The dual mandate redefining the future of tech leadership

Deloitte research shows AI is accelerating expectations for the tech C-suite. The leaders who rise will likely be those who can both go deep on technology and lead the enterprise.

Deloitte’s Global Technology Leadership Study has tracked the steady expansion of tech C-suite roles over the past decade. We’ve watched technology leaders evolve from operational stewards to enterprise strategists, shaping strategy, leading transformation, and driving growth.1

This year’s study, drawing on responses from more than 660 technology leaders globally (see methodology), reinforces that trajectory while revealing an inflection point. As artificial intelligence rises to the top of CEO2 and board priorities,3 technology leaders are increasingly centering their agendas and measures of success around AI, even as their mandate expands beyond it. At the same time, they’re being asked to deliver more while being constrained by the structures they’re meant to transform. The expectation is to embed AI across the enterprise—often within legacy environments and without proportional increases in funding or support—while sustaining everything they already own.4

Despite the pressure, tech leaders are not retreating. More than 7 in 10 respondents to our 2026 survey feel inspired or determined about the future of their role. They recognize that AI introduces complexity but also creates an opportunity to step forward as architects of enterprise advantage.

As AI accelerates expectations, tech leaders may need to fundamentally change how they operate. The future is unlikely to be built on structures and approaches designed for the past. Success increasingly appears to require both deep technical expertise and the ability to drive outcomes across the enterprise—translating technology vision into value5 while maintaining fluency in architecture, AI, cybersecurity, risk, and emerging technologies.6 Enterprise leadership alone may no longer be sufficient, and technical depth is becoming harder to treat as optional. The emerging mandate is both.

The AI lens may be distorting the mandate

Technology leaders are being asked to do more than ever, yet, as this year’s study shows, they’re narrowing their focus around a set of AI-driven initiatives. This creates a disconnect between what the enterprise expects and how technology leaders are delivering.

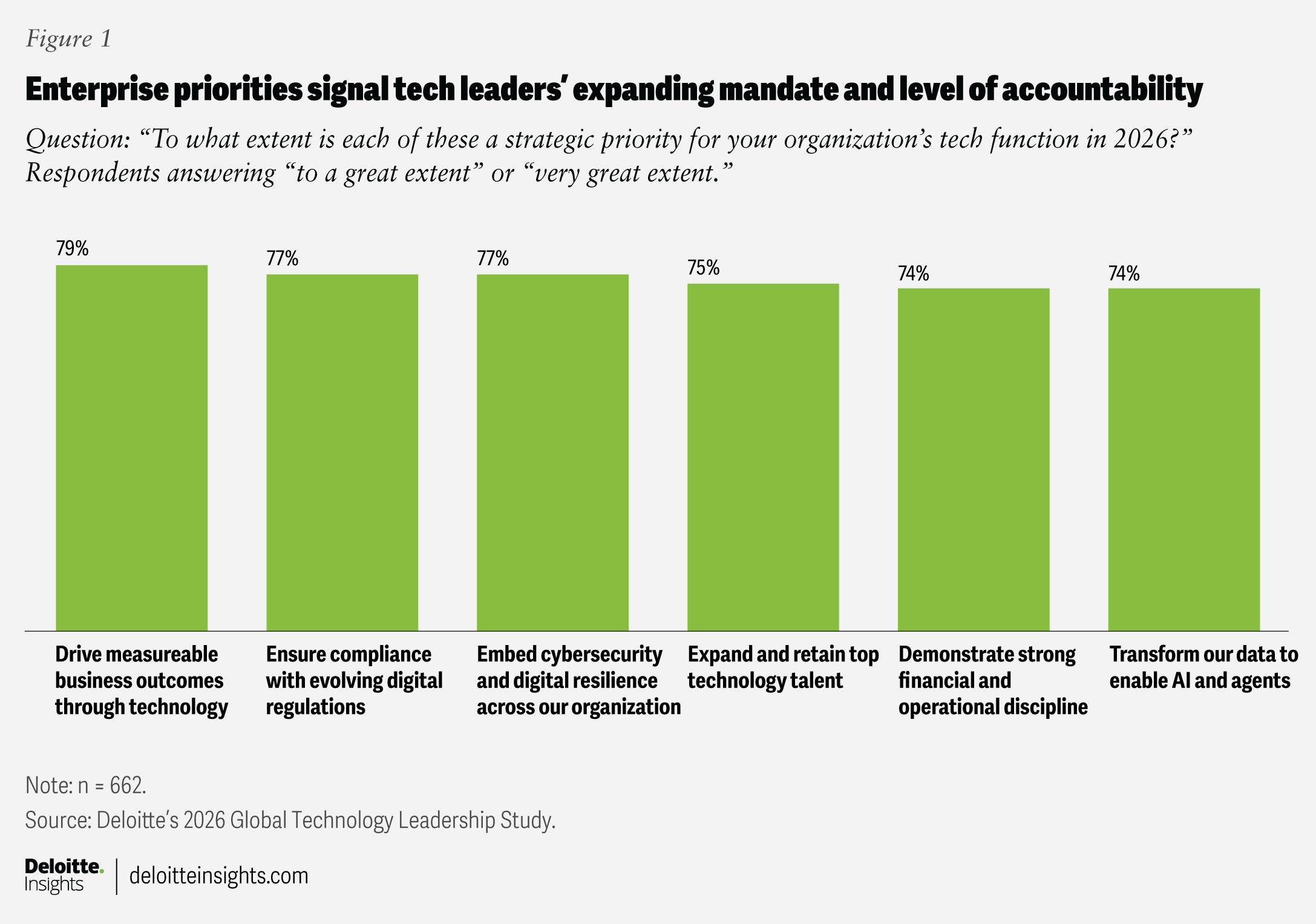

When asked about their top strategic priorities for 2026, technology leaders point to a broad, expanding mandate (figure 1). Delivering measurable business outcomes through technology is the top response, followed by ensuring compliance and strengthening cybersecurity. These priorities reflect a role that extends well beyond technology delivery into enterprise performance.

