Confidence under pressure: How life sciences leaders are recalibrating for the rest of 2026

Life sciences leaders say they’re focused on the economic and policy environment, while increasingly confident in their organizations’ ability to navigate it

Based on new Deloitte research—including an April 2026 survey of 150 life sciences executives and an analysis of first-quarter earnings calls—life sciences leaders indicate a nuanced signal at midyear: Confidence is strengthening, but not necessarily because of any shifts in external conditions (see methodology).

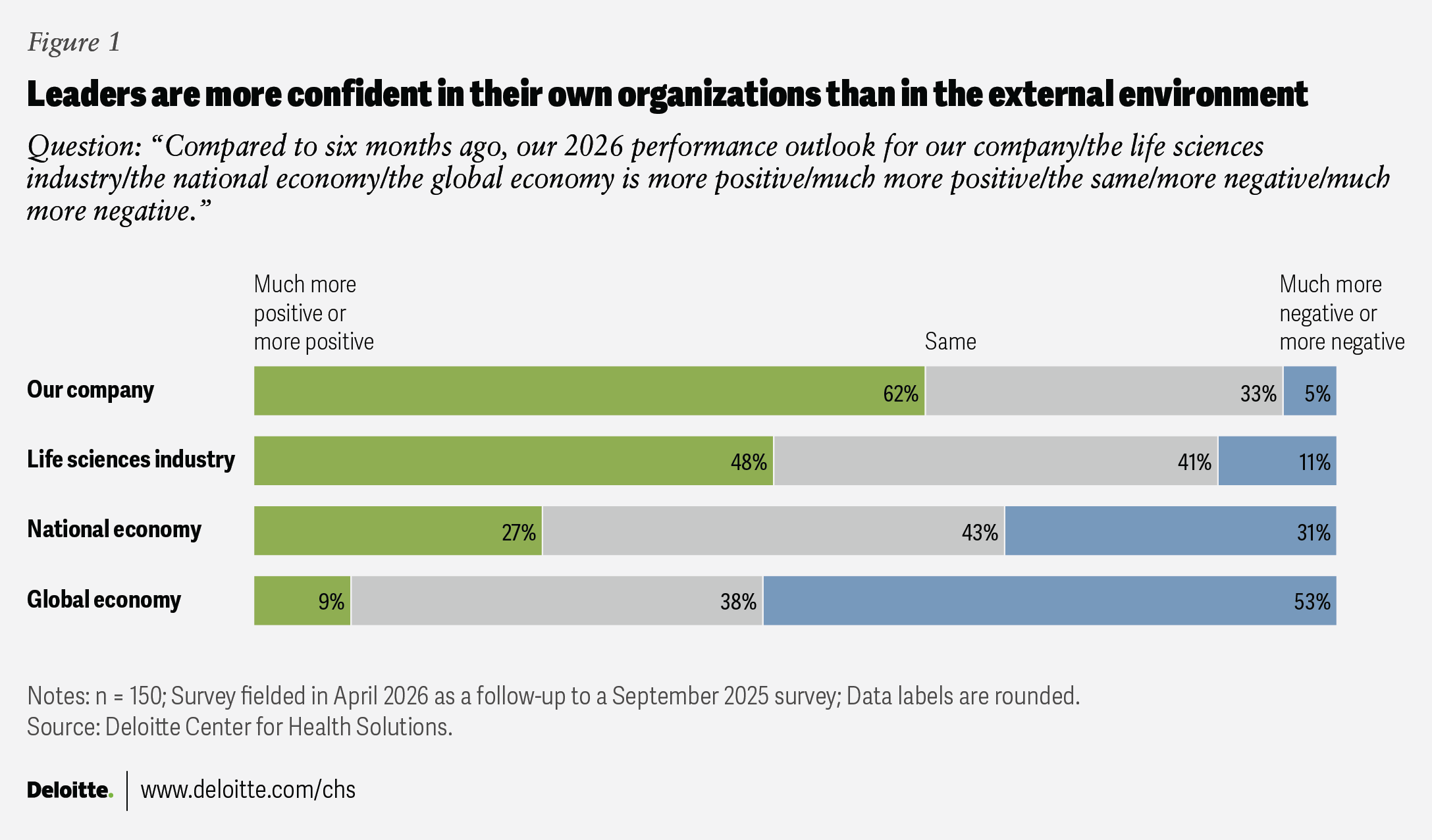

Just 9% of surveyed leaders said they were feeling more positive about the global economy than they were six months earlier. By contrast, 62% said they felt more positive or much more positive about their own company’s outlook compared with six months earlier (figure 1).

