South Africa economic outlook, June 2026

South Africa’s economic recovery might be delayed, but not derailed

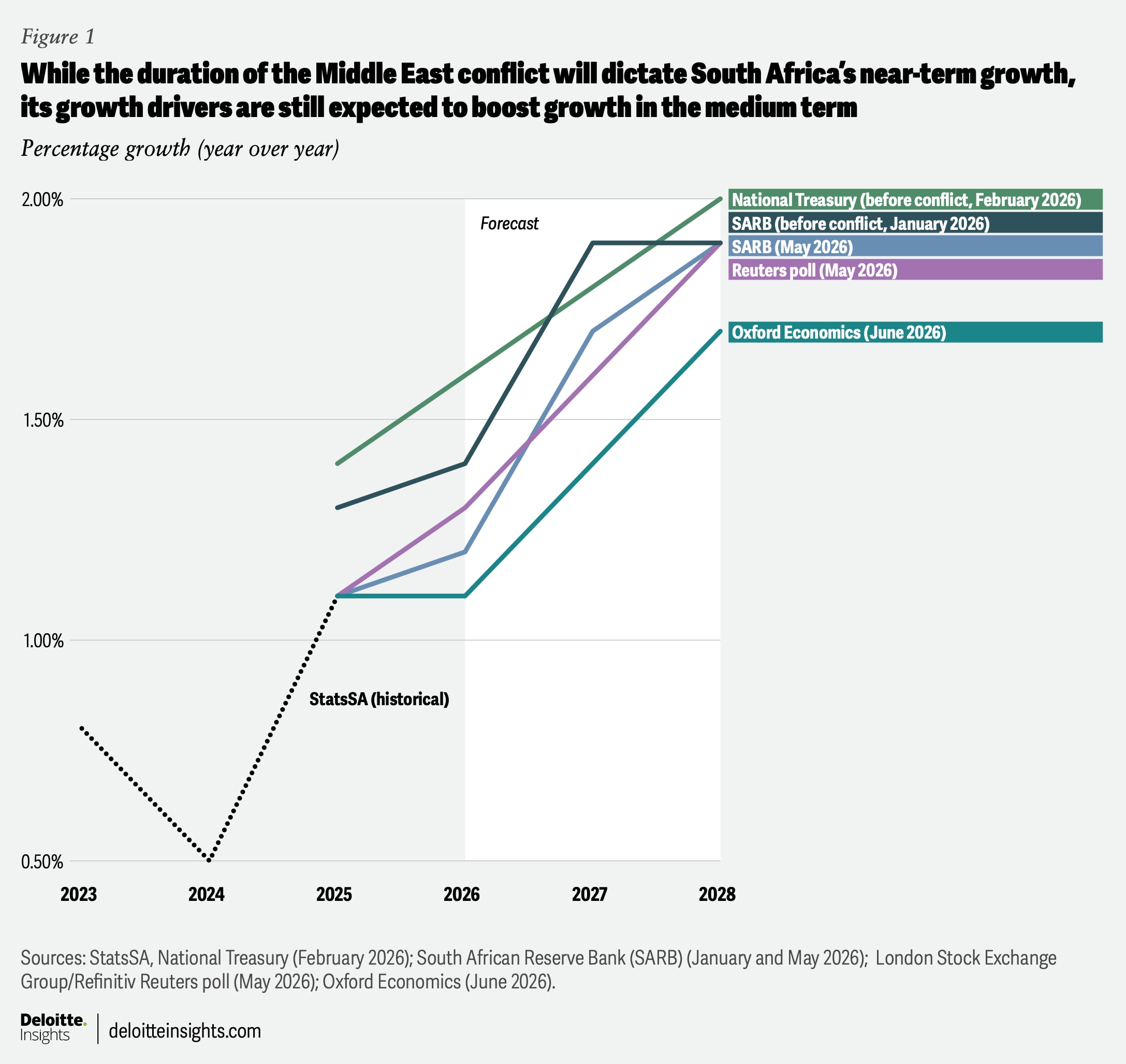

Despite its growth drivers remaining intact, the South African economy will likely see slow growth in 2026, primarily due to the oil price shock from the Middle East conflict

South Africa entered 2026 on a firmer macroeconomic footing than last year: Economic growth expanded modestly through 2025; inflation moved closer to the new target of 3% set by the South African Reserve Bank (SARB); and reform momentum, particularly in electricity and logistics, began to stabilize business conditions and improve confidence in the economy’s medium-term productive capacity.