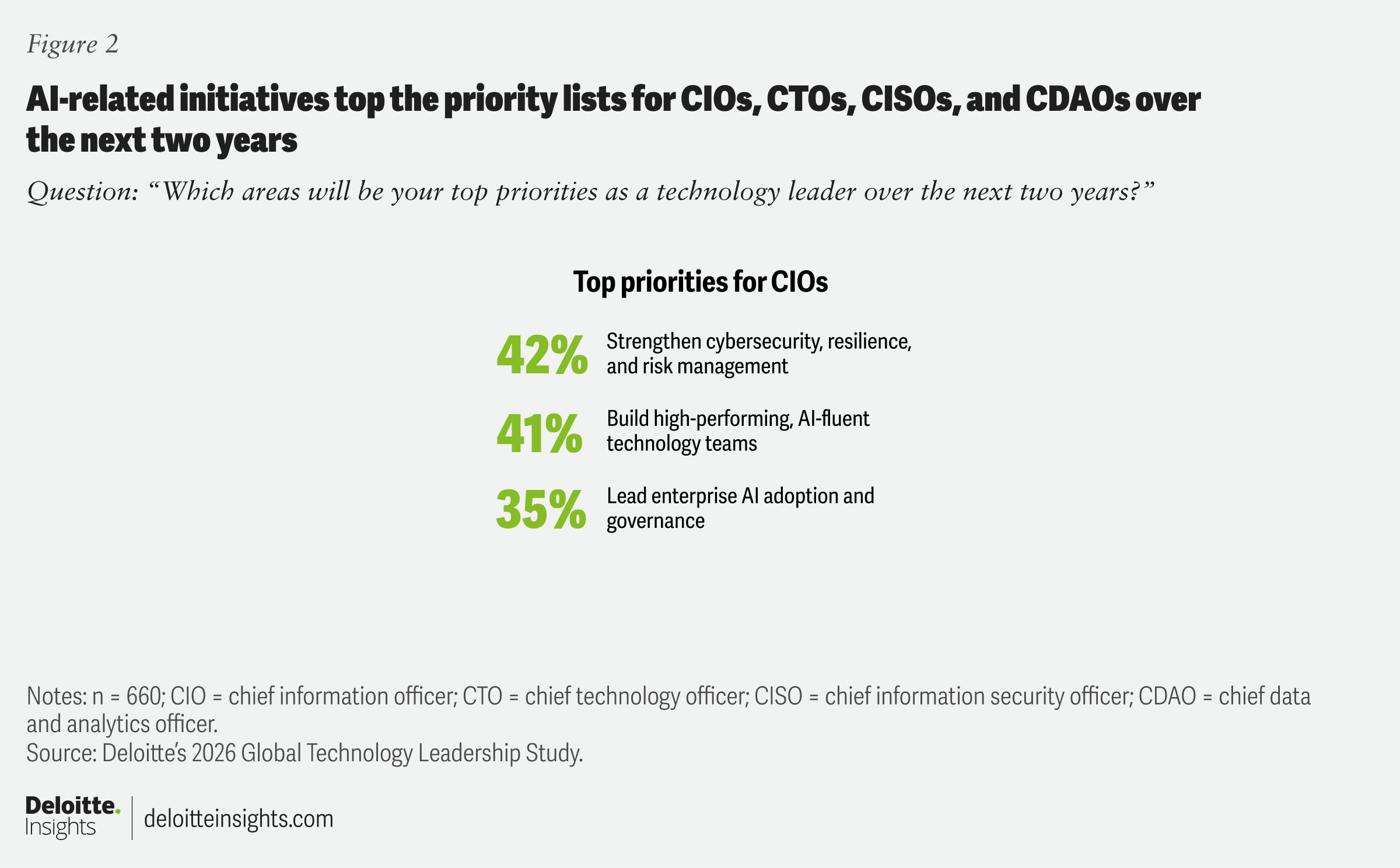

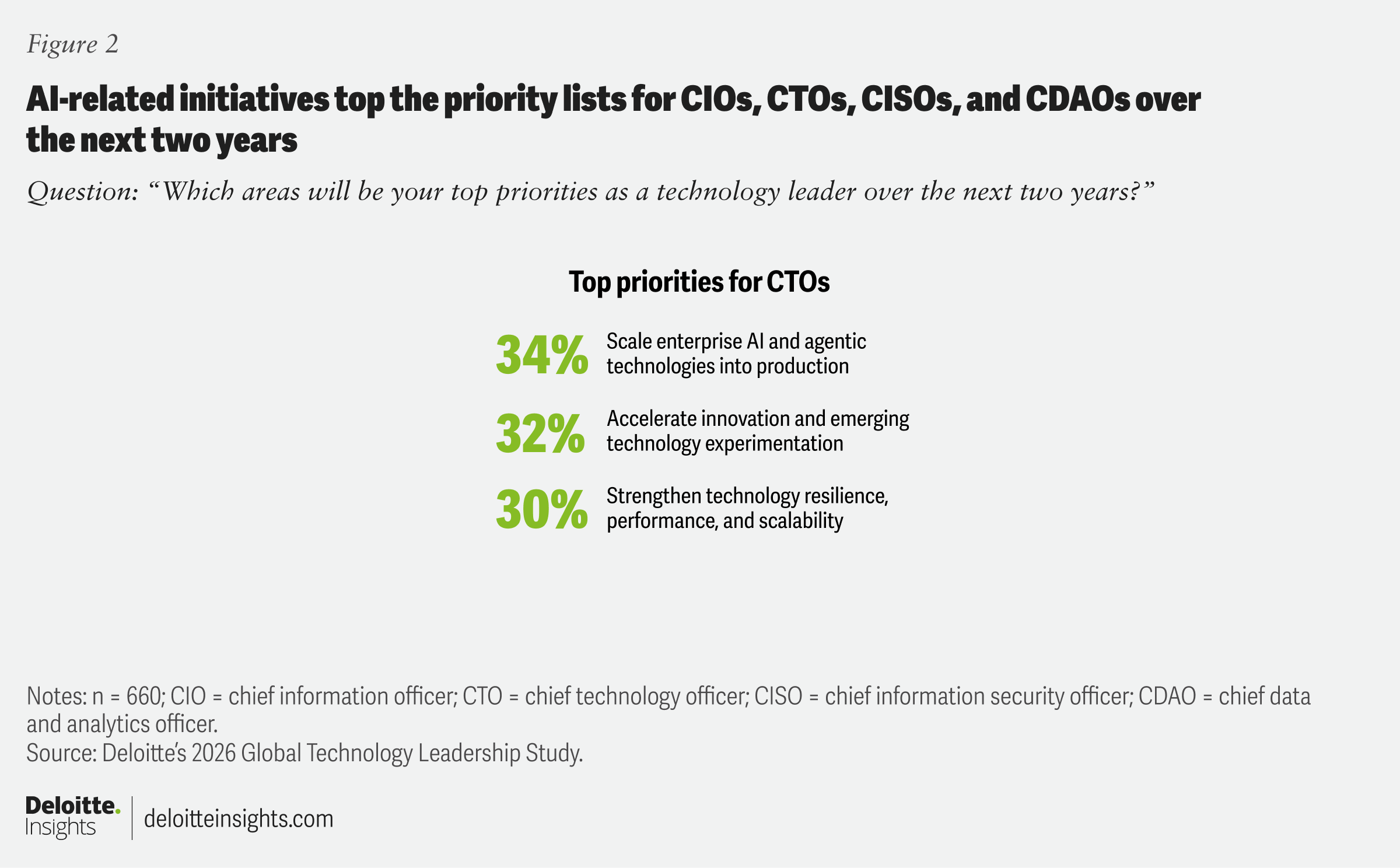

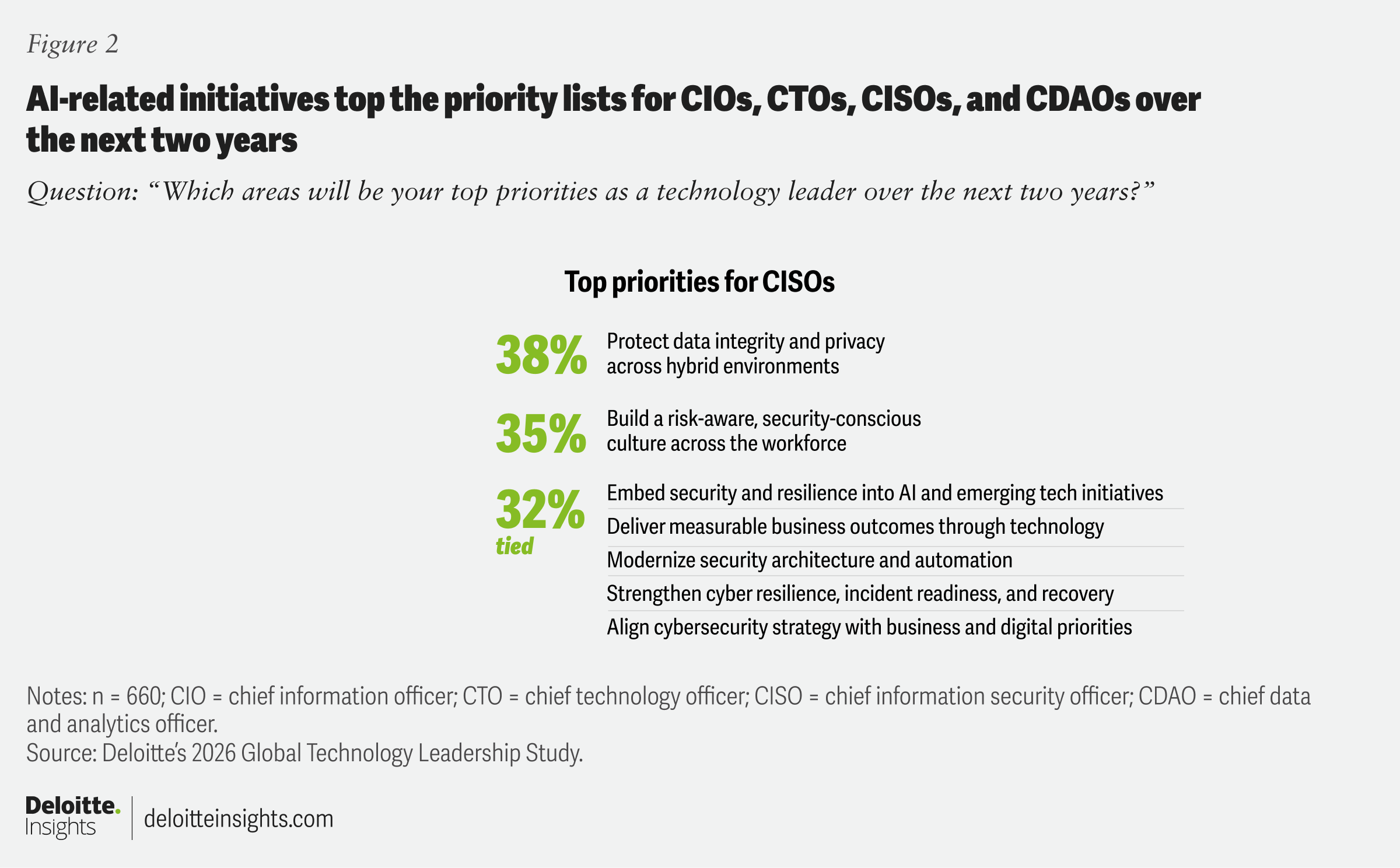

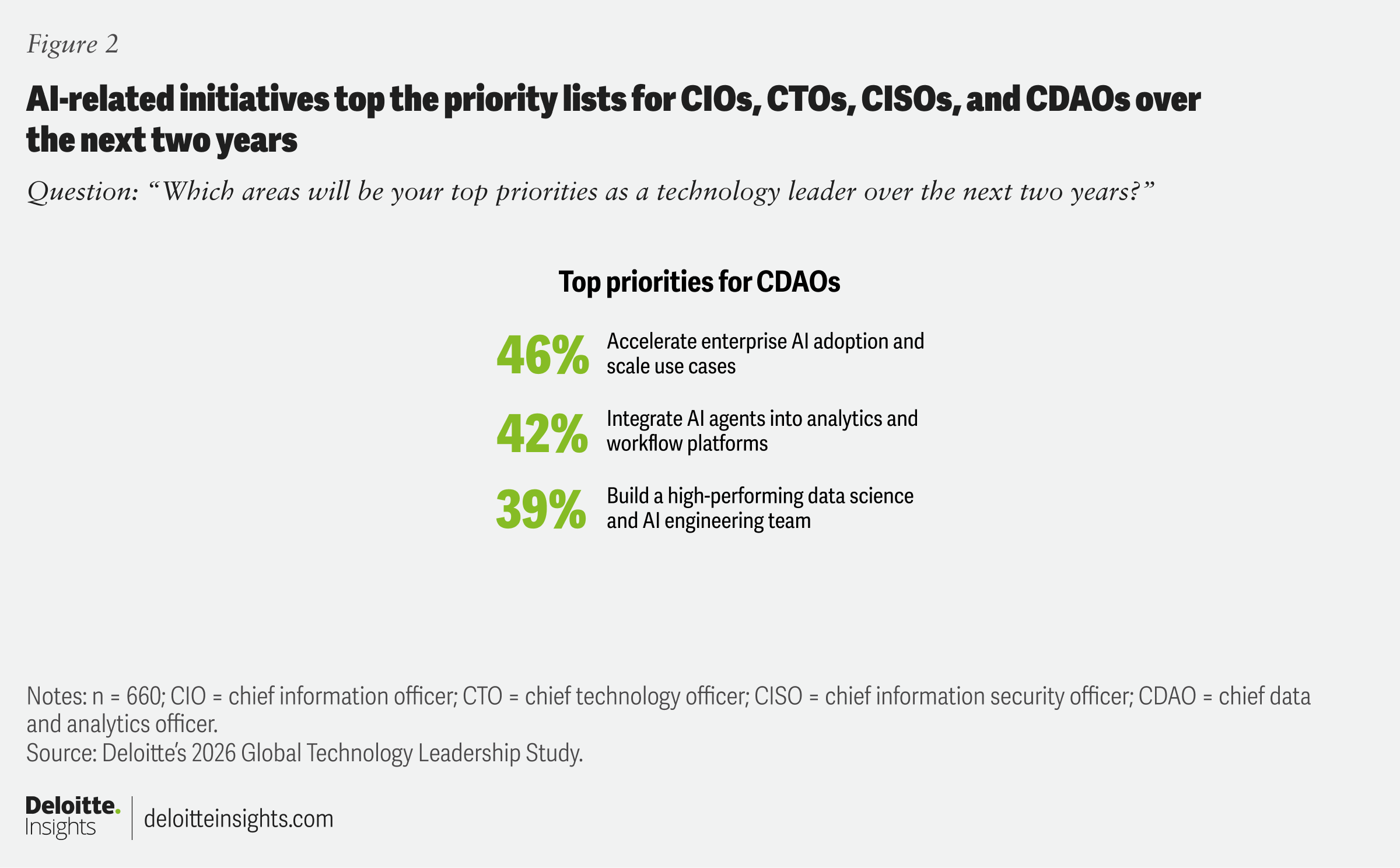

