Three ways mature AI adopters can capture more digital value

Deloitte analysis finds that organizations with higher AI maturity consistently achieve more value from digital initiatives. What differentiates them, and why do they outperform?

Artificial intelligence adoption is more than a technology refresh. It represents a fundamental shift in business strategy. An organization’s AI maturity can directly affect enterprise value, but many organizations struggle to identify and measure their level of AI maturity.

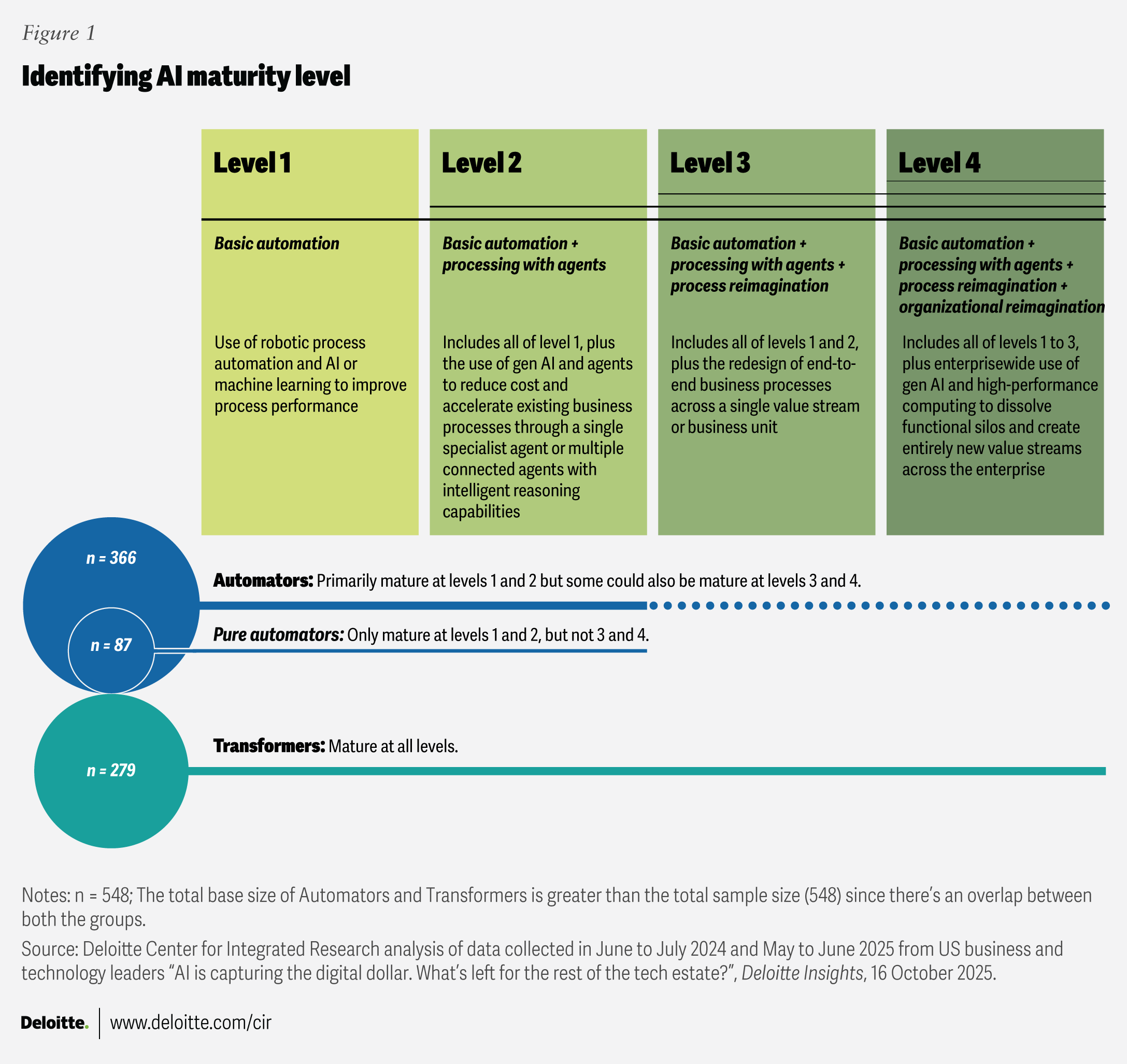

To clarify the path forward, Deloitte mapped AI adoption across four levels of maturity (figure 1): basic automation (level 1), building on agent-based processes (level 2), process reimagination (level 3), and organizational redesign (level 4).

