Five leadership and teaming choices that can help drive increased value

Deloitte’s analysis of survey data from more than 400 US business and tech leaders finds that reporting structure, digital ownership, and team capabilities can strongly influence achieved value

Successful technology transformation is not a game of chance. As Ranjit Bawa, Deloitte’s US chief strategy and technology officer, puts it, “Organizations that realize the most value are those making strategic choices with a future-ready enterprise in mind. As we enter a world increasingly shaped by AI and bold business reimagination, the path to success depends on the actions leaders take today. When decisions are driven from the center and integrated into daily activity across the organization, transformation becomes a mechanism for ongoing reinvention—not a one-time effort.”

To learn which of these actions can drive the most value, Deloitte surveyed around 400 US business leaders from September 2024 to January 2025 across eight sectors to assess their digital transformation investments and priorities. This analysis focuses specifically on five key operating choices: digital primary ownership, reporting structure, organizational models, how organizations close digital gaps, and team capabilities. It also asked respondents the extent to which they achieved the “expected value” from those digital initiatives (see methodology).

These choices were analyzed through the prism of Deloitte’s five-level digital transformation framework, in which each level represents a unique digital vision or ambition. Each successive level becomes more focused on external customers and is more transformative in scope: Levels 0 (incremental digitization) and 1 (advanced digitization) reflect internally focused, data-centric, or “digitization” business cases. Levels 2 (using digital to enter new markets), 3 (using digital to create new products), and 4 (radical transformation1) reflect comprehensive and customer-focused digitally enabled transformation ambitions.

As leaders look to act, achieving their digital ambition depends on their specific operating choices, which can be a function of an array of factors both within and outside their sphere of influence. Ultimately, organizations may be able to enhance the value achieved from digital programs by making even marginal changes to their operating models.

Success may be a choice, or rather many choices

While the choices leaders make may drive value overall, no single operating choice is likely to assure success. But a few things are worth keeping in mind:

It generally starts with people and the roles they play. Many C-suite executives may own the data, but when the digital primary owner reports to the CEO, the results may be better. However, when the CEO (or any other “business-related” role) serves as the digital primary owner, achieved value percentages for digital programs may be lower, regardless of digital ambition. Consider casting roles carefully, both for digital primary owner and the ultimate digital initiative authority, and reevaluate roles in your digital organization as often as you reevaluate your strategy.

Mixed teams may be higher-performing teams. Team composition is consequential. Cast those roles carefully too. On average, teams with mixed skills are reportedly more impactful at achieving expected value for digital programs than specialized teams.

Success is neither cut and paste nor pie in the sky. What works on average may not necessarily work for your organization. What works for another organization may not necessarily work for you either. The best level of digital transformation ambition for an organization can depend on its capabilities and goals. Any other choice is likely a misalignment. Expectations should be realistic. If your organization is pursuing a small incremental business case, don’t expect it to transform your entire organization. If you do, you may be disappointed.

Change should drive change. Success is informed by an array of operating choices and facts on the ground unique to you. And since facts on the ground are subject to change, your operating choices may need to evolve over time as well.

