Tax and tinsel: A guide to taxing holiday perks

December 2024 - Tax Alert

By Katie-Rose Janmaat, Viola Trnski & Amy Sexton

The festive season is upon us! Time for giving, sharing, and navigating the tax treatment of Christmas-related expenditure. While the work Christmas party and gift-giving bring joy, they can also bring confusion when it comes to understanding the tax implications for both employers and employees. The key tax areas to consider are the FBT, PAYE and entertainment expenditure regimes. The different rules for each of these three tax regimes can seem to overlap and are a common source of confusion. No matter what your business is planning to do for Christmas with/for your employees and clients, it is likely that one of these three tax regimes will apply.

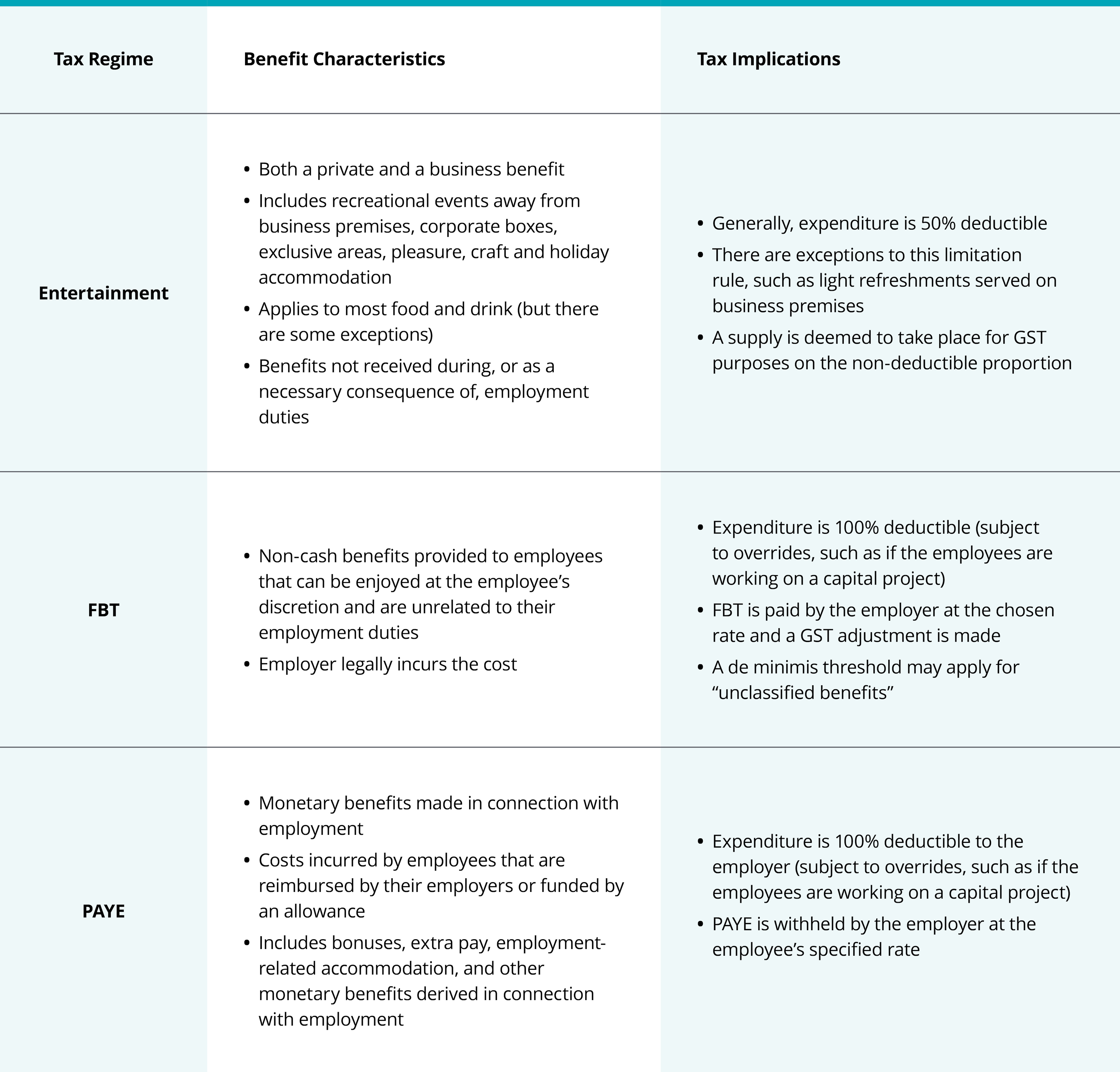

The entertainment expenditure rules limits tax deductions to 50% of costs for certain types of entertainment. The policy rationale for this is that a portion of entertainment expenditure (which is often food and drink related) contains a component of “private enjoyment”, even if consumed as part of a work event.