While there is strong evidence that AI automation and agents can deliver value,1 C-suite leaders are often asking a deeper question: Do more mature AI adopters, on the higher end of the maturity spectrum, achieve meaningfully higher value—and if so, what do they do differently? Our analysis of AI maturity levels indicates that mature AI adopters lead across nearly all value measures compared with their less mature counterparts, grounded in three key behaviors:

- Mature AI adopters don’t fund AI in a vacuum. They invest more broadly in cloud, modern data, connectivity, and other scaling technologies, and report higher return on investment from AI and generative AI initiatives.

- Mature AI adopters are more likely to track the full suite of metrics in Deloitte’s 46-KPI digital transformation framework, which tracks financial, customer, process, workforce, and purpose indicators for 2023 to 2025. They also lead in measuring outcomes for growth, not just cost and efficiency.

- Mature AI adopters allocate significant digital budget to monetization and lead across monetization plays, treating AI as a new revenue creator rather than just a productivity tool.

Using data from Deloitte’s 2025 Tech Value Survey of nearly 550 leaders across five industries, we analyzed the four AI adoption maturity levels and grouped respondents into two personas: Automators and Transformers. Automators operate primarily in the foundational stages (levels 1 and 2). While Automators use single-agent workflows to deliver basic automation, Transformers use multi-agent processes and have advanced to broader organizational reimagination to drive greater value across the organization (figure 1). Because AI maturity builds incrementally over time, Automators can eventually evolve into Transformers, reflecting some overlap between the groups. Think of Transformers as the “fully scaled” persona that is both automating and transforming. Even marginal differences can compound into measurable enterprise value for Transformers.

