A problem shared is a problem halved — Inland Revenue and MBIE’s new information sharing agreement

December 2024 - Tax Alert

By Joe Sothcott & Robyn Walker

Sharing is caring, right? At least, that seems to be the sentiment behind the new information-sharing agreement between Inland Revenue and the Ministry of Business, Innovation and Employment (MBIE). This agreement, known as an Approved Information Sharing Agreement (AISA), was released for consultation at the end of October.

So, what exactly is an AISA? Essentially, it’s a framework set out in the Privacy Act 2020 that allows public agencies to share information that would otherwise be restricted by that Act. The goal is to create a flexible mechanism to support services by sharing information while being transparent about the types of information shared. In this case, the proposed AISA is between Inland Revenue and the Market Integrity (MIB) and the Business and Consumer (BCB) Branches of MBIE.

Currently, three Memorandums of Understanding allow limited information sharing between Inland Revenue and MBIE. However, the Tax Administration Act 1994 and the Privacy Act 2020 still prevent some information from being shared. That’s where the proposed AISA comes in—it aims to help both agencies perform their functions more efficiently and save on costs.

Inland Revenue is different to many agencies in that it has extensive information gathering powers already, so it's worth noting that while Inland Revenue could request this information from MBIE under section 17 of the Tax Administration Act 1994, they prefer not to because it lacks “transparency and public scrutiny.” MBIE has less access to information, so it stands to benefit the most from having access to more data from Inland Revenue.

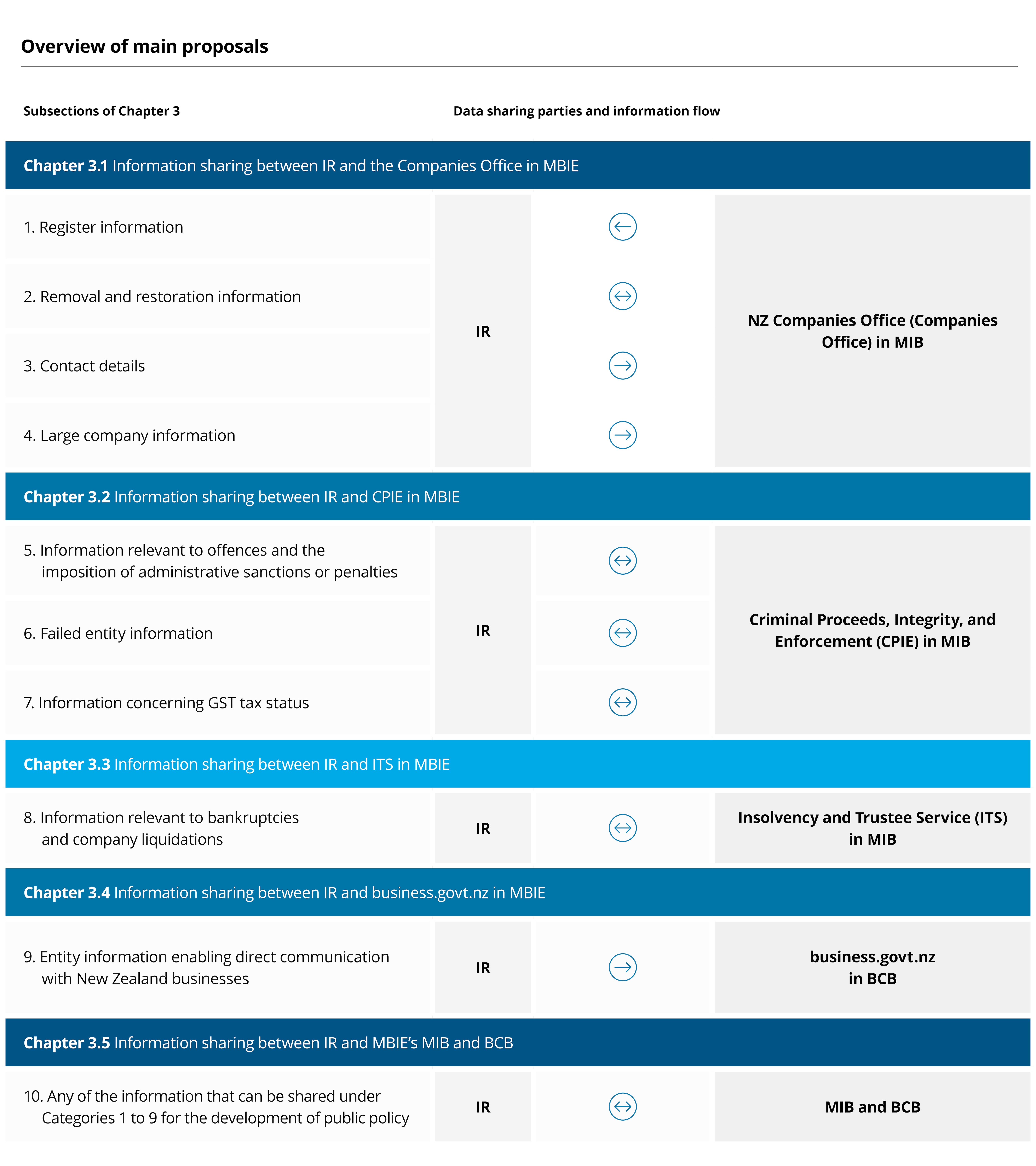

The types of information to be shared and the direction of travel are set out below in this handy table :

The table hints at why the Government would like to implement the AISA. A big reason is phoenix companies—where new companies are set up in the ‘ashes’ of a financially failing company, leaving prior creditors burnt. The consultation document says that whilst this is a known issue, the scale of the problem is unknown due to difficulties in collecting data.

Other reasons include cracking down on non-compliance—particularly people acting as a company director where they have previously been added to the register of banned directors— and getting important information out to relevant New Zealand businesses.

A key benefit of the AISA is increased cooperation between Inland Revenue and MBIE. It will assist in preventing and identifying offences, ensuring appropriate penalties are imposed. For instance, information sharing between Inland Revenue and MBIE’s Criminal Proceeds, Integrity, and Enforcement Unit (CPIE) will help detect and prosecute offences. However, in this case information sharing will only occur if:

- The sharing party has reasonable grounds to suspect that an offence has been, is being, or is likely to be committed, and

- Believes the information is relevant to the other party's ability to detect, investigate, or prosecute that offence.

The AISA also supports the administration and governance of various regimes managed by the two agencies and provides more direct ways to share information. Finally, the consultation document mentions that information can be shared for policy development.

The deadline for submissions is 13 December 2024. The Government is particularly interested in hearing:

- If the issues outlined are of concern.

- Whether information sharing would address the problems.

- Whether there is support for the categories of information proposed to be shared.

- Whether there are sufficient safeguards for the protection of people’s information.

Once the consultation is complete, the AISA will undergo further review by the Privacy Commissioner before heading to Cabinet to be passed as secondary legislation via an Order in Council. After implementation, Inland Revenue and MBIE will annually review the AISA's operation and its safeguards' effectiveness.

Please get in touch with your usual Deloitte advisor if you have any questions about the proposed AISA.

December 2024 - Tax Alerts

- New Tax and Social Policy Work Programme sets the tax policy scene

- Tax and tinsel: A guide to taxing holiday perks

- Gift cards and trade rebates: Inland Revenue sparks tax debate

- Time for a tax residency refresh: How does it apply to individual taxpayers?

- Mix and match: Mixed use rentals

- A problem shared is a problem halved — Inland Revenue and MBIE’s new information sharing agreement

- Snapshot of Recent Developments