The National Treasury framed this backdrop in its 2026 budget as a “fiscal turning point in a resilient economy,” driven by improving confidence, lower borrowing costs, and a stronger reform narrative.1

The South African economy grew by 1.1% in 2025, compared with the 0.5% and 0.8% recorded in 2024 and 2023, respectively. The first quarter of 2026 was the sixth consecutive one with positive growth; real gross domestic product expanded by 0.5% from the last quarter.2

Business sentiment also improved materially: The business confidence index published by Rand Merchant Bank and the Bureau for Economic Research rose to 47 in the first quarter of 2026—its strongest non-rebound reading since 2015—supported by a stable policy backdrop, a stable ruling coalition, and lower interest rates than a year earlier.3

This favorable outlook was, however, disrupted by the escalation of the Middle East conflict and the closure of the Strait of Hormuz. The resultant oil price shock has exposed the country’s structural vulnerabilities as a fuel-importing, transport-intensive economy, mainly through higher oil and refined-fuel prices, increased freight and insurance costs, renewed inflationary pressures, and more restrictive monetary policy.

In its statement dated May 28, 2026, the SARB noted that expectations of a swift resolution to the conflict had largely faded, with the Brent crude oil price fluctuating around US$100 per barrel. It also warned of “a painful combination of higher global uncertainty and reduced disposable income,” prompting the Monetary Policy Committee (MPC) to raise the repo rate by 25 basis points to 7%.4

Therefore, the main question for the rest of 2026 and into 2027 is not whether the country’s economic recovery has been stalled, but how much short-term adjustment is required before the reform-driven recovery path, which was visible before the Middle East conflict, reasserts itself (figure 1).

The distinction matters: Recent SARB statements continue to highlight that the underlying drivers of recovery remain intact, citing favorable trading terms, macroeconomic resilience, and progress in ongoing domestic reforms. While South Africa’s near-term outlook has deteriorated, its medium-term trajectory has not fundamentally changed.5

Economic growth: A softer 2026 outlook

Recent GDP data still reflects an economy that was gaining momentum before the external shock from the blockade of the Strait of Hormuz. In the first quarter of 2026, Statistics South Africa (StatsSA) reported that real GDP increased by 0.5% quarter on quarter—up from 0.4% in the last quarter of 2025.6