Five operating choices that can impact the value of digital programs

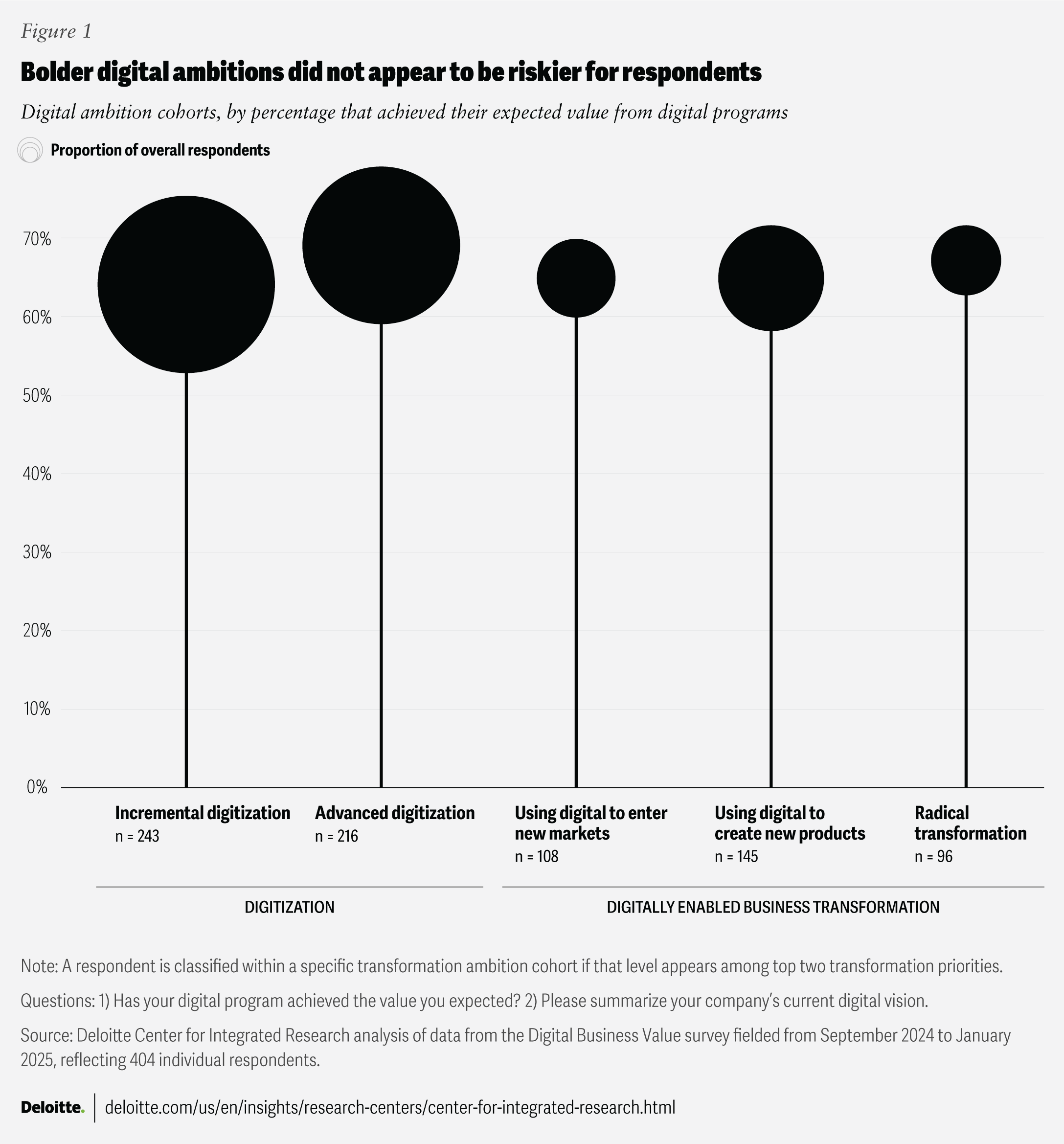

Overall, 64% to 69% of respondents report they are gaining value across each of the five digital ambition levels (figure 1). This seems to imply that no one ambition drives success on its own or is inherently better or riskier in terms of value realization.

Rather, the ambition reflects a specific goal and the respondent’s relative, variable success at achieving it. The analysis that follows uses these same five levels to examine five operating choices that can influence and impact these value dynamics.

