アジア パシフィック プライベート・エクイティ年鑑2025年版 – 2025 Asia Pacific Private Equity Almanac

アジア パシフィックにおけるプライベート・エクイティ活動の2024年全体像および2025年の展望 – Comprehensive picture of Private Equity activity across Asia Pacific in 2024 and 2025 outlook

アジア パシフィックプライベート・エクイティ年鑑2025年版

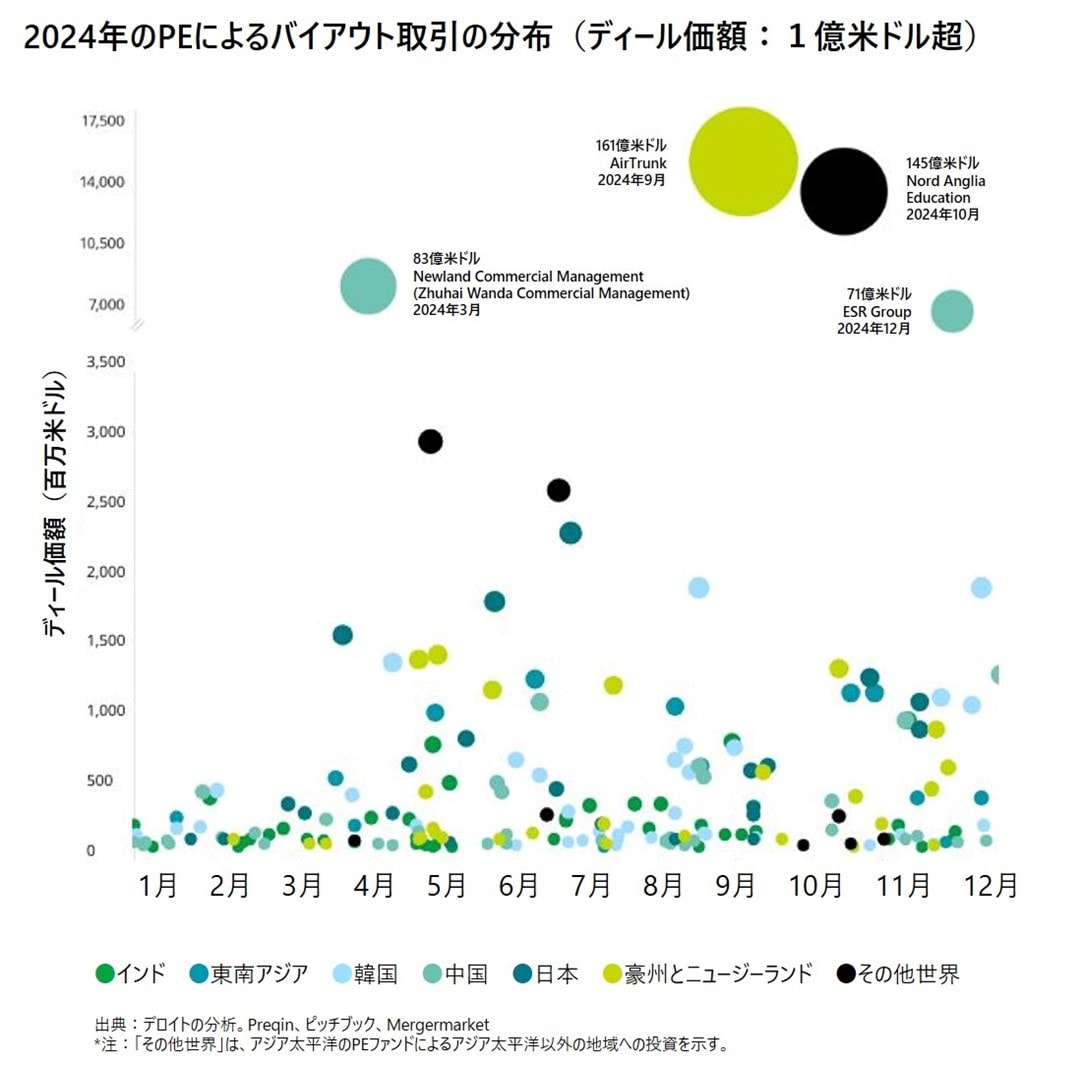

アジア太平洋地域におけるプライベート・エクイティ (PE) 業界は、投資戦略の進化と新たな市場トレンドによって活気づき、2024年に大幅な回復を見せました。2024年の本地域のPEによるバイアウト投資は、1,380億米ドルに達し、2023年から8.1%の増加となり、PEのディール活動が過去10年間で2番目に良い年となりました。このように勢いを盛り返したことから、ジェネラルパートナー (GP) と投資家の間には楽観が芽生え、2025年が活発な年になる下地ができました。地政学上の変化と経済変動が続いているものの、本レポートでは、向こう1年間のPEの状況を形成するのは、M&A活動、地理的な再調整、オペレーションの効率性であろうことが浮き彫りになっています。

主な洞察

- 勢いは強く、PEによるバイアウト活動は2024年を通じて四半期毎に続伸した。

- 新規投資のみならずエグジットにおいても、地域的な重点に変化があり、事業会社からは強力な買収価格の提示がある。

- 大型ディールと小型ディールが大半を占めた。その一方、中規模のセカンダリー取引は2025年に持ち直すと予想される。

- 消費財セクター、テクノロジー・メディア・通信 (TMT)セクター、資本財セクターへの投資が最も多かった。

市場の動向

企業価値の評価で折り合わない部分が縮小し、金利は低下