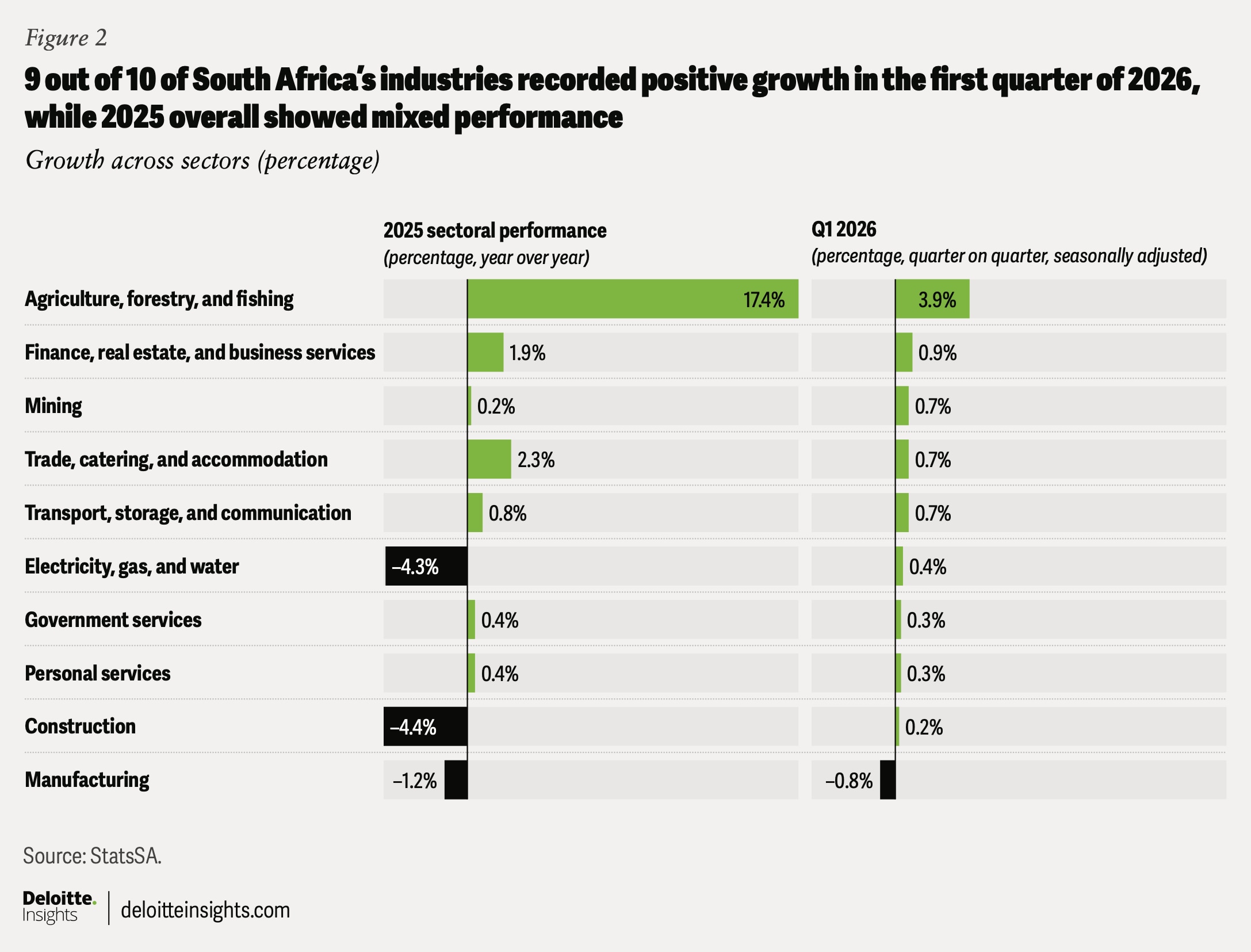

Seven of South Africa’s 10 major industries expanded over 2025, led by a particularly strong recovery in agriculture. But manufacturing and utilities remained weak. Although global trade tensions and evolving US tariff measures have added uncertainty to sectors like agriculture, South Africa’s export base has demonstrated relative resilience, supported by favorable trading terms and strong prices for key commodity exports such as gold and platinum, which have helped sustain export earnings despite a more volatile global environment.7 The most recent data for the first quarter of 2026 shows that 9 out of 10 industries recorded positive growth, led by finance, agriculture, trade, and transport. Manufacturing, however, continued to contract (figure 2).8

On the expenditure side, household spending and investment played a more supportive role than in previous years.9 High-frequency data for the first quarter of 2026 presented a more mixed picture—but one that was broadly consistent with an economy that was demonstrating momentum before the shock from the Middle East conflict came through. As also shown in StatsSA’s economic wrap-up for May 2026, the first quarter was “mainly positive,” with stronger performance in mining, wholesale trade sales, motor trade sales, tourist-related activity, and transport, offset by continued weakness in manufacturing, electricity generation, and construction. This divergence highlights an economy still reliant on services, while tradable and infrastructure-intensive sectors lag.10

This sectoral performance underscores the uneven nature of South Africa’s economic recovery: Finance and broader services have remained relatively resilient, supported by fewer loadshedding or power supply disruptions, modest gains in confidence, and a cautious consumer services economy. Tourism-related categories have also shown improvement. By contrast, manufacturing remains subdued, electricity output has softened, and construction activity has yet to establish a sustained recovery.11

Commodity prices have provided an important external buffer, particularly from mining and export-linked activity. However, it has not been broad-based enough to offset weakness in manufacturing, electricity, and construction, reinforcing the uneven and relatively narrow nature of economic recovery.

