How restaurants can win on value

Quality, service, and execution shape purchase intent across restaurant formats

When traffic declines, restaurants often lower prices to drive demand. But competitors risk losing customers to brands offering more than a good deal. Understanding the non-price factors that drive consumer value perceptions could be key to unlocking preference and performance.

Restaurants are caught between two competing forces. Costs for food, labor, and operations are rising, tightening margins.1 At the same time, prolonged inflation is prompting a subset of consumers to adopt more cost-conscious behaviors. Restaurants are challenged to drive traffic and protect margins as consumers increasingly focus on value when making purchase decisions.

As some restaurants struggle, brands that consistently provide more value than expected for the price are thriving. While pricing strategy is important, “more-value-for-the-price” (MVP) brands seem to understand the full value equation, where quality and consistent execution shape value perceptions. The basics matter, and MVP brands excel at leveraging non-price drivers to build value and drive future purchase intent.

To identify exactly how value is created in the restaurant sector, Deloitte analyzed over 416,000 consumer data points across 271 restaurant brands.2 This research uncovers the most influential drivers of value perception and purchase intent across fast-casual, quick-service, and sit-down restaurants.

Value seekers want more than a low price

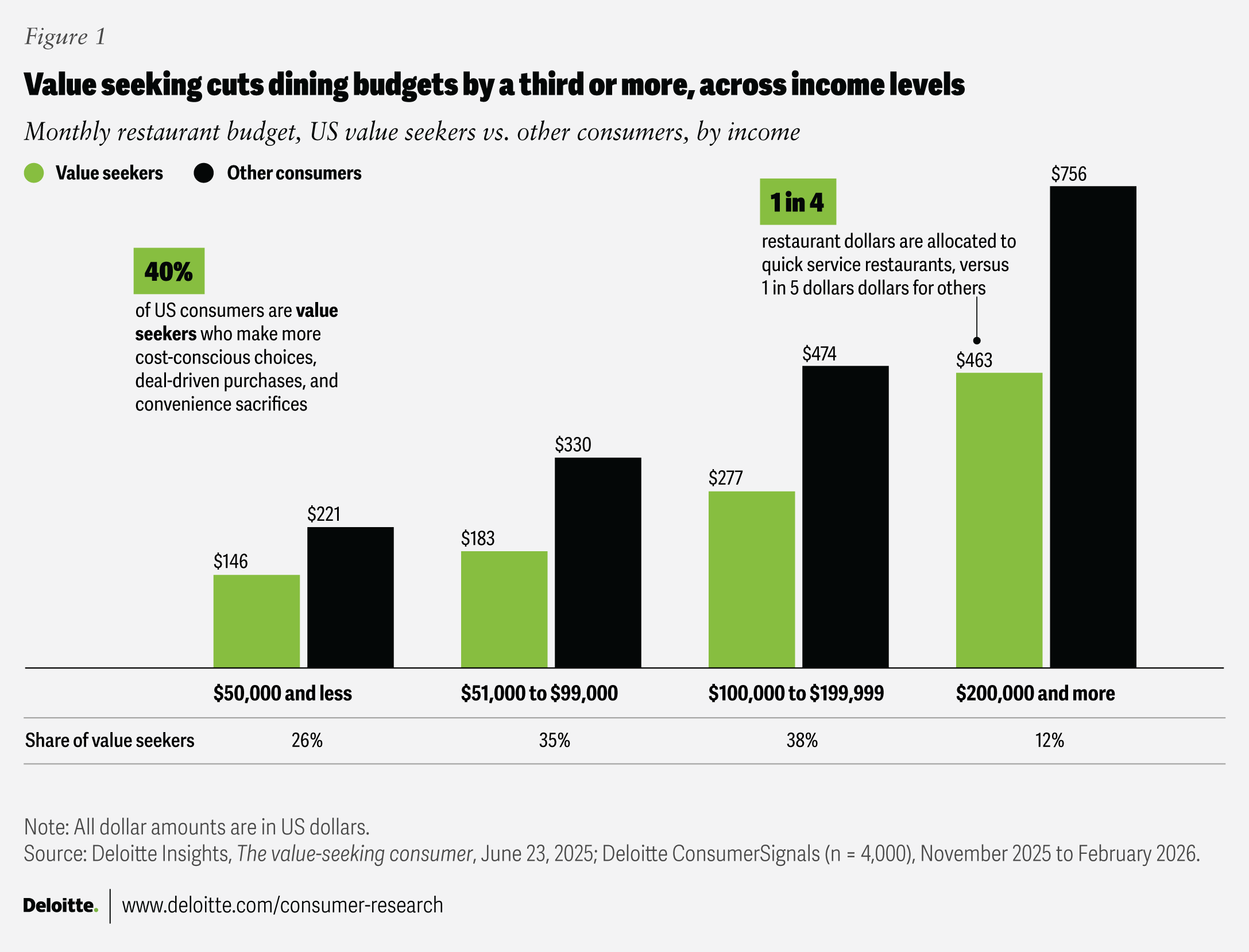

Analysis of Deloitte’s ConsumerSignals data shows that 4 in 10 surveyed consumers are value seekers who actively manage their spending through deal-seeking, cost comparisons, and convenience trade-offs (figure 1).3 When choosing a restaurant, value seekers often prioritize functional basics to minimize risk. These consumers report lower monthly restaurant budgets compared to other diners, and this pattern persists across income levels. Beyond simply spending less, value seekers are making more deliberate decisions about where and how to dine.4

In response, restaurants commonly adjust prices through discounts and promotions to help drive traffic. The cycle is familiar and can be hard to exit: discounts lift demand, margins shrink, investment is constrained, and price sensitivity increases. The next promotion becomes necessary to compensate for the last one.

An alternative is to strengthen quality and other operational and experience-related drivers that compose the value equation. Restaurants that do this can position themselves to sustain demand even as prices rise. Deloitte analysis shows that MVP brands consistently generate stronger purchase intent, making value a powerful lever for increasing future demand.5

Although inflation has eased since its 2022 peak, cost forecasting remains difficult as geopolitical and economic uncertainty persists, reinforcing the need for a long-term approach.6

