Japan’s fragile recovery meets rising oil prices

A weaker yen and surging energy costs could dampen inflation relief and slow wage-driven growth

After falling by an annualized 2.6% in the third quarter of 2025, Japan’s economy made a partial recovery in the fourth quarter when real economic value (in terms of gross domestic product) rebounded by 1.3%.1 A stronger recovery this year had looked promising: Wage growth had picked up a bit, while headline inflation began to fall on a month-to-month basis. This gave workers greater purchasing power after a year of inflation-adjusted wage declines. Unfortunately, the conflict in the Middle East and the resulting spike in energy prices have diminished Japan’s economic prospects. Higher commodity prices could reignite inflation and restrain the nascent recovery in consumer spending.

On the positive side, fiscal stimulus2 is expected to keep the economy moving in the right direction. Measures aimed at easing the cost of living, such as utility-bill subsidies, have helped keep inflation under better control at the start of this year. They also contributed to a jump in retail sales in January. Fiscal spending priorities, which include support for industrial production and defense, will likely provide at least modest support over a longer time horizon.

The moderation in inflation is not entirely due to government intervention. Nearly every broad category of the consumer price index has moderated in recent months.3 This includes clothing and footwear, medical care, and transportation and communication. Tellingly, Western core inflation, which excludes all food, nonalcoholic beverages, and energy prices, has been below the central bank’s 2% target since May 2024 and was just 1.3% on a year-ago basis in February. Indeed, in February, all three indicators of underlying inflation used by the Bank of Japan stood below 2%.4 All else constant, this would suggest that the central bank should push back its plans for rate hikes.

While inflation moderates, wage growth has picked up. For example, total gross cash earnings, which include overtime and bonuses, increased 3.3% from a year earlier in February. This was the highest rate of growth since July 2025.5 In addition, indicators from this year’s shunto—the annual wage negotiations with unions—show strong wage growth. As of this writing, the average wage increase for unions was expected to be 5.3%, down only slightly from 5.5% in 2025.6