Overall, South Africa’s growth profile remains narrow and sensitive to external shocks—lacking a robust investment or production cycle. In this context, fuel-price shocks are transmitted rapidly across the economy, eroding real incomes, raising input costs, and weakening forward-looking confidence. Limited capital formation (StatsSA reports a decline for the first quarter of 2026) and industrial depth amplify the effects of such shocks, thereby disproportionately slowing recovery.

Given these factors, the SARB revised its growth forecasts downward in the May MPC statement, citing weaker investment and household consumption amid heightened uncertainty and reduced real incomes.12 This is a notable shift from the February 2026 budget review, where the National Treasury had projected 1.6% growth for 2026 (SARB now expects 1.2%), which was expected to rise to 2% by 2028 (SARB now expects 1.9%), supported by structural reforms, improving confidence, lower interest rates, and higher investment.

Arguably, the current conflict-driven shock has not reversed the direction of economic recovery, but it has clearly pushed the timing outward.13

Disinflation interrupted

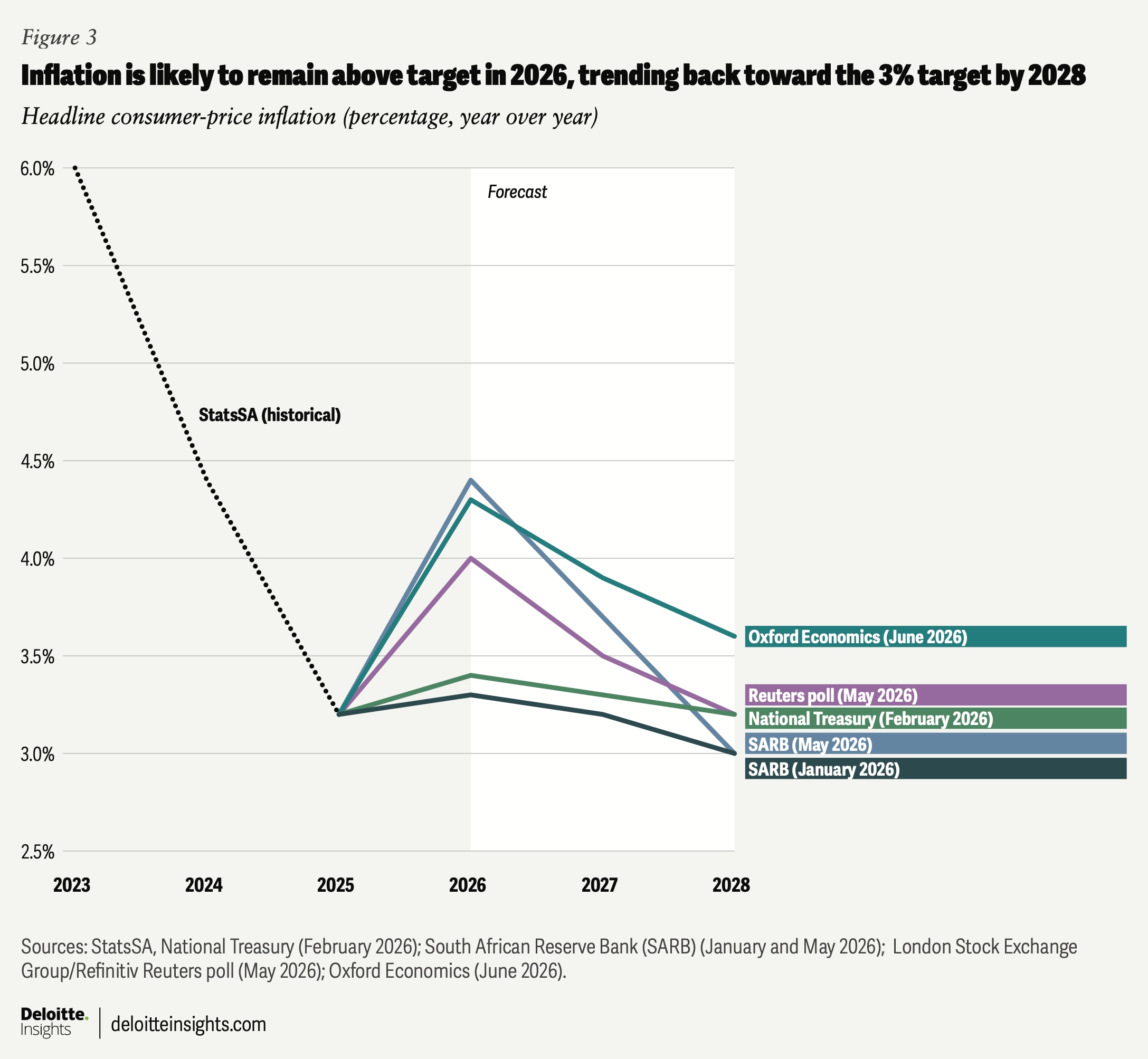

Inflation dynamics were broadly favorable in South Africa at the start of 2026. The first-quarter inflation expectations survey by the Bureau for Economic Research showed that five-year inflation expectations of analysts, businesses, and trade unions had fallen to a record low of 3.6%, while expectations for inflation next year also eased to 3.6%.14 This suggested that the SARB’s effort to shift inflation expectations closer to 3% was starting to gain traction among price-setters.

However, April’s inflation data disrupted this trend. Headline consumer-price inflation accelerated to 4% year-on-year (from 3.1% in March) (figure 3), with a sharp monthly increase of 1.1%, driven primarily by fuel costs. Fuel inflation surged by 11.4% after declining by 8.7% the previous month.15

And this happened despite the National Treasury’s temporary reduction of the general fuel levy—from April and extended through June—which lowered the diesel levy to effectively zero by May.16 While this intervention mitigated the immediate passthrough of costs, it could not fully offset global price increases. The three-month relief, estimated at 17.2 billion rand in foregone revenue, was framed as “revenue-neutral” within the fiscal framework.17

