OECD Pillar Two side-by-side package: A New Zealand perspective

Tax Alert - February 2026

By Joe Sothcott, Young Jin Kim & Annamaria Maclean

2025 marked the first year multinational enterprise (MNE) groups became subject to the OECD’s Global Anti‑Base Erosion (GloBE) Pillar Two rules in New Zealand. These OECD coordinated rules are intended to ensure that MNE groups pay a minimum effective tax rate of 15 percent on their income in each jurisdiction in which they operate.

However, the global implementation of Pillar Two has faced a number of challenges. In particular, the future of the GloBE rules was brought into question when the United States proposed to introduce section 899 under the One Big Beautiful Bill which could have imposed increased taxes on “discriminatory foreign countries”. New Zealand was considered to be a discriminatory foreign country at the time as it had implemented certain aspects of the Pillar Two framework.

Before section 899 was formally enacted, an agreement was reached between the United States and its G7 partners to remove the provision from the legislation. In return, the United States secured an in principle exemption for US‑headquartered MNE groups from the Pillar Two rules (see our August 2025 Tax Alert article).

Following further negotiations, on 5 January 2026 the OECD released the long‑awaited GloBE Side‑by‑Side Package (SbS Package). The SbS Package gives effect to this agreement and introduces a range of additional amendments to the Pillar Two rules.

