Eurozone economic outlook, April 2026

The eurozone economy is poised for moderate but stable growth in a challenging global environment

The eurozone economy is projected to grow by around 1.1% in 2026, supported by relatively resilient household demand and continued public investment support. Despite factors weighing down on the outlook—like renewed uncertainty around trade policy, particularly US tariffs, and escalating hostilities in the Middle East, which could keep energy prices higher for longer and weigh on confidence, real incomes, and input costs)—underlying domestic momentum appears robust enough to keep growth positive, albeit moderate.

Beneath the surface of economic stability in 2025

The euro area ended 2025 on a steady footing, and for the year as a whole, the economy expanded by 1.4%,1 outperforming expectations set at the start of the year. Beneath the headline figure, however, lies an important nuance—an exceptionally strong, front-loaded expansion of around 12.3% in Ireland—which skewed the annual figure upward.

However, excluding Ireland, the eurozone grew by around 1%—just a touch above the 0.9% recorded in 2024. Several other countries also benefited from early-year export boosts, although none came close to Ireland’s levels.

Economic growth was broadly balanced across expenditure components. Private consumption continued to support activity, underpinned by a still-robust labor market and solid wage gains. Public consumption remained a further stabilizing force. Investment, which had lagged in 2024, rebounded, while net exports weighed on overall growth.