As companies enter the second half of 2026, the focus tends to be on strengthening the fundamentals: productivity, commercial performance, investment discipline, partnerships, resilience, and artificial intelligence deployment. While the external environment may remain uncertain, leaders appear increasingly confident in their ability to perform within it.

table of contents

- Internal confidence rises

- External pressures converge

- Pragmatic, proactive response

- AI advances, but value capture lags

- Turning confidence into action

Confidence is improving internally, not externally

The gap between external caution and internal confidence helps explain the sector’s midyear posture. Surveyed leaders express greater confidence in their ability to execute on existing strategy despite the uncertainty.

Deloitte’s 2026 Life Sciences Outlook framed the year as a balancing act between innovation and resilience. At midyear, that balance looks more concrete. Leaders continue to invest in innovation, but with greater emphasis on execution: where to allocate capital, how to improve productivity, where to partner, and how to build resilience into the operating model.

The strategic question is how to keep moving with discipline while the external environment remains difficult for the industry to predict.

External pressures are converging

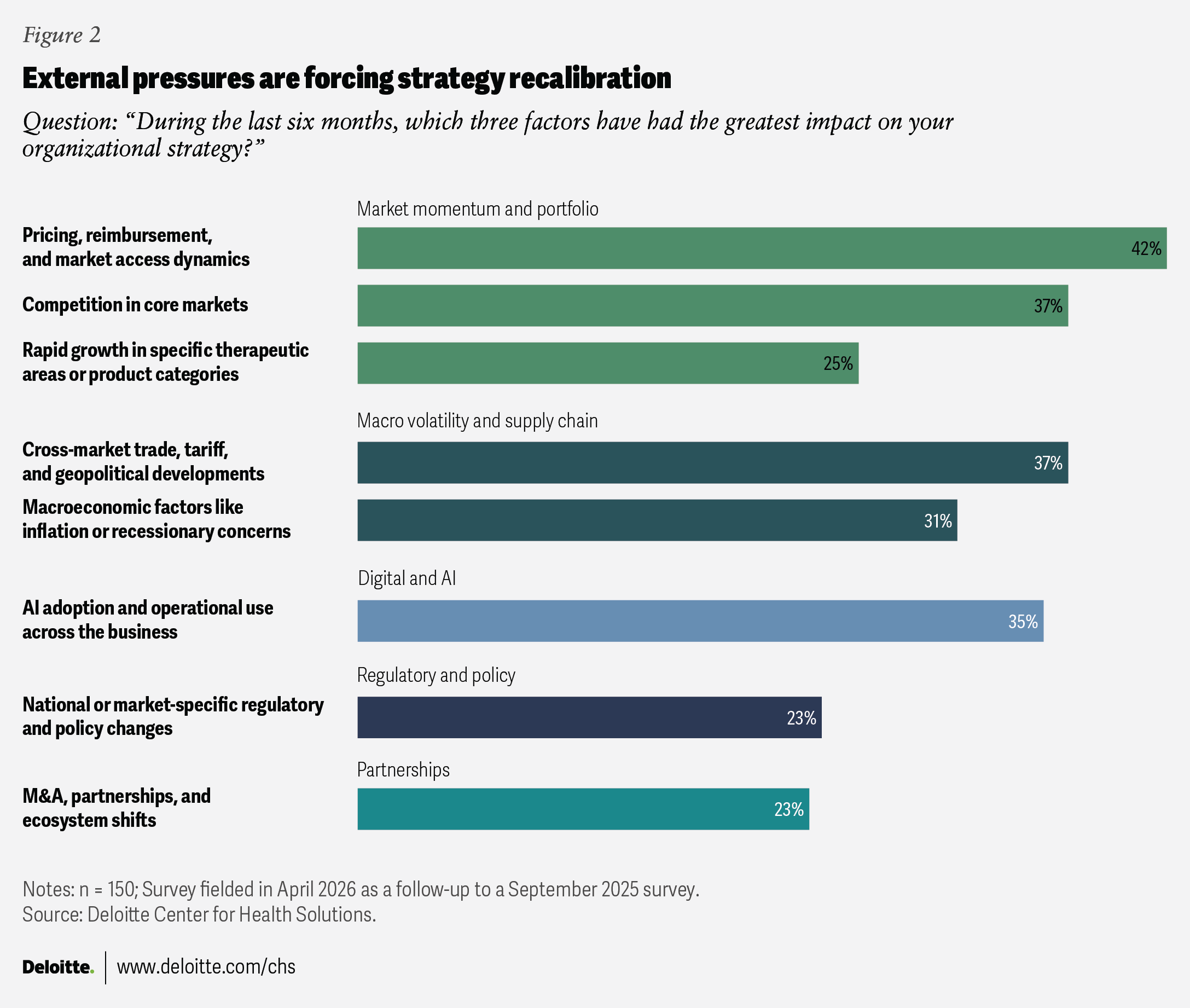

Life sciences leaders continue to manage overlapping forces: pricing and access challenges, competition, macroeconomic and geopolitical volatility, technological advances, and regulatory and policy uncertainty (figure 2).