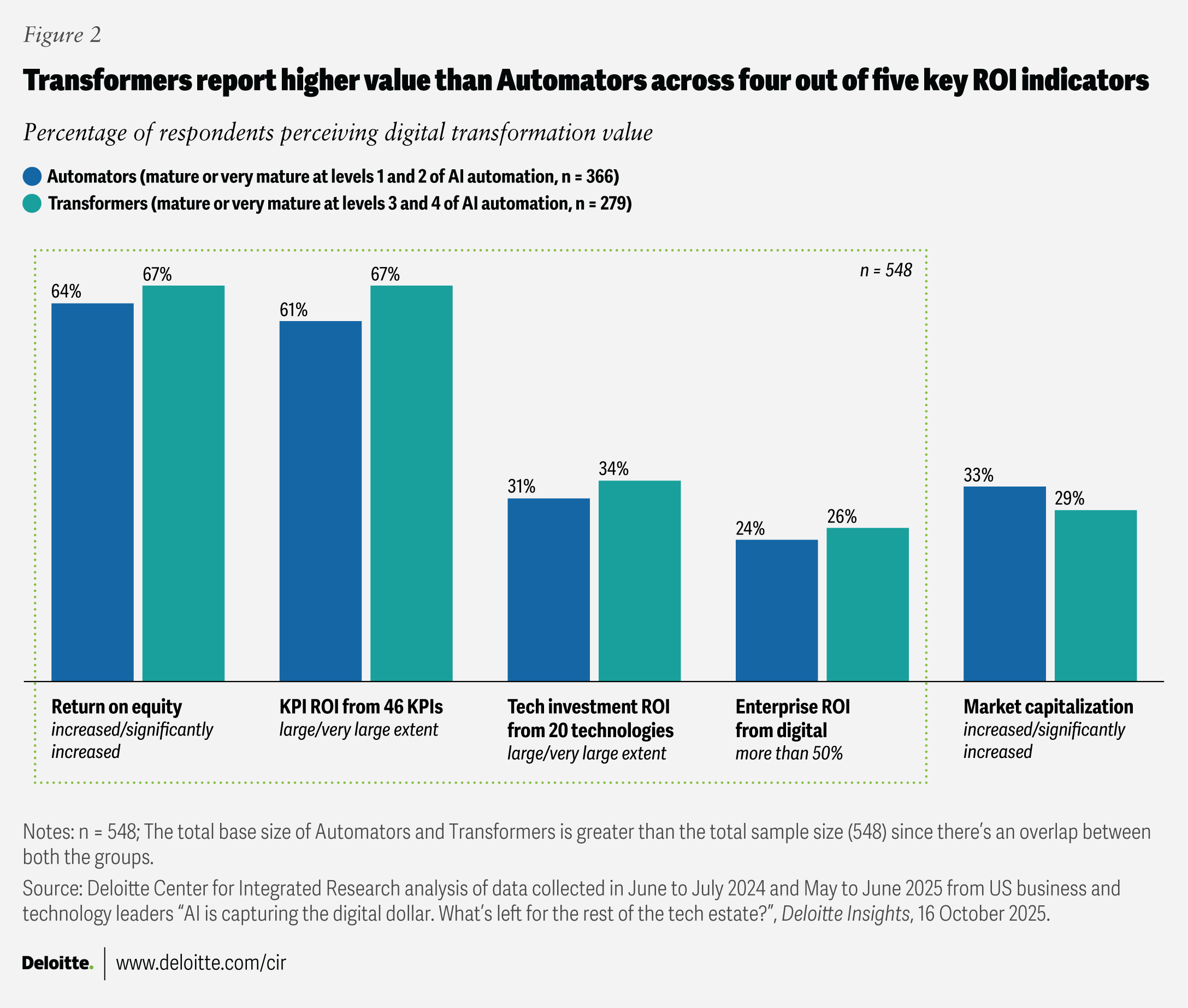

By analyzing the two personas, we found that Transformers outperform Automators across nearly all ROI measures—tech investment ROI, ROI relative to key performance indicators, enterprise value from digital initiatives, and return on equity (figure 2).

For example, 67% of Transformers identified in our survey report achieving large or very large ROI across all 46 KPIs, compared with 61% of Automators. While the difference may seem modest, Transformers consistently report outsized returns across the most strategic business areas, including growth and customer measures. That’s likely because Transformers focus on rewiring end-to-end journeys through multi-agent, cross-functional redesign, so the growth shows up in harder-to-move KPIs, such as digital sales, digital product effectiveness, and net promoter score (NPS), where Automators tend to lag.

The approach to automation versus transformation is fundamentally different: Automators focus on process optimization; Transformers rearchitect the enterprise.2 As a result, a small gap can become material when it compounds across the enterprise at scale. For example, a retailer might use a single agent to reduce customer service handling time (automation), while a Transformer would orchestrate agents across the supply chain to reduce stockouts, adjust prices, and improve recommendations, possibly improving conversion and NPS, not just cost per contact.3 As this gets scaled across thousands of products, millions of customer interactions, and multiple regions and brands, the value multiplies.

What drives this performance advantage? The difference is not just maturity—it is behavior related to tech investment, KPI measurement, and budget allocation that helps set Transformers apart.

Transformers often believe AI can scale only when the whole tech estate scales with it