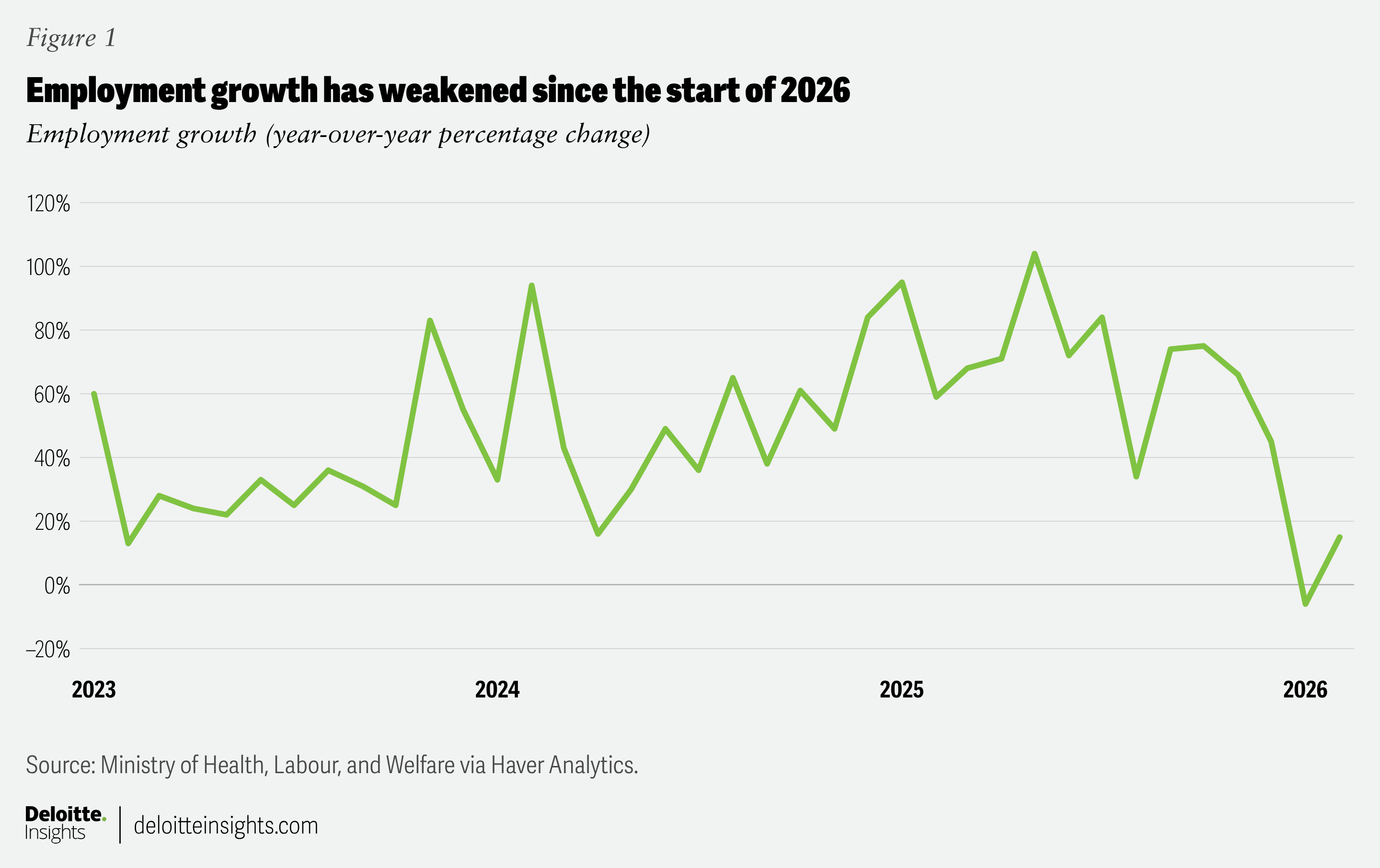

Although wage growth looks relatively strong, other parts of the labor market look weaker. Total employment growth has slowed markedly this year on a year-ago basis (figure 1), pushing the unemployment rate up slightly to 2.6%7 in February. For comparison, the unemployment rate averaged just 2.4% in 2019. The number of job openings as a share of job applicants has trended lower as well, indicating a weakening of the labor market. This occurred before the conflict in the Middle East. The rise in global energy and commodity prices threatens to reintroduce inflationary pressure into the economy just as early signs of labor market weakness have emerged.

Oil-price spikes create risks

Japan is highly dependent on energy imports. It imports large quantities of petroleum, including crude oil and refined products, as well as liquefied natural gas (LNG), primarily used for power generation, and liquefied petroleum gas (LPG), which is used for heating, cooking, and industrial purposes. Japan’s crude oil production is negligible relative to its consumption. In 2025, Japan consumed roughly 870 million barrels of crude oil but produced 2.4 million barrels—roughly 0.3% of its total consumption.8

As of mid-March, the price of Brent crude increased by nearly 60% to around US$110 per barrel, relative to February’s average. Over the same period, the Japan-Korea Marker for LNG has risen by approximately 75% to US$20 per million British thermal units (MMBtu). Oil and LNG prices are now approaching inflation-adjusted levels last seen during Russia’s invasion of Ukraine, when, in today’s dollars, Brent reached nearly US$130 per barrel and LNG in Asia reached US$26 per MMBtu.

If prices were to remain at elevated levels, their impact on Japanese inflation could be significant. Our estimates suggest that a sustained oil price of around US$100 per barrel could increase consumer price index inflation by approximately 0.15 percentage points over the next six months. A sustained LNG price of around US$20 per MMBtu could increase inflation by approximately half a percentage point over a similar horizon. These estimates are a lower bound for the total impact as they capture only the direct effects on gasoline and electricity prices and do not account for any knock-on effects that occur when input costs to other consumer goods and services rise.