The MVP advantage

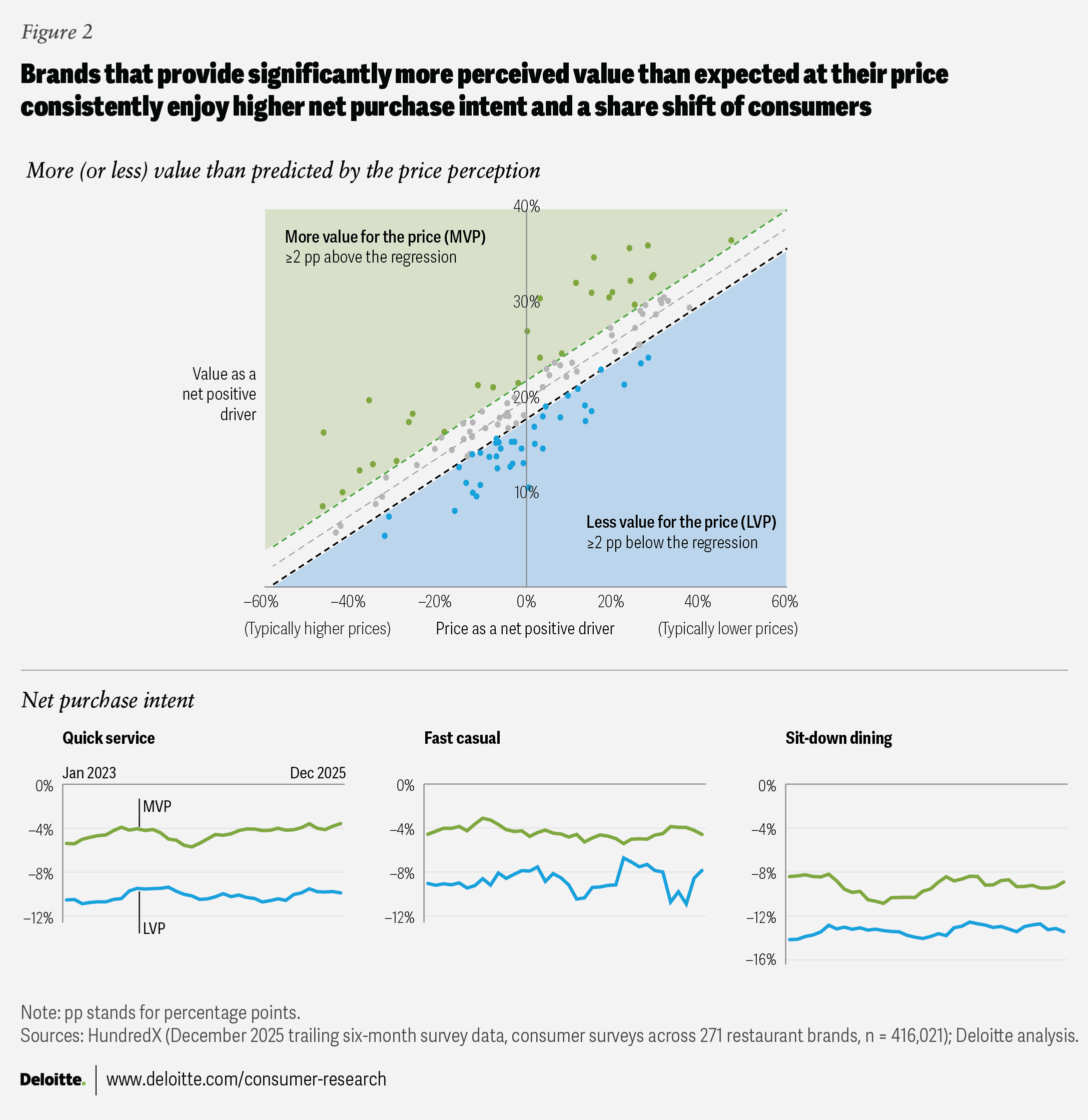

Three in 10 restaurant brands qualify as MVPs, with perceived value that is at least 2 percentage points higher than would be expected based on respondents’ perceptions of their prices (figure 2).7 MVP brands exist at all price points and across each restaurant format, demonstrating that all brands have the potential to strengthen their competitive position by building excess value.

Price shapes value perception in a predictable way: as price perception becomes more positive, value perception improves. But price alone does not determine value. Regression analysis suggests that in the restaurant sector, price explains 67% of what consumers perceive as value, leaving 33% to be influenced by non-price factors.8 When diners choose among restaurants at a similar price point, those factors have the power to tip the scales.

Brands that significantly exceed expectations on factors beyond price outperform competitors and position themselves for faster revenue growth,9 higher net purchase intent, and premium market valuations from investors.10

Based on transactions from Converge by Deloitte’s panel of five million credit cards over three years, MVP restaurant brands collectively grew revenue 7.3% faster than “less-value-for-the-price” (LVP) brands.11 Consumers are spending more with MVP brands—and say they intend to do so in the future.

Net purchase intent, a leading indicator of future demand, is consistently higher for MVP brands than LVP brands across all restaurant formats. The advantage holds across quick service restaurants (QSRs), fast casual, and sit-down dining brands, with QSR MVP brands maintaining the widest margin.

The MVP advantage also extends beyond consumer demand. While many restaurant brands are privately held, available public-market data suggests that parent companies with portfolios weighted toward MVP brands trade at roughly 2.3 times the valuation multiples of those weighted toward LVP brands.12

Focus on the fundamentals

Restaurants are operating in a complex environment, with more ordering channels, a more diverse consumer set, and pressure to improve technology utilization across the business.13 Within this context, it is challenging to sustain high standards of quality and achieve consistent execution across multiple customer touchpoints. Yet these basic elements are central to shaping consumer value perception and driving repeat sales.