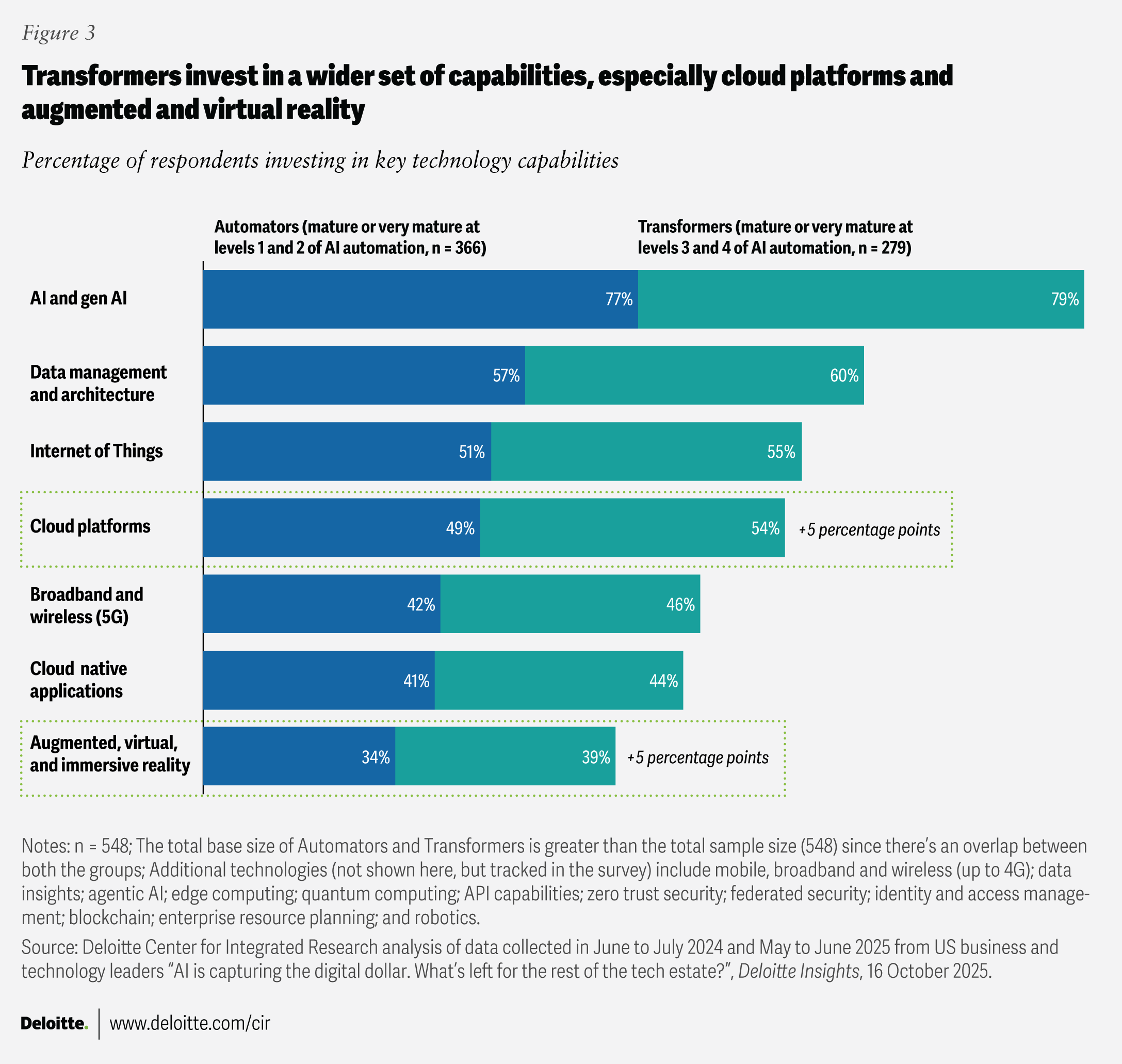

Transformers in our survey invest more broadly across technologies. Rather than funding AI in isolation, they advance AI alongside foundational scaling technologies—cloud platforms, modern data environments, connectivity, and immersive and experiential technologies (figure 3).

This is a notable departure from the overall investment patterns in Deloitte’s 2025 Tech Value Survey, which warned that many respondents risk overfunding AI to the detriment of the broader tech estate. As part of our analysis of AI maturity levels, we segmented the same data set by AI adoption maturity and found that Transformers invested in a wider set of capabilities.

The largest gaps compared with Automators appear in cloud platforms and augmented, virtual, and immersive reality—each with a 5-percentage-point difference. This suggests that organizations that have scaled AI applications have now turned their attention to the infrastructure needed to support them.4

Transformers also report stronger returns from AI itself. Transformers reported the strongest AI and gen AI ROI (72%), outpacing Automators by 5 percentage points. This suggests that AI value emerges when the underlying technology system is upgraded in parallel, not when AI is constrained by legacy infrastructure or siloed strategies. This insight underscores the importance of foundational infrastructure in advancing AI maturity.