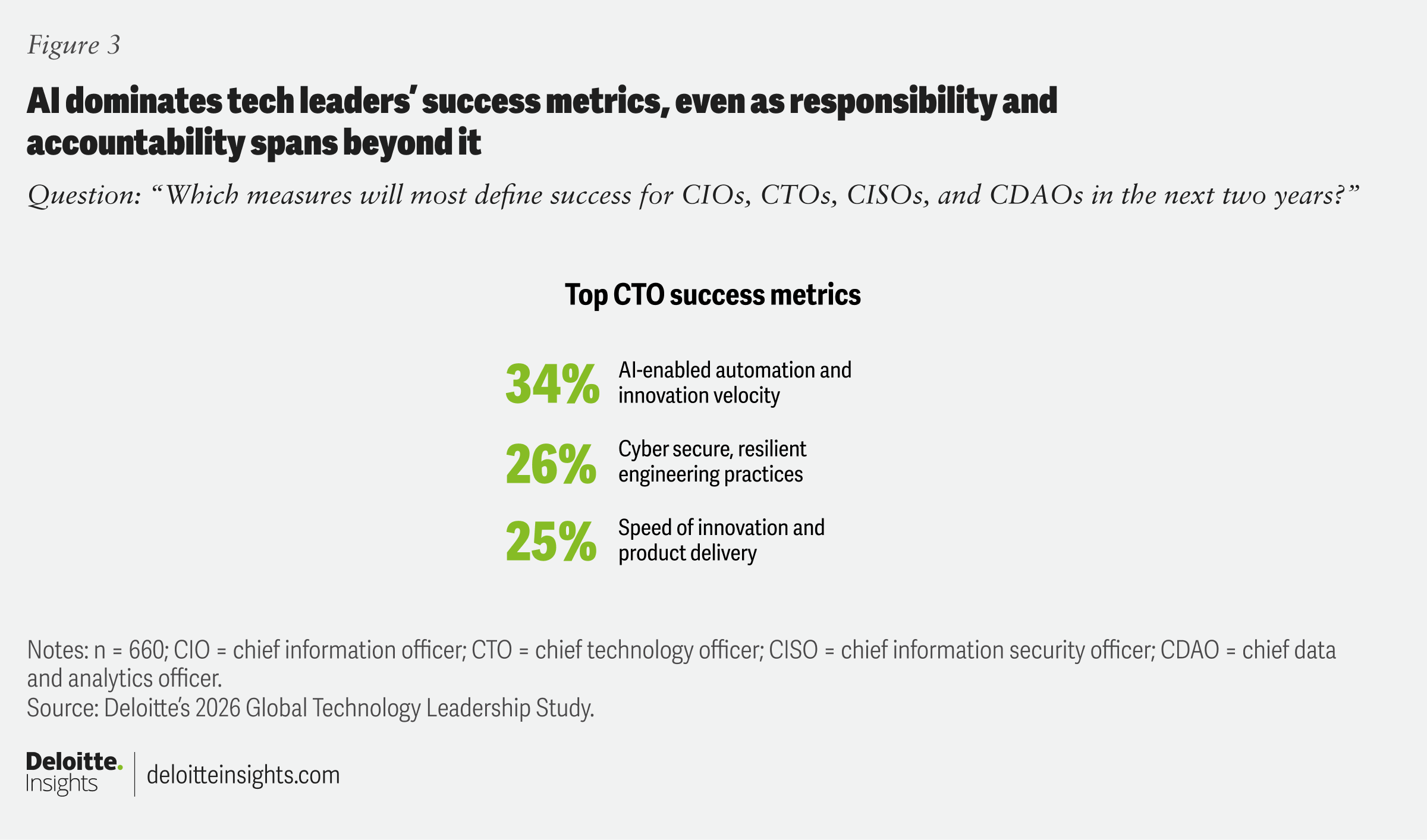

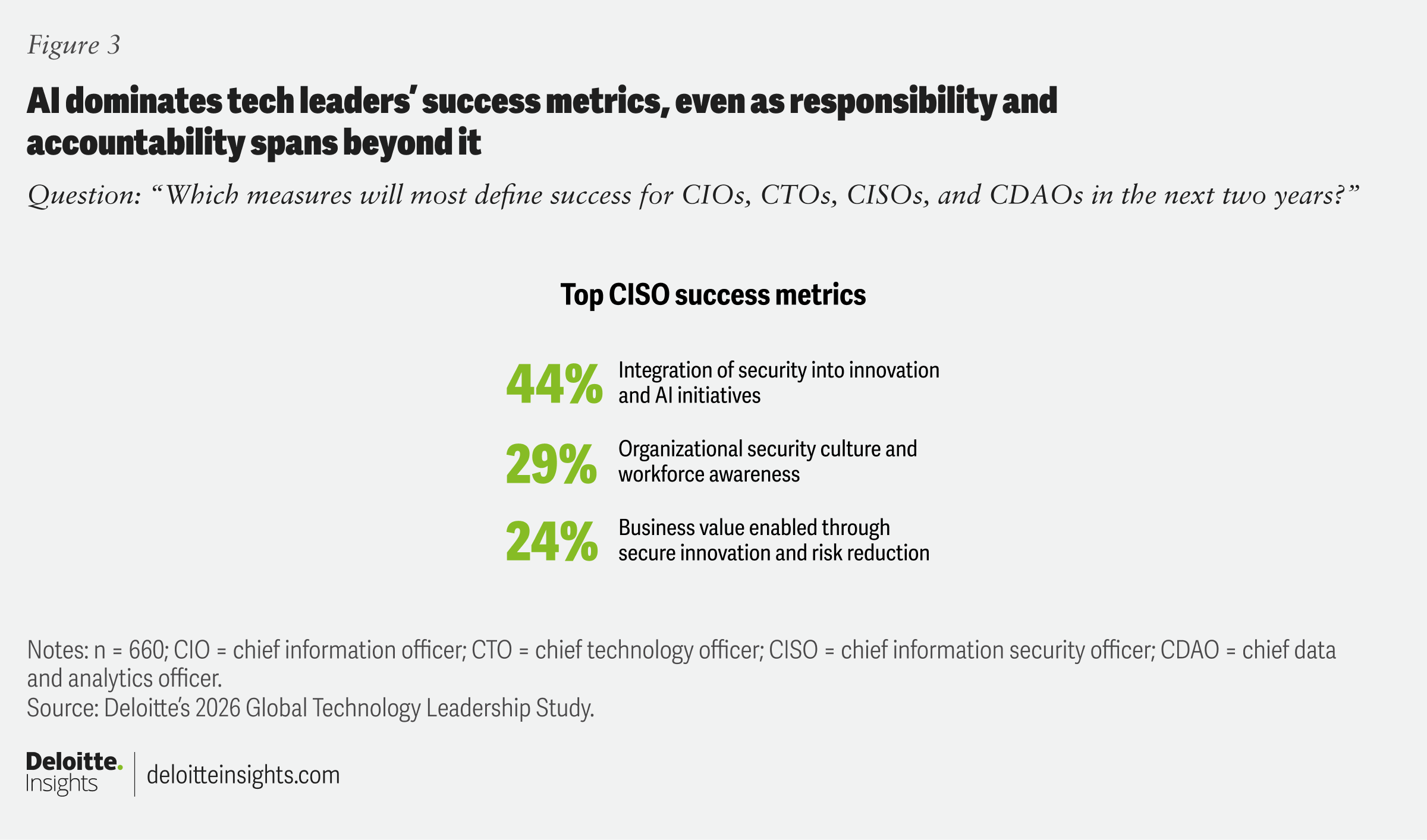

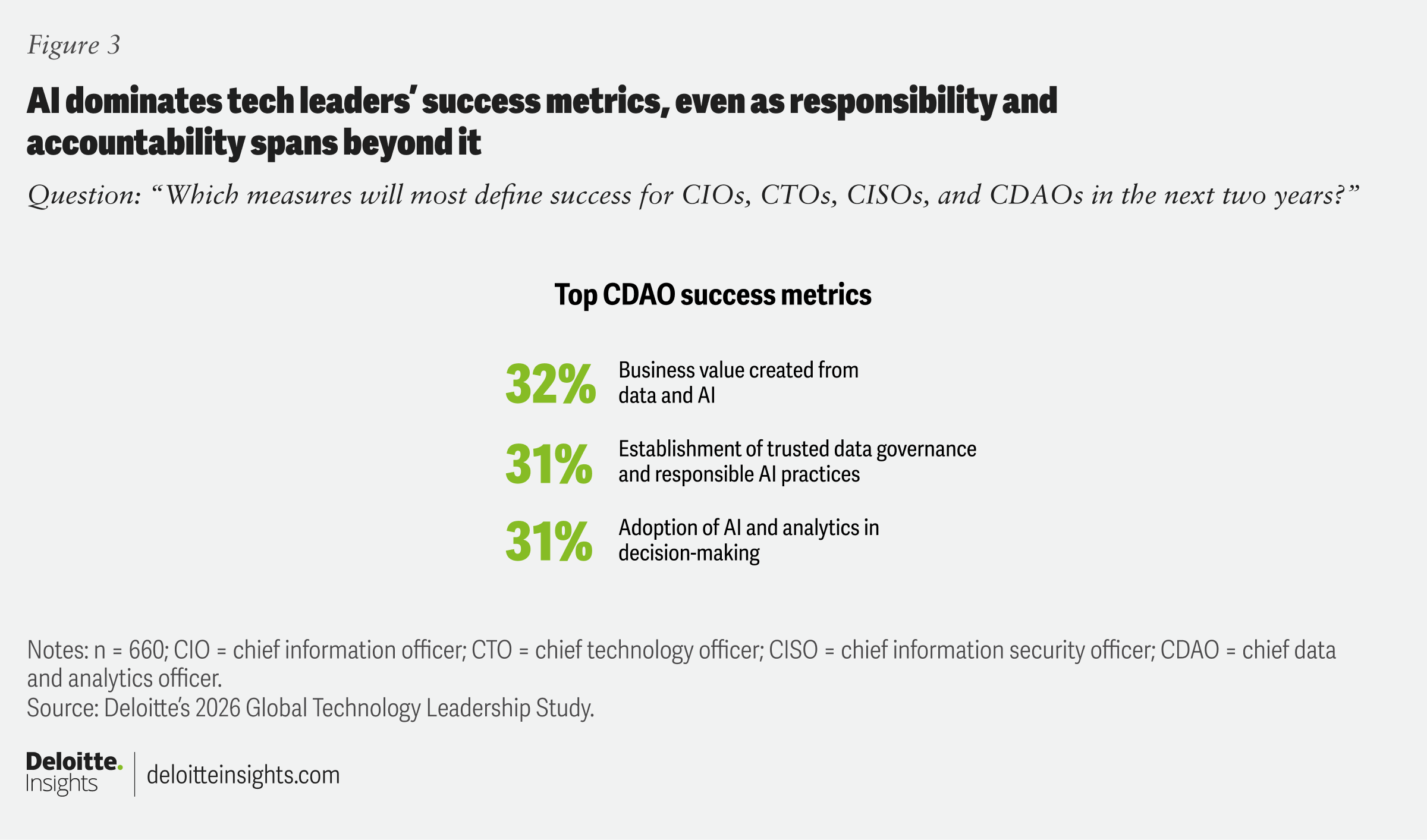

But this breadth is not reflected in how leaders prioritize their agendas. Chief information officers, chief technology officers, chief information security officers, as well as chief data and analytics officers and equivalent roles, consistently anchor their priorities in AI, despite their expanded mandate (figure 2).

