How can tech workforce and AI strategies impact digital readiness?

Deloitte’s system dynamics modeling suggests that cutting technical roles without making corresponding data and AI investments may risk damaging enterprise agility

Leaders are increasingly forced to navigate a paradox: How to implement transformative artificial intelligence, data, and workforce strategies without doing harm to the foundational digital capabilities and organizational readiness fundamentals that drive future growth. To explore how interrelated these dynamics are, we developed a system dynamics simulation to model the trade-offs of various strategic levers (see methodology). We compared two hypothetical S&P 500–style organizations to see how cutting the tech workforce and investing in data and AI modernization would impact core organizational capabilities that are fundamental to the effectiveness and adoption of that modernization.

Our simulation led to three primary observations regarding these organizational trade-offs:

- In the simulated environment, reducing technology staff to meet short-term savings goals tended to significantly decelerate tech modernization. This choice also created a drag on the organization’s capacity to deliver change that persisted for several years.

- Conversely, strengthening the data foundation and scaling AI appeared to improve technology performance and increase the capacity to adopt new ways of working, with each factor reinforcing the other.

- When workforce cuts were combined with AI investments, the simulation showed a nuanced outcome: While carefully planned reductions paired with data investments helped preserve technical scaling, the “human cost” often led to unavoidable short-term pain in an organization’s readiness for change before stability returned.

Table of Contents

- Digital capability and organizational readiness

- A workforce reduction’s ‘tax’ on digital capability

- Why workforce reductions may negatively impact an organization’s capacity to change

- How data and AI maturity can act as a performance multiplier for both digital capability and organizational readiness

- Combining headcount reduction with data and AI maturity improvement

- Preserving capabilities while transforming

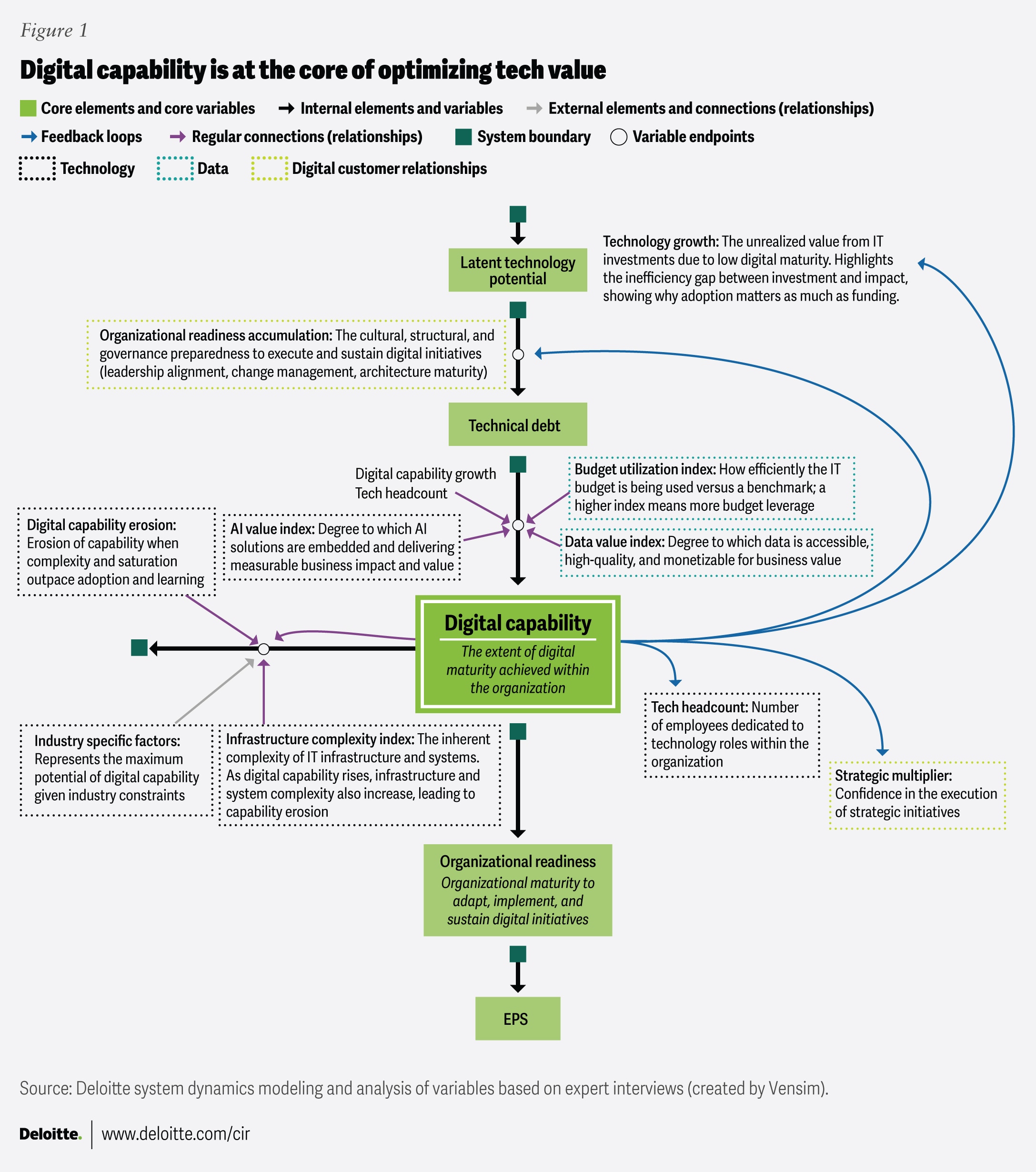

Defining digital capability and organizational readiness

We specifically tracked the tension between two critical engines of growth: digital capability and organizational readiness.

