Time for a tax residency refresh: How does it apply to individual taxpayers?

December 2024 - Tax Alert

By Jayesh Dahya & Mila Robertson

Understanding tax residence is essential. A person's or entity's tax residence status determines their tax obligations, including whether they are taxed on worldwide income or only on New Zealand sourced income.

In November Inland Revenue released a draft interpretation statements “Tax residence” (with accompanying reading guide and three fact sheets) and “Tax residence - government service rule” for public consultation.

The documents are a refresh of the 2016 guidance, IS16/03 Tax residence. Included in this refresh are an overview of the tax residency rules for individuals, companies, and trusts. This article focuses on Part 1 only, which is how the tax residency rules apply to individuals, including the government service rule.

The updates for individual residency largely look to simplify the prior guidance but does offer some new material, including examples to clarify issues we see in practice, such as individuals inadvertently electing out of the transitional residence rules (meaning they lose their temporary tax exemption on most foreign sourced income).

Tax residence for individuals

In New Zealand, the tax residence status of individuals is crucial, as New Zealand has a residency-based tax system, as opposed to a territorial tax system. Tax residency therefore determines whether a person is taxed on worldwide income or only on New Zealand-sourced income. The draft statement does not make any substantive changes to the previous guidance in relation to tax residency for individuals and by way of recap the relevant principles and tests are as follows:

Permanent Place of Abode Test

This test is the overarching test for establishing tax residence for individuals and applies “despite anything else”. A person is considered a New Zealand tax resident if they have a permanent place of abode in New Zealand, regardless of other circumstances or even also having a permanent place of abode overseas.

Case law has established that a "place of abode" generally refers to a physical dwelling, such as a house or apartment, that a person has a continuous and substantial association with. It does not require ownership; rented properties, family-owned homes, or properties held in a trust can also qualify as a place of abode. What’s key is that the dwelling serves as a habitual residence, where the individual resides from time to time in a stable and enduring manner.

Assessing a permanent place of abode requires an overall assessment of the circumstances and involves looking at the individual’s family, economic, and social ties, as well as their connection to the property. Specific factors may include:

- Family and social ties: close family members residing in New Zealand, established friendships and social networks can strengthen a person’s association with New Zealand as a primary residence.

- Economic and business ties: New Zealand-based employment, business activities, or property ownership are indicative of a connection that could make the place an enduring residence.

- Intentions and personal circumstances: frequent visits or ongoing commitments to a property in New Zealand, even if living overseas, often signify that the dwelling functions as a “permanent” residence.

Determining if an individual has a permanent place of abode can be complex, hence Inland Revenue devoting 24 pages of the draft statement to this issue.

183-Day Rule

An individual is also New Zealand tax resident if they spend over 183 days in New Zealand during any 12-month period (not an income year or calendar year). Once the 183-day threshold is reached, the individual is deemed tax resident from the first day of presence within that 12-month period and generally has more relevance to new migrants to New Zealand who may not establish a permanent place of abode when they first arrive.

325-Day Rule

To cease New Zealand tax residency, an individual must meet the 325-day rule, which requires them to be absent from New Zealand for more than 325 days in any 12-month period. In addition, they must also relinquish any permanent place of abode in New Zealand. The 325-day rule does not apply to those in New Zealand government service abroad (discussed further below).

What’s New

For individual tax residence, the draft statement includes new content covering:

- A paragraph acknowledging the existence of a domestic law exemption for employment income derived during short term visits to New Zealand – known as the 92-day rule.

- Comments on tax residence requirements to be eligible for Working for Families Tax Credits (WfFTC). As a result of transitional residents inadvertently claiming Best Start tax credits when receiving automated Inland Revenue notifications offering “free” money, additional paragraphs have been included to make it clear that claiming WfFTC (specifically Best Start) is treated as an election for the individual and their partner to opt out of being a transitional resident. It has also been made clear that FamilyBoost is not part of the claiming WfFTC regime.

- Additional guidance on the habitual abode test under the double tax agreement (DTA) tiebreaker provisions, noting that the focus is generally on where the person resides during the period of dual residence and in some cases it may be appropriate to consider additional periods that are outside the period of dual residence.

The Government service rule

The “government service rule” previously included in IS16/03 has been removed and a separate statement has been issued. The draft statement consolidates the changes outlined in Commissioners Statement CS 21/02 where it clarifies that a person leaving New Zealand to take up a position in the service of the New Zealand Government overseas does not need to have been in the service of the New Zealand Government before taking up that position for the government service rule to apply.

What is the Government service rule?

Essentially, individuals who are tax resident under the 183-day rule when they start their service and are working overseas in the services of the New Zealand Government will always remain tax resident of New Zealand. This is even if they no longer have a permanent place of abode and meet the 325-day rule.

Who is covered by the Government service rule?

The government service rule covers the following:

- Employees of Government departments and agencies;

- Members of the New Zealand defence force and police; and

- Employees of another public body if the public body is closely controlled by the Government. This would include most public bodies outlined in the Crown Entities Act 2004.

The government service rule does not include:

- Employees of state-owned enterprises

- Employees of autonomous public entities such as school boards of trustees or tertiary institutions

The government service rule does not apply to an individual’s spouse/partner or child who are overseas with someone in the service of the New Zealand Government. The tax residence status of family members is determined independently.

When does the rule apply?