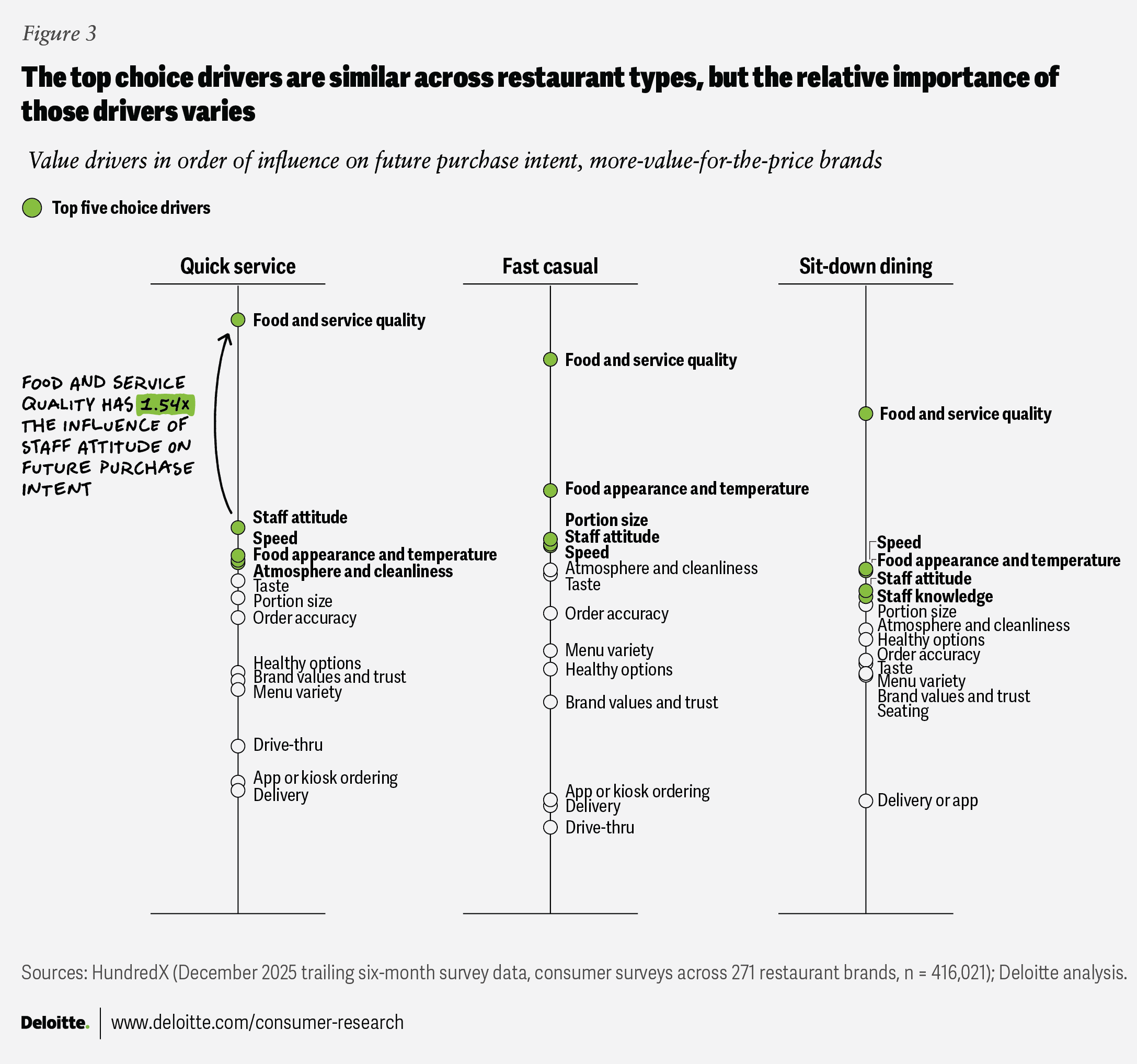

Across restaurant categories, a consistent set of drivers shapes purchase intent (figure 3). Food and service quality stand apart as the most influential, followed by operational and experience factors such as speed, food presentation, staff attitude, and atmosphere and cleanliness.

While quality is the universal anchor for restaurant choice, the secondary drivers of purchase intent differ depending on what consumers expect from a given dining experience. For QSR brands, quality stands apart as the primary differentiator once functional needs are met. In fast casual, where higher quality is expected, success across multiple drivers is needed to justify the trade-up. In sit-down dining, value is judged holistically based on how well food, service, and ambiance come together to create a dining experience worth repeating.

Across restaurant formats, MVP brands consistently outperform on the fundamentals of food execution and operational reliability (figures 4, 5, and 6). This analysis uncovers what sets MVP brands apart and provides a framework to help restaurants identify the product and operational improvements most likely to influence demand.