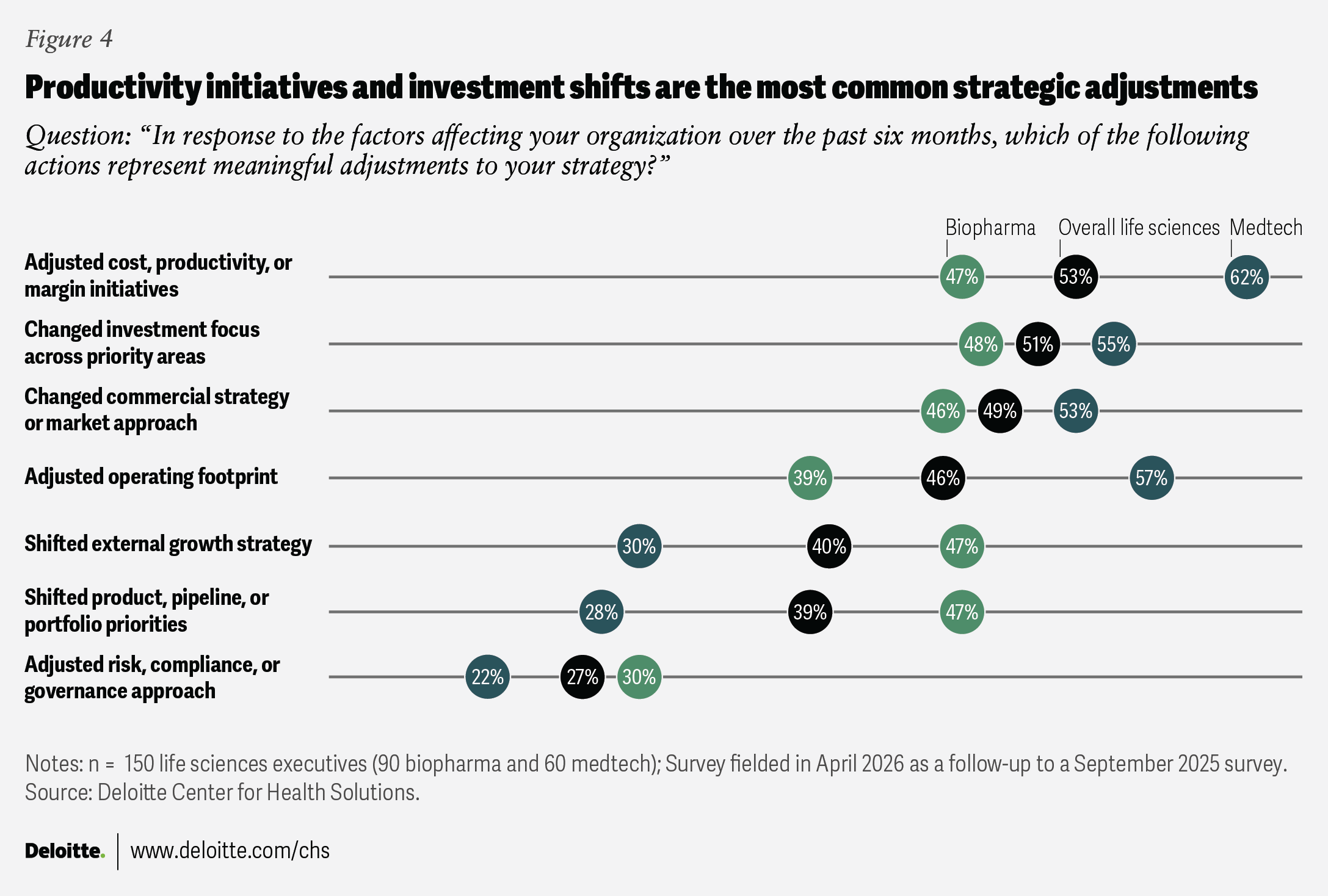

These pressures appear to be converging, which can make the operating environment complex, even for companies that remain confident in their own internal trajectory. For now, many companies are maintaining their broader strategic direction while making targeted adjustments to priorities and execution (figure 4).