Transformers tend to measure what matters for growth—not just efficiency

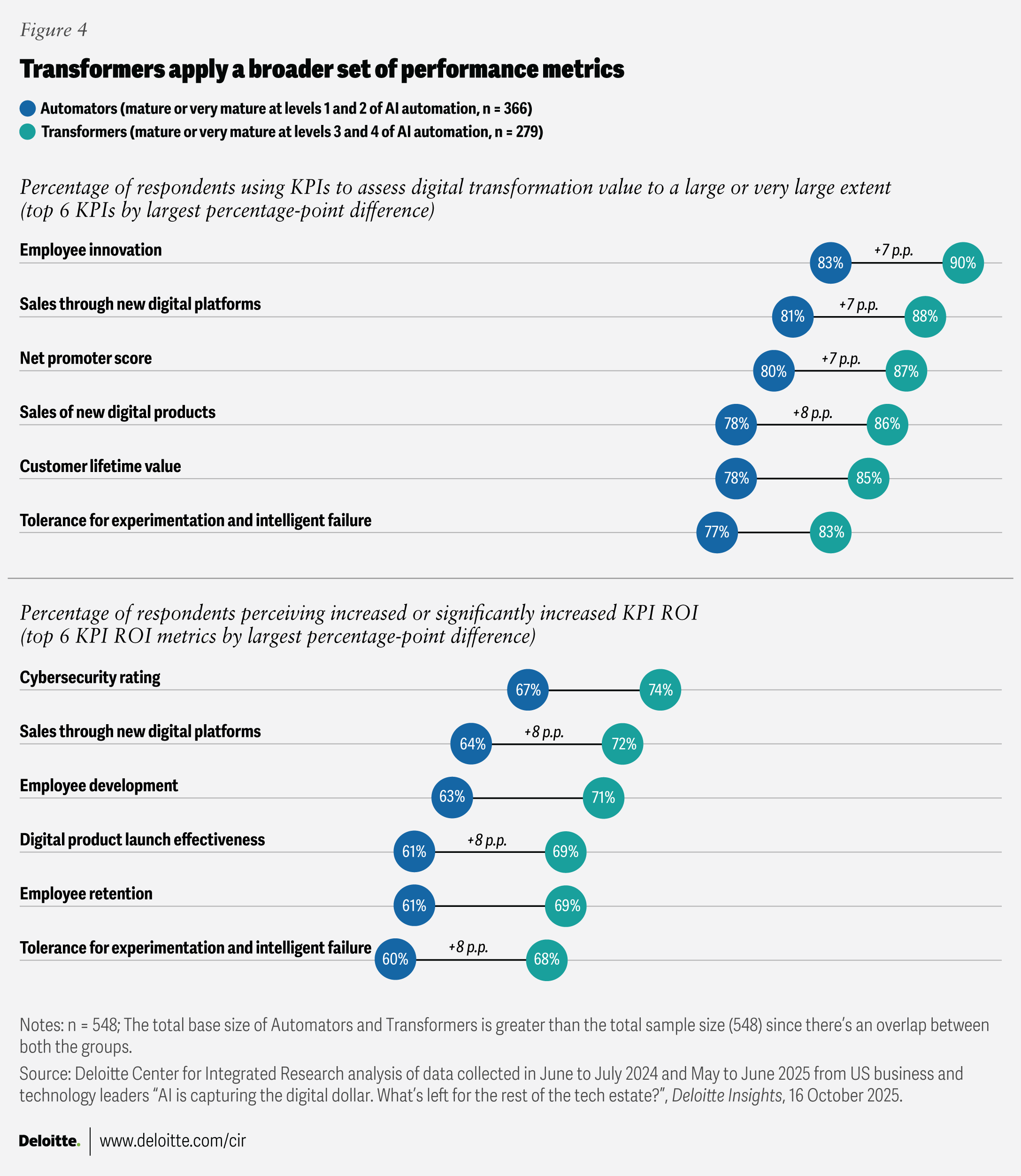

Transformers tend to apply a broader set of performance measures across Deloitte’s 46-KPI digital transformation framework. In 2025, 73% of Transformers surveyed reported using all 46 KPIs frequently or very frequently, compared with 69% of Automators surveyed. The largest gaps appear in financial and customer measures: Automators trail by 7 to 8 percentage points in tracking metrics such as employee innovation, sales through new digital platforms, sales through new digital products, and NPS (figure 4).