金利の低下が明白になり、PEのエグジット時のバリュエーションが低下すれば、この先1年間に、GPはより確信を持って新規ディールを探せるようになる可能性がある。市場の活性化が好循環を生み、ディール活動が急激に加速し、2023年と2024年に下火だった中規模のセカンダリー取引が回復することもあり得る。

案件の発生が乏しい中、大型案件とボルトオン型買収に引き続き重点が置かれている

規模が上位2%の案件 (件数ベース) は、通常ならば市場価額の約3分の1を占めるが、2024年には案件価額の総額の42%になった。その一方でPEは、より小規模の案件と既存の投資先企業のボルトオン買収へ投資を続けた。中規模の案件は比較的少なかった。

地理的な分割と再調整

PEファンドは地理的なバランスの再調整を行うことに力を注いでいる最中であり、その一環として、投資先企業が地理的に分割する戦略を推進している。すなわち、事業運営を最適化して買い手候補を惹きつけるため、地理的な線引きに沿ってポートフォリオを再構築している。

事業会社への売却によるエグジットの増加

多くのGPは、リミテッドパートナー (LP) から新たな資金を募集するために売却を急ぐ必要性がそれほど無くなったため、2024年にエグジットを遅延または延期した。しかし事業会社への売却によるエグジットは増加した。

今後の展望

アジア太平洋地域ではファンドの統合と合併が進むだろう

アジア太平洋のPEファンド業界は成熟と変貌の両方を遂げており、数少ない大型ファンドへと集約され、それに応じて同地域のファンドのオペレーションが拡大している。成長志向の投資からオペレーション志向のバイアウトへの転換も顕著に見られ、GPはそのために自社のオペレーション能力を高めるようになるだろう。

「ゾンビ」ファンドの出現

小型ファンドと中型ファンドの中には、運用者が新規ファンドの募集をほぼ断念し、投資対象をエグジットさせる動機が薄れ、バリュエーションの将来的な上昇を期待して資産を手放さないことに決め、休止状態に入るファンドも出てくるだろう。