Normally, this type of expenditure will be captured by the entertainment regime, and override the FBT rules, unless:

- The employee can choose when to enjoy the benefit, or the benefit is enjoyed outside New Zealand; and

- The benefit is not received or used during, or as a necessary consequence of, the employee’s employment duties.

In these situations, the FBT rules trump the entertainment rules. An example of these contrasting rules would be if you took your staff out for a Christmas lunch, the entertainment rules would apply, but if, instead, you gifted employees a voucher for a restaurant to enjoy when they choose, the FBT rules will apply.

Finally, the PAYE rules will apply to any monetary compensation provided to employees in connection with their employment, think of things like bonuses, gratuities and holiday accommodation provided to employees.

The table below provides a quick summary of the regimes and their tax implications:

Common scenarios

Let’s look at some practical examples that may relate to your business

Costs associated with organising a Christmas party event off premises

Expenditure on food, drink and venue hire will be subject to the entertainment expenditure rules. Incidental costs like crockery, glassware, utensils and hiring waitstaff and/or music are also captured under the limitation rule. Only 50% of this expenditure is deductible.

Staff cash bonuses

Cash bonuses paid by an employer to an employee are taxable under the PAYE rules. These payments are made in relation to the employee’s employment and not a payment that is regularly included in the employee’s salary and wages (the legislation specifically provides for such payments). A cash bonus should be taxed for PAYE at the ‘’extra pay’’ rate.

Providing Christmas gifts to employees

Most gifts to employees are subject to FBT, as the benefits from these gifts can be enjoyed at the employee’s discretion. Similarly, gift baskets for employees containing food and drink, which could also potentially be considered an entertainment expense, would fall under the FBT rules for the same reason (that is, they can be enjoyed at the employee’s discretion).

Note that some benefits subject to FBT may qualify for an “FBT exemption” if certain requirements are met. For example, the de minimis exemption exempt unclassified benefits from FBT provided that:

- The total value of all unclassified benefits provided to all employees is less than $22,500 in the previous 12 months (this amount includes all benefits provided to all employees of associated employers); and

- No employee has received more than $300 of benefits in an individual FBT quarter ($1,200 for annual filers).

Unclassified benefits are those that are not specifically excluded from, or provided for, in the FBT regime. Common Christmas examples include vouchers, gifts, flowers, and non-work-related travel.

Vouchers to employees

If an employer were to give employees vouchers for a store or restaurant as a gift, and the employee can choose when to use the voucher and to whom to use the voucher on, the voucher will be subject to FBT. If the employer were to allow the employee go out for a meal and then reimburse this cost, it would then be subject to PAYE (as it is not a voucher).

Providing gifts to clients and customers

An oddity of the entertainment expenditure regime is that Inland Revenue considers that it applies to the provision of any food and drink, not just food and drink consumed at a function. Inland Revenue has confirmed this with an Operational Position that specifies that if a business provides a client or customer with a gift basket containing wine, cheese, towels, and soap, the tax outcome is that the cost of the towels and soap are fully deductible – but the wine and cheese is only 50% deductible!

From Us to You: Merry Christmas and a Happy New Year!

We hope this article clarifies some of the common misunderstandings that can occur between the different employment tax regimes. If you have any queries about the issues stated, please contact your usual Deloitte advisor.

The Tax Alert Team wishes you all a Merry Christmas and a Happy New Year and hopes you all enjoy a well-deserved break.

We’ll be back with our next issue of Tax Alert in February 2025.

December 2024 - Tax Alerts

- New Tax and Social Policy Work Programme sets the tax policy scene

- Tax and tinsel: A guide to taxing holiday perks

- Gift cards and trade rebates: Inland Revenue sparks tax debate

- Time for a tax residency refresh: How does it apply to individual taxpayers?

- Mix and match: Mixed use rentals

- A problem shared is a problem halved — Inland Revenue and MBIE’s new information sharing agreement

- Snapshot of Recent Developments