These measures become increasingly important as AI programs mature. Transformers outperform Automators in KPI-linked ROI by a meaningful margin—especially in areas such as sales through new digital platforms, digital product launch effectiveness, and tolerance for experimentation and failure. This points to a pattern: AI maturity is closely tied to digital sales strategy and a culture of experimentation. Transformers surveyed distinguish themselves through innovation, new product and platform development, customer advocacy, and workforce creativity.

In short, AI performance tends to improve when innovation becomes systematic rather than episodic. Single-agent automation can thrive without systemic changes, but multi-agent systems and organizational transformation may require greater changes across processes and performance measures.

Transformers tend to shift budgets toward new value and operationalize monetization

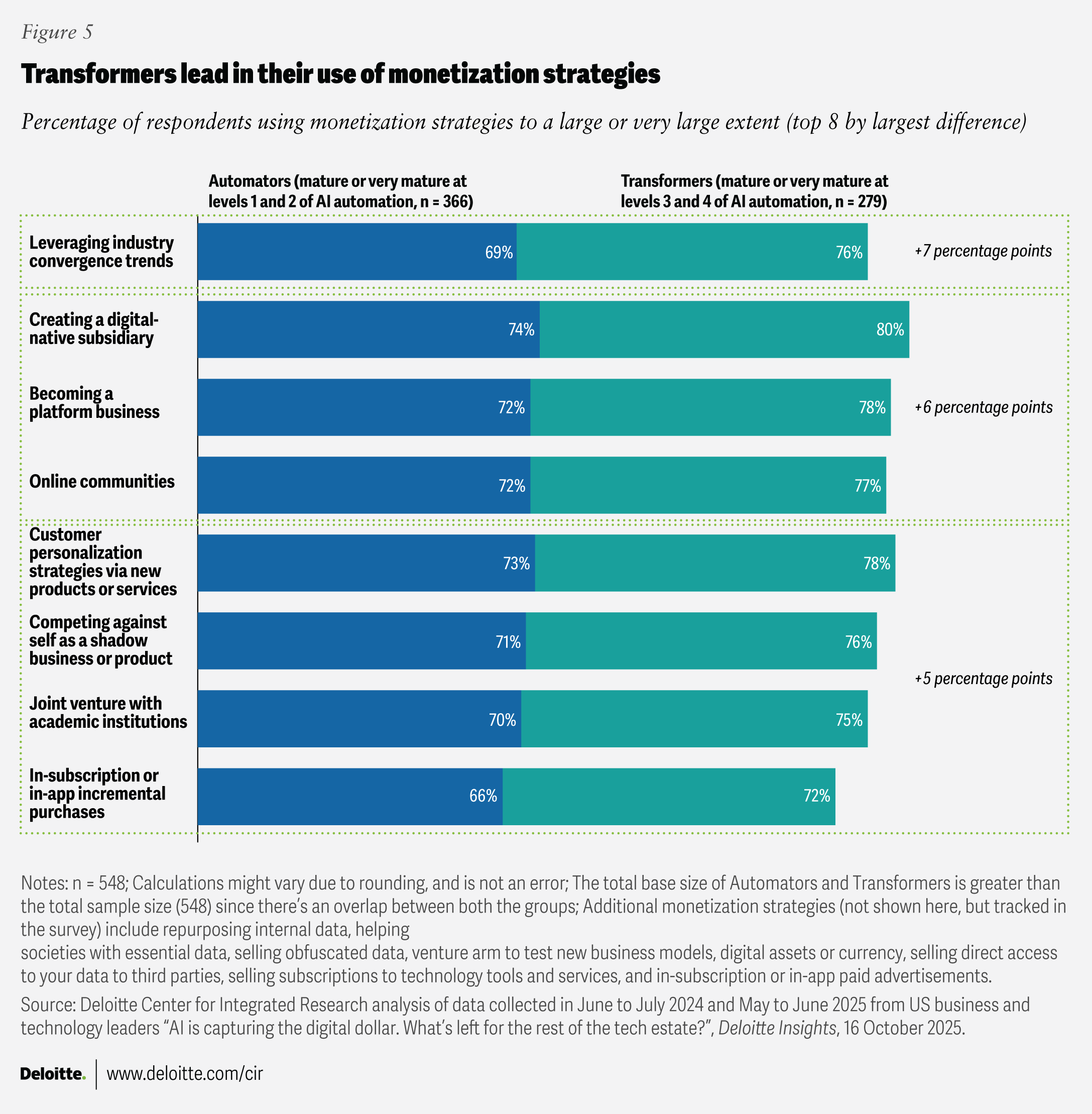

Surveyed Transformers are not only capturing existing value; they are also often building new revenue streams. Our data indicates that they allocate more of their digital budgets to monetization and deploy a wider array of strategies to create new sources of value.

When asked how much of their digital budget is allocated to monetization, 74% of Transformers surveyed reported allocating 21% to 50%, compared with 69% of Automators. This gap is notable and could reflect efforts to recoup ROI from earlier data transformation investments, as well as the reality that, at scale, data itself becomes a more valuable asset.5

Transformers also lead across all 16 monetization strategies we measured. The largest differences appear in creating digital-native subsidiaries, becoming platform businesses, building online communities (6 percentage points each), and leveraging industry convergence trends (7 percentage points).

Together, these behaviors signal an inflection point in scaling AI to value. For Transformers, mature AI adoption is not just an efficiency play—it helps enable organizations to reimagine value creation and pursue emerging markets ahead of competitors.

