The Deloitte Consumer Tracker Q1 2026

Consumer confidence experienced its biggest fall in four years

|

Want to look at the data in more detail including by age or income group? Click here to view demographic breakdown. |

|

The results of the latest Deloitte Consumer Tracker survey show how the impact of recent geopolitical events on prices have created yet another setback for consumers. Many were already facing a squeeze on their household budgets at the start of the year with wage growth slowing and the job market deteriorating. The prospect of another increase in the price of essentials particularly the cost of energy, has hit consumer confidence hard with our index trending downwards to levels last seen four years ago.

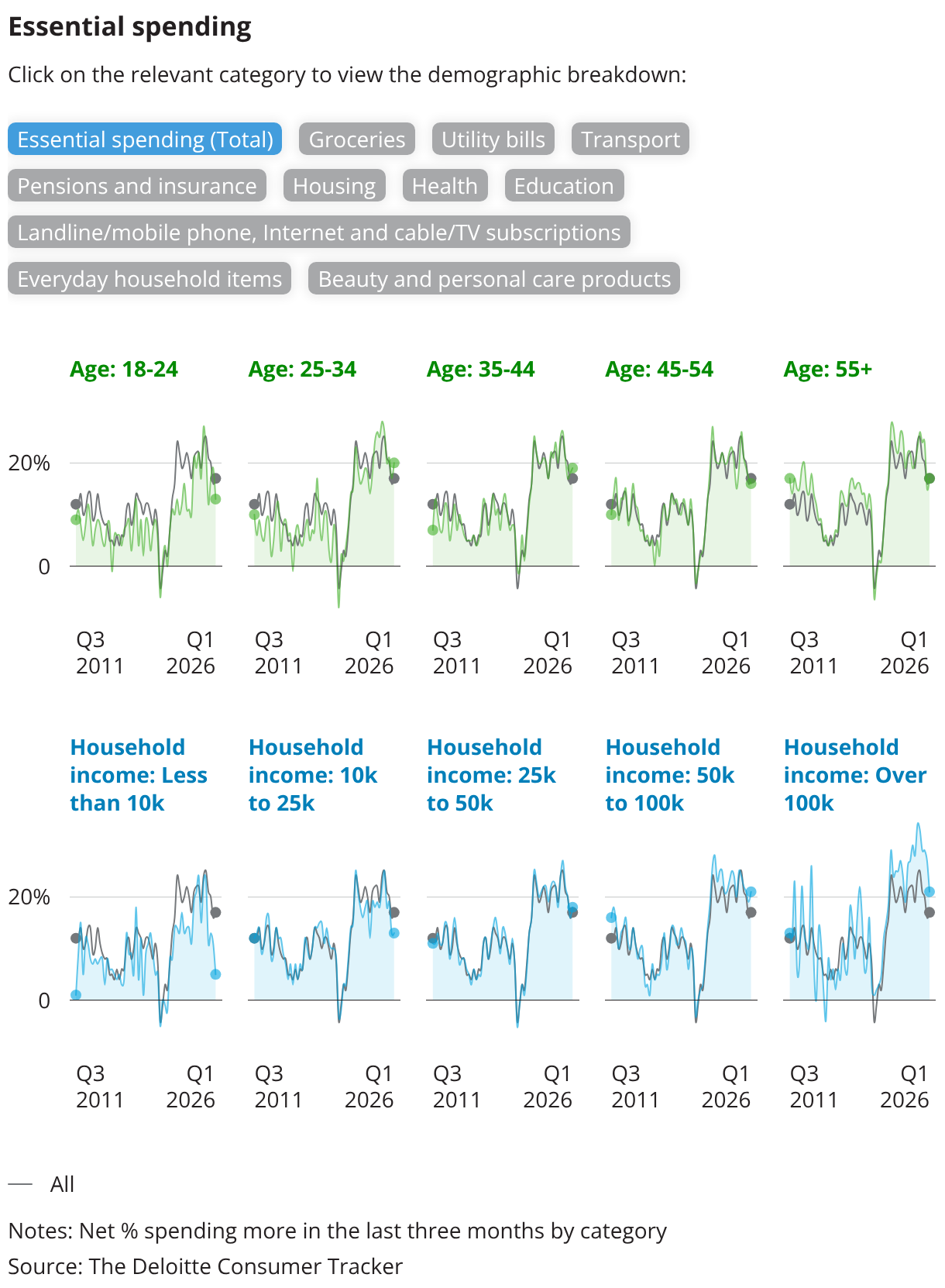

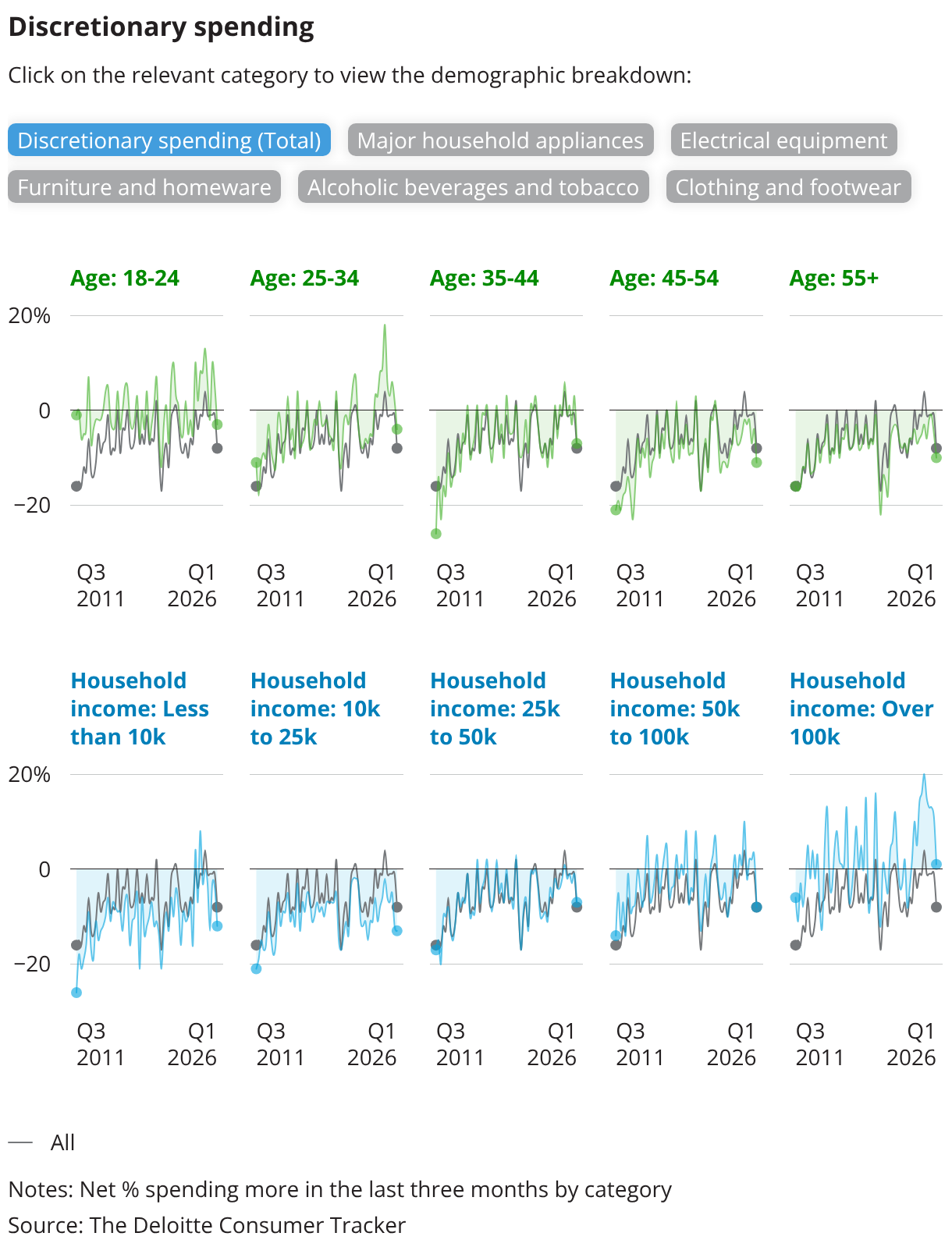

At the same time, consumer discretionary spending has fallen to its lowest level in three years. While there would typically be a drop off in spending in January after the end of year busy festive shopping period, the fall seen in Q1 is more representative of consumers consciously cutting back on non-essentials. Essential spending although unchanged remained high, with consumers allocating most of their budget to everyday items that are particularly vulnerable to inflation. Our data also shows big-ticket purchases stayed subdued, with fewer people planning to buy a car, a house or even a major appliance or piece of furniture compared with a year ago.