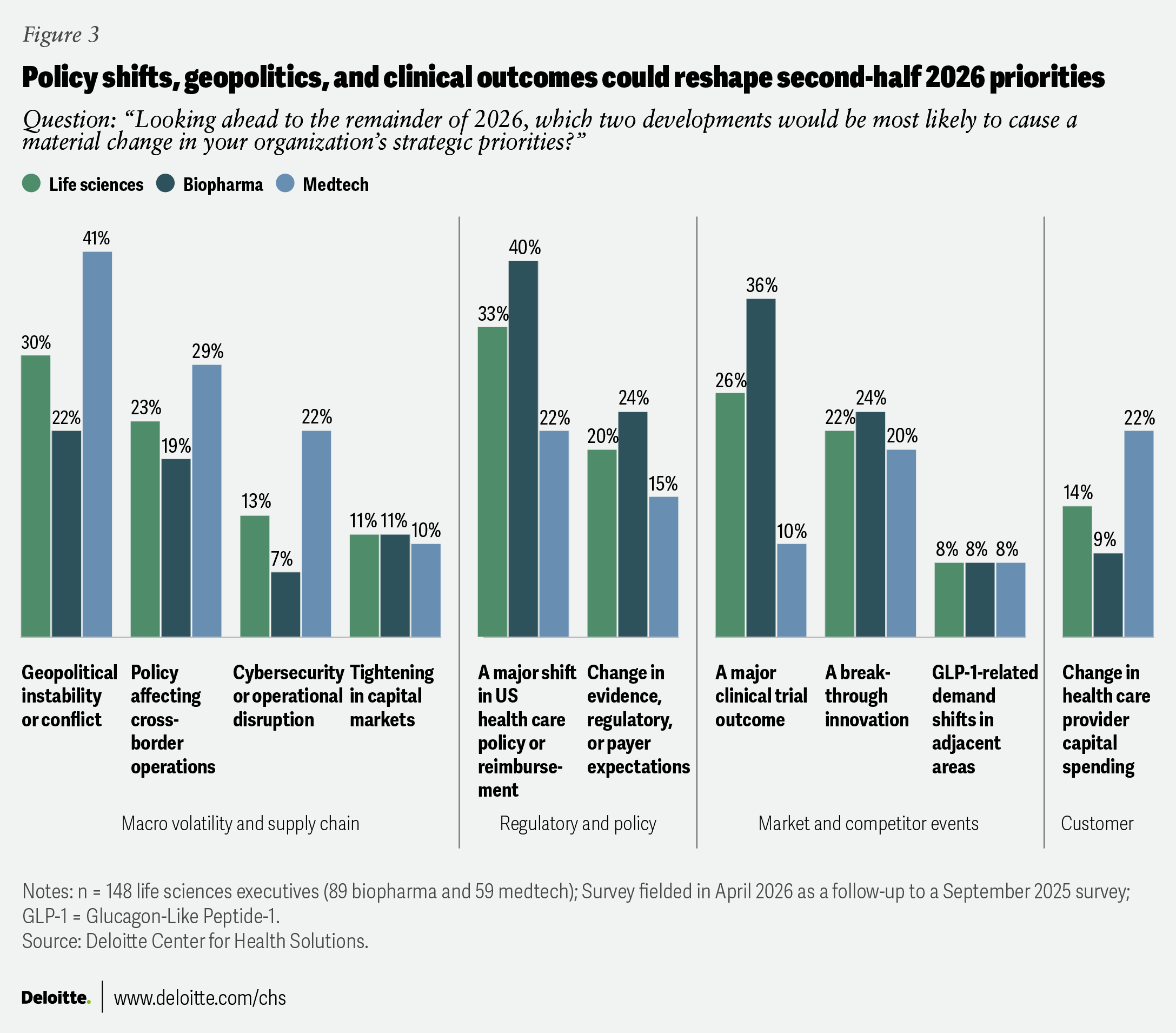

That said, external risks aren’t distributed evenly across the sector (figure 3). In biopharma, survey responses suggest that the most consequential risks may arise from policy and reimbursement shifts, unpredictable clinical outcomes, and the possibility that scientific or competitive developments could reset expectations quickly. In medtech, the most consequential external risks may come from macroeconomic and care-delivery dynamics, where geopolitics, economic policies, provider capital spending, and utilization trends can affect performance.

The response is pragmatic and proactive

Some companies report responding to these external factors through familiar but practical levers such as cost and productivity programs, commercial strategy, investment prioritization, operating footprint decisions, and portfolio choices (figure 4).