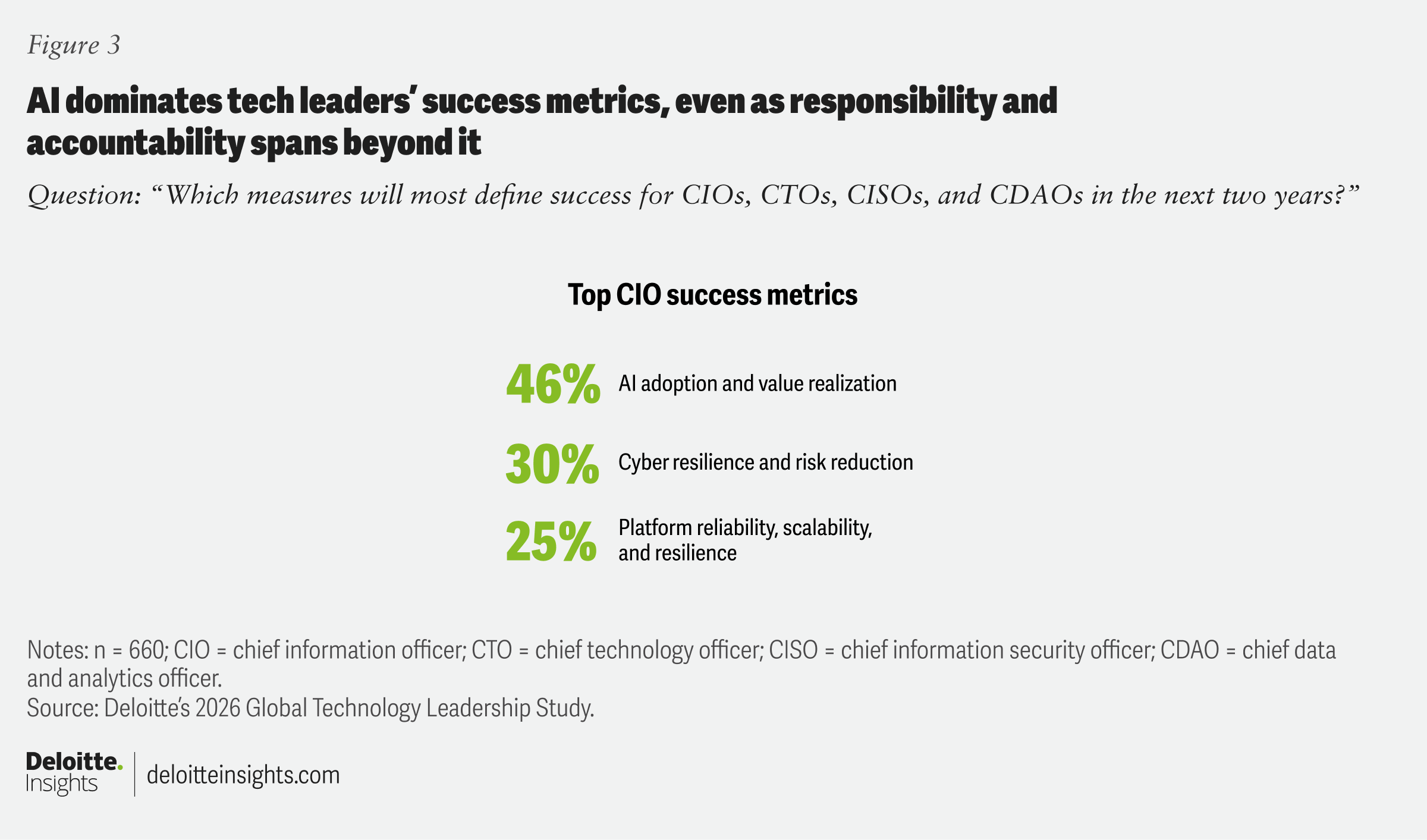

That emphasis becomes even more pronounced when leaders define success. Across roles, AI-linked outcomes rise to the top of performance metrics (figure 3). For CIOs, measurable AI adoption and value realization top the list. CTOs prioritize AI-enabled automation and innovation velocity, while CISOs emphasize security embedded into AI initiatives. For CDAOs, business value created from data and AI tops the list of key performance indicators. In several cases, AI-related measures exceed other criteria by double-digit margins.

In effect, technology leaders are telling us that AI is not simply part of the agenda; it is the primary lens through which they define their success.

This can create a fundamental misalignment. Technology leaders are elevating AI as the focal point of their priorities and perceived success, even as their accountability spans far beyond it. Measurable business outcomes rank as the highest enterprise priority, yet CIOs and CTOs don’t include them in their top three metrics for success. AI may be the dominant lens of self-evaluation, but the mandate is broader. If tech leaders continue to prioritize AI above all else, they may risk allocating too much time, capital, and attention to a narrow set of goals while underdelivering on broader enterprise outcomes—and, in some cases, reinforcing the very fragmentation and inefficiencies AI is meant to solve.

This misalignment doesn’t exist in isolation. It is often reinforced by how organizations are currently structured, funded, and run.

Ambition isn’t the constraint—organizational friction is

Tech ambitions are often moving faster than the enterprise can adapt. Three organizational constraints—structural fragmentation, constrained funding models, and outdated operating models—can limit technology leaders’ ability to translate AI ambition into execution.

Structural fragmentation

An expanding tech C-suite is impacting how decisions are made, aligned, and executed. In our survey, 71% of organizations had five or more C-suite technology leaders, an increase from the previous year.7 For enterprises based in Europe, the Middle East, and Africa, the number is even higher, with respondents reporting an average of six C-suite tech leaders. While nearly all (95%) surveyed organizations have a CIO or equivalent role, many also have CTOs, CISOs, and CDAOs, alongside new roles like chief engineer and chief AI officer.

With an expanding tech C-suite, the challenge is no longer simply driving AI adoption but orchestrating multiple leaders with shared authority and broad enterprise accountability while maintaining coherence under rising scrutiny. If done well, it can be a source of measurable advantage. Recent Deloitte research shows that organizations that fluidly orchestrate people, skills, data, and technologies around business-critical outcomes are about twice as likely as their peers to report better financial results.

