A tax system for all seasons: Inland Revenue’s draft long-term insights briefing

Tax Alert - August 2025

By Joe Sothcott & Robyn Walker

New Zealand’s wrinkles are beginning show. With the country’s aging demographics in mind, Inland Revenue’s latest draft Long-Term Insights Briefing (LTIB) considers the challenges this presents, namely that fewer working-age people will be paying taxes while more will be drawing on New Zealand Superannuation and other public services such as healthcare. Treasury projections paint a stark picture—if New Zealand’s current settings are maintained, the deficit could rise to 13.3% of GDP by 2061.

To respond, the draft LTIB argues for a tax system characterised by durability and flexibility, a tax system for all seasons. The point is that while changing what is taxed—tax bases—can be costly and expensive, adjusting how much we tax is far simpler. In other words, a stable set of tax bases with adjustable rates will make it easier to raise the revenue needed to meet future demands while keeping compliance and administration costs low. Think of it like a garden hose—the lawn stays the same, but you can adjust the flow of water depending on how much you want it to grow.

This LTIB is the second produced by Inland Revenue and is out for consultation now. The Public Service Act 2020 requires government departments to publish LTIBs at least once every three years with the aim of increasing the public service’s focus on the long term. They do not represent Government policy (LTIB topics are chosen by government departments rather than Ministers), instead they seek to discuss the pros and cons of various options and promote debate.

We unpack the Inland Revenue’s draft LTIB below.

Principles and systems

Part one of the LTIB is a rather academic review of the principles of the tax system. It sensibly adopts the McLeod Tax Review’s golden rule for a tax system: that it should raise the required amount of revenue in the most efficient way possible all while promoting fairness. But the question is how this is best achieved while balancing the frequent tension between efficiency and equity (a subjective concept).

The LTIB explains that there are two underlying tax bases: labour income (income from working) and capital income. Capital income can be further split into three categories:

- The normal return – the basic return for delaying consumption, such as interest earned on a savings account.

- Economic rents – the additional return that can be expected from controlling and operationalising a valuable or scarce resource, such as renting out a house in an expensive part of town.

- Return to risk – the additional over and above return expected for putting capital at risk, such as investing in the stock market.

The different bases can be taxed through different types of tax, with the four main types considered in the LTIB being:

- Labour income tax – also referred to as a payroll tax. Wages and salaries are taxed but capital income is not.

- General income tax – wages and salaries are taxed as well as capital income.

- Consumption tax – tax is paid when goods or services are purchased (i.e., income is taxed when it is spent, not when earnt). Doesn’t tax normal returns.

- General income tax with a rate of return allowance – as with a general income tax, but capital income is taxed slightly differently as the normal return is not taxed (or taxed at a lower rate). This is also referred to as a dual income tax.

The four types of tax overlap each other in the type of income being taxed. With this overlap in mind different countries employ different combinations, with New Zealand operating a general income tax and a consumption tax. Inland Revenue propose that this current combination is sufficient and should be maintained, though also considering that swapping in a dual income tax system for a general income tax system could also be worth pursuing. While the LTIB notes that there is some debate about whether normal returns should be taxed, Inland Revenue conclude that the weight of evidence suggest it should be taxed, albeit perhaps at a lower rate.