2025年は、本地域の外で発生するショックや変動性に立ち向かわざるを得ないかも知れないが、成長の年になる様相

事業会社の買収意欲によって楽観が広がり、ディール活動が促進されれば、PEファンドはポートフォリオ資産の売却に関し、より確信が持てるようになる可能性がある。

2025 Asia Pacific Private Equity Almanac

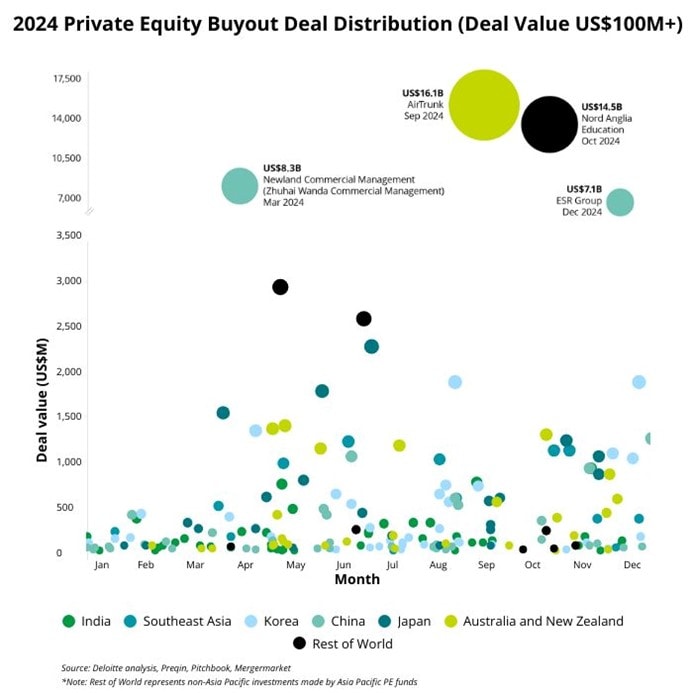

Asia Pacific’s private equity (PE) landscape has experienced a significant rebound in 2024, fueled by evolving investment strategies and emerging market trends. In 2024, PE buyout investments in the region reached US$138 billion, marking an 8.1% increase from 2023 and the second-best year for PE dealmaking over the past decade. This renewed momentum has instilled optimism among General Partners (GPs) and investors, setting the stage for an active 2025. Despite ongoing geopolitical shifts and economic volatility, the report highlights that M&A activity, geographic realignment, and operational efficiency will shape the PE landscape in the year ahead.

Key Insight

- Strong momentum with solid quarter on quarter growth in PE buyout activities throughout 2024.

- Shifting regional focus for new investments as well as exits with a strong bid from strategic buyers.

- Large and small deals dominated, while mid-sized secondary trades are expected to rebound in 2025.

- Consumer, TMT, and Industrials sectors saw the most investment.

Market Themes

Narrowing valuation gap and falling interest rates

Clarity on falling interest rates and lower PE exit valuations may give GPs greater confidence to pursue new deals in the coming year. Greater market activity could feed off itself, leading to a rapid acceleration in deal making and a rebound in mid-sized secondary trades that were relatively suppressed in 2023 and 2024.

We continue to see a focus on big deals and bolt-ons in the absence of deal flow

The largest 2% of deals (by deal count), which typically account for about a third of market value, accounted for 42% of overall deal values in 2024. On the flip side, PEs continued to invest in smaller deals and bolt-ons to existing holdings. Mid-sized deals were relatively scarce.

Geographic splits and realignment

PE funds are going through a period of geographic rebalancing, including PE portfolio companies pursuing a strategy of geo splits – restructuring their portfolio along geographical lines to optimise business operations and attract potential buyers.

A rise in exits to corporates

With less of a push to sell in order to raise new money from Limited Partners (LPs), many GPs chose to delay or postpone exits in 2024; however, exits to corporates were up.

Looking Forward

The Asia Pacific fund landscape will consolidate and converge

The Asia Pacific PE fund landscape is both maturing and morphing, with convergence into fewer, larger funds and a corresponding expansion of fund operations in the region. A transition from growth-oriented investment to operation-oriented buyouts is also apparent and will drive GPs to expand their in-house operational capabilities.

Emergence of the ‘zombie‘ fund

Some small and mid-cap funds will enter a state of suspension as managers, seeing little hope of raising a new fund, will have a reduced incentive to exit investments, choosing to hold onto assets in the hopes of higher valuations in the future.

2025 looks set to be a year of growth, albeit one that may have to contend with shocks and volatility originating outside the region

Corporate confidence will fuel optimism and drive dealmaking, which may in turn fuel greater confidence for PE funds to sell portfolio assets.