Cryptocurrency: Income tax and DeFi - What investors need to know about Inland Revenue’s new issues paper

Tax Alert - February 2026

By Kirsty Hallett & Ian Fay

“Remember: in crypto, nothing is certain except volatility, innovation… and tax.”

With New Zealand gearing up to implement the cryptoasset Reporting Framework (CARF) from 1 April 2026, time is running out for taxpayers to get across their tax obligations before Inland Revenue gets much greater visibility of activities in the cryptoasset sector.

As the Decentralised Finance (DeFi) eco-system continues to expand with new platforms, products and possibilities, many investors are diving in head-first. However, the tax treatment of DeFi is not always what investors expect.

To help, Inland Revenue has released an issues paper Income tax – wrapping, bridging, lending, borrowing and staking cryptoassets (the paper) outlining Inland Revenue’s thoughts on how existing laws apply to DeFi assets and transactions. It’s not binding guidance (yet), but it provides a solid peek into Inland Revenue’s current thinking on the income tax consequences of common DeFi transactions and, in particular, whether these activities involve taxable disposals of cryptoassets and acquisitions of different cryptoassets for tax purposes. The paper is open for consultation, with submissions due 12 March 2026.

Because the paper is an issues paper and not final binding guidance, it should be read as an indicator of Inland Revenue’s current thinking as to how the current income tax rules apply to DeFi transactions based on their current understanding. While the paper focuses on wrapping and bridging, lending, borrowing, and staking DeFi transactions, the paper provides useful insights into and serves as a reminder as to how taxpayers can expect Inland Revenue to interpret and apply the tax rules to a broader range of transactions.

For a refresher on the general tax obligations related to cryptoassets please see our August 2024 Tax Alert article.

What is DeFi (really)?

DeFi, or Decentralised Finance, is a growing financial eco-system using blockchain and smart contracts (self-executing digital agreements) to allow people to transact directly, without banks or brokers. In simple terms, it is ‘online banking without the bank’ (and a lot more jargon).

The issues paper focuses its guidance on DeFi transactions referred to as:

- Wrapping and bridging

- Lending

- Borrowing

- Staking

- Briefly, providing collateral for a loan.

However, the principles discussed can be applied more generally to other types of transactions or arrangements in the DeFi ecosystem.

Key takeaways from Inland Revenue’s initial views

Inland Revenue is sticking to its longstanding view that cryptoassets are property (not currency) and therefore are subject to the same rules as other personal property for tax purposes. Generally, this means selling, trading, or exchanging cryptoassets is taxable on realisation, where a person:

- Has a cryptoasset business

- Acquired the cryptoassets as part of a profit-making undertaking or scheme

- Acquired the cryptoassets for the dominant purpose of disposal.

Determining whether a disposal of a cryptoasset is a taxable transaction will depend on the taxpayer’s circumstances. Inland Revenue typically expect cryptoasset transactions to give rise to taxable income. If an investor wants to assert that they did not acquire a cryptoasset for the dominant purpose of disposal Inland Revenue expects them to hold documentary evidence from the time they acquired the cryptoasset demonstrating a dominant purpose of acquiring it that does not require a disposal.

This means that when an investor’s legal rights in relation to a cryptoasset are surrendered, exchanged, or replaced with different rights, as would typically occur as part of entering into a DeFi transaction this is likely to be viewed as a taxable disposal of property. This is the case even if the investor retains ‘economic’ ownership of the cryptoasset.

In addition, where a person receives rewards for the use of their cryptoassets (often referred to as ‘interest’), the rewards will usually be taxable when received.

When is a cryptoasset considered disposed of?

Unlike other examples of personal property such as shares, there is no register of ownership of digital assets. Rather ownership of a cryptoasset is determined by who holds the private key to the asset. The person that holds the private key for a cryptoasset is the only person that can deal with that cryptoasset.

The paper confirms that where a cryptoasset is no longer in the person’s wallet and they no longer control the private key to access that cryptoasset, a disposal has occurred.

However, a disposal of a cryptoasset typically does not occur in the following situations:

- Moving cryptoassets between your own wallets

- Sending cryptoassets to a custodian who holds it on trust for you (with the owner retaining a beneficial interest in those assets)

- Using an individual vault or smart contract, where the cryptoassets remain separately identifiable and not pooled.