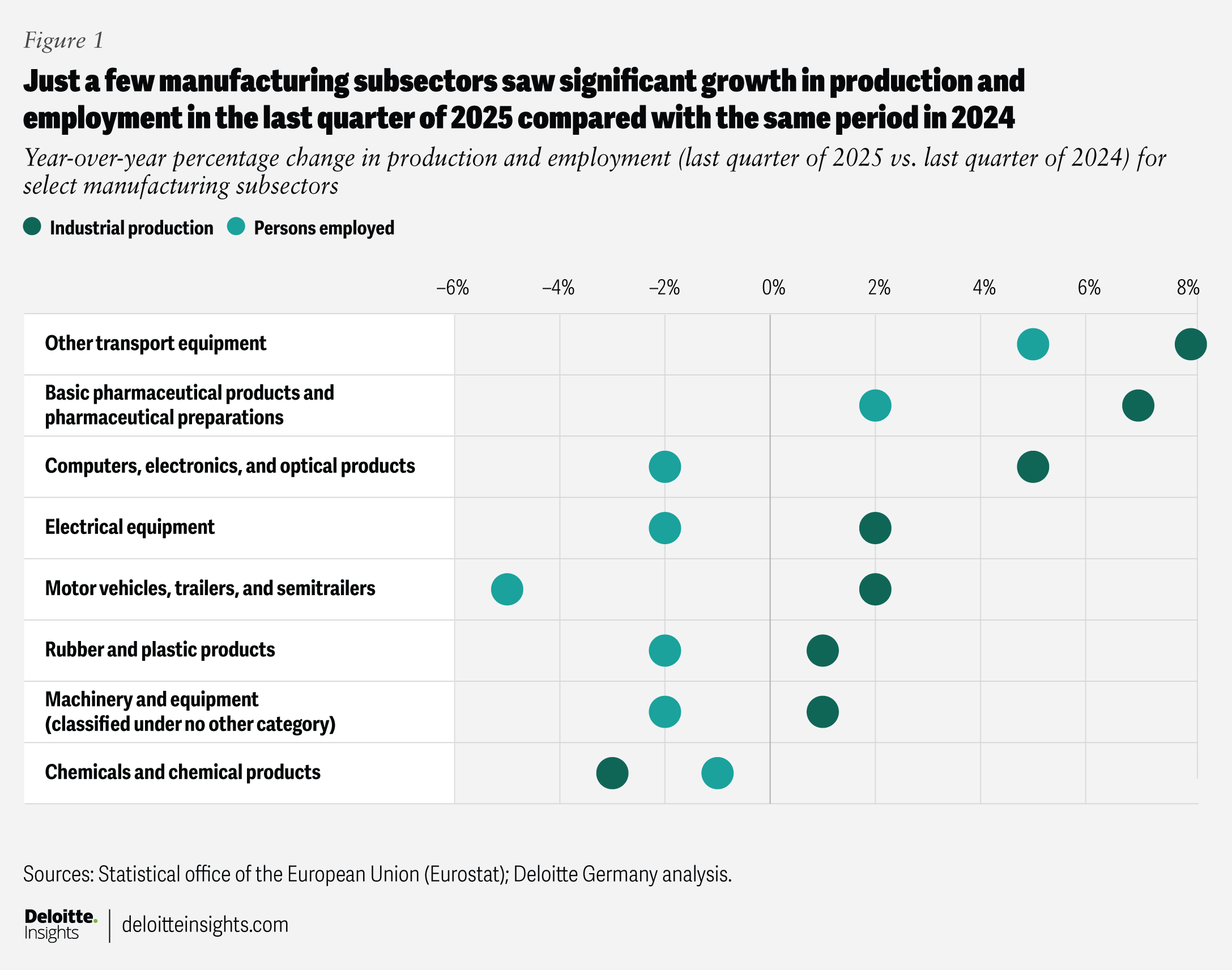

A closer look at sectoral dynamics reveals a heterogeneous landscape: Services continued to expand, momentum in construction started to pick up, and manufacturing appears to have bottomed out. Yet the recovery in manufacturing has been anything but uniform (figure 1). Sectors such as other transport equipment—including defense‑related production—and pharmaceuticals recorded strong growth. By contrast, industries like chemicals, basic metals, motor vehicles, and fabricated metal products experienced stagnation or only marginal growth. Employment patterns mirrored these divergences, as well: high‑growth sectors drove hiring, while several traditional manufacturing segments either held employment steady or saw slight declines.

{kind=link}

The eurozone economy’s complicated entry into 2026

The eurozone’s 2026 macroeconomic outlook remains clouded by renewed geopolitical and trade uncertainty. While the new US tariffs on Europe (introduced after some US import tariffs were invalidated by a US Supreme Court ruling) do not appear to be dramatically different from the previous ones, their impact is likely to vary considerably across sectors. But it is the associated uncertainty, rather than the immediate tariff burden itself, that has the potential to dampen business sentiment and delay investment plans.

To further complicate things, the escalation of conflict in the Middle East has reshaped global risk perceptions and energy prices. Although Europe is less directly dependent on oil and gas from the Persian Gulf than some Asian economies, global pricing mechanisms may mean that supply disruptions may still affect its economies. Higher energy prices for an extended period could complicate the inflation outlook, weigh on household purchasing power and increase input-cost pressures for businesses; the degree of impact, however, will depend largely on the duration and geographic scope of the conflict.

Despite these headwinds, underlying domestic momentum remains sufficiently robust in the eurozone to maintain positive, albeit moderate, growth in 2026, with private consumption and public sector–driven investment serving as primary growth drivers.

Household consumption: From resilience to caution

The labor market remains one of the eurozone’s strongest economic pillars. The unemployment rate stood at 6.1%2 in January 2026—a new historic low after the 6.2% recorded in 2024. Yet employment growth has cooled recently, indicating a likelihood of stagnation in the near future. Wage growth is easing from its post‑pandemic high but remains broadly supportive, however.3