Investment allocation signals disciplined growth

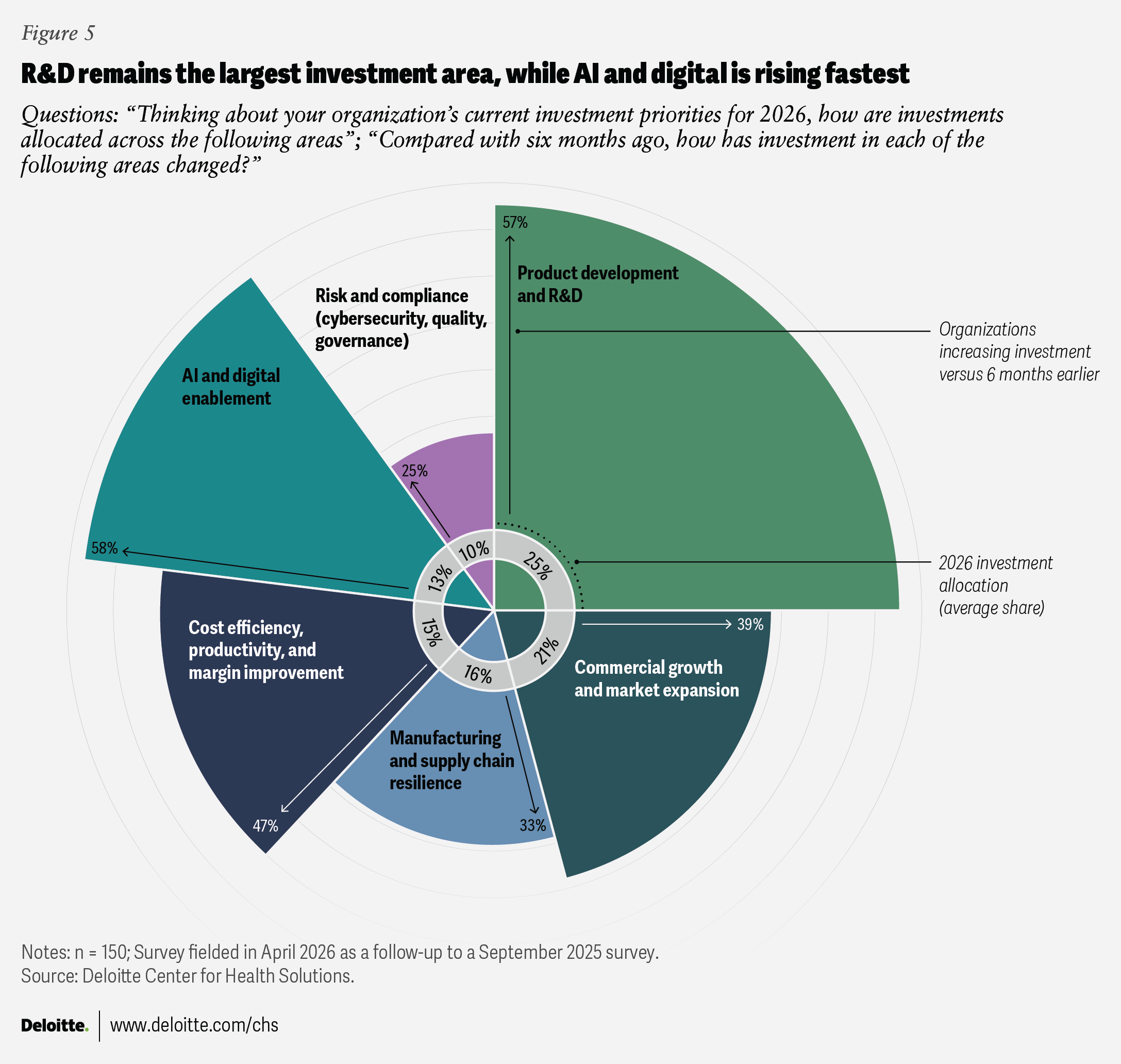

Investment patterns reinforce the same message: Our analysis suggests that life sciences companies are still pursuing growth, but with more discipline. Research and development is the largest area of investment, reflecting the continued importance of pipeline renewal, product development, and evidence generation. At the same time, reported investment in AI and digital is growing at a similar rate as R&D (figure 5).1 Cost efficiency, productivity, and margin improvement also show strong momentum.

About half (49%) of surveyed leaders describe their company’s current investment posture as balanced between growth and risk management, while 36% describe it as more growth-oriented than it was six months earlier.

Taken together, the pattern suggests a more disciplined growth agenda that funds the areas that matter most to organizations, improves execution, and preserves flexibility if conditions change.

Partnerships can be a practical way for companies to move faster without overextending internal capabilities. Midyear survey data suggests that partnerships can be especially important for AI capabilities (61%) as well as innovation, product, or pipeline development (45%), helping companies access capabilities and scale faster than they may be able to on their own.

