Immigration will play an essential role in shaping the future of US economic growth

The February 2026 Economics Insider analyzes recent US immigration trends and their possible impact on the US economy

Immigration patterns in the United States appear to be shifting after the post-pandemic surge. Between 2022 and 2024, the foreign-born labor force expanded at an average annual rate of 4%,1 while the native-born labor force grew by just 1.1%. But that trend now seems to be changing: Net immigration fell sharply last year, and is expected to fall even further this year.2

At a time when native-population growth is slowing due to persistently low fertility rates, declining immigration is poised to weigh heavily on labor supply, debt sustainability, and long-term economic growth, with negative effects likely to emerge even in the near term. Some localized benefits may arise—such as modest improvements in state and local government budgets that could support wage increases—but these gains will likely be sporadic and limited. Broader economic literature shows that immigration tends to have a net-positive effect on the native-born population across skill levels, though highly skilled immigrants contribute significantly more to the economy through higher earnings, innovation, and spillovers.

Tighter immigration and falling fertility rates could impede labor-force growth

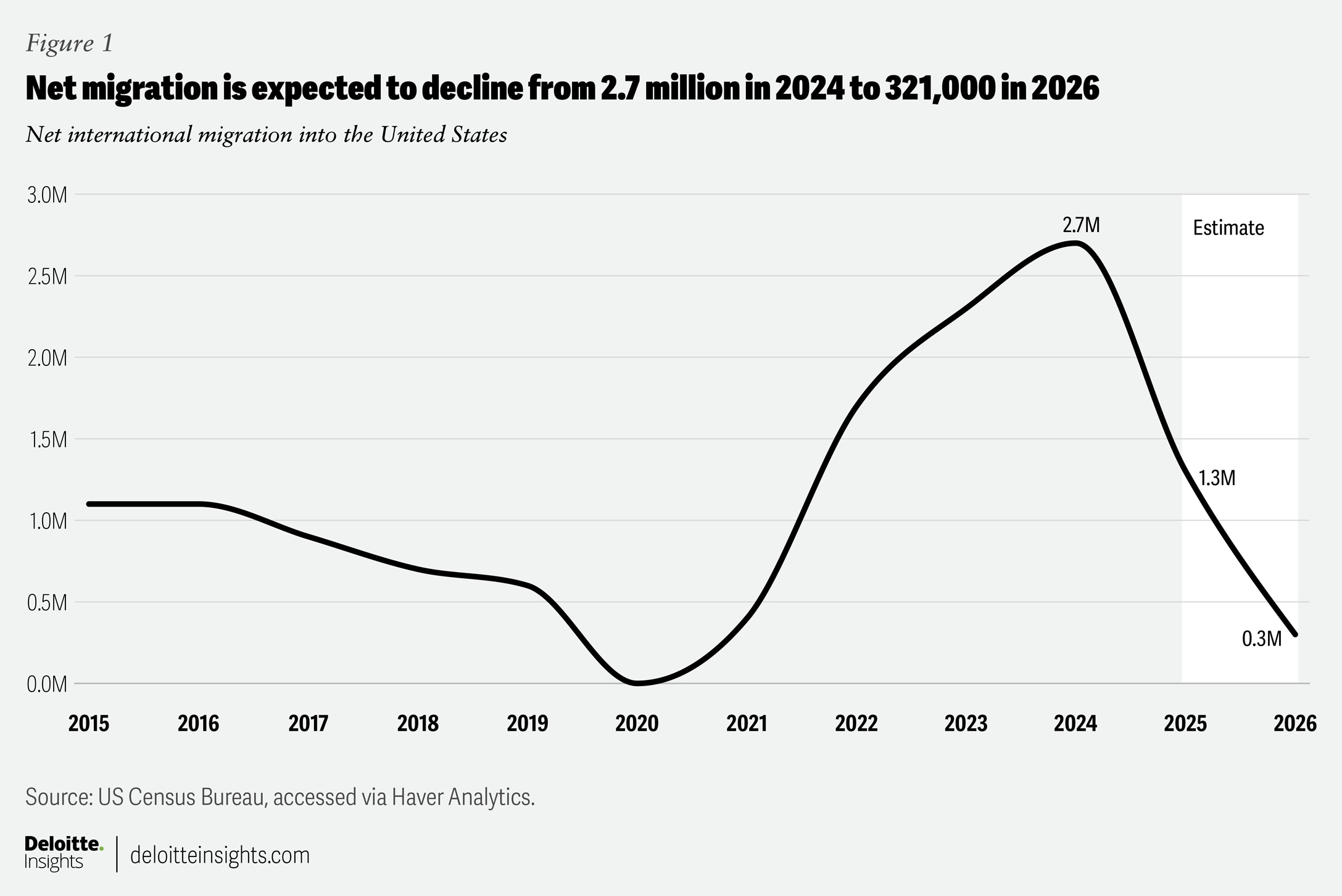

Although exact estimates of net migration vary widely due to differences in policy assumptions, enforcement outcomes, and the inherent difficulty of measuring population flows in real time, most point in the same direction—down. The latest US Census Bureau estimates show that net international migration into the United States went from 2.7 million in the year ending July 1, 2024, to 1.3 million one year later. The estimate also expects that the number to fall even further to just 321,000 in the year ending July 1, 2026 (figure 1). The Congressional Budget Office has made a similar projection for the year.3 Other researchers expect that net migration could even turn negative this year.4

The drop in net migration coincides with weaker demographics. The US fertility rate, which stood at 1.6 in 2024, has been below the 2.1 replacement rate required to sustain population growth since 2008.5 Hence, without immigration, the size of the US population is expected to decline. The drop in fertility partially reflects the aging US population, which is exerting additional downward pressure on labor-force growth. Older individuals are shifting into lower labor-force participation age brackets. That is, baby boomers are quickly retiring. Indeed, the native-born labor force declined in 2024 to 135.8 million from 136.1 million in 2023.6

A reduced labor force is expected to lower output