We define digital capability as an enterprise’s ability to deploy and scale technology effectively—a measure of how mature its tech strategies, tools, and processes are. An average S&P 500 company (the baseline for our analysis) is already mature. Such an organization would have scalable technology platforms, a distinct and increasingly valuable data layer, and digitally mediated customer relationships. It would also have digital assets that go beyond just supporting the company’s maturity and value. In the simulation, Company One reflects an organization with digital capability in the 76th percentile of maturity. Company Two reflects the five-year impact of helping to drive the company’s maturity and value. When reinforced by strong, top-led digital cultures, these capabilities act as multipliers on performance, further contributing to the company’s maturity and value.

Organizational readiness is the human element: the capacity to adopt change, mobilize people, and operationalize new ways of working. While technology can be upgraded quickly, the human bandwidth to absorb that technology is often the hidden bottleneck. In the simulation, Company One reflects an organization with organizational readiness in the 40th percentile, a mid-level state of preparedness consistent with Deloitte’s research findings1 and typical starting conditions for transformation efforts.

In high-performing enterprises, digital capability and organizational readiness often advance together, unlocking new opportunities while ensuring those opportunities take hold through tech and data assets, digital customer relationships, people, culture, and governance. This interdependence is embedded in Deloitte’s system dynamics model, which treats both pillars as foundational drivers of enterprise performance. Together, a strong digital capability and a high level of organizational readiness can drive shareholder value and its underlying value streams, including profit-and-loss advantages, new revenue, and enhanced digital asset monetization (figure 1).

As digital capability grows, it can further boost readiness by strengthening the organization’s confidence, governance, and ability to take on the next change. By considering these details, we can run a five-year simulation that mimics how our real-world decisions and actions may affect the company’s digital maturity and organizational readiness.