How common DeFi transactions are treated

Wrapping

Wrapping typically involves exchanging a native token (e.g. ETH) for a wrapped token (e.g. wETH) that is intended to track the same value as the native token but is a separate token with different legal and technical characteristics. Inland Revenue’s initial view is that wrapping commonly involves disposing of one cryptoasset and acquiring another, because the investor’s rights and the token held change. Therefore even if the economic value is identical, as the legal rights differ, wrapping and unwrapping may crystallise taxable gains (or losses).

Bridging

Bridging moves assets between blockchains using a bridge protocol. Depending on the design, the original token may be locked, burned, or otherwise put beyond the investor’s direct control, with a different token (or representation) issued on the destination chain. Inland Revenue’s view is that bridging can involve a disposal of the original cryptoasset and acquisition of a different cryptoasset, rather than a mere transfer. This means for tax purposes, based on the legal form, each bridge in and out may be a taxable transaction (even if you were just trying to chase a better yield on another chain).

Lending, borrowing and liquidity pools

DeFi lending and borrowing often involves supplying cryptoassets to a protocol (or liquidity pool) and receiving a receipt token or liquidity provider (LP) token in return. Later, the investor may redeem or burn that token to withdraw assets (sometimes plus yield). Lending transactions will almost always reshuffle legal ownership, even if temporarily. Inland Revenue’s approach to respect the legal form of the transaction means each of the steps involved in the transaction must be analysed to determine if there is a separate disposal and acquisition.

Taxable triggers may include:

- Depositing tokens into a protocol where legal ownership/control is transferred or pooled

- Receiving LP tokens, receipt tokens, or other derivative tokens as a new cryptoasset

- Redeeming/burning LP tokens to withdraw underlying assets

- Liquidation events (e.g., collateral sold) and protocol fees paid in cryptoassets

- Claiming or auto‑compounding incentives that are received as new tokens.

Further, many lending or borrowing transactions involve the exchange of ownership of a cryptoasset for a right to acquire or receive cryptoassets in the future. These types of arrangements may be subject to the financial arrangement rules, bringing even more complexity than most investors expect.

Staking and DeFi Rewards

Rewards from staking, liquidity mining and governance token distributions will generally be taxable when you receive and take ownership of them, even where you don’t ask for them.

Whether entering into a delegated staking arrangement (i.e. where a person gives a validator the right to use their cryptoassets as collateral in return for payment of rewards) will give rise to a disposal of the cryptoasset for tax purposes will depend on the fine print of the protocol, as the legal form of the transaction will determine the tax implications.

What does all this mean for Investors?