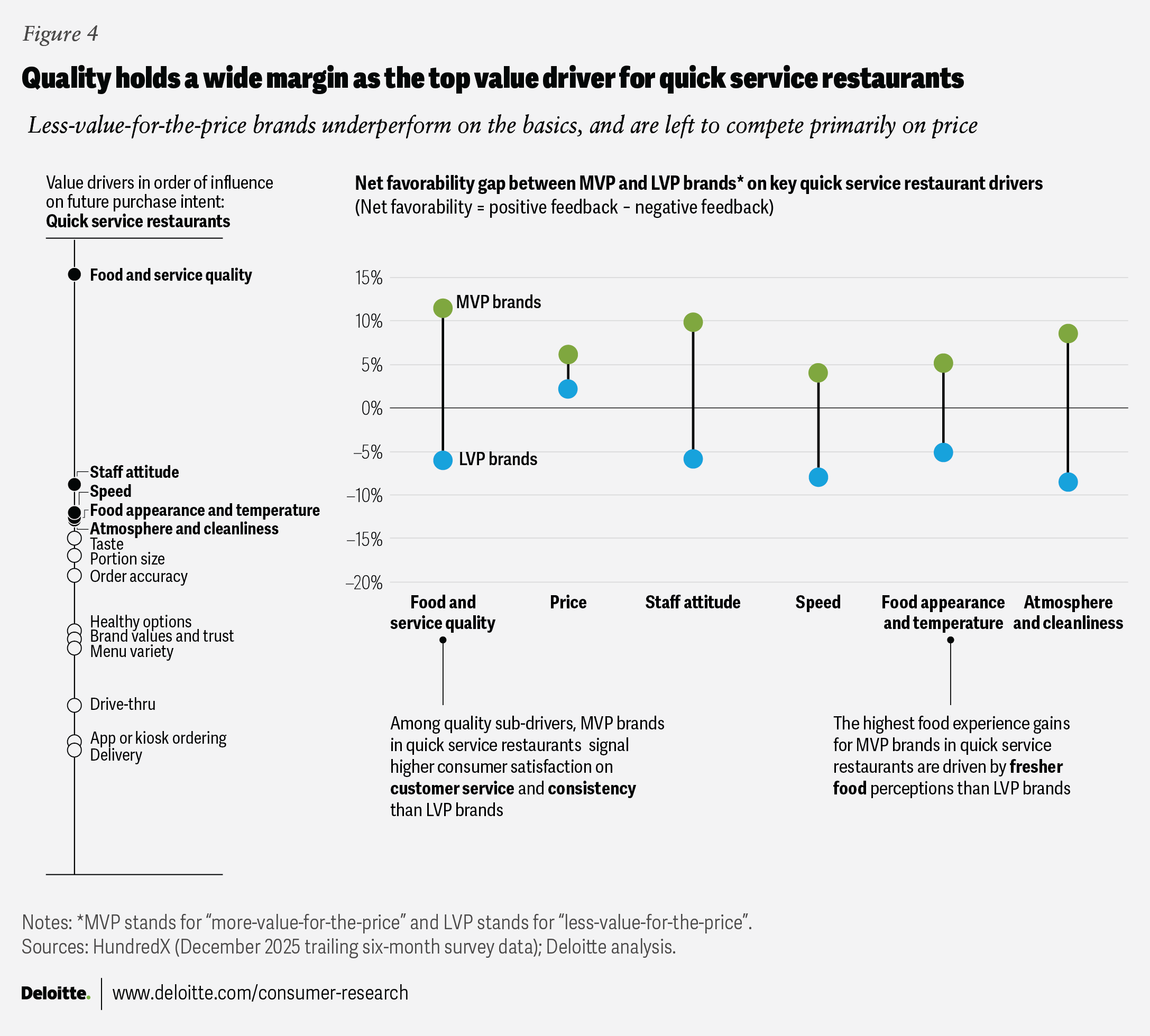

Quick-service restaurants: Lead with quality

In quick-service restaurants, where price sensitivity may be higher, there is a wide gap in performance between MVP and LVP brands (figure 4). Quality stands out as the top driver of restaurant choice in this format, with MVP brands outperforming by a significant margin.

The differences between MVP and LVP brands become even clearer at the sub-driver level, where specific elements of execution indicate where value is won or lost. In QSR, MVP brands outperform across both service quality and food execution. Customer service and consistency stand out as key areas of differentiation, while food freshness shows a strong advantage (+15 percentage points), highlighting the importance of reliable food quality and execution. Together, these results indicate that MVP QSR brands outperform across both human and operational dimensions of the experience.

In contrast, LVP QSR brands perform poorly across the top drivers of purchase intent, where they have negative net favorability. The pattern is associated with weaker demand despite similar price perceptions across QSR brands.

This dynamic is especially important given the role of value seekers in the segment. Value-seeking consumers allocate a higher percentage of their restaurant spending to QSR compared to other diners, and this pattern holds even at higher income levels.14 Yet even in this price-sensitive format, where value seekers are most concentrated, competing on price alone does not sustain demand.