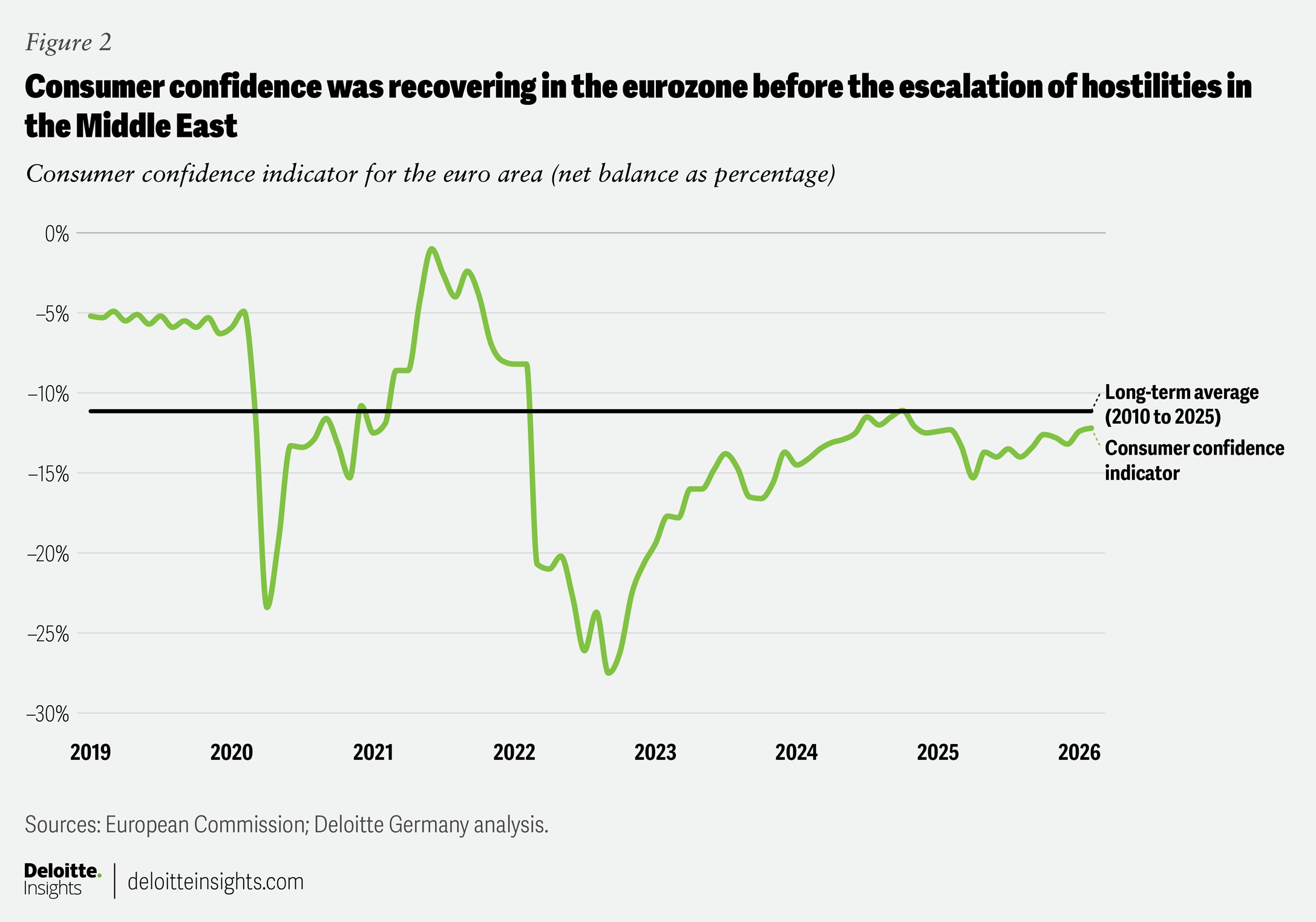

Before the escalation of war in the Middle East, consumers appeared less cautious. Now, however, the household saving rate—which had been trending upward in recent years—is stabilizing.4 Combined with lower interest rates and steadily improving consumer sentiment (figure 2),5 this may suggest a gradual increase in willingness to spend across the eurozone.

However, the conflict and its effects on energy supply chains are likely reminiscent of the energy-price surge European consumers faced during and after the Russian-Ukraine conflict. If the war in the Middle East persists, both sentiment and real-income outlooks are likely to weaken considerably.

{kind=link}

Investment momentum and EU reforms aim to sustain eurozone growth

Fiscal policy is expected to play a meaningful role in 2026, even as some countries return to more restrictive monetary stances. Germany’s infrastructure investment and defence spending packages are now feeding into the economy (figure 1), with effects expected to extend over multiple years. Other member states are also increasing defence spending, adding to aggregate demand.

