Digitally enabled supply chains make recovery speed a medtech differentiator

Digital capabilities can help medtech organizations sense earlier, decide faster, execute tradeoffs in near real time, and turn recovery speed into outperformance

How a medtech company handles its next supply chain disruption may reveal something more fundamental than resilience: whether it can recover faster than competitors. Research conducted by the Deloitte Center for Health Solutions, including a November 2025 survey of 100 medtech executives across 15 countries and two in-depth executive interviews, suggests recovery speed is increasingly a performance separator, and digital enablement is what makes that speed achievable (see methodology).

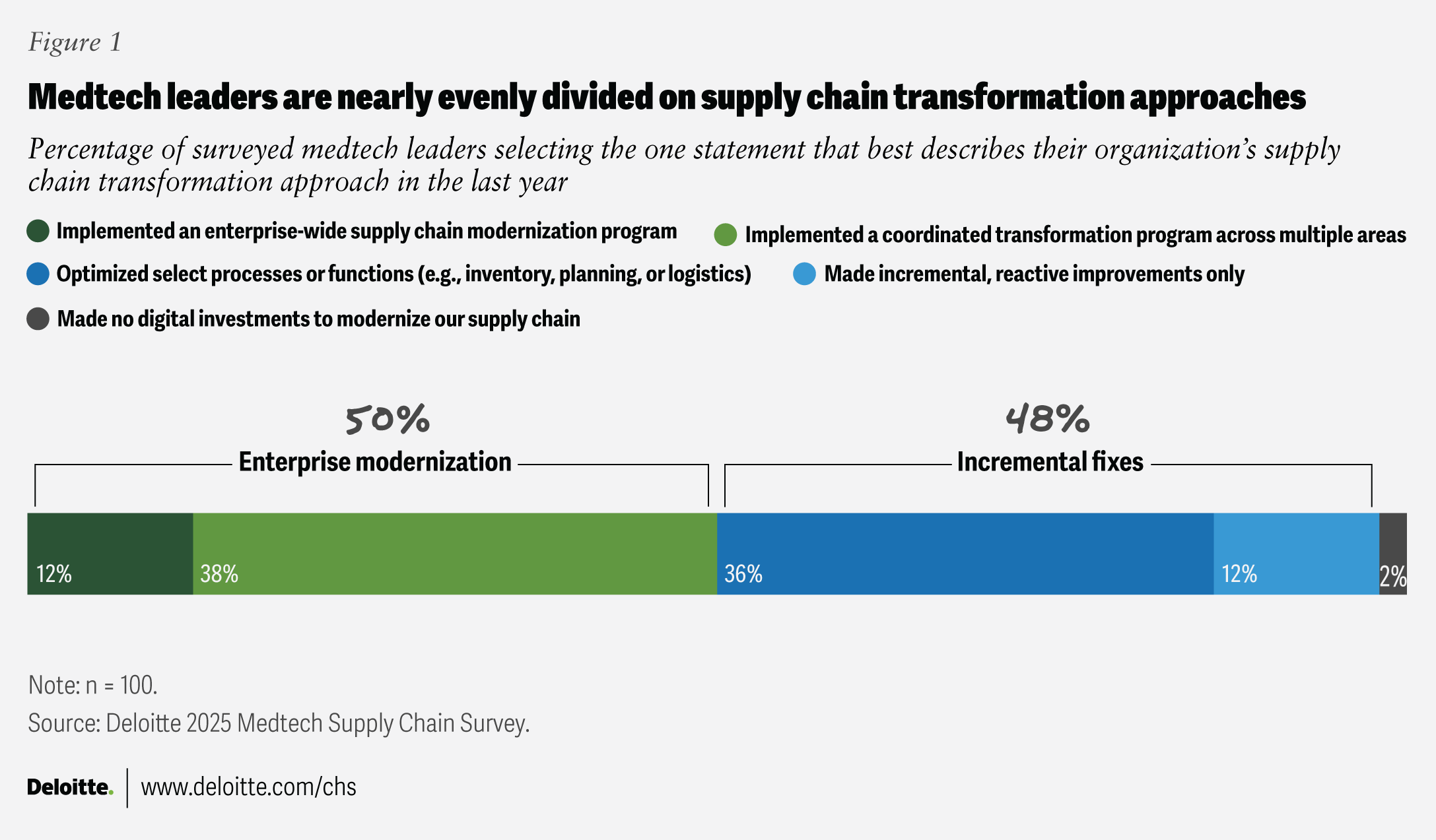

Of the medtech organizations we surveyed, those with digitally enabled supply chains were 38 percentage points more likely to deliver stronger margin improvement. That advantage appears to come from having connected data, decision-ready visibility, and the ability to model and execute trade-offs in near real time, especially when information is incomplete and the stakes are high. The findings also highlight a divide: Fast-recovery organizations are advancing operationally and financially, while 48% of the industry is strengthening individual processes without redesigning how enterprise decisions get made under pressure.