The exchange rate has also provided a partial mitigating effect. The value of the rand has been volatile in 2026, depreciating from around 15.7 per US dollar in early January to above 16.8 per dollar during the initial escalation of the conflict, before retracting to the middle of the 16-per-dollar range more recently as commodity prices strengthened and risk sentiment stabilized.18 This partial recovery, supported partly by higher gold prices and associated export earnings, has helped to moderate the domestic impact of elevated oil prices by limiting the passthrough of exchange-rate effects to fuel costs. But the buffer has not been enough.

Concerns now extend beyond first-round effects through transportation costs. In the May MPC statement, the SARB highlighted services inflation of 4.6%—above its 3% target—and emerging nonfuel pressures in categories such as insurance and financial services.19 The shock is no longer confined to the petrol pump, thus, and cost pressures seem to be broadening.

Producer-price data reinforces this: Headline producer-price inflation rose to 4.8% in April from 2.3% in March, with a monthly increase of 3%. This was the largest monthly jump in the current producer-price inflation series. Key drivers were fuel- and petrochemical-related categories: Diesel prices rose 39.4%, and petrol prices rose 18.3% at the factory gate. Fertilizer prices also surged sharply (ammonia nitrate fertilizer prices jumped 37.6%, while other fertilizers jumped 20.1%). Petrochemicals and feedstock prices increased by 19.5%.20 As a leading indicator for consumer-price inflation, the producer-price data suggests further upward pressure on consumer prices. Consumer-price inflation stood at 4.6% year on year, in May 2026, driven by fuel price increases.21

The inflation outlook now depends on the extent to which the initial fuel shock translates into broader price pressures. Given the role of fuel as a systemwide input, second-round effects—particularly through food and services—remain a key risk.