Demographic shifts carry macroeconomic consequences: Generally, more people and workers in a country translate to more spending and higher economic output. For example, the Congressional Budget Office estimated that a rise of 8.7 million immigrants over a five-year period would raise real gross domestic product by 2.9% a decade later.7 It also found that higher immigration leads to a rise in the labor force, higher employment, and greater productivity growth.

These factors also have a positive effect on the federal deficit, allowing revenue to rise faster than expenditure. A study by the International Monetary Fund also found that stronger rates of immigration drive lower local inflation.8 In the long term, immigration also contributes to economic output through intergenerational effects. Children of immigrants are more likely to attain postsecondary education9 and secure higher-paying jobs, thereby raising economic output more than the average. For example, in 2023, while 53% of first-generation immigrants have some postsecondary education, 68% of second-generation immigrants pursue higher education. That is even larger than the 63% of the native-born population in the latter category.10

But despite the positive implications, there are still some potential economic downsides to immigration. For example, there is some evidence that state and local government budgets can become more strained under higher immigration scenarios, depending on the laws in each jurisdiction.11 In addition, housing costs can move higher, particularly in the short run, when there is a large increase in immigration.12 However, the rise in housing costs is typically smaller than the fall in other prices.

It is also possible that the rise in economic value and employment from a wave of immigration could result in adverse effects for the native-born population. However, economic literature suggests that that is not the case. In fact, research shows that immigration boosts output without reducing native employment.13 There is also scant evidence that native-born workers’ wages are adversely affected. If anything, native-born worker wages rise after a wave of immigration.14

This result may seem counterintuitive. A rapid increase in able-bodied workers willing to accept relatively low wages might be expected to weaken native workers’ employment and wage prospects. However, immigrant workers are not perfect substitutes for native workers. Instead, workers who would otherwise compete with immigrant labor move into different tasks that allow them to maintain their employment and increase their wages. The group of workers that are most vulnerable to a new wave of immigration is previous immigrants.15 These are the workers who tend to compete more directly with newer migrants.

