Are you building AI partnerships or dependencies?

Partnership mentions in earnings calls have jumped dramatically in the last 18 months. One reason: AI partnerships. But collaboration comes with hidden costs to consider.

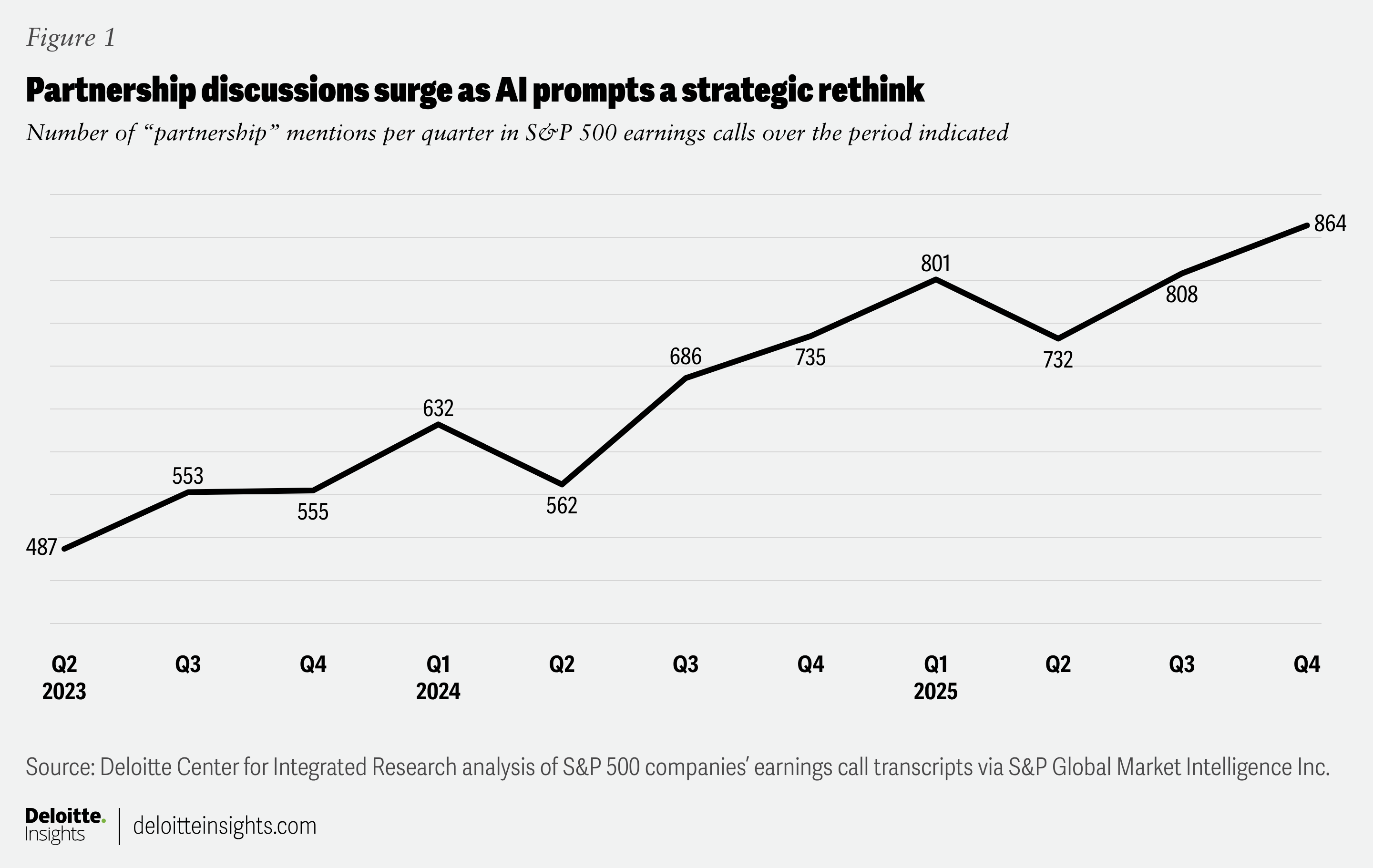

Between the second quarter of calendar year 2023 and Q4 2025, something revealing happened on S&P 500 earnings calls: Mentions of the word "partnership" surged 75%—from 487 per quarter to roughly 864 (figure 1). This isn't just semantic inflation. There are marketplace signals indicating why companies may be responding to AI-driven disruption with partnership agreements.

- The new economics of AI: According to Deloitte's 2025 Tech Value Survey, digital budgets are expected to nearly double from 14% of annual revenue in 2025 to 26% by 2027. Much of that growth is tied to AI investments. Few companies can shoulder these costs alone. That’s pushing many toward cost-sharing partnerships—and locking companies into multi-year contracts with vendors.

- Building technological resilience: As cloud dependence deepens, so does vulnerability to outages. Companies are pursuing "interoperability" agreements with cloud providers to build redundancy and reduce single-point failures. The problem: These agreements mean more partners involved in the process that keep cloud services running smoothly.

- Reimagining creativity and IP: Generative AI is democratizing content creation, putting tools for storytelling, design, and video into more hands. Rather than restricting access to IP, some organizations are partnering with AI companies to enable fan-inspired content and user-driven innovation. In doing so, they are generally ceding some control in exchange for reach.

The message is clear: Some partnerships are less of an option and more of a necessity. But does teaming up make companies more adaptable to change, or just change who calls the shots?

Gillian Crossan, Deloitte’s Global technology, media, and telecommunications industry leader has a similar view: “Companies need to find ways to embrace the complexity of a technology landscape that includes an increasing number of models, agents, vendors, new ecosystems, and new data relationships. For example, there are over 2,000 new AI companies launching annually, all vying for customers.1 That means those customers are focused on finding a way to assess and understand dependencies and data flows, anticipate regulatory complexity, and build resilience into their cloud stacks.”

What’s more, Deloitte’s TMT Predictions 2026 points out that 90% of all AI compute today is managed by US and Chinese companies, so according to Crossan, “sovereignty is becoming a bigger issue around the world, and finding the right partners to meet those needs is not always as simple as it seems.”

Here's the tension: While partnerships can help companies improve speed, scalability, and capability, they also introduce vulnerabilities that many legacy governance models weren't built to handle.

Take cross-licensing agreements in AI. Companies need access to each other's models and training data to stay competitive, but sharing the IP creates new exposure—and mutual reliance. Then there's regulatory complexity: What's compliant in one jurisdiction might violate data sovereignty rules in another. And as more partners plug into your systems, your vulnerability to cyberattacks has the potential to grow. One weak link in the chain can compromise the entire network. At what point does partnership become dependency?

What should leaders do? These moves can help maintain control:

- Treat partnerships as strategic infrastructure—and potential single points of failure. Map your partner ecosystem the way you'd map critical systems. Where are the hard dependencies? What happens if a key partner fails, pivots, or becomes a competitor? Build contingency plans before you need them.

- Build the right governance. Traditional contract reviews and compliance checks are too slow. You need dynamic frameworks that use automated monitoring, real-time risk assessments, and agile governance structures that adapt as partnerships evolve—while maintaining your ability to exit or renegotiate.

- Invest in interoperability as protection against lock-in. Don't only tie yourself to single-vendor ecosystems. Whether it's cloud infrastructure, AI platforms, or data systems, design for portability. The flexibility to switch partners—or add new ones—is itself a form of resilience.

The question for leaders is not whether you'll need more partners. It's whether you'll still be the primary partner in your own value chain. That shift is already underway.

BY

Aditya Narayan

Timothy Murphy

Cover image by: Shutterstock