At the EU level, several initiatives continue to bolster the investment and reform outlook. One of the ongoing investment and reform pushes is the Recovery and Resilience Facility (RRF) of the NextGenerationEU instrument. With the RRF formally closing at the end of 2026, member states must request remaining funding this year. By February 2026, around 66% of grants (nonrepayable) and around 72% of loans had been disbursed.6 An additional 35 billion euros7 (around 6 percentage points of total funds) had already been requested by the member states but remained pending disbursement. Currently, it looks like a timely completion is within reach, and the boost to investment activity is likely to be somewhat higher this year than previously, as the remaining amounts exceed those of the previous years across member states.

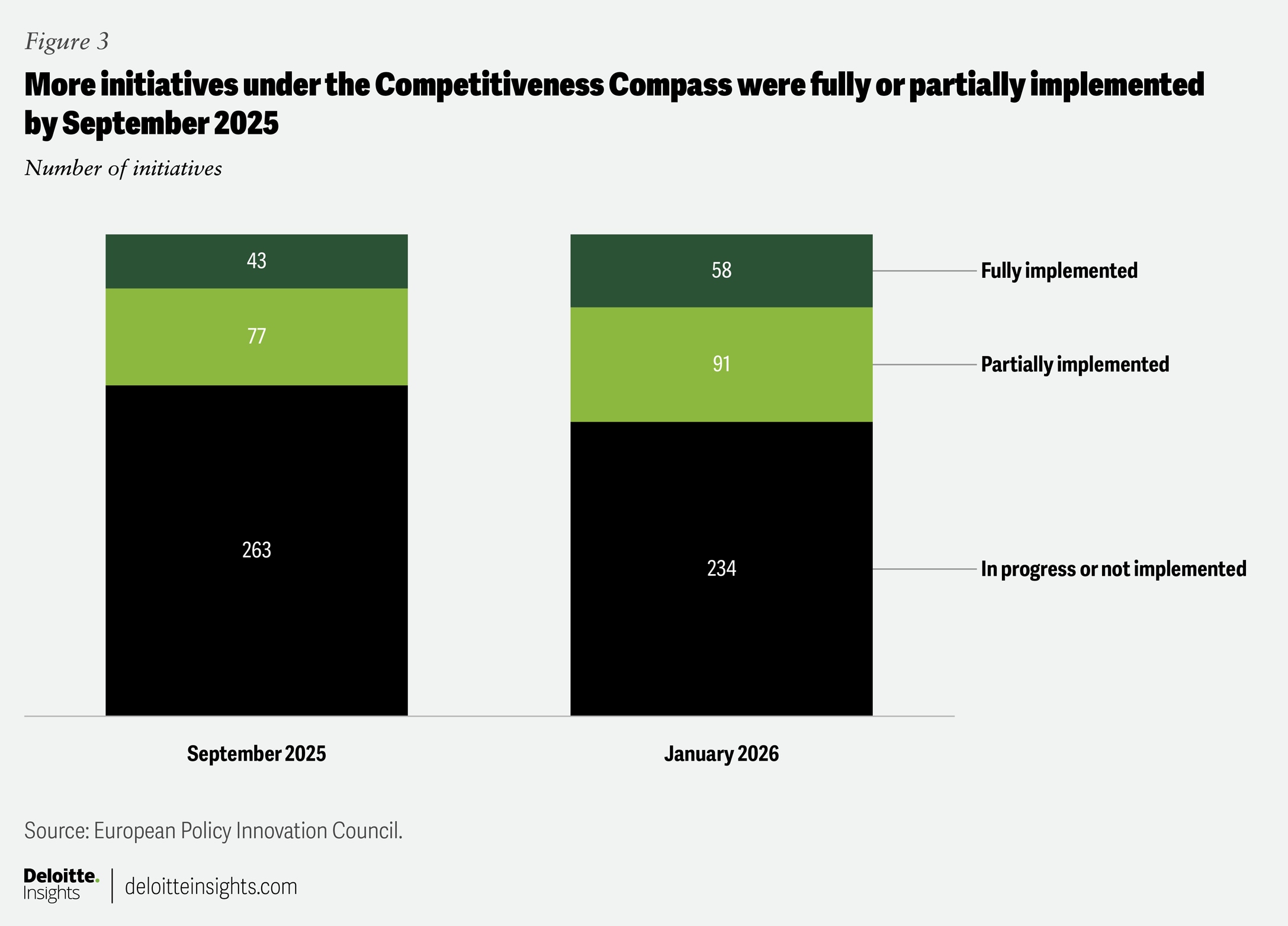

Another such EU-wide initiative is the implementation of the Competitiveness Compass8—the European Union’s flagship framework for structural reforms to enhance competitiveness—which is progressing moderately. By early 2026, a slightly growing number of the identified measures had either been fully implemented or were advancing (figure 3).9 Notably, efforts to reduce administrative and regulatory burdens gained momentum in 2025, with 10 omnibus simplification packages proposed.10

Several major initiatives are expected to shape the reform agenda in the coming months.11 The long-awaited 28th regime—designed to create a single, harmonized set of rules for innovative companies across the European Union—is expected to be announced within the first quarter of 2026.

The Digital Networks Act—a framework incentivizing the development of integrated connectivity and computing infrastructures—has already entered the legislative process.12 Additional large-scale proposals, such as the European Innovation Act13 and the Quantum Act,14 are due in the first half of 2026.

Together, these measures could help foster investment and innovation, improving productivity and competitiveness at a time when Europe faces intensifying global competition.

Exporters face challenges, but with pockets of opportunity

The external environment remains challenging for the eurozone and the global economy. Global trade is expected to recover modestly, but uncertainties around geopolitical tensions, US tariff policy, and China’s uneven growth trajectory will likely cap export momentum. A strong euro may further complicate the outlook for manufacturers competing in price-sensitive markets.

