Permission to splurge: Gen AI is changing how consumers treat themselves

Gen AI tools are emerging as valuable companions along the splurge journey

Who doesn’t love a little treat now and then, especially when stressed?

Every month, at least 7 in 10 US consumers surveyed treat themselves to something special, driven by a need for comfort, temporary escape, and a little well-earned joy.1 That hasn’t changed since we first reported on this behavior in our 2023 report, “For consumers, splurges aren't just lipstick.”2

What has evolved since then is how consumers find, evaluate, and justify those splurges. Recent US ConsumerSignals data shows that generative AI tools are now embedded in the purchase journey for nearly half of all splurgers, indicating a structural shift in the path to purchase (see methodology).3

Here’s a big-ticket treat for retailers: Splurgers who find gen AI useful tend to treat themselves more often and spend 2.3 times more on their priciest treat.4

The rise of gen AI’s influence along the splurge journey presents an opportunity for retailers to capture more value from every treat—whether it’s lipstick or a lawnmower—by meeting consumers in the right place with the right reason to buy.

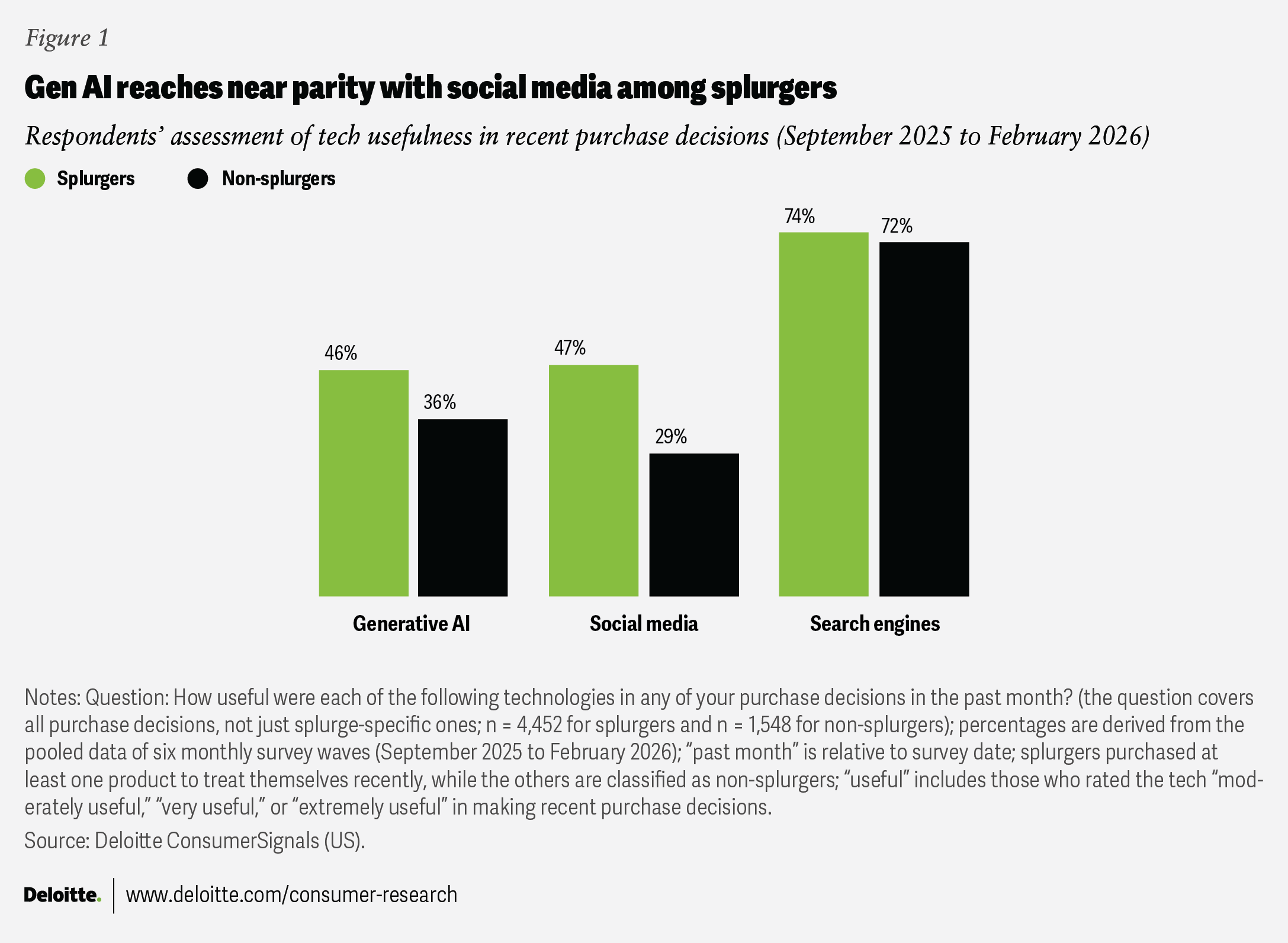

Decoding gen AI’s influence on splurge behavior

While search engines remain the dominant discovery channel for purchase decisions, what’s remarkable is that, for respondents, gen AI usefulness has surged to near parity with social media, where retailers have invested for more than a decade, in a fraction of the time.

With gen AI exerting a comparable level of influence over splurgers’ purchase decisions, retailers should consider treating it as a relevant journey touchpoint, not a future experiment (figure 1).

Beyond influence, our data indicates a compounding effect that amplifies both frequency and spending.

- Gen AI is associated with higher purchase frequency. Splurgers who find gen AI useful in their shopping journey are 61% more likely to make three or more treat purchases in a month.

- Active splurgers spend much more. Those who make three or more treat purchases a month spend 93% more on their priciest treat purchase than those who make one or two treat purchases a month.

- Clothing and accessories top digital splurge purchases. While food and beverages lead overall splurge purchases, consumers who find gen AI useful are more likely to treat themselves to clothing and accessories, a pattern consistent with social and search behavior.

Tailoring splurge moments to motivations

What makes a purchase splurge-worthy isn’t one-size-fits-all. Our previous research found that drivers shift across categories and even price points within them.5 Layer in various demographics, regional preferences, and life stages, and the picture grows more complex.

Our splurge survey shows that age is one useful lens.

- Younger consumers (18 to 34 years) are primarily impulse-driven, acting on purchasing something they couldn’t pass up, suggesting that urgency and novelty could be effective levers.6