Although food inflation has not yet fully reflected that stress, the underlying data still suggests that earlier supply conditions and good harvest outcomes buffered price pressures. But food inflation is usually slower to react in such situations, especially where cost increases first pass through producers, transporters, and wholesalers before reaching retail shelves.22

In mid-June, the signing of the memorandum of understanding between the United States and Iran—which has resulted in the temporary opening of the Strait of Hormuz—has already seen Brent crude prices moderate to around US$80 per barrel. Hopefully, this provides some stability and moderation to inflation numbers in the coming months, although negotiations are still underway on the final terms of the deal.23

Interest rate easing postponed

The risk of a broader cost-of-living shock may be likely for the second half of the year, particularly if no final US-Iran deal is reached in the next two months.

The MPC hiked the repo rate by 25 basis points in May to 7%, with a split decision, reflecting both the seriousness of the inflation outlook and ongoing uncertainty. Revised forecasts indicate average inflation of 4.4% in 2026, likely turning toward the SARB target of 3% only by 2028.24 As a result, the anticipated policy-easing cycle has been postponed, with risks tilted toward further tightening if elevated inflation persists.

That shift matters greatly for both households and firms. The year that was widely expected to deliver lower borrowing costs now looks more like a year of restrictive policy with a real risk of further tightening. If oil markets remain constrained and cost passthroughs become broader, the probability of further repo rate hikes—once in July and potentially again in September—cannot be ruled out.25

Even in a more benign global scenario, weather-related risks—particularly a potential El Niño event—could place additional upward pressure on food prices into 2027.26

Fiscal trajectory shows progress but remains under pressure

South Africa’s fiscal outlook had also been improving at the start of the year. In the February budget review, the National Treasury framed 2026 as a turning point for public finances, with the debt-to-GDP ratio expected to stabilize in fiscal year 2025 to 2026 and gradually decline thereafter.

The consolidated budget deficit was projected to narrow from 4.5% of GDP in fiscal 2025 to 2026 to 3.1% by fiscal 2028 to 2029, with gross loan debt expected to stabilize at 78.9% of GDP over the current fiscal year and ease to 76.5% over the medium term. The government also projected a main budget primary surplus of 0.9% of GDP, supported by stronger revenue collection and somewhat lower debt-service pressures.27

However, weaker growth and higher interest rates now complicate this trajectory. Lower revenue buoyancy, elevated debt-service costs, and the need for policy interventions like the fuel-levy relief, highlight fiscal fragility. While fiscal credibility is unlikely to be undermined, the pace of fiscal consolidation will likely be slow.

Still, South Africa’s fiscal “repair” story has been an important part of the recovery in economic confidence. If growth disappoints materially or rates remain elevated for longer, the country’s fiscal trajectory is likely to become incrementally more challenging in 2027.

Investment: A key medium-term growth driver

Investment remains the most important determinant of sustained economic recovery. While there were early signs of improvement—particularly in the data for the last quarter of 2025—overall capital formation remains weak at just 13.7% of GDP, down from 14.2% in 2024—well below the National Development Plan’s 30% target.28 Going into 2026, gross fixed capital formation declined in the first quarter of 2026, after two quarters of marginal expansion.29

Weak growth, limited state capacity, inefficient public investment management, supply-side bottlenecks, and policy uncertainty have all constrained capital formation in South Africa.30

But there is some medium-term support: About 1.07 trillion rand in public sector infrastructure spending over the three-year Medium-Term Expenditure Framework period was penciled in by the National Treasury in February, with state-owned companies being the largest contributor (about 445.5 billion rand). Capital payments are also the fastest-growing item of expenditure in the budget framework.31 A more deliberate attempt to raise public investment, crowd in private capital, and rebuild delivery capabilities in key sectors like energy, transport, and logistics will remain an important foundation for faster growth in gross fixed capital formation. However, it is execution that remains the most crucial challenge for South Africa.

Encouragingly, investment commitment has improved in headline terms. Since 2018, South Africa’s presidential investment drive has secured over 2.4 trillion rand in pledges across six investment conferences, with around 634 billion rand already flowing into the economy. At the most recent 2026 South Africa Investment Conference, the government reported roughly 890 billion rand in commitments across 81 investments—the strongest outcome for a single conference to date. A second mobilization drive has been launched, targeting a further 3 trillion rand in investments over the five years to 2030.32

South Africa’s credit ratings confirm investment case

South Africa’s investment case has been reinforced by recent sovereign rating actions. In May 2026, Moody’s revised South Africa’s outlook from stable to positive, citing improving fiscal performance, rising primary surpluses, and sustained commitment to structural reforms, while explicitly noting that stronger investments supported by reforms should buoy growth over the medium term.