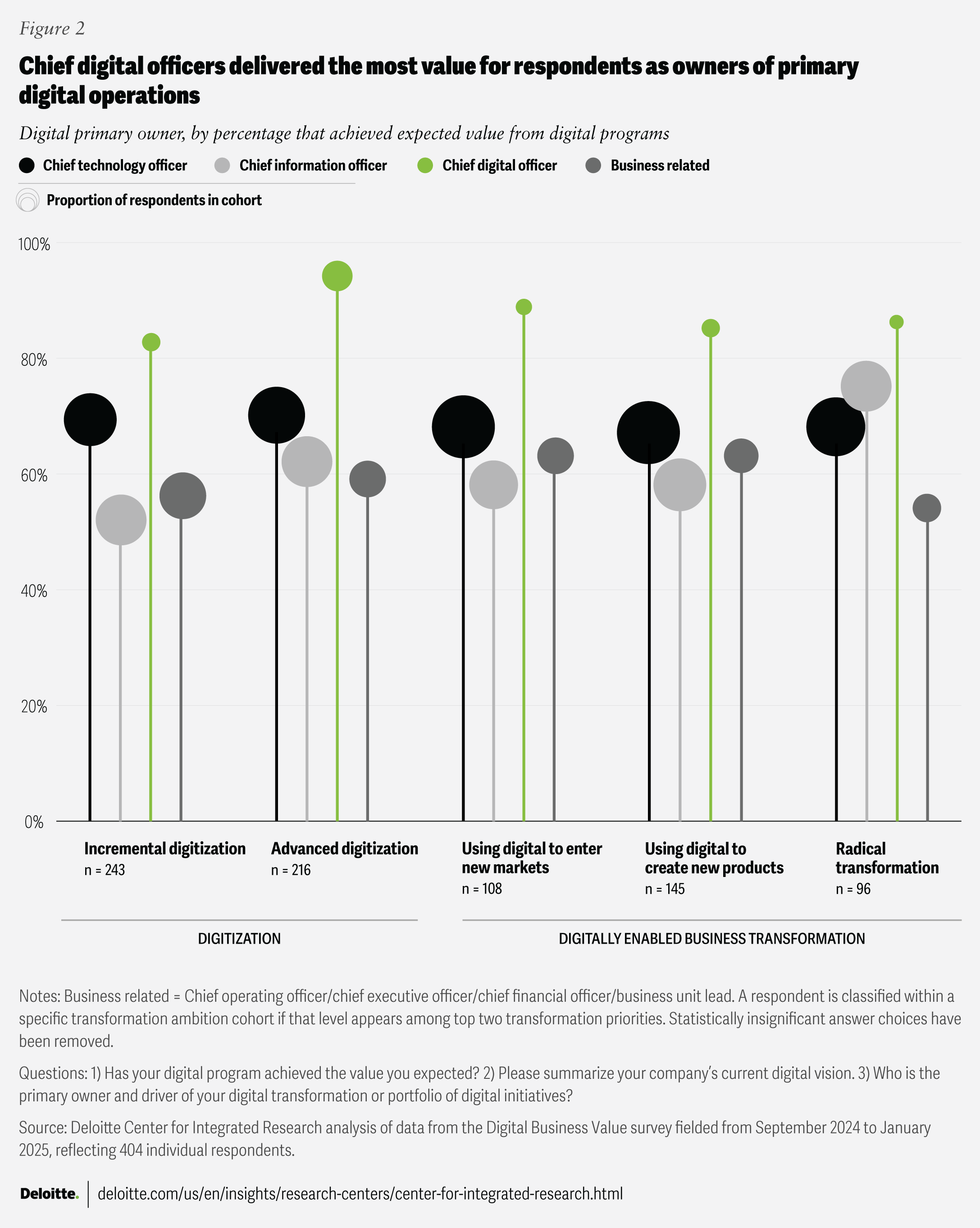

Operating choice 1: Chief digital officer model vs. other ownership models for digital operations

Digital ownership should be considered carefully.

Primary digital ownership models may impact the success of digital programs (figure 2). According to survey respondents, the chief digital officer (CDO) ownership model appears more successful than other models in achieving digital expectations across all digital ambition types, although this model represents only 7% to 15% of respondents within each type. Specifically, an average of 88% of respondents achieved expected value from their digital programs when the CDO is the digital primary owner, compared with 69% for the chief technical officer and 59% for the chief information officer (CIO). The CDO may have the best “hands-on” perch during a digital transformation initiative.2

According to respondents, business-related ownership models are not as successful at achieving expected value, including in product- and market-oriented digital ambitions. This means that organizations should exercise care in casting roles, especially when pursuing radical transformations, prioritizing more cross-functional roles like the CDO (or new titles) that straddle business, technical, and human capital functions.

At the same time, organizations might interpret the exact set of responsibilities and authority accorded to each role through the prism of their respective organizational experiences. A less standardized role, such as CDO, may have varied responsibilities and skills based on the organization, industry, and tenure, whereas a role like CIO may be more standardized. As such, one should exercise a measure of discretion when aligning the right title based on how it’s defined in their organization.