A workforce reduction’s ‘tax’ on digital capability

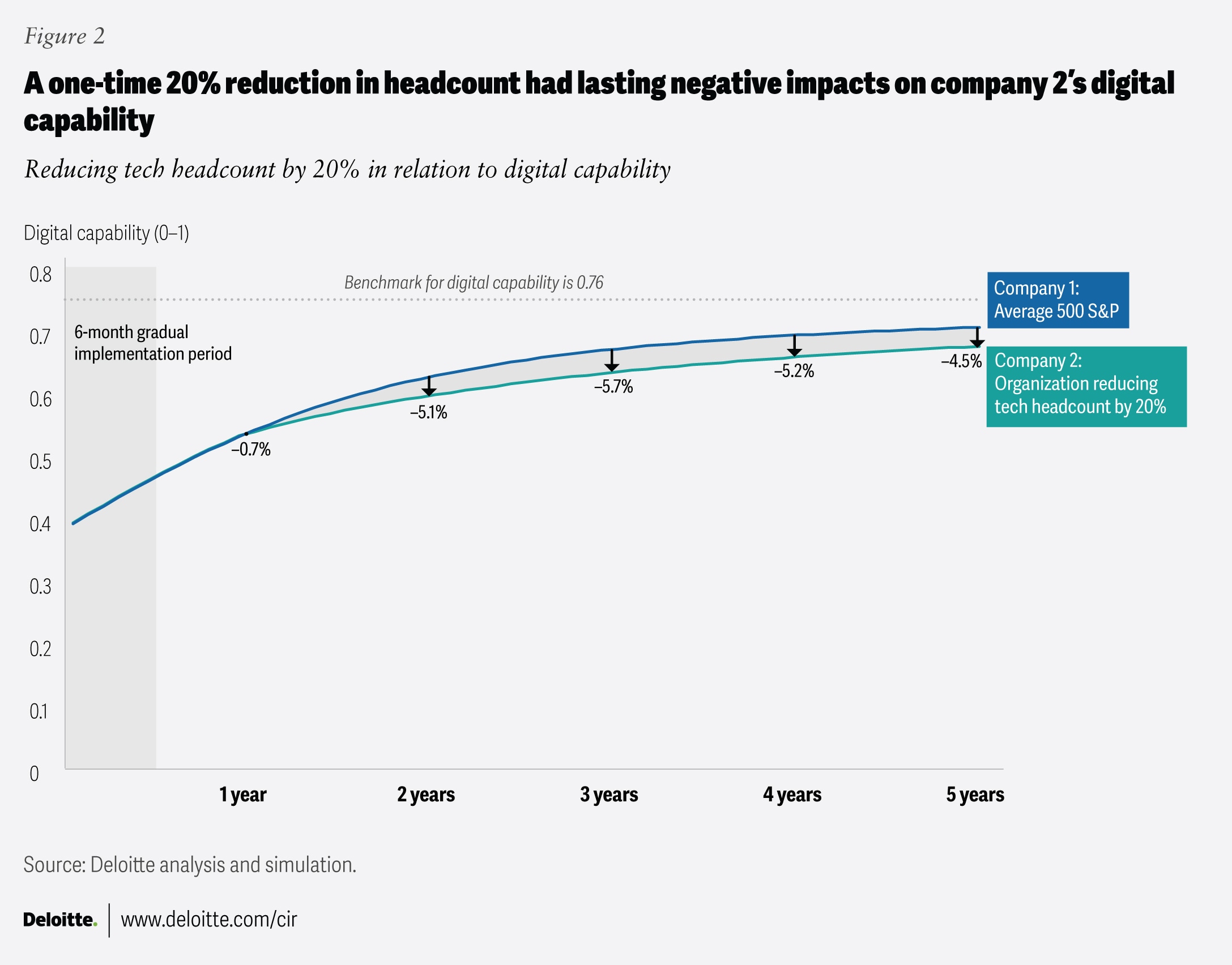

Digital capability can take a sustained hit when the workforce is cut, according to the Deloitte simulation. To test the second-order effects of capacity decisions, we had Company Two reduce tech headcount by 20% over a six-month implementation period. We wanted to isolate a common executive decision—capacity reduction to manage costs—and quantify how it can ripple through the system by constraining business or tech delivery speed, slowing modernization, and reducing the organization’s ability to sustain transformation at scale.

The simulation shows the long-term impact of a single decision in isolation. In the real world, these decisions can be even more pronounced as a strategy is often executed as a series of decisions made over time. For example, headcount reductions may not be one-time events; they’re likely to happen repeatedly. But for the purpose of this research, we modeled a one-time headcount reduction of 20%.

The model shows an immediate and sustained erosion of digital capability relative to Company One. The gap begins modestly in year one, and as reduced staffing translates into delayed work delivery, deferred modernization, and slower adoption of enabling technologies, the erosion of digital capability peaks at 5.7% below the average organization (which did not cut its tech workforce) in year three, based on model simulations. Essentially, Company Two’s core digital capabilities were impaired, and it fell behind competitors on the digital maturity scale. The impact of the decision had a lasting effect, and digital capability maturity didn’t start to rebound until year three (figure 2).2

Reducing a technology workforce doesn’t just impact costs; it can be a bottleneck to modernization, resilience, and the ability to operationalize change. Deloitte’s 2025 Global Human Capital Trends report underscores that many organizations still over-index on short-term business outcomes at the expense of human capabilities, which are still essential for long-term needs. That tension between short-term cost and long-term needs can become more visible during downturns, when technology headcount is frequently an early target for cost savings.