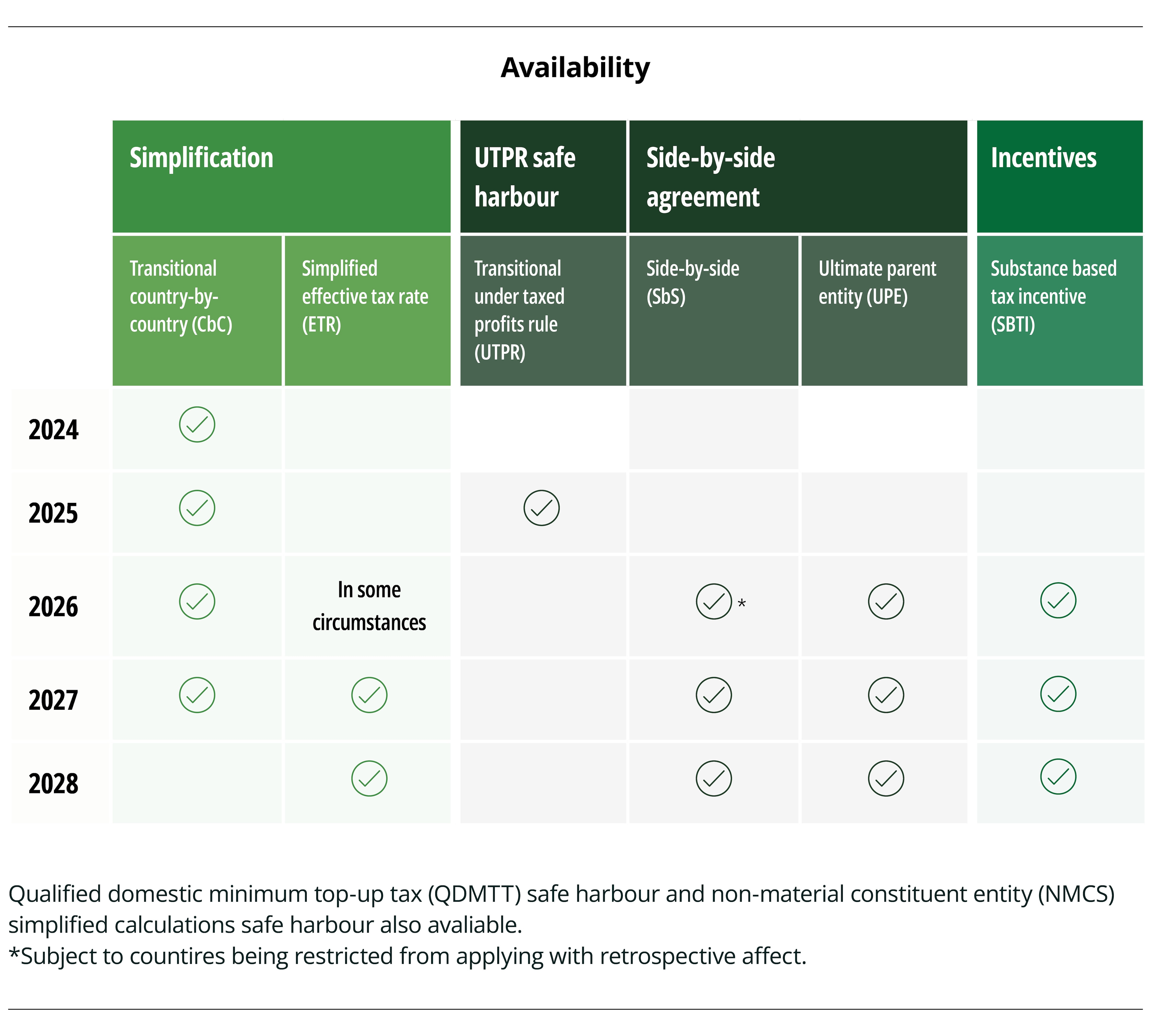

What is included in the SbS Package?

The SbS Package is not just a side-by-side system but includes additional new or extended safe harbours. The SbS Package comprises:

- Simplified Effective Tax Rate Safe Harbour

- Extension of the Transitional Country-by-Country Reporting Safe Harbour

- Substance-based Tax Incentive Safe Harbour

- Side-by-Side System, consisting of the Side-by-Side Safe Harbour and the Ultimate Parent Entity Safe Harbour

Permanent Simplified Effective Tax Rate Safe Harbour

The SbS Package introduces a permanent Simplified Effective Tax Rate (ETR) Safe Harbour. This safe harbour allows MNE groups, by election, to apply a streamlined ETR calculation based on financial statement data, subject to a limited set of prescribed adjustments.

Under this safe harbour, a jurisdiction qualifies where the simplified ETR is at least 15 percent, or where the jurisdiction is in a “simplified loss” position. Where the safe harbour applies, the jurisdiction is treated as having zero Pillar Two top‑up tax for the relevant fiscal year, and a full GloBE calculation will not be required for that jurisdiction.

The Simplified ETR Safe Harbour generally applies for fiscal years beginning on or after 1 January 2027, with availability for earlier application in 2026 in certain circumstances.

Extension of the Transitional Country‑by‑Country Reporting Safe Harbour

The SbS Package also extends the Transitional Country‑by‑Country Reporting (CbCR) Safe Harbour by one additional year, to years beginning on or before 31 December 2027 and applying a 17% transitional rate. This extension avoids an abrupt compliance cliff and provides MNE groups with additional time to transition to the Simplified ETR Safe Harbour or the full GloBE calculations.

Substance-Based Tax Incentive Safe Harbour

The SbS Package introduces a new Substance‑Based Tax Incentive Safe Harbour. By election, this safe harbour allows for certain qualifying tax incentives that are linked to substantive economic activity (expenditure based or production based) to be taken into account when determining Covered Taxes for Pillar Two purposes.

The availability of the safe harbour is subject to caps that are tied to the level of substance in the jurisdiction, ensuring that only incentives aligned with genuine economic activity are recognised.

An election to apply the Substance‑Based Tax Incentive Safe Harbour can apply for income years beginning or on after 1 January 2026.

Side-by-Side System

The key feature of the SbS Package is the Side‑by‑Side System, which is designed to allow Pillar Two to coexist with domestic tax regimes that deliver comparable minimum tax outcomes.

Under the Side‑by‑Side Safe Harbour, MNE groups with their Ultimate Parent Entity (UPE) in a jurisdiction that has implemented a Qualified SbS Regime may elect to obtain relief from the application of the Income Inclusion Rule (IIR) and the Undertaxed Profits Rule (UTPR). Application of the Qualified Domestic Minimum Top‑Up Taxes (QDMTTs), however, remain unaffected by the Side-by-Side Safe Harbour. As of January 2026, the United States is the only jurisdiction that qualifies under this regime.

