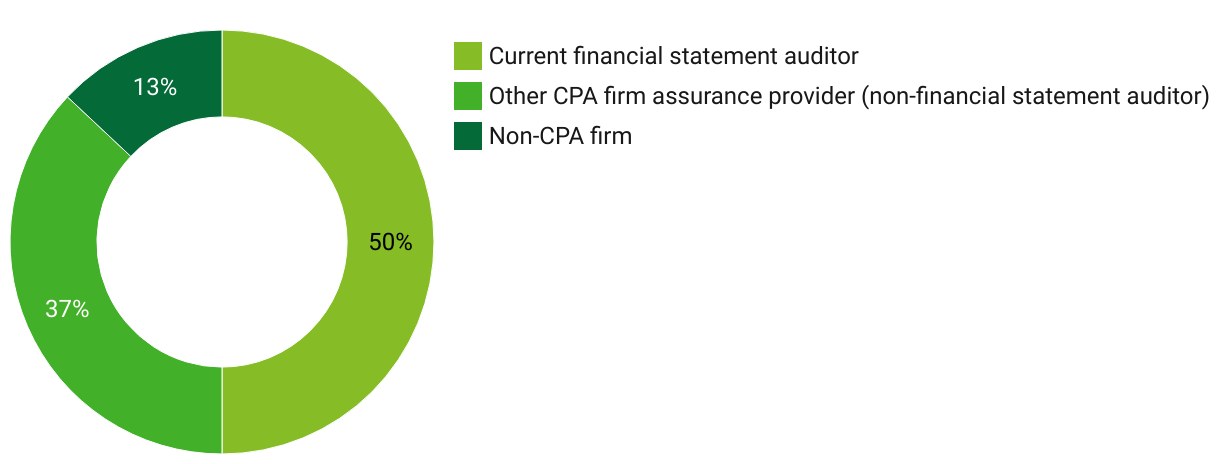

Some TMT companies are proactive about external assurance

Half of TMT companies surveyed have their current financial statement auditor perform external assurance over certain specific aspects of ESG reporting, while more than a third use other certified public accountant (CPA) firm assurance providers to perform assurance over ESG reporting.

Figure 4. ESG reporting assurance provider at TMT companies

Historically, assurance for TMT companies has been largely voluntary. But an evolving regulatory environment with assurance requirements (and growing interest from various stakeholders) suggests that assurance providers proactively engage on matters of ESG reporting.

The establishment of a robust global regulatory reporting framework largely depends on having a third party present to provide assurance as needed.

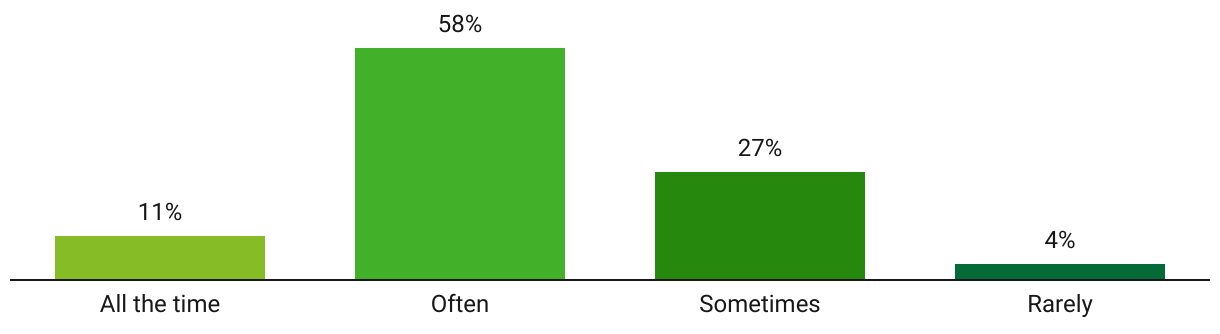

RFP requirements for GHG (greenhouse gas) reports drive TMT priorities

Nearly seven in 10 TMT companies (69%) report that their customers often—or always—request that they report GHG emissions as a requirement to respond to a request for proposal (RFP) or to do business.

Figure 5. Number of TMT companies required to disclose GHG emissions in RFPs or to do business

ESG reporting transparency isn't just about adhering to rising regulatory requirements. Nor is it just about addressing growing investor interest. Now, customers (particularly those who serve mostly multinational or Fortune 500 companies) are increasingly demanding this data as a prerequisite for RFP submission. Consequently, focusing on a global regulatory framework can imply a business impact beyond mere regulatory compliance. ESG data is often evolving into a business imperative that can be important for continued operations, growth, and resilience. Therefore, it's suggested for TMT companies to recognize and elevate its importance.