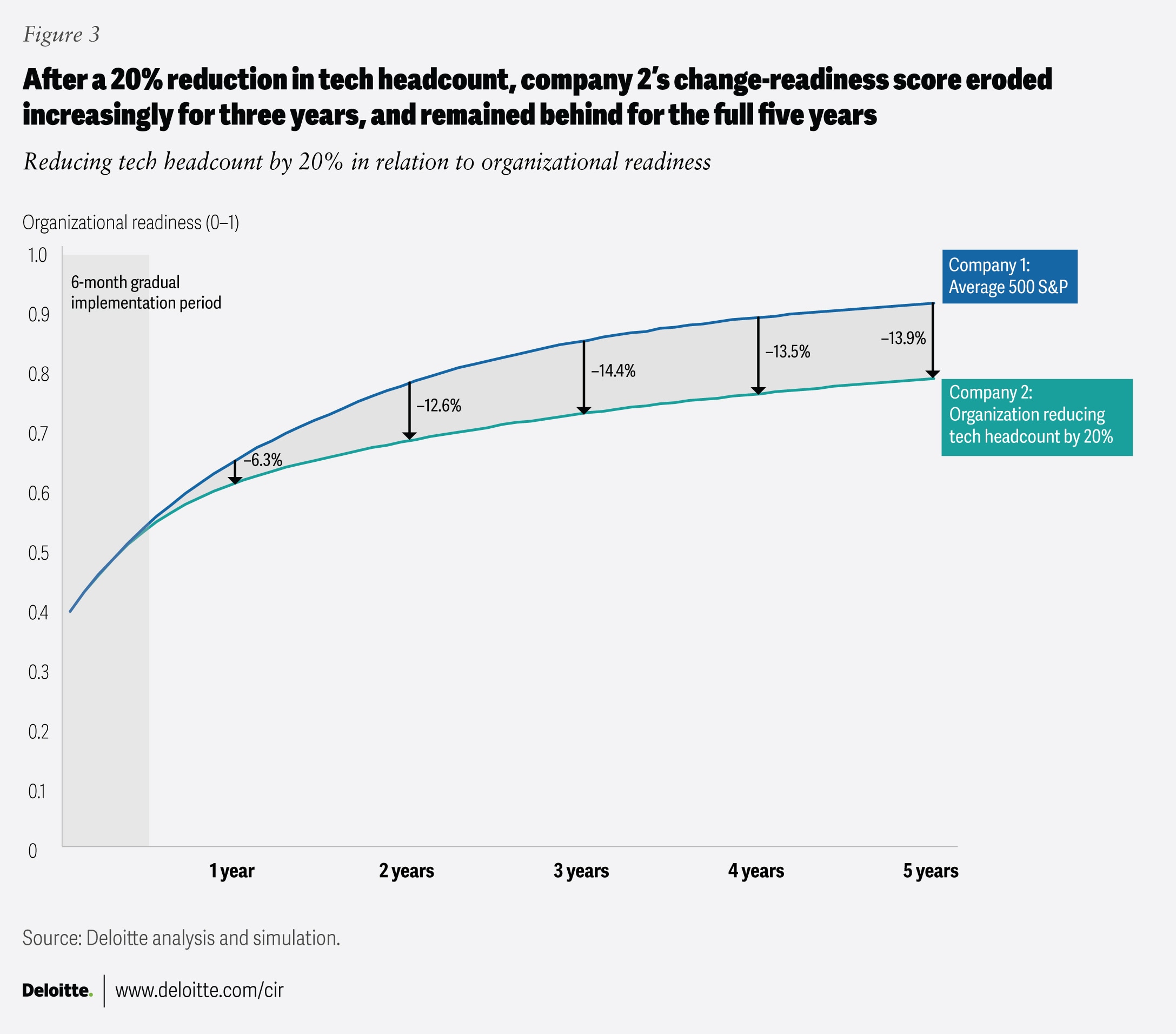

Why workforce reductions may negatively impact an organization’s capacity to change

The impact of workforce cuts on organizational readiness was more pronounced in our modeling. Erosion in organizational readiness (defined earlier as the capacity to execute change, including all change management and digital transformation) started early, with Company Two’s score at 6.3% below Company One’s in year one. The gap between the companies widens sharply to 12.6% in year two, and Company Two reaches its largest drop below the baseline at 14.4% in year three. This is like being in the 73rd percentile versus the 86th percentile in your company’s ability to strategically transform with new technologies—a huge loss in competitive positioning. Even as effects in the model stabilized at a high maturity level, the erosion remained significant, at 13.9% below Company One’s performance in year five, indicating that recovery is slower (figure 3).3

Notably, in both the digital capability and organizational readiness scenarios, companies experience the peak impact of their decisions after three years. This could be because headcount expansion and contraction are familiar moves for organizations that have built mechanisms to adapt, so that the impact, while felt, is not a transformative shift.

One key leadership lesson is that human cost takeout without investing in adequate transformation steps (people, processes, and technology) to perform their work can create a value trap. Fewer teams and less human bandwidth can delay modernization efforts, increase backlogs, weaken governance and adoption support, and ultimately erode both digital capability and organizational readiness. In contrast, cost savings that are invested back into automation are more likely to sustain performance because scaled AI depends on strong data, governance, risk, and compliance disciplines.4

How data and AI maturity can act as a performance multiplier for both digital capability and organizational readiness