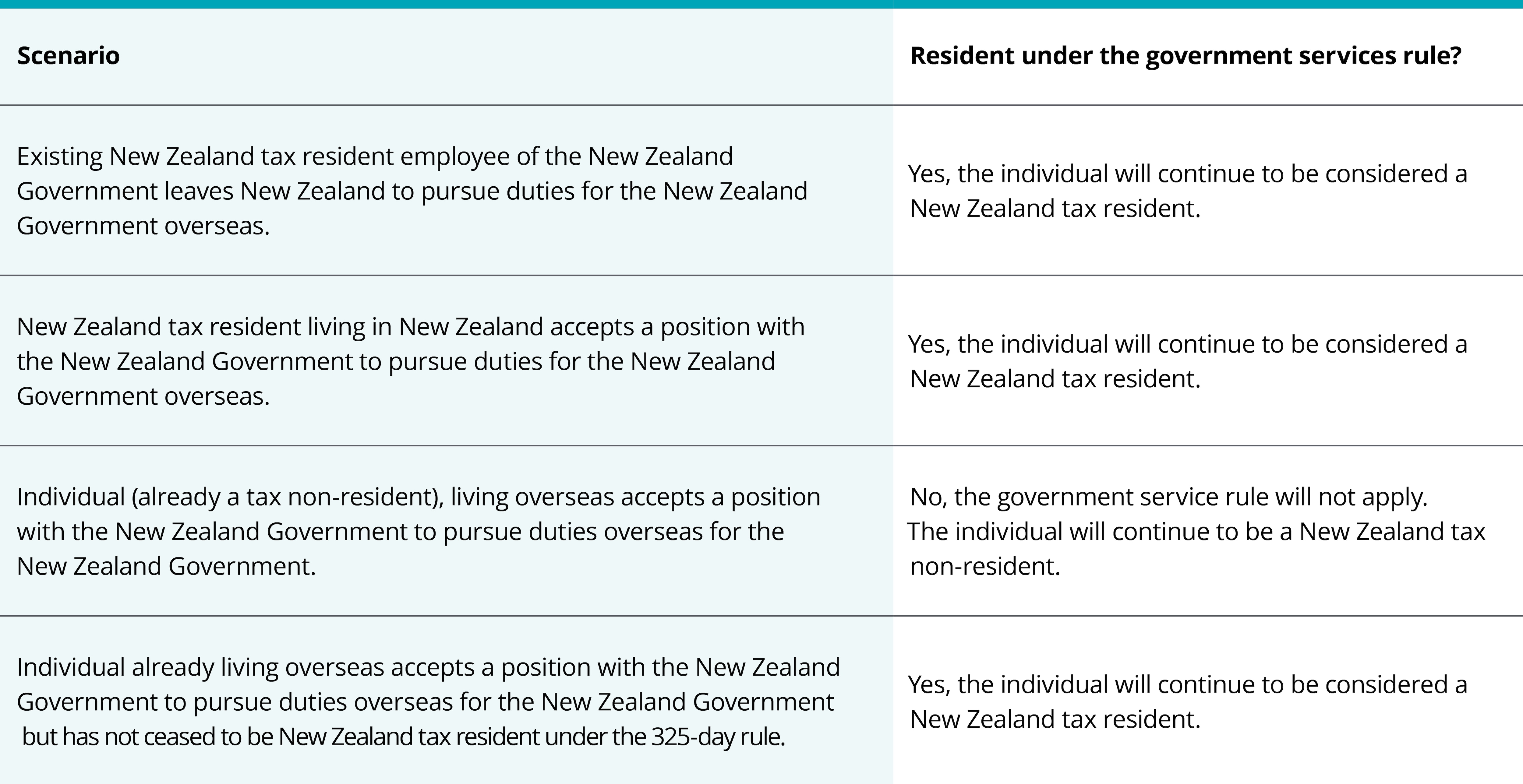

The following scenario’s set out when the government service rules apply.

The last two scenarios show that the Inland Revenue interpretation of the government service rule can give rise to an odd result, depending on whether the individual takes up employment for the New Zealand Government pre or post meeting the 325-day threshold.

What if there is a Double Taxation Agreement (DTA)?

When an individual is considered a New Zealand tax resident due to Government service and a tax resident of the country they are living in, and there is a DTA between New Zealand that country, the government services article in that DTA needs to be considered.

Generally, New Zealand retains the right to tax the individual’s government salary and benefits. However, in some situations the other country may have the sole right to tax the employment income of the individual under the DTA residence tie breaker tests and the individual:

- Is a national of the other country, or

- Did not become a tax resident of the other country solely for the purpose of rendering government service for New Zealand.

In these scenarios, it will be necessary to consider the circumstances of the individual to determine if New Zealand retains taxing rights.

If there is no DTA, there are potential double taxation issues for the individual.

Deloitte comment

As acknowledged by Inland Revenue, the guidance documents are essentially a refresh of the previous statement with no substantial change in the interpretation of these rules.

In our experience, Inland Revenue are quick to conclude the existence of a permanent place of abode in New Zealand. For example, when there is a holiday home in New Zealand that is regularly occupied through the course of the year. It would be helpful for some additional guidance or examples of how these types of scenario would be interpreted by the Inland Revenue when dealing with individuals who may spend time in New Zealand in holiday homes without any other substantive ties.

Submissions on these consultation documents close on 11 December 2024 and if there are any points you think should be considered, or you have questions about your own tax residence, please contact your usual Deloitte advisor.

December 2024 - Tax Alerts

- New Tax and Social Policy Work Programme sets the tax policy scene

- Tax and tinsel: A guide to taxing holiday perks

- Gift cards and trade rebates: Inland Revenue sparks tax debate

- Time for a tax residency refresh: How does it apply to individual taxpayers?

- Mix and match: Mixed use rentals

- A problem shared is a problem halved — Inland Revenue and MBIE’s new information sharing agreement

- Snapshot of Recent Developments