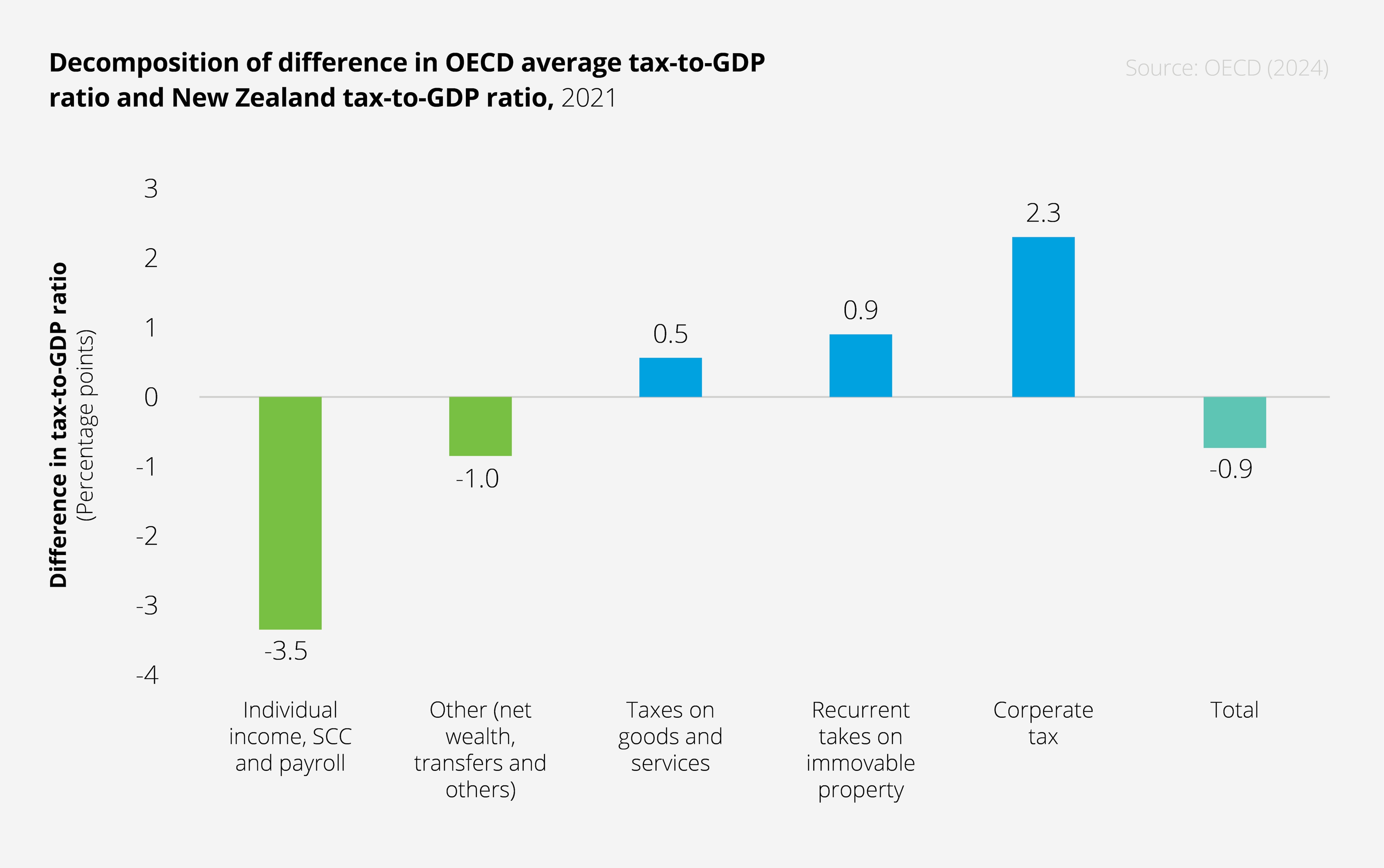

For what it’s worth, New Zealand is highlighted as being rather unique in its mix of taxes. New Zealand does not have a separate labour income tax, unlike many other OECD countries which have social security contributions. However, New Zealand raises more revenue from GST and corporate tax than other OECD countries. The difference in what New Zealand taxes relative to other OECD countries is illustrated below:

Income tax systems

Part two of the LTIB deals with the design of tax systems, firstly income tax. Having concluded that either a general income tax or a dual income tax could provide the desired stability and flexibility, the LTIB examines existing issues with the income tax system and how different options may address these issues.

First, taxing capital gains. New Zealand does not have a capital gains tax, and this arguably makes the income tax base not as comprehensive as it could be. Whilst Inland Revenue note that taxing capital gains would result in a more neutral treatment of different types of income, the trade-offs include increased compliance costs, the potential of capital gains being ‘locked-in’, penalised risk taking, and the risk of taxing only the inflation element of a gain. It is also noted that when the Cullen Tax Working Group considered a capital gains tax, they estimated it would eventually generate around 1.2% of GDP in revenue (about $3 billion based on current GDP). This is a long way away from closing the projected deficit of 13.3% of GDP in 2061, so even if New Zealand implemented a capital gains tax and it raised the estimated revenue, more will be needed to reduce the projected deficit.

Second, the interaction between personal and corporate taxation. The corporate tax rate is currently 11% lower than the highest personal marginal tax rate (28% vs 39%). The reason the corporate tax rate is lower is to ensure New Zealand is attractive to foreign investment, but a concern Inland Revenue has is that this incentivises sheltering income in a company where it is taxed at a much lower rate. While the solution could be to lower the personal tax rates, Inland Revenue point out this may conflict with the distributional goals of different governments, not to mention revenue sufficiency. Ultimately a gap between the two rates will likely need to be tolerated.