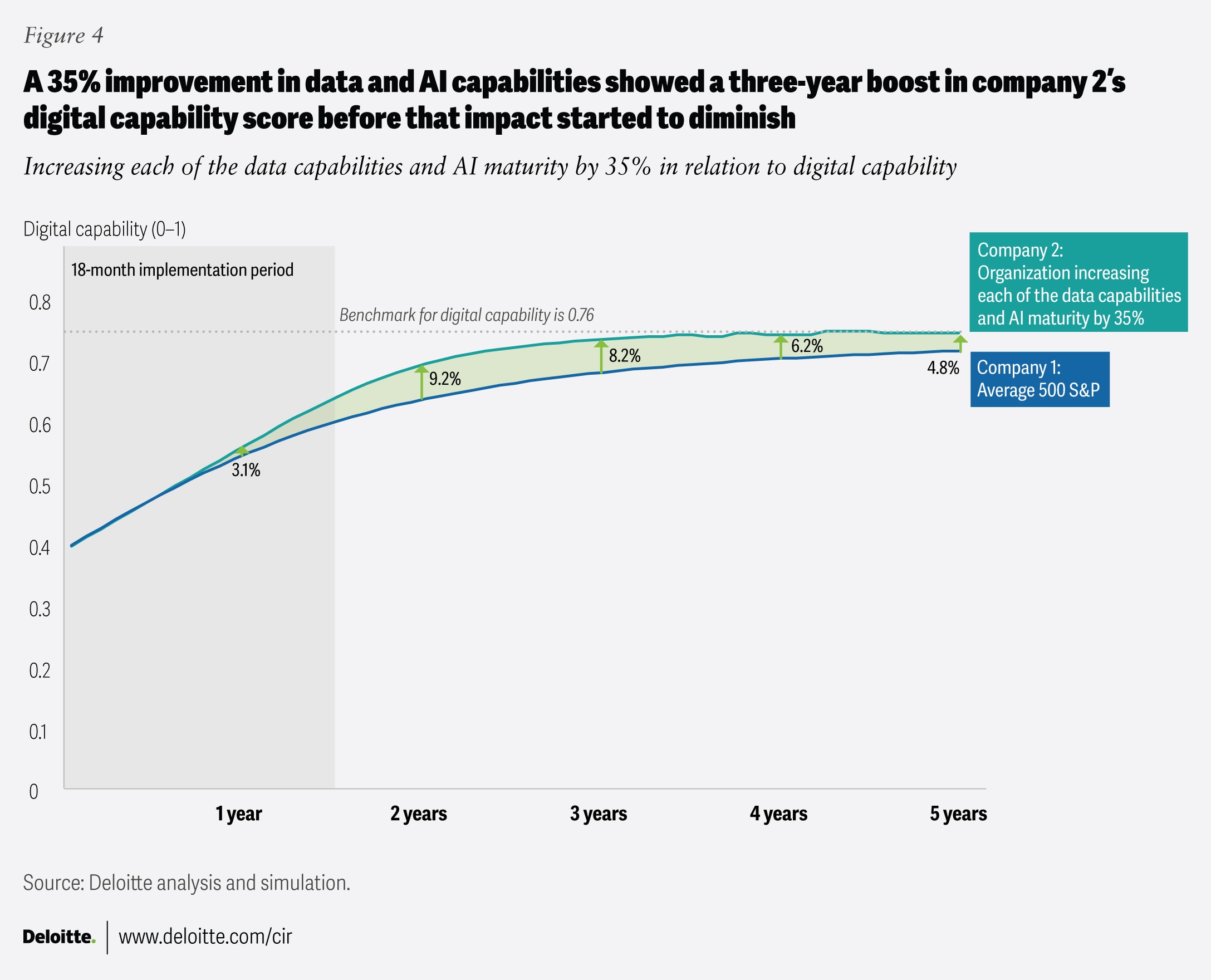

Deloitte modeled a combined intervention in which we enhanced data capability and AI maturity for Company Two. Company One (our baseline) starts with an average score in the 64th percentile, while Company Two has maxed its capability to the 100th percentile to reflect a 35% increase in data and AI capabilities. In practical terms, this increase represents a coordinated set of moves to strengthen its data foundation—quality, accessibility, governance, and reuse across contexts—while simultaneously scaling its AI capabilities. This could manifest through a disciplined use-case pipeline, production deployment, responsible AI controls, and workforce adoption. This combined push creates a clear performance gap: year one delivers a 3.1% uplift in digital capability compared to Company One as the 18-month implementation period begins to take hold; year two expands that gap to 9.2% above the baseline as early investments compound and scale; and year three remains strong at 8.2% above Company One, reflecting a sustained momentum. From there, the uplift moderates, indicating that there is a shelf life on how long it will take before transformative action has less of an impact on core capabilities based on the model (figure 4).5

In this instance, the impact on digital capability wears down after only two years, perhaps given the fast pace of change and innovation and the need to maintain both the data and AI capabilities, which are tightly linked. Deloitte research on scaling generative AI shows that organizations move from pilots to performance only when they strengthen the underlying data foundation and the governance disciplines required.6 Data readiness accelerates adoption by improving the accessibility, quality, and usability of information across the business, creating the conditions for AI to deliver repeatable outcomes rather than isolated wins. When advanced together, data and AI act as reinforcing levers, raising digital capability while also strengthening organizational readiness through better decision-making, clearer accountability, and greater trust in how AI is governed and operationalized.