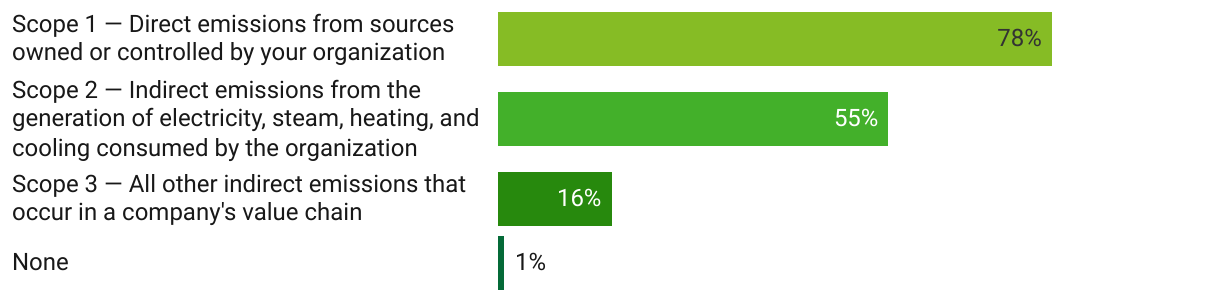

TMT GHG (Greenhouse Gas) emissions disclosures are driven by Scope 1 and Scope 2

Scope 1 emissions (direct emissions from sources owned and controlled by a company) and Scope 2 emissions (indirect emissions released from purchased energy) are important to disclose for most companies. And while the SEC's March 6 ruling excludes a direct requirement for all companies to disclose Scope 3 emissions (all other indirect emissions that are outside of the organization's control) from its reporting requirements, increasingly stakeholders and reporting bodies may expect them to be reflected on their climate-related reports. Compared to other industries surveyed, the TMT industry has the most companies that currently prepare and disclose Scope 1 emissions (78%). Another 55% prepare and disclose Scope 2 emissions. Just 16% prepare and report Scope 3 emissions.

Figure 6. GHG emissions reporting currently prepared and disclosed by TMT companies

For many TMT companies, determining materiality when disclosing GHG emissions may be a challenge, particularly for those that do not have a large physical footprint that produces significant Scope 1 and Scope 2 emissions at scale. Even if Scope 3 emissions are not significant, companies subject to climate regulations set by California, the CSRD, or the ISSB likely need to consider them, regardless of whether it is required by the SEC.

This requirement could catch companies off guard if they do not pay close attention, highlighting the importance of understanding their global ESG requirements and the stakeholders to whom they are accountable. Therefore, it's important to work to integrate this understanding into a global regulatory and voluntary reporting framework. This proactive approach allows companies to be prepared to meet some potential disclosure requirements, thereby potentially minimizing risk and enabling readiness.

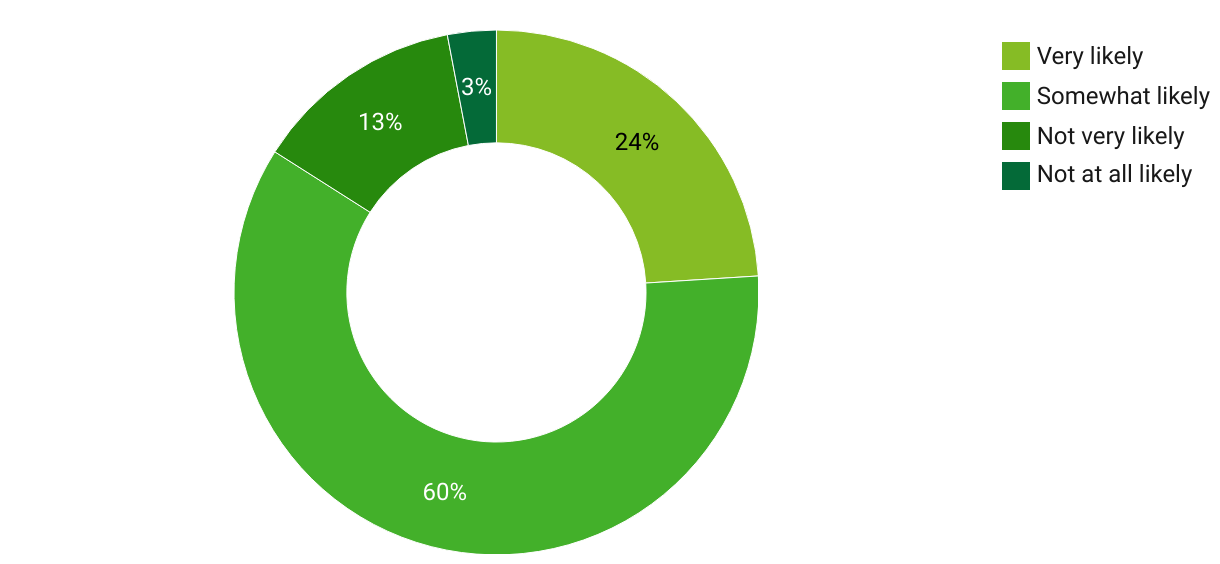

TMT considering new technology to enhance its ESG capabilities

On a scale from “not at all likely” to “very likely,” 60% of TMT companies report being “somewhat likely” to invest in new technology or tools to enable more timely data and high-quality disclosure in the next 12 months.