Compared to other OECD countries, New Zealand already has a relatively high corporate tax rate, and this may make New Zealand a more unattractive destination for foreign investment. That said, Inland Revenue point though this may be comparing apples with oranges, as many countries with lower corporate tax rates operate classical tax systems where corporate income is taxed twice (first when received by the company and second when distributed to shareholders as dividends). Meanwhile, New Zealand has an imputation system intended to alleviate this double taxation. The effect of having a classical tax system is that the tax cost on residents is high, but low for non-residents. The point seemingly being suggested by Inland Revenue is that the trade-off for operating an imputation system is arguably a higher corporate tax rate.

One option to address these problems the LTIB considers is Norway’s dual income tax system. Effectively, a dual income tax is a general income tax but with a lower tax rate for normal returns which is deemed at a certain rate as being the risk-free rate, similar to how the Fair Dividend Rate method works for the Foreign Investment Fund rules. Such a system would require the taxation of capital gains.

So taking an example where an individual has income of $100,000, assets valued at $500,000, and the deemed rate of return is 4%:

|

Current rules |

Dual income tax system |

|

Income of $100,000 is taxed at marginal tax rates. |

The rate of return is calculated as 4% of the value of the assets (4%*$500,000 = $20,000) This $20,000 is the normal return and taxed at a lower rate. $20,000 is then subtracted from the income of $100,000 to give net income of $80,000. The net income is taxed at the full marginal rates. |

Consumption taxes

New Zealand’s consumption tax, GST, is famously broad meaning there are very few goods and services it does not apply to. In fact, New Zealand has the highest VAT revenue ratio (which attempts to measure the broadness of GST/VAT) in the OECD. This is considered a great strength of our GST, in that its breadth allows it to be low cost but raise a lot of revenue. On paper, this makes GST a prime candidate for a rate increase to improve tax revenues.

The concern is that GST, as a flat tax, is considered by many to be a regressive tax. Treasury evidence suggests that while the proportion of income tax by households is fairly proportionate across household disposable income deciles, GST is more evenly distributed. Other academic research has also found that New Zealand’s GST—like in other countries—is regressive relative to income and expenditure.

The issue New Zealand faces therefore is that while raising GST is the easiest and most cost-efficient way of increasing Government revenue, the brunt of a GST rate increase is borne by lower income New Zealanders. The solution put forward in the LTIB is to increase GST rates while simultaneously providing some type of cash transfer/tax credit to lower income households (this approach was taken when the rate of GST was increased to 15% in 2010). It is suggested that the other approach of exempting certain goods from GST does not achieve the desired effect as evidence suggests reduction in the rates of GST on particular products are not always passed through to consumer prices.

Inland Revenue ran a model where the rate of GST was increased by 3% while providing a tax credit to the 26% of households with disposable income below 60% of the median family disposable income, so they were no worse off. The result was $5.5 billion revenue raised at a cost of only $0.44 billion (net revenue of $5.06 billion). On the face of it, such an approach could be a practical solution.

What are the other options and what’s not there?

The LTIB also outlines several other tax types that New Zealand does not currently have in effect but that have been floated in the past, such as, payroll taxes, wealth taxes, inheritance taxes, land and property taxes, and social security contributions. Inland Revenue’s view is that the type of income being taxed by these other taxes is already covered in one way or another by a general income tax or a consumption tax. So if one of the other tax types were to be implemented, it should be a supplementary tax (rather than in lieu of the existing taxes) and consideration should be given to reducing the rates of the existing taxes to offset.

What is also interesting is what is not covered in the LTIB. In particular, there is limited discussion on the economic costs of taxation and the interaction between tax and productivity. The LTIB analysis essentially sits in a vacuum and assumes that more tax, on existing taxpayers, is the only solution to the aging population, whereas any solution will ultimately need to be a combination of revenue and expenditure changes. More fulsome discussions on these points in the final version could paint a clearer picture about the place of the tax system within the broader New Zealand economy.

If you are interested in submitting on the LTIB, Inland Revenue have set out some questions they would be interested in receiving responses on to help shape the final version of the LTIB. The deadline for submissions is 1 September 2025.

If you have any questions, please contact your usual Deloitte advisor.

August 2025 - Tax Alerts

- A tax system for all seasons: Inland Revenue’s draft long-term insights briefing

- Participating Advisor: pioneering a stronger, transparent tax system

- Pillar Two is changing. What does it mean for New Zealand?

- Pillar Two FAQs

- Operational transfer pricing: real time efficiency and compliance tailored for your business

- Snapshot of recent developments