Still, there appear to be pockets of optimism. The trade agreement with India15—although still undergoing refinement and unlikely to be implemented before 2027—signals a willingness on both sides to deepen economic and trade ties. In addition, the EU-Mercosur Interim Trade Agreement is now moving toward provisional application, potentially opening new market opportunities for European businesses. However, the outcome of the review by the EU Court of Justice is unclear, and the agreement might need to be reshaped or even stalled.

A year of moderate but positive growth for the eurozone

Considering the indicators, eurozone gross domestic product is projected to grow by around 1.1% in 2026—lower than the 1.4% recorded in 2025. Yet the quarterly pace is set to improve over the year, as the underlying adjusted economic momentum is gradually improving for the eurozone as a whole. The annual figures are partly distorted by differences in carryover effects and the exceptional growth of Ireland in 2025.

The risks are tilted to the downside, owing to the situation in the Middle East. Higher energy prices remaining elevated for longer, and the resulting uncertainty, represent clear risks. If energy prices stay elevated for longer, it could have an impact on GDP growth (in the range of 0.1 percentage points to 0.2 percentage points).

Yet there are also plausible growth opportunities, particularly if legal challenges and political constraints make it harder to implement new US import tariffs, and if the implementation of the Competitiveness Compass is hastened. Furthermore, high energy prices could speed up the energy transition, making Europe less dependent on fossil fuel imports in the future.

What is clear is that the eurozone enters 2026 with a slightly firmer foundation than in previous years, driven by a robust labor market, easing underlying (core) inflationary pressures, strengthening investment activity, and the tangible delivery of long-awaited structural reforms. The rest of the year will not only test Europe’s resilience once again but also offer opportunities to reinforce its competitiveness, helping chart a more sustainable path for the decade ahead.

By

Dr. Pauliina Sandqvist

Dr. Alexander Börsch

Editorial (including production and copyediting): Arpan Saha, Sayanika Bordoloi, and Anu Augustine

Design: Harry Wedel and Govindh Raj

Cover image by: Rahul Bodiga

Knowledge services: Agni Wagh

Visit the Deloitte Global Economics Research Center

Access more insights for the consumer spending, housing, business investment, globalization & international trade, fiscal & monetary policy, sustainability, equity, & climate, labor markets and prices & inflation sectors.