Earnings call questions suggest investors are asking for proof, not promises

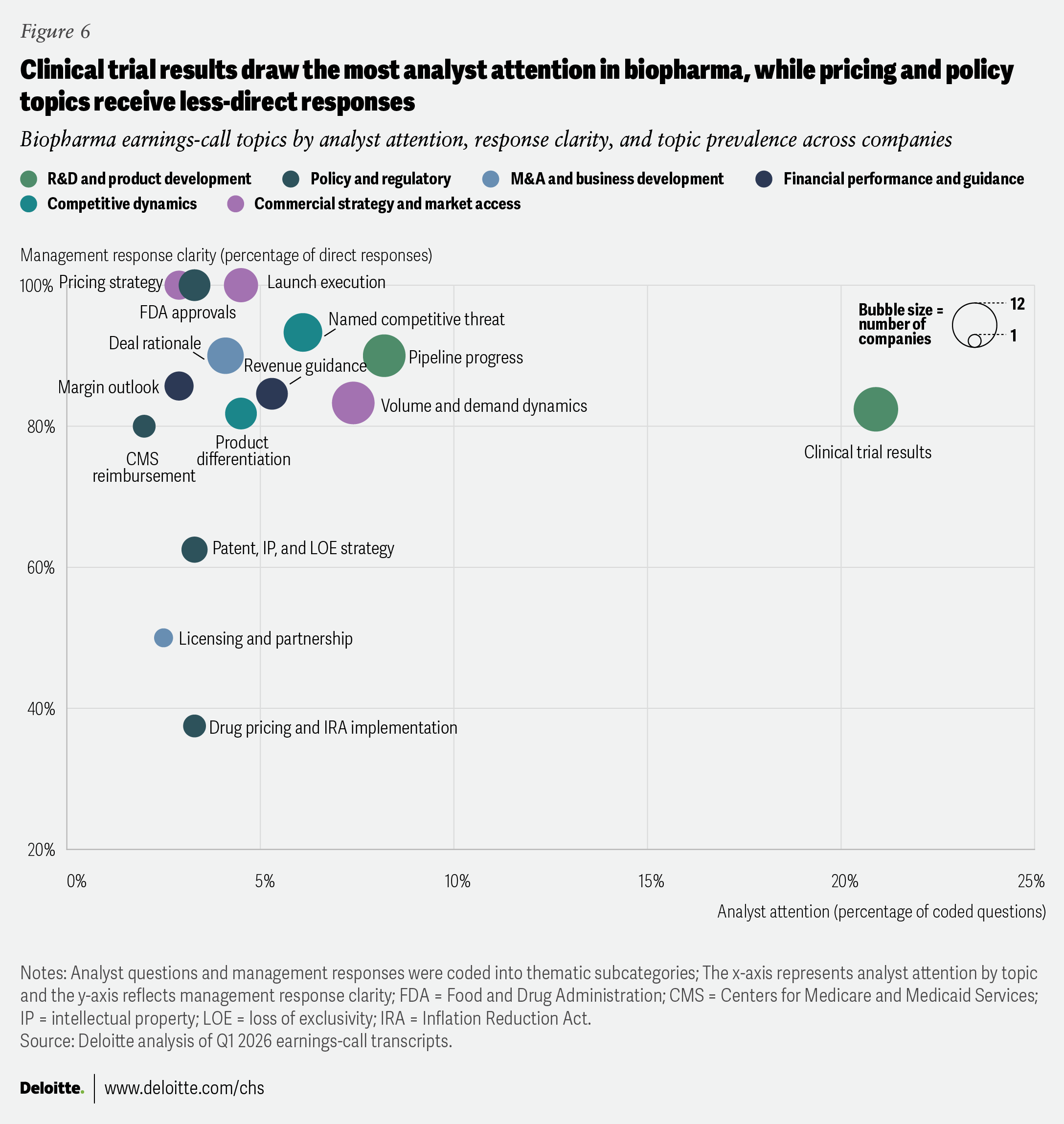

Our analysis of first-quarter 2026 earnings call transcripts suggests that life sciences companies are likely being pressed not only on where they invest but also on whether those investments are delivering measurable results.

In biopharma, analyst attention centered on R&D and product development, commercial strategy and market access, and competitive dynamics. Questions frequently focused on clinical trial results, pipeline progress, launch execution, demand trends, differentiation, and competitive threats. These questions suggest a strong focus on whether companies can convert innovation into commercial performance (figure 6).