S&P followed suit, on June 1, 2026, by affirming South Africa’s “BB/BB+” ratings after an upgrade in November 2025 and maintaining a positive outlook, highlighting stronger revenue collection, a third consecutive annual primary surplus, and reform progress in electricity and logistics.

Fitch then upgraded South Africa’s long-term foreign- and local-currency issuer default ratings to “BB” from “BB–” on June 5, 2026, with a stable outlook, citing prudent fiscal management, progress on fiscal consolidation, and an improved debt trajectory relative to expectations at the time of its 2020 downgrade.33

Together, these decisions provide external validation that both South Africa’s fiscal trajectory and reform agenda are improving in ways that support investor confidence, lower perceived sovereign risk, and strengthen the case for crowding in private capital alongside the public infrastructure push and wider investment mobilization drive.

Labor market weakness, low confidence, and a tricky political backdrop

The labor market remains a key structural constraint for South Africa. StatsSA’s quarterly labor force survey showed the official unemployment rate rising to 32.7%—up from 31.4% in the previous quarter. Employment fell by 345,000, while the number of unemployed persons increased by 301,000.34 That deterioration is especially concerning as it weakens household demand amid rising inflation and monetary policy tightening.

Business confidence has also moderated recently: The RMB/BER business confidence index dropped by 8 points from the previous quarter to 39, below its long-term average, in the second quarter of 2026. The survey fielded in mid-May pointed to firms experiencing a deteriorating operating environment due to the Middle East conflict and a higher lending-rate environment. Across sectors, a decline in confidence was mostly seen in those exposed to household spending changes, financing conditions, and the effects of elevated fuel prices.35

The Electoral Commission of South Africa confirmed a date—Nov. 4, 2026—for the next local government elections.36 Economic conditions are likely to feature more prominently in political discourse over the coming months, as South Africans head to the polls amid rising living costs, service delivery constraints, and persistent socioeconomic challenges.

A further layer of uncertainty comes from the reemergence of anti-immigrant mobilization in parts of the country. Recent protests, alongside warnings from policy and rights organizations, point to immigration becoming increasingly politicized ahead of the elections, particularly in the context of high unemployment, socioeconomic pressures, and general public frustration. New waves of anti-foreigner incidents—in April, May, and June—saw migrants (and people wrongly mistaken as migrants) being attacked.

There have also been large-scale repatriation efforts supported by different African governments amid safety concerns, together with an increased number of deportations. Meanwhile, the government has pledged greater efforts to crack down on illegal immigration.37

More recently, political noise around potential impeachment proceedings against the president has added to uncertainty, although for now, it remains a tail risk.38 Taken together, these dynamics compound an already fragile external environment.

Looking ahead

The 2026 outlook for South Africa has become more constrained and uncertain compared to expectations at the start of 2026. While South Africa retains a credible pathway to recovery—one that remains fundamentally contingent on continued reform progress—the near-term environment has become much more challenging. As evident from surveys and market commentary, the country is headed for weak growth in 2026, firmer inflation, and interest rates that might remain higher for longer.39

In this context, 2026 seems more to be a year of renewed resilience testing than one of accelerating economic recovery—echoing some of the same dynamics seen in 2025. If external pressures ease, the recovery trajectory could regain momentum from 2027 onward. For now, however, the margin for error—and for additional external shocks—seems to have narrowed significantly.

BY

Hannah Marais

Editorial (including production and copyediting): Arpan Saha, Preetha Devan, and Pubali Dey

Design: Harry Wedel

Audience development: Kelly Cherry

Cover image by: Rahul Bodiga

Knowledge services: Agni Wagh

Visit the Deloitte Global Economics Research Center

Access more insights for the consumer spending, housing, business investment, globalization & international trade, fiscal & monetary policy, sustainability, equity, & climate, labor markets and prices & inflation sectors.