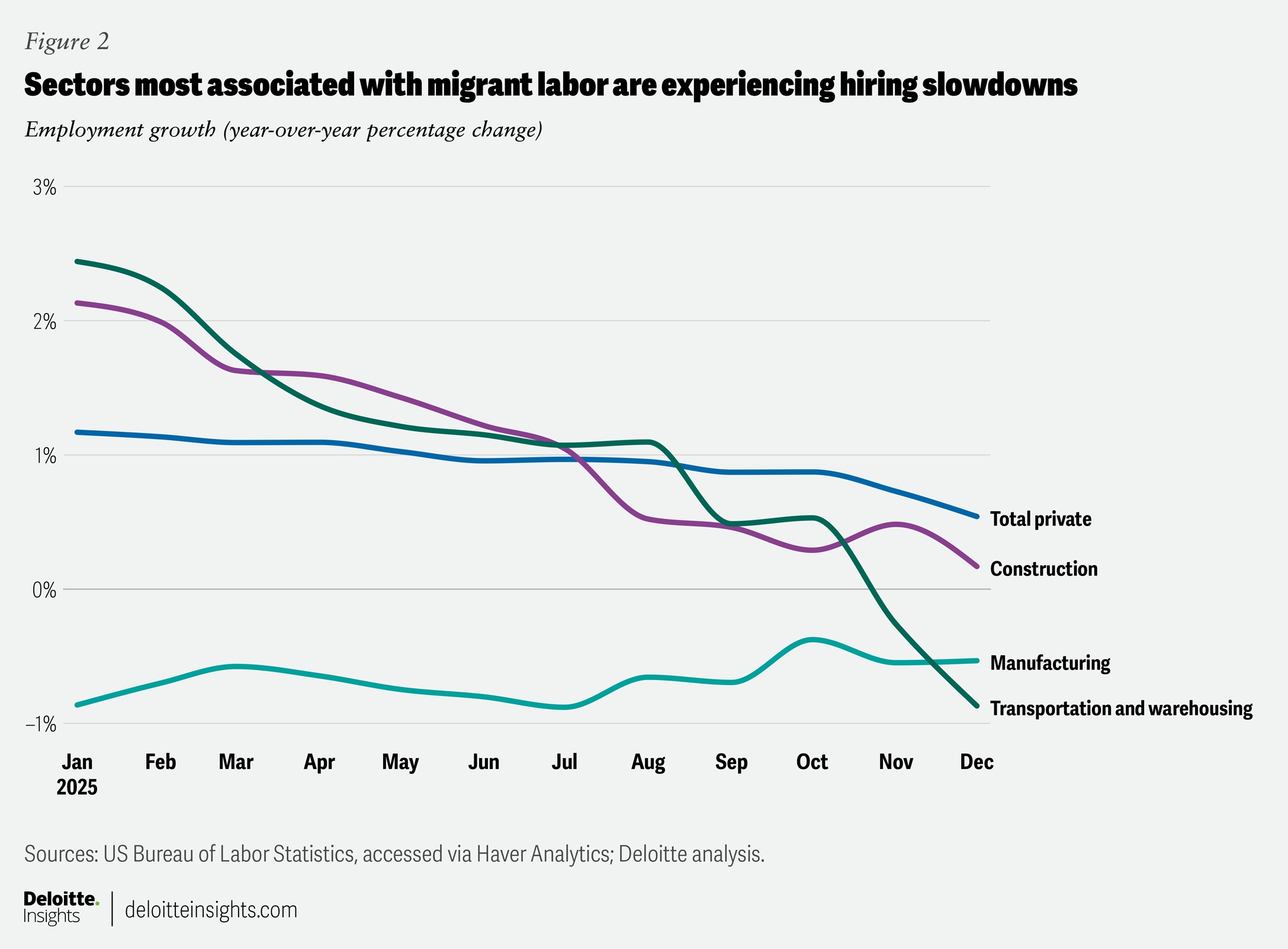

We are likely already seeing the effects of slowing net migration on the labor force. Payroll growth averaged just 29,000 per month between October and December 2025—well below the 166,000 recorded per month in 2024.16 We do not know for certain how much of the employment growth slowdown is due to a drop in net migration. However, based on the latest Census Bureau estimates, researchers have estimated that the sustainable pace of monthly job growth was between 20,000 and 50,000 at the end of 2025.17 In addition, certain sectors that typically employ large shares of immigrants, such as construction, transportation, and manufacturing, are seeing a sharper slowdown in hiring when compared with others.18