The package also introduces a separate UPE Safe Harbour (to replace the Transitional UTPR Safe Harbour), which allows an election to switch off the UTPR in respect of UPE jurisdiction profits where the UPE jurisdiction has an eligible domestic minimum tax regime but does not have an eligible worldwide regime.

Both the Side‑by‑Side Safe Harbour and UPE Safe Harbour apply for fiscal years beginning on or after 1 January 2026.

A New Zealand perspective

The SbS Package should be automatically incorporated into New Zealand law under section HP 3 of the Income Tax Act 2007. However, there is some uncertainty regarding its practical application. This is particularly relevant for the Side-by-Side Safe Harbour, which is expected to apply for fiscal years beginning on or after 1 January 2026.

Importantly, the Side-by-Side Safe Harbour for US headquartered multinational groups does not apply in 2025 - the first year in which the Pillar Two rules take effect in New Zealand. As a result, we expect the New Zealand compliance obligations, including registration and the filing of the multinational top-up tax return, to remain for the 2025 year for all MNE Groups.

At this stage it remains unclear moving forward how Inland Revenue will interpret the impact of the Side-by-Side Safe Harbour on these New Zealand compliance obligations. Deloitte will continue to engage with Inland Revenue to seek clarity on the intended compliance approach.

Unlike many other jurisdictions that have implemented the GloBE rules, New Zealand has not adopted the QDMTT. As such, MNE groups with a UPE located in a jurisdiction that has implemented a Qualified SbS Regime (currently the US) are likely to obtain full relief from the operation of the Pillar Two rules in New Zealand (expected for income years beginning on or after 1 January 2026). This differs from the position in many other jurisdictions, where such MNE groups are still required to comply with a local QDMTT in subsidiary countries.

For New Zealand headquartered MNEs, it will be important to consider how the SbS Package (and in particular, the first three safe harbours above) are implemented in other jurisdictions. Although New Zealand’s legislation automatically incorporates any additional commentary or guidance issued by the OECD with respect to the GloBE rules, this is not expected to be the case in most jurisdictions.

Against this backdrop, New Zealand headquartered MNEs should be putting systems and processes in place to monitor and meet compliance obligations for previous income years and future years, potentially across multiple jurisdictions with different implementation timelines. With these changes, it is relevant to note that:

- The introduction of the Simplified ETR Safe Harbour for fiscal years beginning on or after 1 January 2027 (or potentially 1 January 2026 in certain circumstances) together with the extension of the Transitional CbCR Safe Harbour to the 2027 year provides additional choices of methods that could be applicable in the 2026 and 2027 years.

- Taxpayers should carefully assess the availability and interaction of these safe harbours, including the differing ETR thresholds (15% for the Simplified ETR Safe Harbour and 17% for the Transitional CbCR Safe Harbour ETR test for the relevant years).

- New data points will be required for the application of the Simplified ETR Safe Harbour and the Substance‑Based Tax Incentive Safe Harbour that should be incorporated into systems and processes as needed.

What about the Global reaction?

Deloitte has written extensively about the SbS Package, and some perspectives from our colleagues around the world can be found below:

- OECD Pillar Two: Side-by-side package released

- OECD Pillar Two side-by-side package: An Australian perspective

- OECD Pillar Two side-by-side package: An US perspective

- OECD Pillar Two side-by-side package: A China and Hong Kong SAR perspective

And for more information about the application of the Pillar Two rules in New Zealand, please see:

- OECD Pillar Two rules enacted in New Zealand - navigating the 15% minimum tax for multinationals

- Pillar Two FAQs

If you have any questions about Pillar Two or the SbS Package, please contact your usual Deloitte advisor.

February 2026 - Tax Alerts

- Cryptocurrency: Income tax and DeFi - What investors need to know about Inland Revenue’s new issues paper

- New year, new KiwiSaver rules, same you

- Inland Revenue continues to ramp up transfer pricing reviews

- OECD Pillar Two side-by-side package: A New Zealand perspective

- Snapshot of recent developments