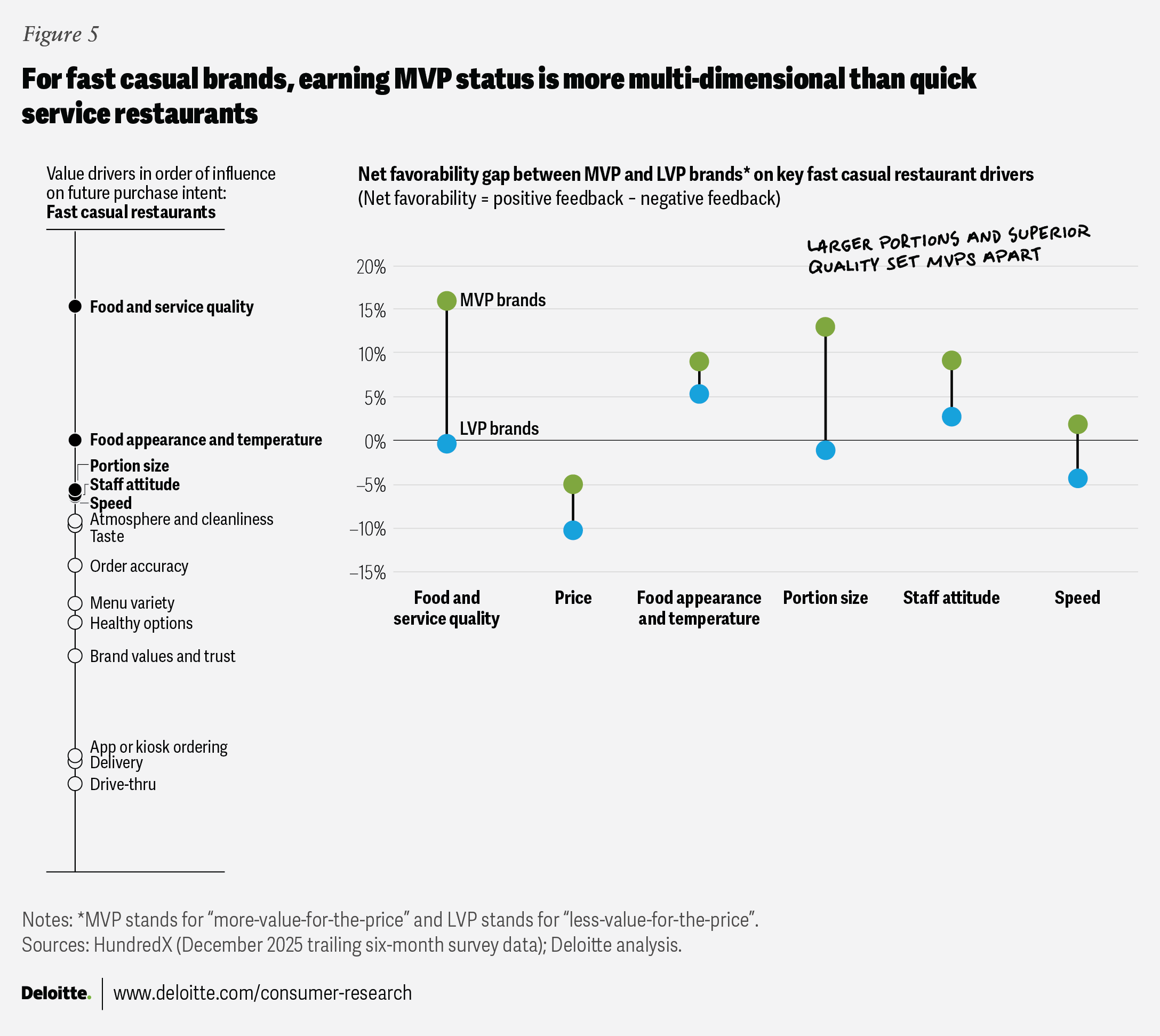

Fast casual: Justify the trade-up

In fast casual, where many brands already meet baseline expectations, differentiation depends on delivering consistently across multiple product and experience drivers (figure 5). In this “upscale convenience” segment, consumers expect stronger performance on fundamentals like food quality, making it harder for brands to stand out on any single attribute.