Overall, for consumer sentiment and spending to improve, households will want to see a more certain outlook for the economy. This means the long-awaited rebound in consumer spending might yet take more time.

Key findings Q1 2026

- Consumer confidence experienced its biggest drop since Russia invaded Ukraine four years ago. The Deloitte Consumer Confidence Index dropped 3 percentage points from -11.1% in Q4 2025 to -14.1% in Q1 representing the largest fall in confidence since Q1 2022, putting the index at its lowest level since Q3 2023. Overall confidence was also down 6.3 percentage points year-on-year.

- The fall in the overall confidence was driven by a drop across five of the six measures included in the index. In particular, a significant decline in confidence about household disposable income, and worsening sentiment around job security, job opportunities and career progression drove the decline in overall consumer confidence. Sentiment towards levels of household disposable income saw the most significant fall (down 7.2 percentage points from Q4 2025 and 9.5 percentage points year-on-year). This also marked the measure’s largest quarterly decline since Q1 2022. Meanwhile, sentiment towards job security was down 2.1 percentage points on the previous quarter and 6.2 percentage points year-on-year.

- Consumer sentiment about the state of the UK economy also fell significantly and is back to levels last seen at the end of 2022 when inflation reached an historical high. The measure of confidence in the UK economy, which is separate from the main index, fell 13.5 percentage points to -69% in Q1 2026 from -56% in Q4 2025, representing the biggest fall since Q4 2024 and returning to levels last seen in Q4 2022.

- Discretionary spending reached a three-year low, falling by 7 percentage points reaching its lowest level since Q1 2023 just months after the UK saw inflation reach an historical high of 11.1%. While we expect elements of seasonality in Q1, this drop represents the biggest fall since Q2 2020 when the UK was the midst of a global pandemic. This was driven by a fall in spending across all non-essential categories, namely on clothing and footwear (down 11 percentage points on Q4 2025, and 10 percentage points year-on-year) and alcoholic beverages and tobacco (down 15 percentage points on Q4 2025, and 7.7 percentage points year-on-year). The year-on-year drop was also significant across bigger ticket items, especially for major household appliances (down 4 percentage points) and electrical equipment (down 7 percentage points).

- Overall spending on essentials was relatively flat. With the increase in the cost of fuel consumers spent significantly more on transport but spent less in most other essential categories. At the same time, in a sign of pressures on budgets, almost a third of consumers (29%) agree that they are only spending on essentials, up from a quarter (25%) in Q4 2025.

- Consumers are consciously cutting down. Our data also shows that of those consumers who said they spent less, 50% attributed this to spending on fewer items to save money (up from 44%). There was also an increase in the total number of consumers reporting being more careful with their money, with nearly half (45%) saying they are being more frugal with their overall spending (up from 39% the previous quarter). Similarly, there was a five-percentage point increase in consumers consciously cutting down on any luxuries or treats (37%).

- Consumers blame higher prices. Of those consumers who said they spent more in the last three months, there was a nine percentage point increase in those attributing this to prices going up (79%, up from 70% in Q4 2025).

- Spending on travel remains the exception for now. Our data shows fewer are reporting spending more on experience and leisure with the exception of holiday budget which remains ring-fenced.

- Consumers say they are using their savings more. With consumers reporting an increase in their overall expenditure compared with the end of last year, there are also signs in the data that people are starting to use their savings or credit cards more. Looking ahead, many consumers expect their overall spending to continue to increase and expect to continue to use their savings to maintain similar living standards.

|

Want to look at the data in more detail including by age or income group? Click here to view demographic breakdown. |

|