- Middle-aged consumers (35 to 54 years) are more likely to splurge on something they’ve been eyeing for a while, pointing to a longer consideration window where discovery and inspiration can have more of an impact.7

- Older consumers (55+ years) are primarily motivated by a deal they can’t pass up, making value the most effective splurge driver for this group.8

Retailers who connect customer data to these motivational and behavioral patterns across channels may be better positioned to deliver not just the right product, but also the right reason to buy it, at the right moment.

Where retailers should invest

The 2.3x splurge spend differential represents an opportunity for retailers, especially those that have their data infrastructure in order. Retailers who have spent a decade optimizing for human shoppers on a glass screen now have to optimize for machine readers acting on a shopper’s behalf. Here are three steps retailers can consider now.

- Make your catalog AI-readable. Gen AI can only recommend what it can find, parse, and trust. Retailers with clean, structured product data are likely already ahead the moment a splurge decision materializes.

- Use motivational drivers. Retailers who connect unified customer data to motivations across gen AI, search, and social may be better positioned to turn a browser into a potential buyer.

- Design for the next splurge, not just this one. To continuously capture this multiplier effect, retailers should employ a closed-loop measurement system that tracks splurge cadence at both the transaction and customer level so they better understand how and when to re-engage.

The path to splurge purchase has changed, with gen AI emerging as a useful shopping companion. The retailers who show up with the right product, the right message, and the data infrastructure to consistently meet these moments stand to capture more value from every splurge occasion.

Methodology

This analysis is based on survey data collected via the Deloitte ConsumerSignals platform in six monthly waves from September 2025 through February 2026. The sample consisted of 6,000 US respondents (approximately n = 1,000 per wave). Note that “splurgers” refer to respondents who reported making at least one purchase to treat themselves in the past month (n = 4,452), with “past month” being relative to the survey date. Unless otherwise noted, findings in this paper are based on this pooled US sample.

by

Natalie Martini

Brian McCarthy

Lupine Skelly

Stephen Rogers

The authors would like to thank Sofia Barbieri, Anup Raju, Ram Sangadi, Manvi Verma, Sanjay Vadrevu, and Akash Kumar for their support and research throughout the development of this report.

Editorial (including production and copyediting): Rithu Thomas, Preetha Devan, and Pubali Dey

Design: Molly Piersol and Natalie Pfaff

Audience development: Kelly Cherry

Cover image by: Alexis Werbeck; Adobe Stock

Knowledge services: Vanapalli Viswa Teja

Visit the Deloitte Consumer Industry Center

Access more insights for the automotive, consumer products, food, retail, wholesale and distribution, airlines and hospitality, and transportation sectors.