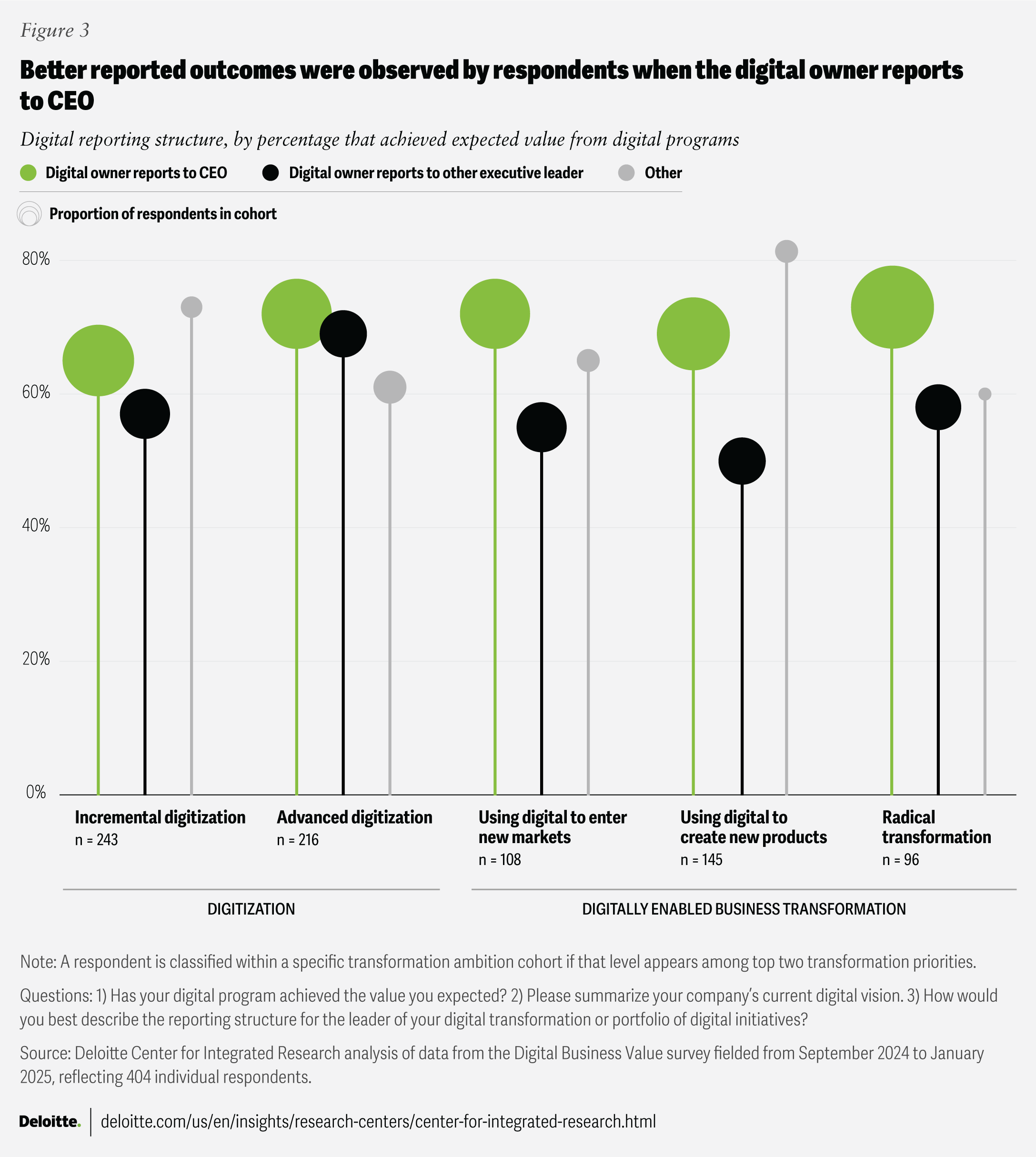

Operating choice 2: Digital leader reporting to the CEO vs. other C-suite executives

Does your digital leader report to the CEO? If not, why not?

Digital reporting structure—specifically, to whom the digital primary owner reports—can also be considered as it relates to value realization. Across all five digital ambition levels, a higher percentage of survey respondents whose digital primary owners report to the CEO indicated that their digital programs achieved expected value, compared to those whose digital owners report to a different C-suite executive (figure 3). On average, 69% of respondents say they achieve expected results when the digital owner reports to the CEO, compared with 59% of respondents when the digital owner reports to a different C-suite executive.

Moreover, reporting directly to the CEO appears to be linked to some of the biggest success gains by respondents in the more advanced kinds of digital transformation initiatives. Higher-level digital ambitions could tend to affect the organization on a more wide-ranging basis, and thus, CEO involvement may become more important.

Based on the survey data, there appear to be other advantages to organizations when the digital leader reports to the CEO. For example, 64% of respondents say they achieve at least 10% margins from digital programs when digital leaders report to the CEO (vs. 57% who achieve those margins when leaders report to other C-suite executives). Also, 37% of respondents whose digital leaders report to the CEO say they will increase digital investments by at least 11% in the next one to three years (vs. 26% of respondents when the leader is reporting to other C-suite executives).