That gap is widening amid persistent device shortages and continuity risk; ongoing component constraints; and regulatory changes rewriting assumptions on cost, sourcing, and market access.1 Medtech supply chain leaders can add value by coordinating end-to-end decisions in real time, and aligning demand, supply, quality, and logistics to anticipate bottlenecks early and keep patient-critical products moving safely and on schedule.

The transformation gap: Why traditional resiliency measures may no longer be enough

Medtech supply chains are operating in near-constant disruption as trade policy, tariffs, and regulatory expectations shift. We define the transformation gap as the point where resilience capabilities improve, but decision-making doesn’t keep pace—so recovery stays slow and costly.

Two-thirds of the executives surveyed report moderate (54%) to significant impact (12%) from recent economic and policy changes. At the time of our interviews taking place in late 2025, industry leaders described tariffs as a “moving target,” requiring frequent scenario analysis rather than stable long-term planning.2 One global deliver leader at a large medtech company we interviewed explains, “We look at what the current tariffs in effect are and the tariffs that could come, and we do a financial analysis every week. To help strip the noise, we socialize a simple view of what changed, our current exposure, and what each scenario could mean for the business.” Since those interviews, legal and policy developments have brought greater clarity to certain tariff authorities, though trade policy remains an ongoing consideration.3

Medical device shortages tend to further heighten the stakes. When supply disruptions occur, providers may delay procedures or substitute products, affecting patient access and care continuity.4 For manufacturers, these disruptions can trigger allocation decisions, production replanning, and regulatory reporting obligations, making recovery speed important for restoring supply.

Given this policy environment, tariffs are increasingly as much a tax and trade issue as a sourcing issue. Tariffs and customs duties should be viewed as a first-order cost driver in disruption planning as they can affect landed cost. An advantage can go to teams that can translate changing assumptions into scenario models quickly, comparing margin, service, and compliance trade-offs within the same decision cycle.

Against this backdrop, 48% of surveyed medtech organizations remain in what we call “incremental mode.” They strengthen individual processes but do not redesign how enterprise decisions are coordinated across the supply chain. Many of the surveyed organizations rely on resilience moves, including stronger supplier monitoring (64%), higher inventory buffers (59%), and improved visibility and traceability (56%). These actions matter: They can help absorb shocks and stabilize operations in the short term.

However, when disruption hits, siloed initiatives and unclear decision rights can slow the response. Trade-offs across cost, service, and compliance tend to be negotiated repeatedly rather than resolved systematically. Visibility alone does not necessarily accelerate recovery. Supply chain teams also can use decision-ready data, clear governance, and digital tools that allow them to model trade-offs and act quickly.

By contrast, 50% of respondents say they’re modernizing through coordinated, enterprise-wide programs that span multiple supply chain areas. These approaches recognize that disruption rarely remains isolated: Supplier constraints can quickly cascade into production adjustments, logistics disruptions, and customer delivery risks. The fastest recoveries come from solving the supply chain as an integrated system rather than function by function (figure 1).

The survey also reveals potential blind spots. Only 17% of respondents cite cybersecurity readiness as a supply chain priority while 15% cite regulatory readiness, even as medtech supply chains become more digitally connected and compliance demands grow.5 While 8 in 10 organizations use operational data for scenario planning, only about half incorporate external risk signals such as regulatory alerts, supplier financial distress indicators, or geopolitical developments. Without early warning, response often begins after disruption has escalated.

Recovery speed is a key differentiator that converts operational capabilities into enterprise performance

When asked how quickly their organization can recover from disruptions such as supplier shutdowns or logistics bottlenecks, only 27% of surveyed executives say their organizations can recover within two to four weeks. For most, recovery takes several months (figure 2).