Not every use case requires reinvention. As advanced AI technologies are tapped to automate tasks across single and connected value chains, some instances may simply require basic automation or a more intelligent version of today’s processes.6 But our analysis suggests that Transformers pursue additional value beyond optimization—tracked through measures that reflect growth and competitive advantage—indicating that unlocking additional value often requires a strategy beyond incremental process improvement.

Automators to Transformers: Moves leaders should consider making now

As organizations debate whether AI delivers value, our analysis shows how value appears across a scaling maturity curve. Transformers surveyed consistently report higher returns than Automators, even with partial overlap between the groups. The difference isn’t AI activity alone—it’s enterprise-level behavior: investing across the foundational technology estate, measuring value beyond efficiency (including growth and innovation KPIs), and allocating meaningful budgets to monetization.

The question is not just whether AI maturity pays off. It’s also whether organizations are prepared to move beyond optimization and operate like Transformers. The goal should be to scale programs that don’t just improve performance but create advantage. Achieving that goal will likely require shifting from an optimization-first mindset to a holistic strategy that aims to optimize, protect, and create new value.

Continue the conversation

Meet the industry leaders

Tim Smith

Garima Dhasmana

Diana Kearns-Manolatos

BY

Tim Smith

Garima Dhasmana

Diana Kearns-Manolatos

Iram Parveen

We thank David Levin for his support with the survey questionnaire, fielding, analysis, and vendor management; and Rajesh Medisetti for his support with the Tableau dashboard development. We are also grateful to the Deloitte Insights team, including Corrie Commisso for her editorial input, Sofia Laviano for her creative vision, and Blythe Hurley and Prodyut Borah for production support.

Our appreciation goes to the marketing team—Ireen Jose, Rachel Freya Rosenberg, Sarah Q. Long, and Saurabh Rijhwani—for their guidance and leadership in extending the impact of these insights.

Editorial (including production and copyediting): Corrie Commisso, Prodyut Borah, Anu Augustine, Cintia Cheong, and Sayanika Bordoloi

Design: Molly Piersol

Cover artist: Sofia Laviano

Knowledge services: Rohan Singh

Visit the Deloitte Center for Integrated Research

Access more insights on some of the most complex issues facing businesses today.