High-skilled immigrants contribute more to economic output

Immigrants are not all the same, and neither are their economic contributions. Their skill level makes a significant difference when it comes to their effect on the economy. For example, highly skilled immigrants represent only about 5% of the US workforce, but they generate over 10% of national labor income.19 Some of this is due to the fact that high-skilled immigrants earn above-average wages. For example, median wages for H-1B recipients range from US$97,000 (initial employment) to US$132,000 (continuing employment)20—almost double the national median income.21 According to the Penn Wharton Budget Model, keeping total immigration constant while raising the share of high-skill immigrants would result in higher economic growth compared to a scenario with a larger share of low-skill immigrants.22

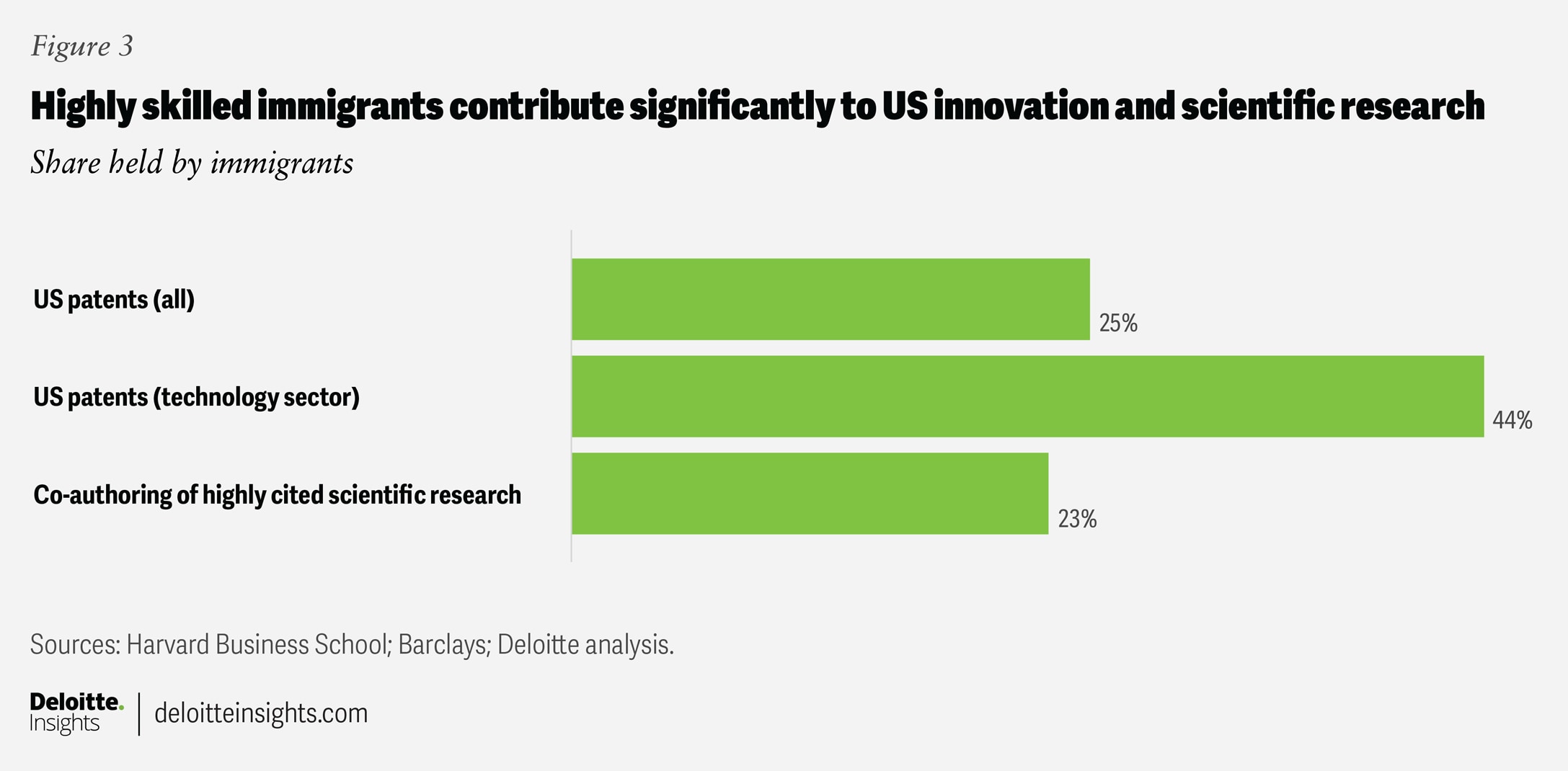

However, it is not just salaries that are important for growth. High-skill workers also tend to be more innovative than the average worker, which raises productivity growth. Research shows that such immigrants account for nearly one-third of aggregate innovation in the United States.23 These workers contribute more than 25% of all US patents by total market value, including 44% of all tech-sector patents,24 and coauthor 23% of highly cited scientific works.25 Immigrant inventors not only complement their native-born counterparts but are also productive for more years, thereby generating greater economic value.26

Although high-skilled immigrant workers make outsized contributions to economic growth, low-skill immigrant workers’ contributions have also been positive. At an aggregate level, even those immigration surges that include large numbers of lower-wage workers raise federal revenues and economic activity, as reflected in Congressional Budget Office budget analyses.27 Conversely, the reduction of unauthorized immigrants—who are disproportionately employed in lower-skilled roles—would place the economy on a weaker growth trajectory. Some estimates suggest that the removal of roughly five million unauthorized migrants by 2028 could reduce GDP by about 1 percentage point.28 According to the Federal Reserve Bank of Dallas, immigrants employed in labor-intensive sectors such as agriculture, construction, hospitality, and care services complement the existing workforce, increasing production capacity and easing inflation.29