Digital initiatives may be deprioritized when the responsible person doesn’t report directly to the CEO: Forty-two percent of survey respondents whose digital leaders report to the CEO say that their organization views digital as central to the overall strategy compared to 25% of those whose digital leaders report to another C-suite executive. Deloitte’s prior research also suggests that CEOs could have an important role in digital transformation across these digital ambition levels.3

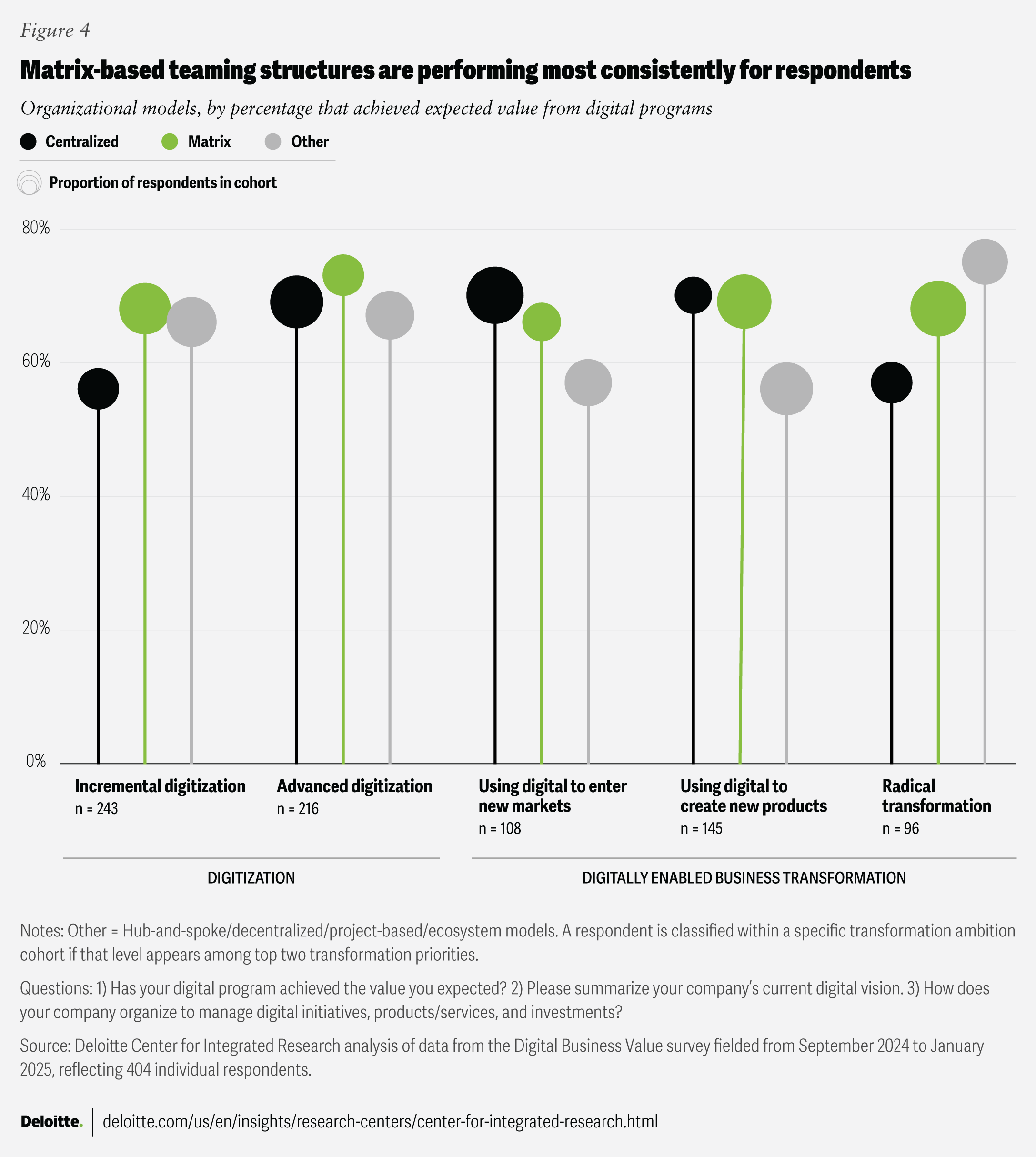

Operating choice 3: Matrixed vs. centralized organizational models

Matrix-based teaming structures perform best overall; benefit of centralization is context dependent, based on digital maturity and transformation ambition

Deloitte also examined three digital team organizational models: matrixed, centralized, and “other” which collectively includes hub-and-spoke, project-based, and ecosystem models, among others. Respondents with matrixed organizational structures—where a central team provides support and foundational capabilities, while individual business units have autonomy over their initiatives—reported consistent results across the digital ambitions (figure 4).