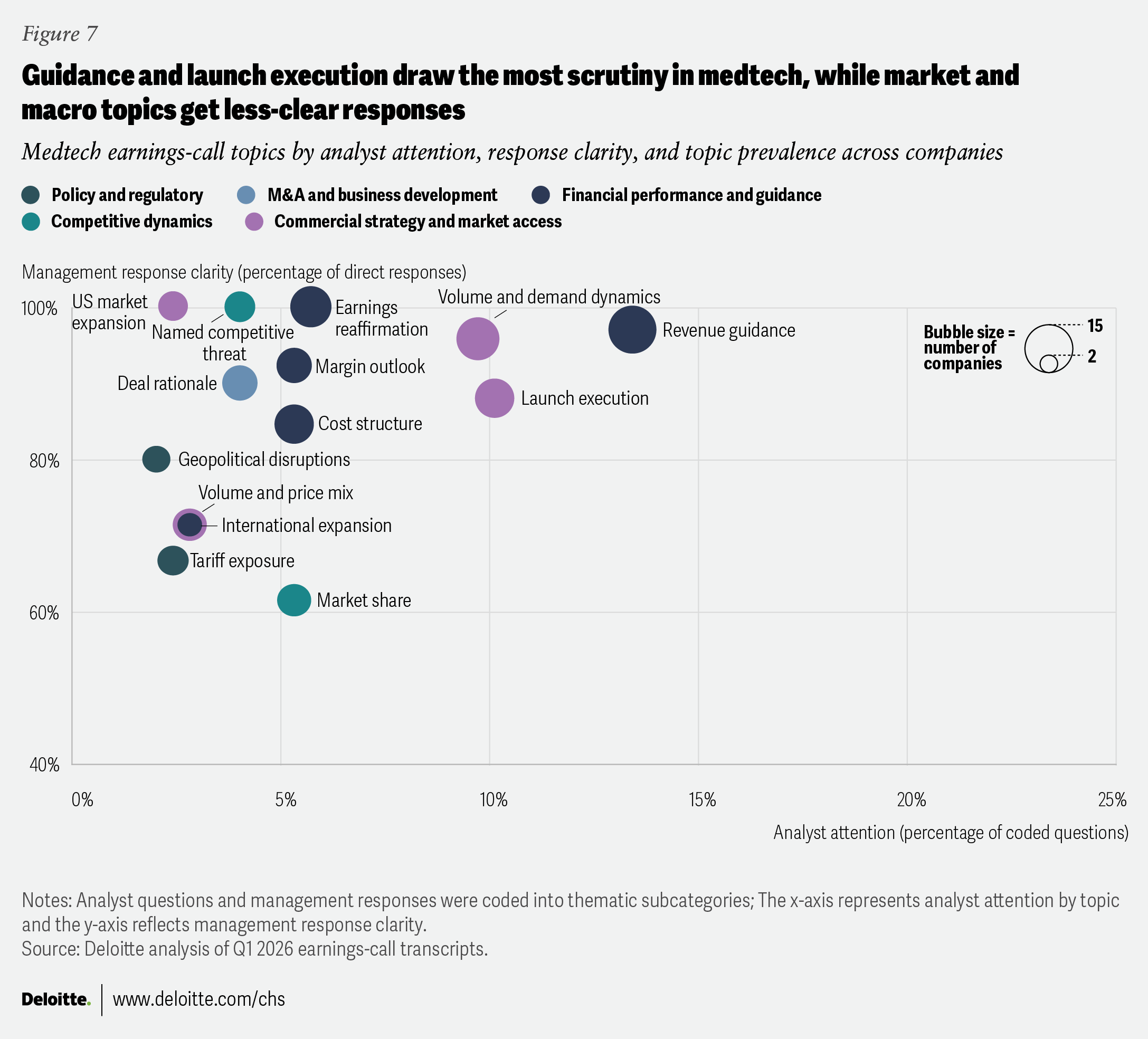

In medtech, the emphasis is somewhat different. Analyst attention focused more heavily on financial performance and guidance, commercial strategy and market access, and competitive dynamics. Questions often centered on revenue outlook, launch execution, demand trends, margins, cost structure, and market share. This suggests that analysts are likely watching whether companies can sustain growth, protect profitability, and defend guidance while continuing to invest in innovation and transformation (figure 7).

Notably, management teams were generally more direct on issues with greater control, influence, or measurability, including clinical trial readouts, launch execution, guidance, and demand trends. Launch execution and guidance are largely within management’s control; clinical readouts provide known evidence once reported; and demand, while less controllable, can be measured and influenced. Responses were less consistently clear on topics shaped by policy, reimbursement, tariffs, international exposure, and market structure, reinforcing the survey finding that leaders generally see policy and macro conditions as key sources of uncertainty for the rest of 2026.

AI is advancing, but value capture is still catching up

AI and digital enablement is one of the clearest areas of investment momentum in the survey. Seventy-one percent of respondents said AI deployment has advanced at least somewhat compared with six months earlier. Meanwhile, 35% reported significant progress in agentic AI, including enterprisewide rollout or scaling. But fewer respondents reported measurable performance gains: 45% said their AI initiatives have produced measurable improvement, including 13% who reported measurable improvements at scale.

That gap suggests deployment is advancing faster than many companies’ ability to define success measures, set baselines, and track impact consistently. For the rest of 2026, the AI question may increasingly be one of proof: Which use cases improve outcomes? Which workflows need to be redesigned? And how will value be tracked consistently across the enterprise?

Turning confidence into measurable action

The midyear outlook shows that companies generally believe they can manage through uncertainty (figures 6 and 7). Based on the survey findings and earnings-call analysis, three considerations stand out for the second half of 2026:

- Strengthen resilience where exposure is highest. For biopharma, that may mean improving regulatory and competitive intelligence, evidence strategy, pipeline execution, and launch readiness. For medtech, it may be about competitive positioning, supply chain management and operating footprints, cyber and operational continuity, and planning for volatility in provider capital spending.