MVP brands distinguish themselves through superior execution across several drivers simultaneously, including quality, portion size, and menu variety. This balanced performance reinforces the fast-casual segment’s elevated positioning relative to QSR and translates into stronger purchase intent. At a more granular level, cleanliness of the food preparation area stands out as a key differentiator, signaling the importance of back-of-house standards.

LVP brands struggle when they fail to reinforce the value of the trade-up. While they may perform favorably on some attributes, MVP brands perform better while also maintaining a substantial lead in areas such as portion size. As a result, LVP brands risk being perceived as relatively expensive without offering sufficient additional value.

In fast casual, the challenge is not meeting basic expectations but exceeding them consistently enough to justify a higher price point.

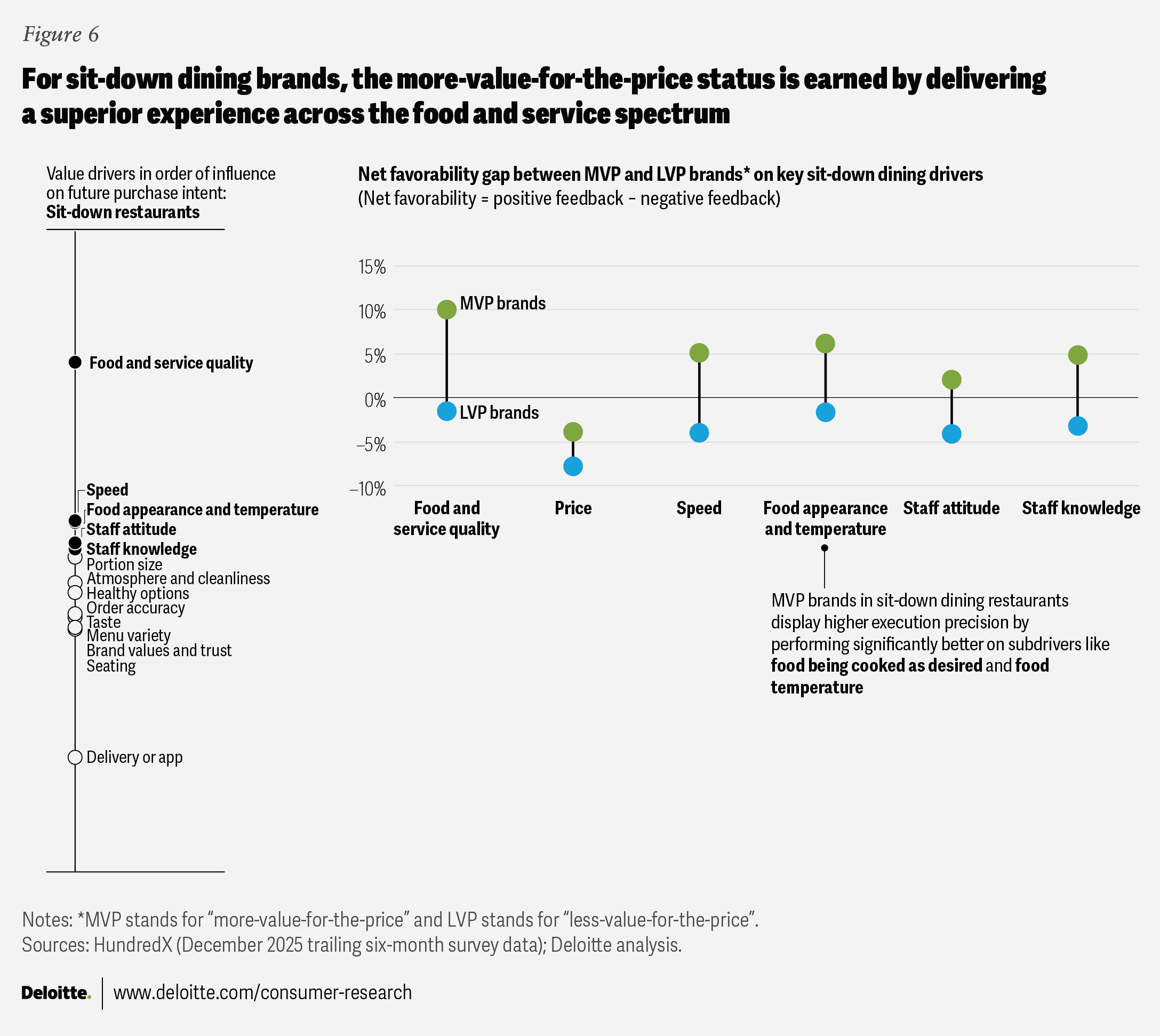

Sit-down dining: Deliver the complete experience

In sit-down dining, customers evaluate the experience as a whole, and value depends on how well multiple high-impact drivers come together (figure 6). MVP brands outperform most on food and service quality, the strongest driver of purchase intent.

