Shortfall penalties, the devil is in the detail

Tax alert - September 2025

The tax technical team at Inland Revenue’s Tax Counsel Office (TCO) has been very active publishing a number of draft consultation documents recently. As part of that flood of consultation items the TCO published five draft interpretation statements, accompanied by five draft fact sheets, (the draft IS) at the end of August. These documents specifically address shortfall penalties:

- PUB00498 Shortfall penalty for not taking reasonable care

- PUB00499 Shortfall penalty for taking an unacceptable tax position

- PUB00500a Shortfall penalty for gross carelessness

- PUB00500b Shortfall penalties – requirements for a “tax position” and a “tax shortfall”

- PUB00500c Shortfall penalties – reductions and other matters.

The first three draft IS (PUB00498-PUB00500a) represent a long-anticipated update of existing shortfall penalty guidance, originally published way back in 2004 and 2005. While the underlying definitions of each shortfall penalty remains unchanged, the draft IS have been revised to incorporate recent case law and reflect specific legislative changes. The final two draft IS (PUB00500b and PUB00500c) are welcome expanded guidance on the often misunderstood concepts of ‘tax position’, ‘tax shortfall’ and the criteria for shortfall penalty reductions.

Given the recent increase in Inland Revenue investigation activity, the release of new, clear, and accessible guidance documents on shortfall penalties is both timely and welcome.

But what are shortfall penalties?

To clarify, shortfall penalties are imposed by Inland Revenue when a taxpayer’s tax position is incorrect and results in insufficient tax being paid (creating a tax shortfall). Further detail on what constitutes a tax position and a tax shortfall will be discussed later in the article.

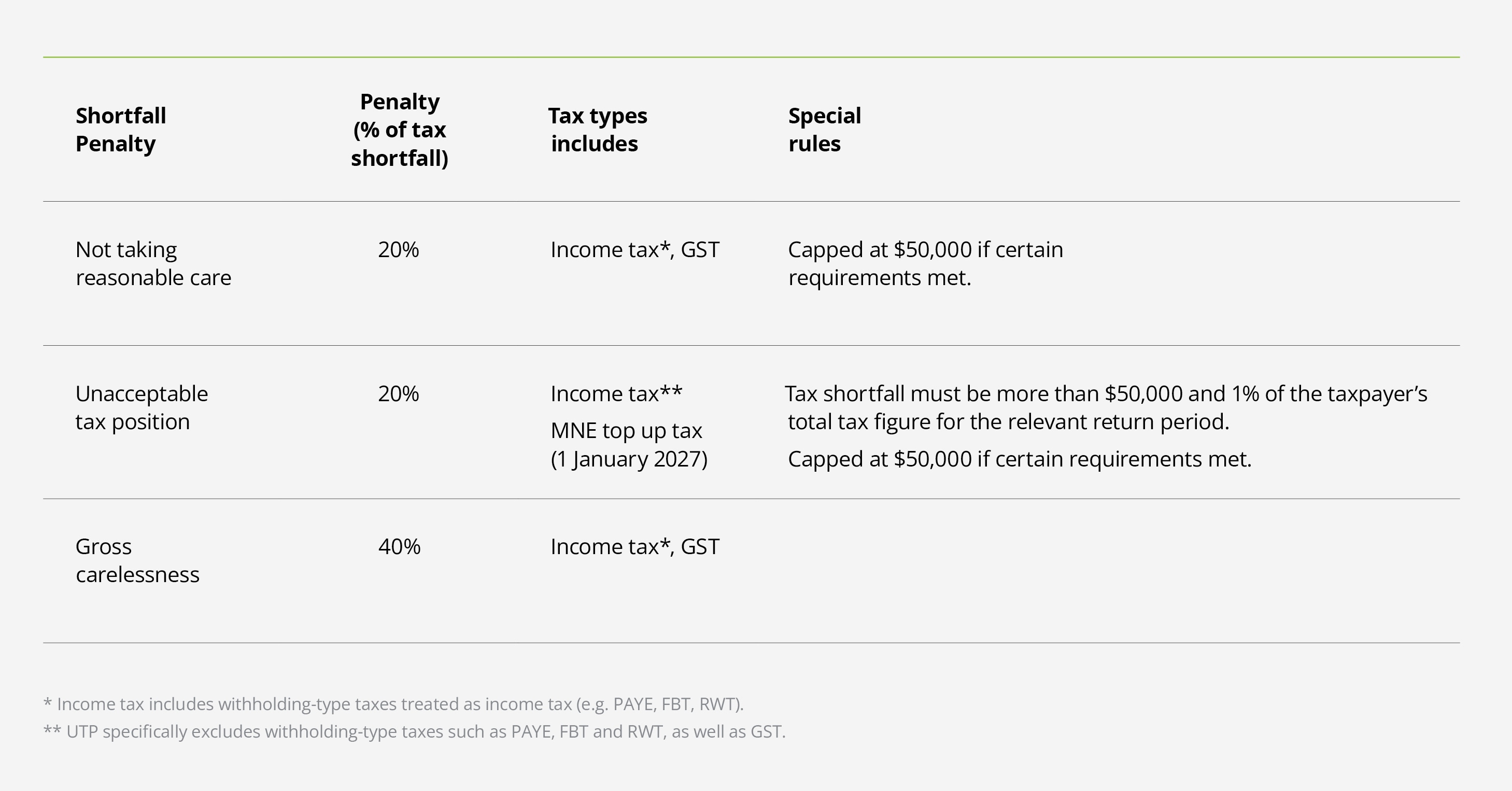

Not taking reasonable care (NTRC)

PUB000498 outlines that reasonable care involves taking the actions that a ‘reasonable person’ would take in the given circumstance (commonly referred to as the ‘reasonable person test’). This is an objective assessment, meaning it is not relevant whether a taxpayer believes they have exercised sufficient care. Taxpayers are expected to take appropriate steps to confirm the accuracy of their tax positions, maintain adequate tax records, and generally make a genuine effort to comply with tax law. In most instances, relying on the actions or advice of a tax advisor is considered to be taking reasonable care, although there are specific exceptions to this. The draft IS provides several useful examples and includes a clear flowchart illustrating how the NTRC shortfall penalty is applied.