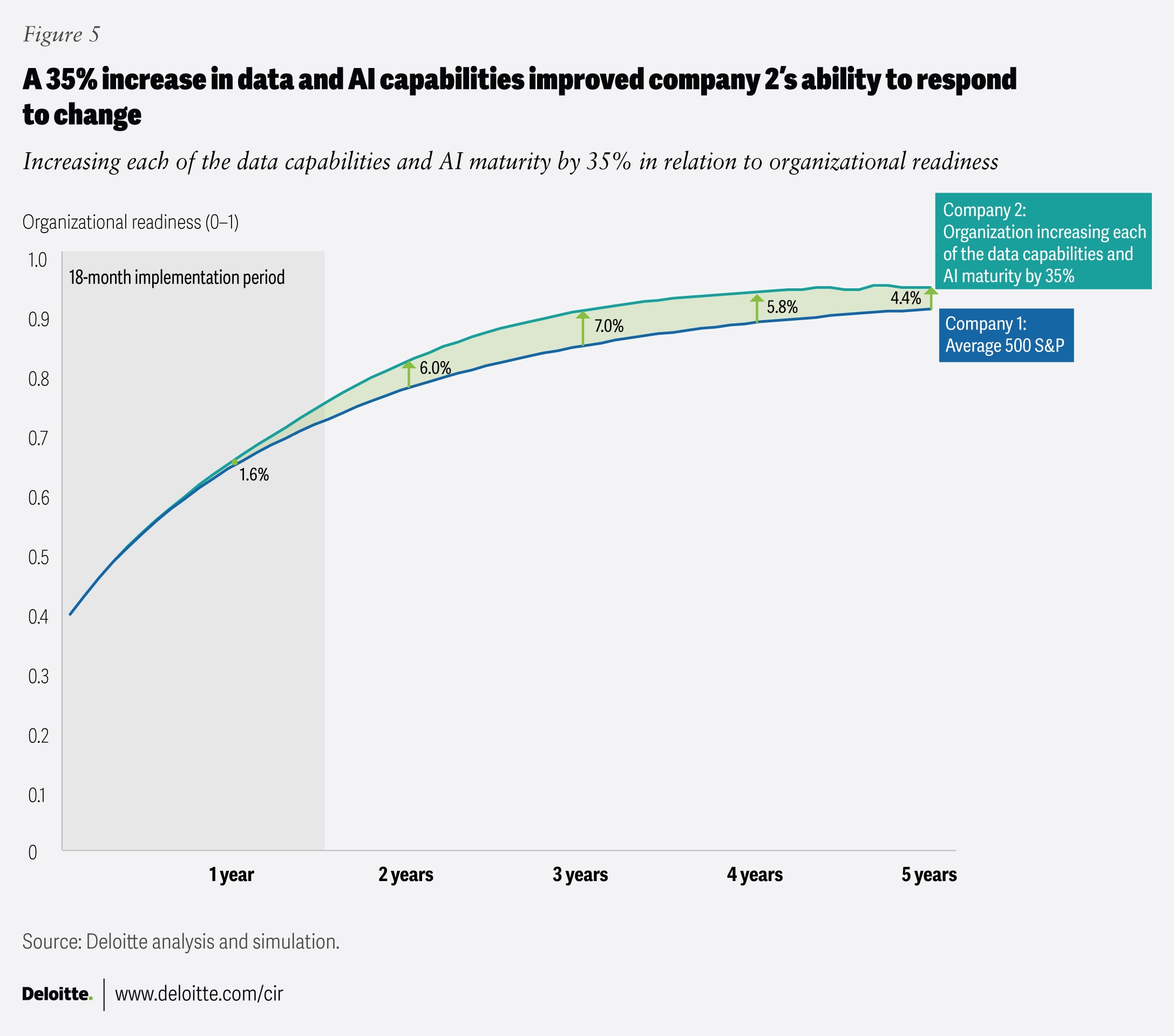

The same data and AI interventions strengthen organizational readiness in our modeling, reinforcing the conditions required to make technology change stick. The model indicated just a 1.6% improvement in organizational readiness over the average company in year one, suggesting that bigger transformations can take more time to impact core processes. The impact was clearer in years two and three, as the investment in data and AI strategy translated into meaningful improvements in the organization’s ability to adopt and adapt when compared to the baseline (figure 5).7 Both Company One and Company Two demonstrate high organizational readiness, ranking in the 80th and 90th percentiles in our model. However, even a minor improvement—transforming a high-performing organization into a very high-performing one—can provide a significant competitive edge.

Combining headcount reduction with data and AI maturity improvement

To test whether leaders can “cut and still transform,” Deloitte modeled a combination intervention in which Company Two reduces tech headcount by 20% while simultaneously boosting data capability and AI maturity by 35% each over 18 months.

The traditional linear relationship between headcount and enterprise growth is breaking down. Technology, particularly AI and increasingly agentic systems, has reached a point where adding more headcount is no longer a prerequisite for scaling output or enterprise value. Growth may be decoupling from workforce expansion. That said, it matters greatly which technologists we’re talking about and whether their roles directly drive revenue. For most large, non-tech-native companies, value creation isn’t coming from adding more system integrators or implementation-heavy roles; it’s coming from shifting to a product operating model that embeds reusable platforms, automation, and software leverage, often without adding incremental headcount at all. In some cases, removing headcount can even improve performance if roles are low productivity or structurally misaligned with the new model. The more useful strategic question, therefore, is not simply “fewer people,” but “What types of technologists actually drive scalable value in an agentic, product-centric enterprise?”