- Make AI value measurable. AI deployment appears to be advancing faster than value measurement. Leaders should focus on workflow redesign, governance, key performance indicator definition, and use cases where impact can be tracked.

- Prepare for sharper pivots. Companies may be staying the course now, but changes in policy, geopolitical conditions, clinical or regulatory changes, supply chain disruption, and breakthrough innovation could still have an impact on an organization’s priorities before year-end.

In the second half of 2026, industry leaders may not be able to control the global economy, policy shifts, reimbursement pressure, or the pace of disruption. But they can control how decisively they allocate resources, how quickly they improve productivity, how effectively they execute commercially, how selectively they partner, and how rigorously they measure AI value.

The companies that perform best may not be the ones that wait for conditions to improve before acting. They may be the ones that turn internal confidence into disciplined, measurable action.

Methodology

Survey methodology: The Deloitte US Center for Health Solutions and Deloitte Global surveyed 150 C-suite and senior executives from life sciences companies, including 90 from biopharma and 60 from medtech. In this study, biopharma is defined as organizations focused on developing and commercializing drug and biologic therapies, while medtech refers to companies that design and manufacture medical devices and diagnostic equipment. Respondents represented pharmaceutical, biotechnology, biosimilar, and medical device manufacturers that operate primarily in the United States, Europe (France, Germany, Switzerland, and the United Kingdom), and Asia (China and Japan). The survey was conducted in April 2026.

As a reference point, the 2026 Life Sciences Outlook surveyed 280 life sciences executives, including 180 from biopharma and 100 from medtech, from the same roles and geographies, with fieldwork conducted in August and September 2025.

Earnings-call analysis methodology: The Deloitte US Center for Health Solutions analyzed Q1 2026 earnings-call Q&A transcripts from 14 biopharma companies and 17 medtech companies. Analyst exchanges were broken into discrete question units and coded by primary category and subcategory to identify where investors were applying pressure. Management responses were coded as direct, cautiously direct, hedged, deflected, or not answered to assess response clarity. Our observations are based on coded Q&A patterns from the earnings calls analyzed and should be interpreted as directional rather than representative of all public companies.

Categories included financial performance and guidance; commercial strategy and market access; R&D and product development; competitive dynamics; policy and regulatory; operations and supply chain; mergers and acquisitions and business development; workforce and operating model; and capital allocation. Subcategories captured more specific topics, such as clinical trial results, pipeline progress, launch execution, demand trends, pricing and reimbursement, margin outlook, market share, competitive threats, supply chain, AI and digital enablement, partnerships, and capital deployment.

In figures 6 and 7, the x-axis represents management clarity, the y-axis represents each subcategory’s share of coded analyst question units, and the bubble size reflects the number of companies where the subcategory appeared.

Continue the conversation

Meet the industry leaders

by

Pete Lyons

Todd Konersmann

Sheryl Jacobson

Dr. Jay Bhatt

Darshan Gosalia

The authors would like to express their gratitude to those who contributed to this paper.

Project team: Natasha Elsner led the survey design and supported analysis, narrative development, and writing key sections of the report. Apoorva Singh led the earnings call research, designed a generative AI-driven analytical framework, generated key insights, interpreted key findings, and helped write key sections of the report. Anjalee Khemlani reviewed the report, provided subject matter expertise, and helped shape its narrative direction. Jared Johnson provided editorial guidance throughout the process.

The authors wish to thank Rob Jacoby, Andrew Davis, Frank Bressau, and Tobias Langenberg for reviewing the survey and the report. Special thanks to Terry Koch, Scott Sun, Marc Caeneghem, Michael Dohrmann, Shinji Nishigami, Alex Mirow, Colin Jeffery, Teresa Leste, and Lynn Marks for their support.

The authors would like to thank Leah Micalizzi, Namrita Negi, Chase Langhorne, George Forakis, Liv Rogal, Lisa Illif, Christie Murphy, and Roxanne Lucy for their subject matter expertise and review.

The authors express appreciation for Rebecca Knutsen’s significant contributions to the editorial strategy of the paper. Additional thanks to Shyamili M, Debra Pielack (Asay), Jennifer Wotczak, Julie Landmesser, Christina Giambrone, Dimple Jobanputra, Jesse Antony, Radhika Pandey, Komal Sapra, and the many others who contributed to the project. The authors would like to thank Alexis Werbeck and Natalie Pfaff for their creative work on the paper’s art concept and visuals.

Cover image by: Alexis Werbeck; Adobe Stock

Knowledge services: Rishitha Bichapogu

Visit the Deloitte Center for Health Solutions

Access more insights for the hospital, health system and provider, pharmaceutical manufacturer, health plan and payer, medtech, and health tech organization sectors.