These brands also lead across a broad set of secondary drivers, including service speed, staff knowledge, food appearance and temperature, taste, portion size, and order accuracy. Precision in food execution is a key area of differentiation, with MVP sit-down dining brands outperforming on factors such as cooking the customers’ food as desired (+13 percentage points) and achieving the optimal temperature (+12 percentage points), highlighting the importance of consistency at the plate level.

While service and value gaps are narrower than in QSR, these execution details play a central role in shaping the overall dining experience. Together, these results indicate that MVP sit-down brands outperform by delivering a consistently high-quality experience across key moments of the meal.

LVP brands, in contrast, fall behind in multiple areas, often showing negative net favorability on drivers with strong influence on purchase intent. Weakness across several drivers can erode perceived value and reduce willingness to pay. In sit-down dining, isolated strengths are not sufficient—pricing power depends on superior end-to-end execution.

Across formats, MVP brands win on execution, not aesthetics. While LVP brands sometimes rank higher on sub-drivers such as seating, noise levels, or trendiness, those surface attributes may not necessarily translate into future visits. Operators seeking to cultivate MVP-level patronage should prioritize food quality, service reliability, and execution over physical investment alone.

From value creation to pricing power

Pricing power—the ability to raise prices without weakening demand—depends on consistently delivering value through drivers beyond price. As rising costs for labor, ingredients, and operations continue to pressure margins, many restaurant owners have increased prices. But when prices rise in the absence of strong value perception, demand weakens, often triggering a repeating cycle of reactive discounting to increase traffic.

MVP brands operate differently. By investing in the fundamentals that matter most, they sustain demand even when net price perception is negative. In doing so, these brands earn the option to raise prices—but often choose not to exercise it, leaving perceived value on the table to reinforce long-term customer relationships and loyalty rather than short-term gains.

Value is not built through pricing strategy alone. It is earned by strengthening non-price drivers—quality, service, and consistent execution—so demand remains resilient.

What leaders can do next

The following actions can help restaurant leaders shift from competing on price to building value:

- Diagnose your value position. Assess how your brand performs on price and value perception versus peers. Benchmark against MVP competitors to understand where you are delivering more—or less—value than expected for the price.

- Recognize that restaurant basics matter. Customers want high-quality, hot, fresh food served by friendly people in a clean restaurant. The data presented here shows that the quality, appearance, and temperature of the food, the attitude of the employees, and the atmosphere and cleanliness of the restaurant are all important drivers of purchase intent. Getting these basics right is the first step toward MVP status.

- Prioritize improvements that can help shift demand. Based on your format, customers, and competitive position, close the most critical gaps versus competitors across the drivers and sub-drivers most likely to influence purchase decisions—and stop investing in those that do not.

- Leverage industry imperatives to drive future performance.15 Use Deloitte’s five imperatives for restaurants—growth, efficiency, convenience, sustainability, and a future-ready workforce—to help navigate macro challenges and position your brand for long-term success.

- Choose pricing tactics that reinforce value rather than erode it. Instead of broad discounting, consider targeted promotions, bundling, tiered menu options, or portion adjustments that can strengthen value perception without undermining profitability.

Continue the conversation

Meet the industry leaders

Evert Gruyaert

Ed Lee

Maggie Rauch

BY

Evert Gruyaert

Ed Lee

Stephen Rogers

Maggie Rauch

Upasana Naik

The authors would like to thank Akash Kumar and Cathy Walsh for their contributions to this article.

Editorial (including production and copyediting): Rithu Thomas, Preetha Devan, Anu Augustine, and Pubali Dey

Design: Pooja Lnu, Molly Piersol, Natalie Pfaff, and Jaime Austin

Cover image by: Alexis Werbeck; Adobe Stock

Knowledge services: Rohan Singh

Visit the Deloitte Consumer Industry Center

Access more insights for the automotive, consumer products, food, retail, wholesale and distribution, airlines and hospitality, and transportation sectors.