Unacceptable tax position (UTP)

PUB00499 addresses the UTP shortfall penalty and clarifies that an ‘unacceptable tax position’ is one that is not “about as likely as not to be correct”. While this phrase may initially seem confusing, the draft IS breaks it down, explaining that a tax position is “about as likely as not to be correct” if:

- even though wrong, it can be argued on rational grounds to be right.

- it is one on which “reasonable minds could differ”. There must be room for a real and rational difference of opinions.

- it has about an equal chance of being correct.

As with NTRC, UTP is assessed objectively. It is not surprising that there are a number of tax cases examining the meaning of “about as likely as not to be correct”, and the draft IS provides a detailed legal analysis of this concept. Importantly, a taxpayer who is not liable for a UTP shortfall penalty may still be liable for an NTRC shortfall penalty. The draft IS includes a range of examples illustrating different taxpayer scenarios.

Gross carelessness (GC)

PUB00500a explains the GC shortfall penalty. GC means to doing (or not doing) something in a way that, in all circumstances, suggests or implies complete or a high level disregard for the consequences. This standard involves more than simple oversight or a lack of reasonable care. The conduct must create a substantial risk of a tax shortfall, which a reasonable person in the taxpayer’s situation would have anticipated. Intentional behaviour is not a factor in determining GC.

Similar to UTP, the draft IS provides a detailed analysis of the numerous tax cases concerning the GC shortfall penalty, along with several taxpayer scenario examples to offer guidance.

The table below summaries these three shortfall penalties:

Click here to enlarge the table below

There are two other common shortfall penalties that can be imposed by the Inland Revenue – abusive tax position and evasion - and the TCO have advised that they are currently working on new guidance documents that would be consulted on in the near future.

Tax position and tax shortfall

The terms ‘tax position’ and ‘tax shortfall’ are frequently used by Inland Revenue and tax advisors, yet they are often not fully understood. It is encouraging to see Inland Revenue taking a proactive approach by publishing specific guidance on this matter in PUB00500b, as accurately interpreting these terms is essential for a range of tax matters, including (but not limited to) voluntary disclosures, shortfall penalties, and tax pooling.

A taxpayer takes a tax position when they take a position or approach under a tax law, as specifically defined in section 3(1) of the Tax Administration Act 1993. This section outlines in detail what constitute a tax position. For most taxpayers, this may include (but is not limited to):

- having a liability for an amount of tax, or the payment of an amount of tax

- have an obligation to deduct or withhold an amount of tax

- filing, or not filing, a tax return

- the derivation of an amount of income, or exempt income or capital gain

- the incurring, allowing, denying as a deduction an amount of expenditure or loss

- the estimation of provision tax.

A taxpayer can take a tax position knowingly, intentionally or involuntarily by:

- claiming or not claiming, or returning or not returning, a tax position

- being placed in a tax position when something is done on their behalf.

A tax shortfall occurs when a taxpayer’s tax position is incorrect, leading to insufficient tax being paid, or an overstatement of a tax benefit, credit or advantage. Typically, a tax shortfall represents the difference between the tax effect of the taxpayer’s position and the correct position for a return period.

Determining whether a tax shortfall exists, and calculating it, can be complicated. The draft IS includes several examples of taxpayer scenarios to assist with interpreting and applying the guidance.

Shortfall penalty reductions, assessment, payment due dates and disputes

The final draft IS, PUB00500c, outlines the various reductions that may be applied to shortfall penalties, as well as how different shortfall penalties interact. This area can be complex and requires careful consideration. The draft IS includes examples and several summary tables to clarify how reductions may be applied and what occurs when a taxpayer is liable for more than one shortfall penalty.

Additionally, the draft IS addresses how Inland Revenue assesses and amends these penalties, the due dates and payment requirements, and the process for disputing a shortfall penalty if a taxpayer disagrees with it.

While these updated and new guidance documents are intended to provide clear and accessible information for taxpayers, shortfall penalties remain a complex aspect of tax administration, with several potential challenges. If you believe your tax position may be incorrect and are considering making a voluntary disclosure, we recommend contacting your usual Deloitte advisor to discuss the process and possible outcomes before approaching Inland Revenue.

The draft IS are open for public consultation until 31 October 2025.

September 2025 - Tax Alerts

- Tax bill promises simplification

- Revenue Account Method: Government’s opening move or missed opportunity?

- Timing is everything – proposed changes to the timing of taxation for employee share schemes

- An update on remote working in New Zealand: sun, sand (and tax!)

- Shortfall penalties, the devil is in the detail

- End of the row: Tax considerations when concluding a farmland sale or lease

- Royalty or not? What New Zealand businesses need to know about the PepsiCo case

- Snapshot of recent developments