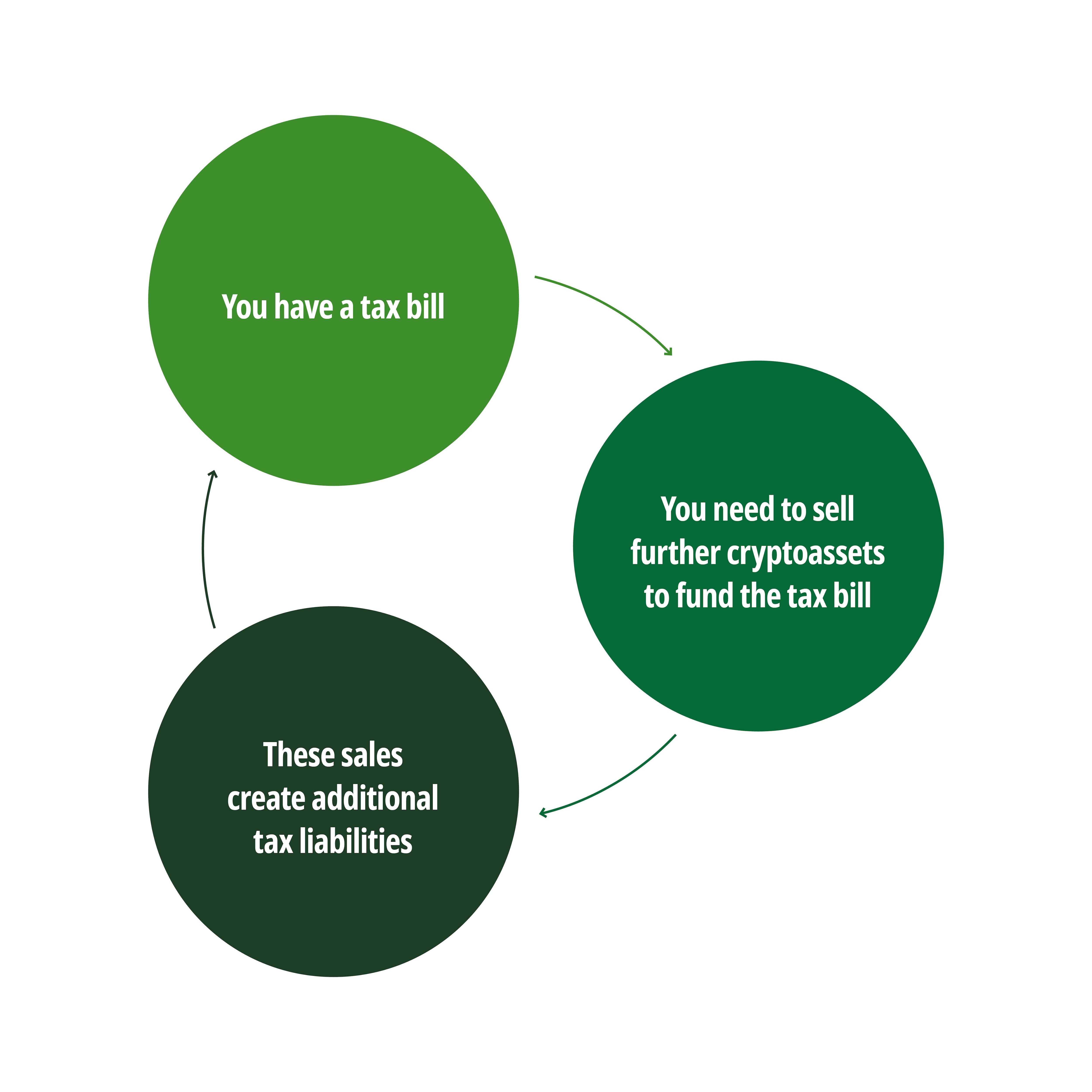

In a nutshell, DeFi tends to generate more taxable events than people realise. Investment strategies such as wrapping, bridging, lending and liquidity pool participation can rack up disposals (taxable events) quickly, often without producing liquid cash to fund the resulting tax bill.

This can create a frustrating cycle:

To help navigate the tax complexities it is crucial to seek professional tax advice before interacting with the complex DeFi protocols to ensure you understand your tax obligations.

Record-keeping is also crucial to help ease the compliance burden.

Is it time for a new cryptoasset-specific tax framework?

While the paper provides a comprehensive summary of how the current tax rules apply to various types of cryptoasset transactions, it highlights an important reality. The current tax rules (related to property) work, but they are complex and difficult to apply to the quickly developing and fast moving DeFi sector.

Complexity, compliance costs and timing challenges are the reality, particularly where tax liabilities are crystallised before liquidity. A new cryptoasset specific tax regime focused on taxing the economic substance of transactions could simplify compliance and better reflect the nature of modern digital transactions.

Alternatively, existing share-lending rules (already based on economic substance rather than legal form) potentially could be adapted to include cryptoasset arrangements.

Inland Revenue is actively seeking submissions on:

- Practical concerns

- Administrative improvements

- Whether current outcomes are ‘right’

- Whether the law itself needs to evolve.

Have questions or want to provide feedback?

If you would like some help unpacking the issues paper, preparing a submission, or reviewing the tax treatment of your crypto asset activity, please reach out to your usual Deloitte advisor.

February 2026 - Tax Alerts

- Cryptocurrency: Income tax and DeFi - What investors need to know about Inland Revenue’s new issues paper

- New year, new KiwiSaver rules, same you

- Inland Revenue continues to ramp up transfer pricing reviews

- OECD Pillar Two side-by-side package: A New Zealand perspective

- Snapshot of recent developments