Misaligned funding models

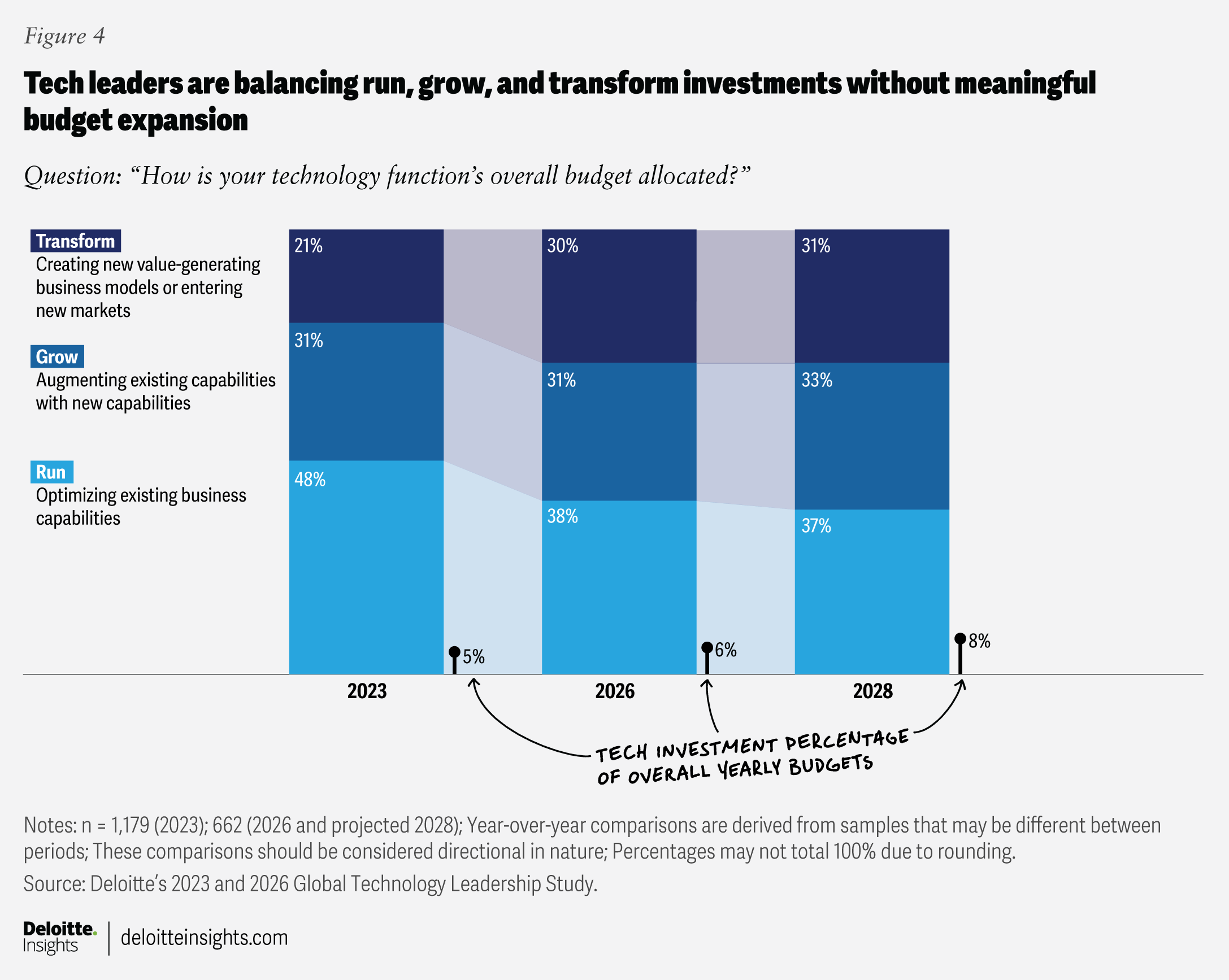

Leaders are being asked to scale AI and drive transformation without a commensurate shift in funding. According to this year’s survey, technology investment represents, on average, approximately 6% of revenue in 2026 and is projected to rise to about 8% over the next two years. Despite AI’s stated importance, 89% of surveyed tech leaders report allocating no more than 25% of their technology budgets to AI initiatives.

At the same time, spending is being spread across competing priorities rather than reallocated to reflect how AI is changing the way tech creates value. In 2023, tech executives reported spending almost half of their tech budget (48%) on “run” activities, 31% on “grow” activities, and just 21% on “transform” efforts.8 In 2026, for the first time, we’re seeing a shift toward a more even distribution of spend across run, grow, and transform initiatives, with that trend expected to continue into 2028 (figure 4).

That means leaders are funding operational stability, growth initiatives, and transformation simultaneously without a corresponding shift in capital. In our 2023 survey, tech spend was also hovering around 6% of revenue.9 The data also suggests AI may often be treated as a net-new investment rather than as a lever to reduce “run” activities and free up both capital and capacity, which represents a missed opportunity.

81% of leaders are confident their current operating model can deploy and govern AI enterprisewide, but 75% also say they must change their operating model within the next 12 to 18 months to drive greater value.

Outdated operating models

While 81% of surveyed leaders say their current operating model can deploy and govern AI enterprisewide, 75% also say their organization must change its operating model within the next 12 to 18 months to drive greater value. This disconnect suggests that while organizations have established models to deploy and govern AI, they are still working through foundational questions around ownership, prioritization, and integration needed to truly capture value.

These dynamics point to a common constraint. Technology leaders are not limited by technological capability but often by the friction created when organizational structures, funding models, and operating approaches are not aligned to support organizational goals. Until that friction is addressed, AI ambition will likely continue to outpace enterprise impact.

Why tech leaders should pair technical depth with enterprise leadership

Technology leaders are clear that delivering on this broadened accountability requires more than technical expertise. When asked which capabilities they most need to develop over the next two years, 44% cited deepening AI and data literacy as their biggest focus area. Close behind are capabilities that extend beyond technical fluency: leading human-AI collaboration, developing next-generation talent, and translating technology vision into enterprise strategy.

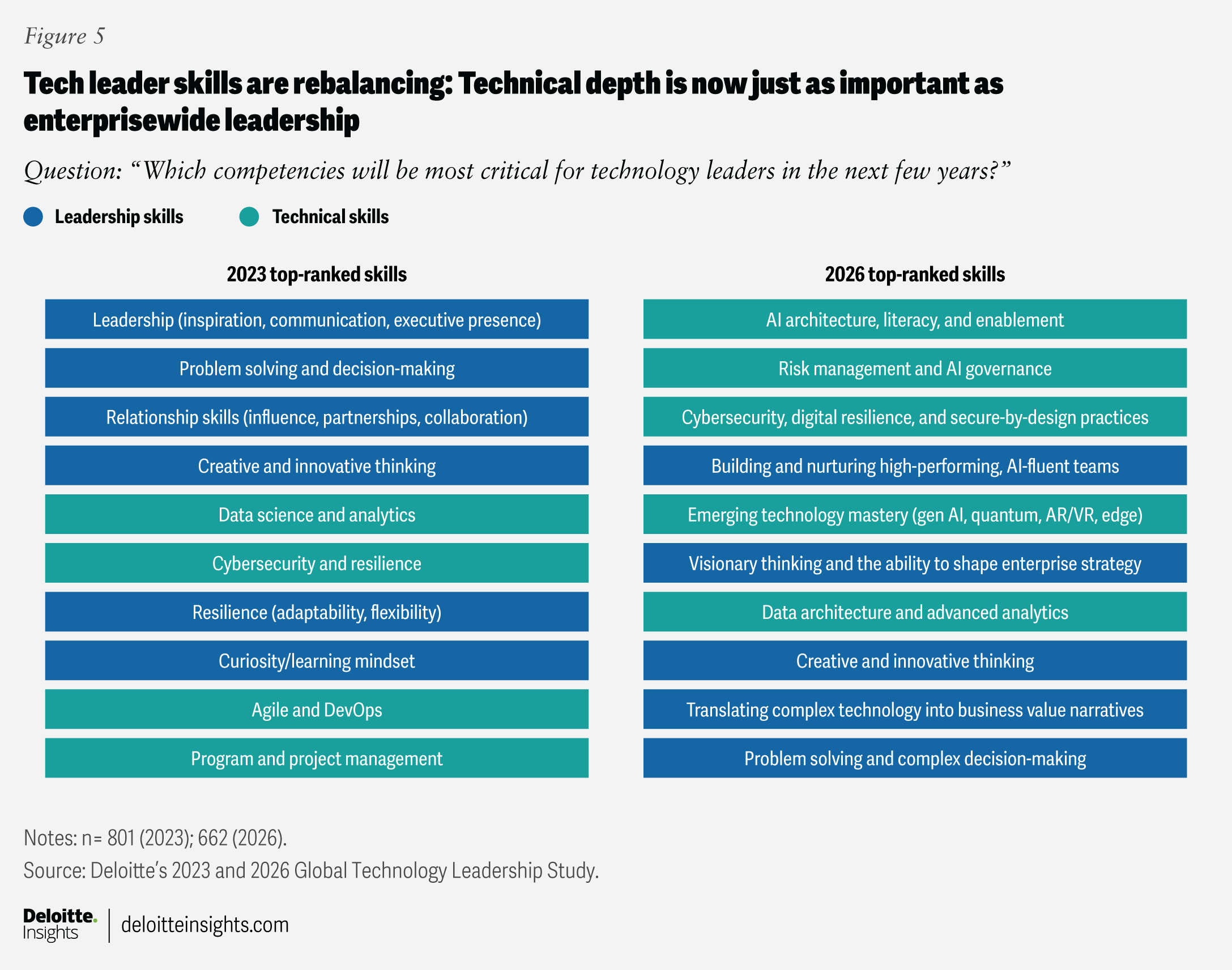

Looking further ahead, respondents view technical and leadership competencies as nearly equal in importance over the next three to five years. AI architecture, governance, and cybersecurity rank high on the list of needed skills, as do building high-performing, AI-fluent teams and the ability to shape enterprise strategy (figure 5). This signals that technology depth should be matched by the ability to lead and orchestrate across the enterprise.