According to the survey respondents, the centralized organizational model with a single decision-making body is less consistent in driving value for respondents. Transformation initiatives may not always benefit from top-down decision-making. For example, a digitally mature organization pursuing radical transformation ambitions may work better with decentralized approaches, given the full and complex array of impromptu decisions that such radical initiatives could require—an environment that may be less compatible with a centralized approach. Alternatively, a digitally immature company pursuing an advanced digital transformation with something other than a centralized approach may not succeed as well in such an environment if its digital processes are less evolved.

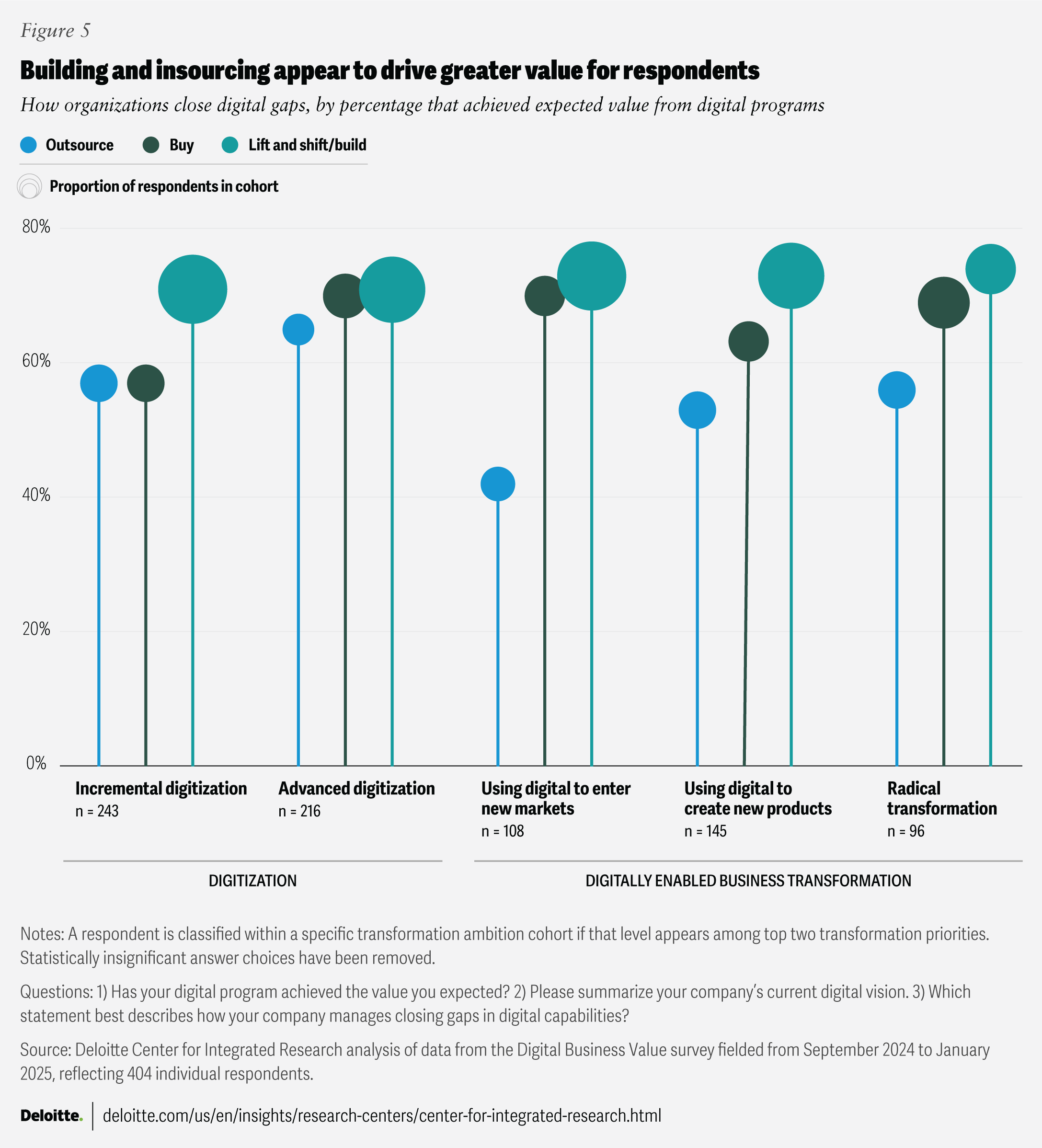

Operating choice 4: Closing digital gaps in-house vs. buying vs. outsourcing

Self-reliant ways to close digital gaps appear most effective; outsourcing methods can come with costs.

As organizations decide whether to buy, build, or outsource tech development, which approach most corresponds with respondents reporting higher value realization? The reliance on internal resources—so-called “build”—yields the best results for respondents across the different digital ambitions (figure 5).

Moreover, survey analysis reveals that “build” approaches appear to perform better in digitally mature environments with strong leadership and team alignments and internal solution design and execution skills. Specifically, based on analysis of survey data, when a “build” decision is pursued in a digitally mature environment, an average of 81% of respondents that pursue a “build” approach achieved expected value from digital programs compared to only 50% of such respondents that exist in a digitally less mature environment.

At the same time, respondents report a diminished likelihood of value realization when they choose outsourcing to close digital gaps. This is especially noticeable within the more external and radical transformation ambitions.