Another of those knock-on effects is the value of the yen, which hovered just below the psychological threshold of 160 yen per dollar in the second half of March.9 This is roughly 5% to 6% weaker than the currency was just a year earlier. A sudden rise in oil prices, which are denominated in US dollars, typically causes a depreciation in the yen. This can then lead to higher import costs across numerous categories unrelated to energy, thereby adding inflationary pressure. The Bank of Japan has indicated that it is monitoring the exchange rate and its effects on inflation, suggesting that it could become more hawkish if the yen weakens further.10 Even without additional depreciation, the Bank of Japan may opt to raise rates to prevent higher inflation expectations from taking hold.

One upside to a weaker yen is that it often promotes stronger business investment. Exporting companies benefit from the more favorable prices in the international market. In addition, multinational companies are able to book stronger profits when repatriating their earnings. Unfortunately, the higher energy prices likely offset much of this advantage, limiting the upside to a weaker yen this time around.

Japan’s energy sources are likely to shift

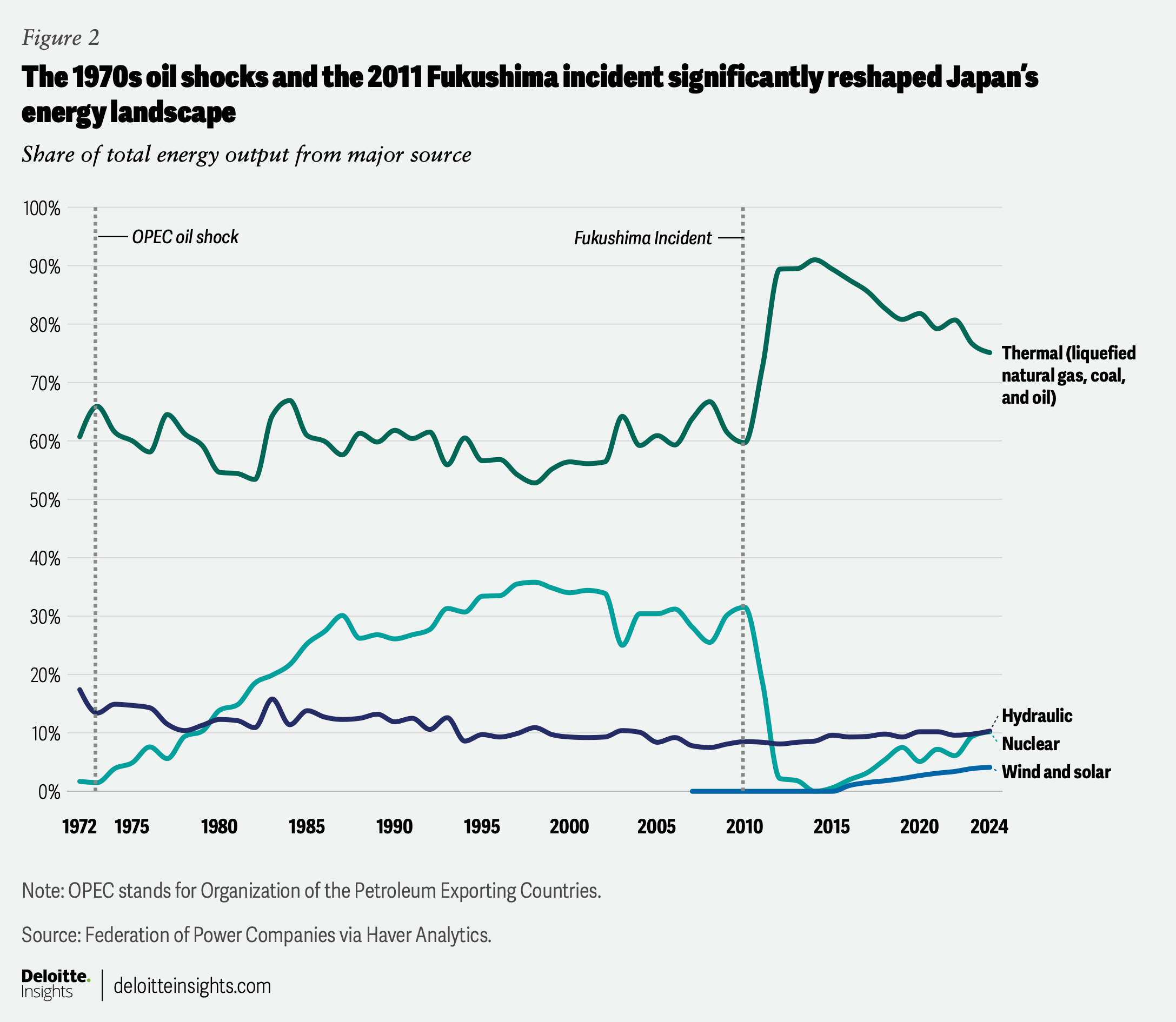

Japan’s energy landscape and policy have been shaped by two main inflection points: the oil shocks of the 1970s and the Fukushima nuclear incident (figure 2). At the time of the 1973 oil shock, nuclear power accounted for just 2% of Japan’s power generation.11 This share eventually increased to around 25% to 30% before collapsing in the aftermath of the 2011 Fukushima disaster.12 In the years that followed, reliance on thermal energy sources, primarily LNG and coal, increased sharply, peaking at nearly 90% in 2015. Since then, the share has declined modestly as renewable energy sources, namely wind and solar, have expanded and nuclear power has gradually gained renewed interest.13 Today, thermal sources account for roughly 60% of Japan’s power generation, while modern renewables (such as wind and solar) and nuclear contribute approximately 11% and 8%, respectively.14