We’ve seen this over the past decade across our Global Technology Leadership Studies, with tech leaders increasingly acknowledging the importance of enterprise leadership, influence, and business alignment as defining attributes of the modern technology leader. In 2023, the importance of “soft” skills was readily apparent.10 This year’s ranking is not a reversal of those needed skills but likely a rebalancing, with technical depth reasserting itself as a critical capability—alongside enterprise leadership, not in place of it.

The next evolution of tech leadership is likely not “either/or,” but “both/and.” Technical depth is—and will remain—a baseline expectation, yet it is likely insufficient to produce sustained enterprise outcomes on its own. This dual expectation is no longer aspirational; it is required. Leaders are now often expected to pair technology judgment with enterprise integration, mobilizing stakeholders, driving adoption, managing trade-offs, and translating technology ambition into measurable business value.

This shift is also driven by the nature of AI itself. As AI becomes embedded across core business processes, it introduces new forms of risk, governance complexity, and enterprise exposure.11 Technology leaders will likely need to operate in much closer alignment with cyber, data, AI, and talent leaders, integrating security, resilience, and governance into how AI is designed, deployed, and scaled.12

Closing the gap between AI ambition and execution

Technology leaders today are not navigating a single transformation. They are managing overlapping shifts in mandate, measurement, governance, and execution all at once. If the past decade was about earning a seat at the table,13 this decade is about using it to reinvent the enterprise.

The leaders who succeed will likely be those who understand AI is not just a technology transformation but an enterprise transformation requiring stronger competencies in areas like value, orchestration, and judgment.

Here’s how tech leaders can meet the moment:

- Anticipate and shape what AI changes next. Look beyond immediate use cases to address second-order impacts on architecture, talent, governance, capital allocation, and risk. Tomorrow’s tech leaders understand AI is not additive, but integrative, and treat AI as a catalyst for continuous enterprise redesign, anticipating how it reshapes the business, not just where it can be deployed.

- Make the hard technology trade-offs. Apply disciplined judgment to translate technology and AI ambition into a focused portfolio with clear value cases, defined risk posture, and explicit time horizons. In a world of incremental budget growth and increased expectations, successful leaders use AI to improve the speed and quality of decisions and then make trade-offs transparent, defend them in enterprise terms, and stop low‑value work to fund what matters most.

- Navigate risk without stalling progress. Advance AI while managing risk, compliance, legal, and security functions that can potentially slow change. Leaders are navigating a risk landscape that’s still taking shape, from regulatory uncertainty and data exposure to third-party dependencies and unintended operational consequences. There’s no clear playbook. Success likely depends on bringing stakeholders along early and balancing the push to move fast and operate responsibly.

- Colead, don’t just collaborate. Orchestrate the entire C-suite (not just the tech chiefs) to drive prioritization, enforce trade-offs, and align around shared business outcomes. AI success is not the mandate of a single role but the accountability of the entire organization. Elevate it to the enterprise agenda by pulling the chief executive officer, chief financial officer, chief human resources officer, chief strategy officer, and other business leaders into active ownership.

- Make AI an enterprise muscle, not an IT project. Embed AI into core platforms, processes, and operating models so it becomes part of how the business runs rather than a series of isolated initiatives. Build repeatable capabilities that scale AI while sustaining operational excellence, cybersecurity, and resilience.

- Show up as a business executive, not just a technologist. Tie technology choices directly to enterprise performance and value creation. Communicate in terms of value, risk, and execution realities, earning the influence required to deliver in an environment driven by multiple voices rather than one.

The next standard for technology leadership likely won’t be defined by tools or platforms but by leaders who can integrate technical depth with enterprise influence and pair AI ambition with operational discipline and strategic clarity. This can be a career-defining moment, and the advantage will likely go to those who step forward to not just implement AI but leverage it to redesign how the entire business operates around it.14

But this responsibility does not (and should not) sit with technology leaders alone. CEOs and executive teams are placing unprecedented expectations on technology leaders while often underestimating the constraints they face, from legacy environments to fragmented operating models and the absence of clear road maps. The pace of change is so rapid that there is no playbook yet for how to move forward.

If AI is an enterprisewide transformation, accountability should be as well.15 Strong CEO leadership can align priorities, drive adoption, and ensure transformation extends beyond the technology to the enterprise itself. It’s not about CEO sponsorship, but CEO ownership. And part of that ownership is viewing, supporting, and elevating technology leaders differently. They are not there just to keep the lights on—they are there to light the way forward.

Methodology

Deloitte’s 2026 Global Technology Leadership Study surveyed 662 senior technology leaders in the Americas (including Latin America); Europe, the Middle East, and Africa; and Asia-Pacific regions to understand how senior technology leadership roles and responsibilities are evolving, as well as the key challenges and strategic priorities shaping 2026 and beyond. Data was collected through an online survey from Dec. 22, 2025 to Feb. 23, 2026.

A majority of the respondents (87%) were C-suite tech leaders. For thematic and role analysis, respondents were grouped into four C-suite personas based on their title, including chief information officers, chief technology officers, chief data and analytics officers, and chief information security officers. Executives represented organizations with annual revenues of US$1 billion or more, including publicly and privately owned companies, as well as not-for-profit and government entities. Primary industries represented include consumer products and services; financial services; technology, media, and telecommunications; energy, resources, and industrials; life sciences and health care; and government and public services.

Continue the conversation

Meet the industry leaders

Anjali Shaikh

Steve Pratt

by

Anjali Shaikh

Steve Pratt

Lou DiLorenzo Jr.

Diana Kearns-Manolatos

Fay Chen

The authors would like to thank Monika Mahto and Erika Maguire for their significant contributions to the development of the article—Maguire for her leadership in shaping and advancing the CIO Program’s thought leadership agenda. Her perspective on how the role is evolving, combined with her unwavering commitment to excellence, was foundational to this work. This report would not have been possible without her leadership, vision, and orchestration throughout. And Mahto, for her strong partnership and collaboration in bringing this work to life. Her ability to mobilize the Center for Integrated Research and contribute both rigor and momentum was instrumental to the development and delivery of this article.

We would also like to thank Subodh Chitre, Michael Caplan, Tarun Sharma, and Michael Wilson, as well as Deloitte’s CIO Advisory Council, for their leadership and guidance in the development of the storyline.

We extend our appreciation to Ayush Kumar and Abha Kulkarni for their support in data analysis, and to Angelle Peterson for her involvement in the insights development, as well as to the marketing team, Jennifer Rood, Saurabh Rijhwani, Jenn Popovic, and Pratyusha Peddasomayajula for their support in amplifying these insights.

Editorial (including production and copyediting): Corrie Commisso, Annalyn Kurtz, Shyamili M, and Anu Augustine

Design: Sonya Vasilieff and Molly Piersol

Audience development: Pooja Boopathy

Cover image by: Sonya Vasilieff

Knowledge services: Rishitha Bichapogu

Visit the Deloitte Center for Integrated Research

Access more insights on some of the most complex issues facing businesses today.