Figure 7. Likelihood of investment in new reporting technology or tools

As more than half of respondents reported that they plan to invest in new technologies or tools, the expectation is to prepare to see an increased usage in reporting technology that can strengthen internal governance, processes, and controls. While it's an effort that almost always comes with upfront costs, technology is typically at the center of a much larger spend that is centered on enhancing ESG reporting capabilities across people, process, and existing solutions.

In addition, given the assurance requirements that accompany most new ESG reporting regulations, investments in new reporting technology can help with timely and accurate data reporting to allow for compliance with regulations, to increase operational efficiency, and to manage risks more effectively.

Taking a holistic approach to ESG reporting and disclosures

Between ever-expanding regulations and heightened interest from various stakeholders, TMT companies seem to be feeling more pressure to enhance their ESG disclosure reporting capabilities. Despite this mounting pressure, it is important for these companies to avoid a piecemeal approach to regulation. For instance, even though it is important to prepare for the California rule or the SEC’s final climate rule (regardless of the stay), the focus should ideally be on creating a more holistic global regulatory framework and approach—one that can encompass broader ESG regulations and considers key stakeholders such as investors, customers, and suppliers. For example, many companies that determine that the CSRD will apply may use it as a platform to build a broad global reporting framework given the significant amount of disclosure requirements, which are among the broadest of any current regulation. Further, many companies are also looking to use the GHG Protocol (greenhouse gas emissions reporting) and Task Force on Climate-related Financial Disclosures (TCFD) recommendations (e.g., including a climate risk assessment and scenario analysis) as the basis for starting their global reporting framework because the disclosure of a GHG emission inventory and climate risks aligned to TCFD are central to almost all global regulations.

One of the first steps toward achieving compliance with these ESG reporting requirements is typically conducting a comprehensive review of which global ESG reporting regulations apply to a company and over what time frame. Next, it’s important to identify the data needed for compliance and to satisfy interested parties through a data, process, and controls gap assessment. Once a company identifies the data required to be collected, designs the necessary processes and controls, and evaluates the potential technology needs, it should create a strategic implementation plan or roadmap. This roadmap should promote the completeness and accuracy of data collection and governance to enable assurance-ready reporting of required disclosures. Waiting too long to make a strategic plan may impede progress and result in a scramble for resources when a company ultimately decides to act.

Whether your company is looking to understand the global ESG regulatory landscape, assess the impact of regulation on your ESG strategy, or define an implementation plan, find out how our breadth of knowledge, resources, and experience might advise you on your journey. Another suggested first step is a materiality assessment. Contact one of our experienced resources to learn more and get started.

Matt Pelton

Featured resources

Methodology

The Deloitte ESG Survey was conducted by Wakefield Research (www.wakefieldresearch.com) among 300 Executives at publicly owned companies with a minimum annual revenue requirement of $500 million or more. Executives are defined as Senior Finance, Accounting, Sustainability, and Legal Executives with a minimum seniority of director, or Chief Risk Officers, General Counsels, Chief Legal Officers or Chief Sustainability Officer. Oversample interviews were conducted to increase the total sample size to 250 public and private companies in each of the following industries: Life Science and Healthcare; Financial Services; Consumer Products; Technology, Media & Telecommunications; Energy & Utilities. The survey was fielded between January 4th and January 18th, 2024, using an email invitation and an online survey.

Data rounding

Percentages throughout survey may not sum to 100% due to rounding.

Endnote

1 On April 4, 2024, the SEC voluntarily stayed the effective date of the final rule pending judicial review of petitions challenging it, which have been consolidated for review by the US District Court of Appeals for the Eighth Circuit. The SEC stated that it “will continue vigorously defending the [climate rule's] validity in court” but issued the stay to “facilitate the orderly judicial resolution of” challenges presented against the climate rule and to avoid “potential regulatory uncertainty if registrants were to become subject to the [climate rule's] requirements” before the legal challenges were settled. The stay does not reverse or change any of the final rule's requirements nor does it affect the SEC's existing 2010 interpretive release on climate change disclosures. For additional details, read Deloitte's “Comprehensive Analysis of the SEC's Landmark Climate Disclosure Rule.”

iAmanda K. Beggs, Promoting human rights and environmental sustainability: Integrating ethics into the supply chain,” National Law Review, March 26, 2024.

The services described herein are illustrative in nature and are intended to demonstrate our experience and capabilities in these areas; however, due to independence restrictions that may apply to audit clients (including affiliates) of Deloitte & Touche LLP, we may be unable to provide certain services based on individual facts and circumstances.

This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.

As used in this document, Deloitte means Deloitte & Touche LLP, a subsidiary of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of our legal structure. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Copyright © 2024 Deloitte Development LLC. All rights reserved.