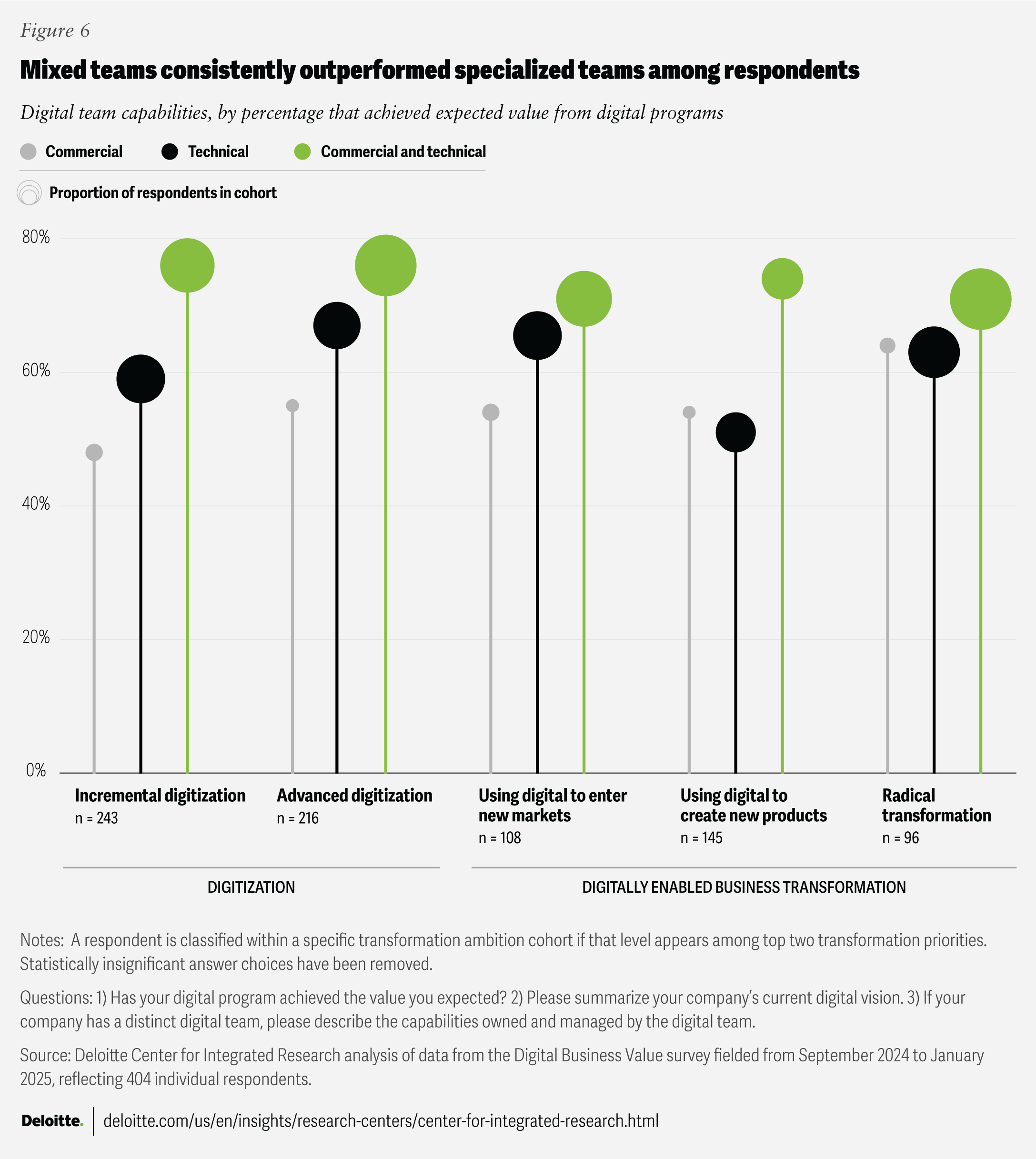

Operating choice 5: Mixed teams vs. specialized business or technology teams

Mixed teams consistently outperformed specialized teams for respondents, especially for those with product innovation ambitions.

Finally, Deloitte analyzed digital team constructs by considering teams with exclusively technical or commercial capabilities as well as mixed commercial and technical teams. Survey respondents with teams with mixed capabilities reported greater value realization compared to those with teams with purely technical or commercial skills (figure 6). Respondents with the ambition to launch “new digital products” showed particularly stark gaps, possibly related to the need for both commercial and technical skills for solution design and taking products to market. Expectations from digital transformation initiatives tend to reflect the business needs of the organization, even digital transformation initiatives that are more internally focused. As such, teams that reflect a wide range of priorities, from customer to technical requirements, may generally be more successful.

While mixed teams appear to lead to better value returns compared to specialized teams on average, there may be situations where mixed teams don’t perform as well as expected based on other considerations. For example, gains in value realization from mixed teams were less dramatic among respondents with radical transformation ambitions, perhaps indicating that it’s not as significant a success factor in these types of transformation scenarios.

Methodology

To better understand how organizations are approaching digital transformation, Deloitte launched a benchmarking survey, collecting data from over 400 US-based organizations across eight sectors, including consumer products, consumer services, energy and chemicals, industrial products, financial services, health care, life sciences, and technology. The survey combined robust quantitative and qualitative inputs gathered from C-level executives to assess digital ambition, investment strategies, operating models, and growth priorities. Survey data was gathered from September 2024 through January 2025.