Faced with another energy shock, Japan is likely to continue reducing its reliance on thermal sources and more quickly ramp up its use of renewables. It is also likely to diversify the sources of its LNG, LPG, and oil. While Japan historically sourced a significant share of its LNG from the Middle East (nearly 25% in 2010), it has diversified considerably over the past decade. Today, roughly 40% of LNG imports come from Australia and approximately 7% from the United States.15 Still, disruptions in the Middle East, such as the halting of LNG production in Qatar,16 will impact roughly 10% of Japan’s LNG supply.

Japan’s diversification efforts are most pronounced in LPG. In 2010, approximately 80% of LPG imports came from the Gulf. That dependence has shifted dramatically toward the United States. Last year, Japan imported over 80% of its LPG from the United States. This shift is closely tied to developments during both Trump administrations. In 2017, imports of US LPG surged from 30% to 57%. In 2025, amid tariff negotiations, imports rose further from 60% to 80%.

While Japan has diversified its sources of LNG and LPG in recent years, it remains heavily reliant on Gulf countries for crude oil. In 2025, nearly 95% of Japan’s crude oil came from the Gulf, including 40% from Saudi Arabia and 43% from the United Arab Emirates.17 By comparison, imports from the United States accounted for only 4%.18 The United States has already signaled its capacity to provide more crude oil to Japan, raising the prospect that Japan will be able to find new sources of oil as it looks to limit the risks involved in such concentrated buying.

Higher energy prices and a weaker yen are emerging as headwinds for Japan’s economic growth trajectory this year. Both trends could weigh on consumer spending and push interest rates higher. A weaker yen is generally positive for business investment as it makes exports more competitive and raises the value of foreign earnings, but the rise in energy prices likely offsets the benefits of currency depreciation. Real economic growth is still expected to remain in positive territory but will likely moderate if oil prices stay elevated.

By

Michael Wolf

Niko Sawan

Editorial (including production and copyediting): Arpan Saha, Preetha Devan, and Anu Augustine

Design: Harry Wedel and Alexis Werbeck

Audience development: Pooja Boopathy

Cover image by: Rahul Bodiga

Knowledge services: Rohan Singh

Visit the Deloitte Global Economics Research Center

Access more insights for the consumer spending, housing, business investment, globalization & international trade, fiscal & monetary policy, sustainability, equity, & climate, labor markets and prices & inflation sectors.