The impact on digital capability in our model

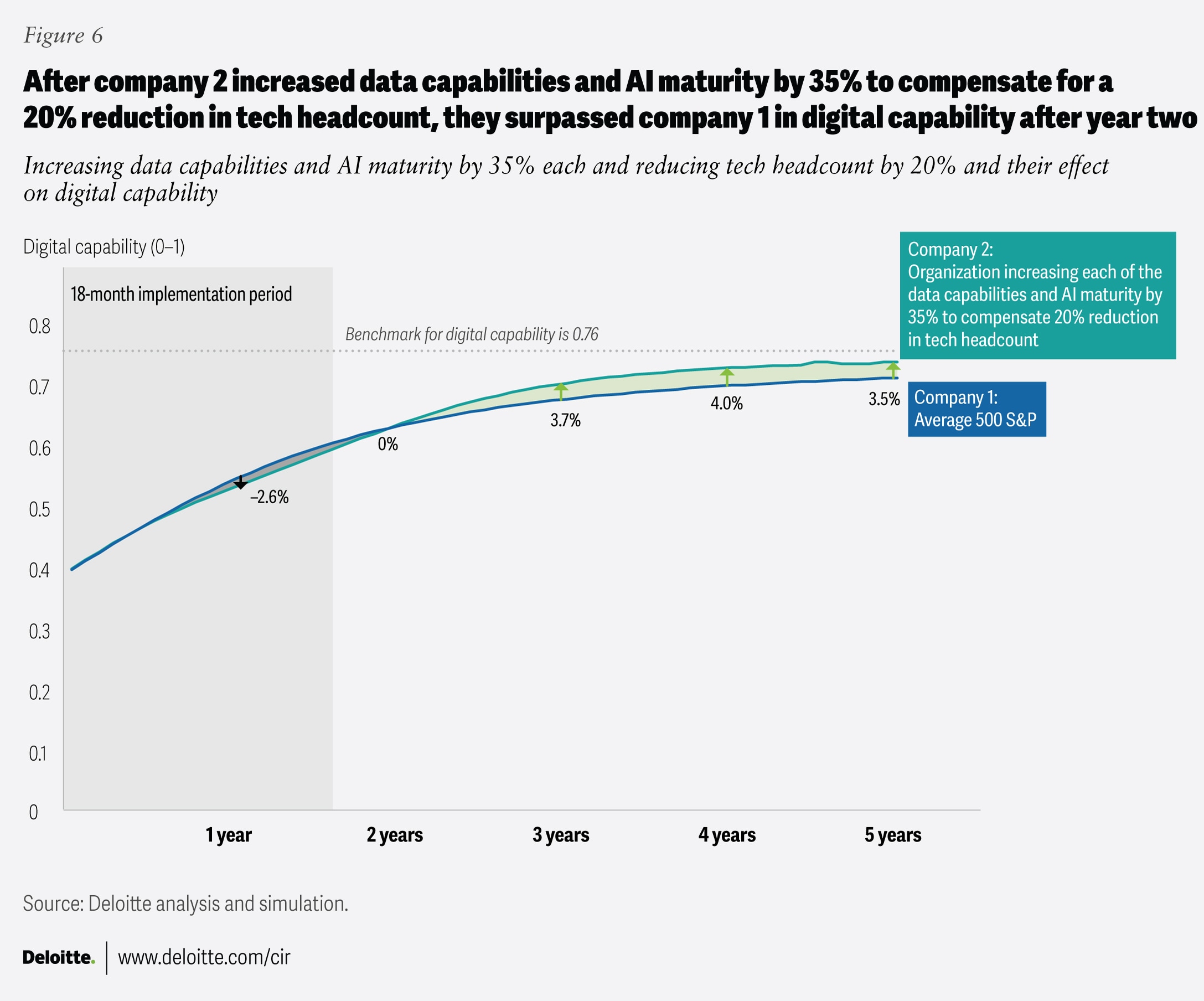

In this combo scenario, Company Two cut headcount while transforming data and AI. This showed an initial drag before the benefits compounded. In year one, digital capability was 2.6% below Company One’s (the average company), as headcount reductions negatively impacted Company Two faster than data and AI improvements could be fully scaled to offset the reductions. For the first two years, Company Two shows a slight decrease in digital capabilities, but after year two, the investments it made in data and AI give it an advantage over Company One, even with the 20% cut in workforce (figure 6).8

The premise is simple: If an organization intends to run leaner, it must run smarter, using stronger data foundations and scaled AI to drive automation, data reuse, faster delivery cycles, and tighter governance.