In developing this thought leadership piece, Deloitte’s Center for Integrated Research examined insights from the survey results. The analysis places particular emphasis on identifying behaviors most associated with successful digital transformations, including team structure, organization design, closing digital gaps, digital primary ownership, and reporting structure.

The analysis in this paper occurs through the prism of Deloitte’s five-level digital transformation framework that identifies five levels of digital transformation ambitions—each ambition across the spectrum is progressively more comprehensive and external in scope.

Continue the Conversation

Meet the industry leaders

Ben Ninio

Jonathan Holdowsky

Chris Iannacone

Parker Mackie

Tim Smith

Gagan Chawla

by

Ben Ninio

Jonathan Holdowsky

Chris Iannacone

Diana Kearns-Manolatos

Parker Mackie

The authors are grateful to Marissa Sawicki for her invaluable contributions to the research and analysis.

They are also grateful to the marketing team, including Saurabh Rijhwani, Ireen Jose, Lily Miskimmin, Grace Geehan, Faith Shea, Jackie Polson, and Sarah Long, for their guidance and leadership on extending the global reach of these insights.

The authors would like to thank Karthik M Bugude, Sudharsan Venkataramanan, and Radhika Talwar for their contributions to survey design and analysis.

The authors extend their gratitude to the Deloitte Insights team, including Elisabeth Sullivan and Andy Bayiates for their editorial input; Molly Piersol, Alexis Werbeck, and Jaime Austin for their creative vision; and Blythe Hurley and Prodyut Borah for their production support.

Finally, the authors express thanks to Garima Dhasmana for her overall support.

Cover image by: Jaime Austin, Alexis Werbeck

Visit the Deloitte Center for Integrated Research

Access more insights on some of the most complex issues facing businesses today.