There is, however, some disagreement regarding the effect of low-skill immigration on the economic prospects of the native population. The degree of substitution of new immigrants’ skills determines the extent of adverse impact, if any, on the native population.30 Some studies show that a native-born worker with less than a high school diploma is the closest substitute for an incoming low-skilled immigrant and. hence, prone to experience more pressure on employment and wages.31

However, other experts have noted that such studies have very small sample sizes and make assumptions that appear to be at odds with empirical evidence.32 Either way, the share of native-born workers with less than a high school diploma in the civilian workforce is a mere 5.3%,33 highlighting just how limited any potential negative employment and wage effects are on the native population. Certain studies also find that as immigrants enter the labor force, native-born workers move to new occupations that require higher skills or to more complex tasks, which results in economywide productivity gains.34

Despite these nuances, economic evidence suggests that a sustained decline in net migration would restrain US GDP growth relative to a scenario without such tightening. This holds true even if the reduction is concentrated among lower-skilled workers, as immigration broadly supports labor-force growth, production capacity, and aggregate demand. The growth impact, however, would be more muted than in a scenario involving a large outflow of highly skilled immigrants whose contributions to innovation and productivity are disproportionately large. While tighter immigration could yield modest and localized benefits—such as improved state and local government budgets and a stronger labor market for the small share of native-born workers without a high school diploma—these effects are uncertain, narrowly distributed, and unlikely to offset the broader economic losses associated with a decline in immigration.

By

Michael Wolf

Rohini Sanyal

Editorial (including production and copyediting): Arpan Saha, Sayanika Bordoloi, Cintia Cheong, and Pubali Dey

Design: Harry Wedel and Govindh Raj

Audience development: Atira Anderson

Cover image by: Harry Wedel

Knowledge Services: Agni Wagh

Visit the Deloitte Global Economics Research Center

Access more insights for the consumer spending, housing, business investment, globalization & international trade, fiscal & monetary policy, sustainability, equity, & climate, labor markets and prices & inflation sectors.