The impact on organizational readiness

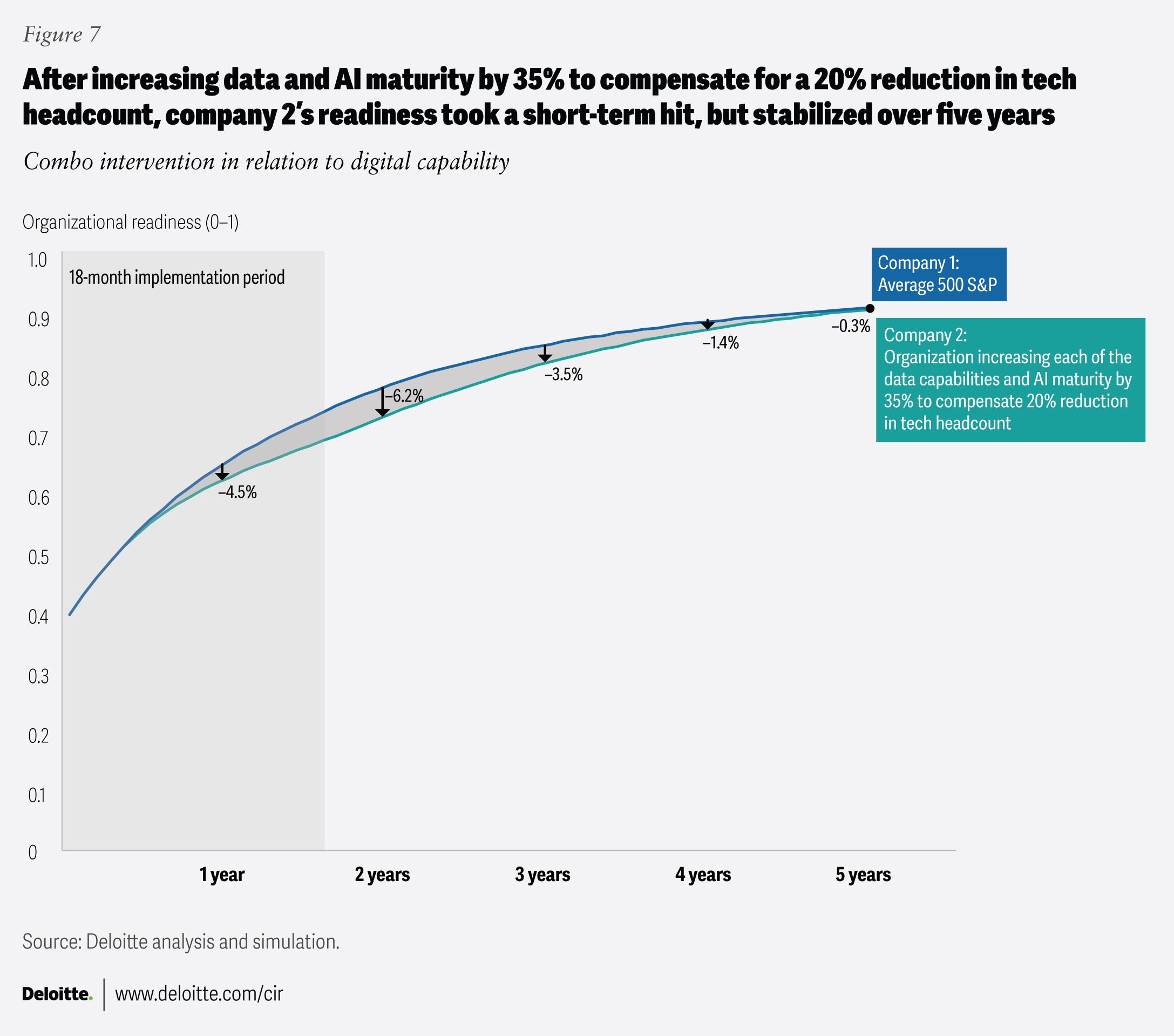

Organizational readiness can be more sensitive to capacity reductions early on and may take longer to recover, even with strong data and AI investments. The model shows readiness erosion of 4.5% below the average company in year one and 6.2% below the average in year two, reflecting reduced change capacity.

Data and AI investment can largely neutralize the long-run readiness penalty of workforce cuts, but readiness recovery is slower because it depends heavily on people capacity, operating rhythms, and sustained change leadership—not technology alone. As data and AI maturity take hold (improving decision quality, standardization, and the ability to scale repeatable ways of working), the gap in our simulation narrowed materially by year three (figure 7).

Preserving capabilities while transforming

Organizations that fail to modernize can often struggle to grow and thrive. However, modernization should be viewed as a set of strategic actions that often have long-term and lasting impacts on core capabilities. A reduction in headcount without also investing in AI and data can have lasting impacts on a firm’s core digital capabilities and related revenue streams. Organizations can become more ready for future change by modernizing their data and AI capabilities. As leaders think across their workforce optimization and AI automation, statistically, the best path forward could be a balanced strategy: Don’t make cuts without increasing investments in AI and data unless you expect to take a hit on modernization efforts.

Methodology

This article is the third in a three-part series exploring how technology drives enterprise value based on a robust system dynamics modeling exercise. For more details, see the methodology section of the first article in the series, “Tech decisions can drive big earnings-per-share gains.”

This article contains general information only and Deloitte is not, by means of this article, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This article is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this article.

Continue the conversation

Meet the industry leaders

Ben Ninio

Diana Kearns-Manolatos

Monika Mahto

By

Ben Ninio

Diana Kearns-Manolatos

Monika Mahto

The authors would like to thank Louis DiLorenzo Jr. for his support and guidance, which were pivotal in framing the research article and the direction of the storytelling.

We would like to thank Ahmed Alibage for his key contributions throughout the analysis and model development process as well as Subodh Chitre and Tarun Sharma. We would also like to thank Tim Smith, Nikhil Roychowdhury, Michael Wilson, Mike Caplan, and Sid Seshadri for their valuable insight and knowledge sharing that have been pivotal in shaping the core model.

We extend our appreciation to the marketing team – Akshay Poojari, Ireen Jose and Saurabh Rijhwani – for their guidance and leadership in amplifying the impact of these insights.

Editorial (including production and copyediting): Andy Bayites, Prodyut Borah, Sayanika Bordoloi, Shyamili M, Cintia Cheong, Anu Augustine

Design: Molly Piersol

Cover artist: Jaime Austin

Knowledge Services: Agni Wagh