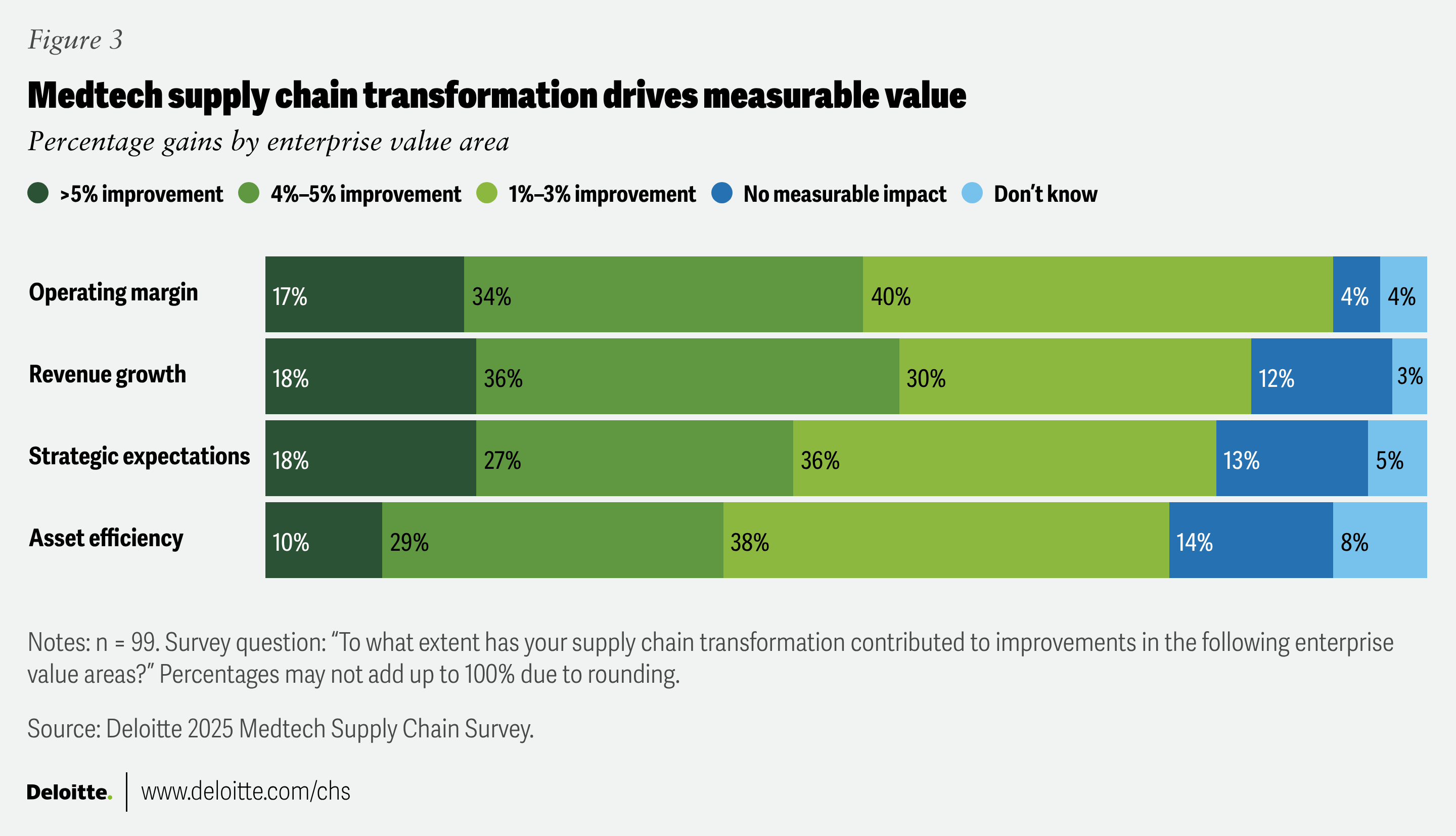

Supply chain transformation can be a meaningful enterprise value lever, but the upside is not evenly distributed. In our survey, organizations that pair transformation with strong, digitally enabled recovery report that they are far more likely to convert capability into measurable results.

Organizations with digitally enabled recovery capabilities are about three times more likely to report at least 4% operating-margin improvement than those relying on ad hoc recovery (60% versus 22%) and are nearly twice as likely to report at least 4% revenue growth. A separate industry analysis indicates that medtech companies typically spend roughly 3% to 5% of revenue on supply chain services. And with total supply chain costs reaching up to 20% of revenue, this underscores how supply chain performance can materially influence margins.6

This relationship suggests that recovery speed can influence financial performance as organizations stabilize operations and avoid disruption-related costs. Teams that regain control faster can stabilize operations, avoid costly expediting and premium freight, reduce scrap and write-offs, and manage working capital more deliberately—directly helping absorb margin pressure.7

Fast recovery tends to reflect the ability to make enterprise trade-offs deliberately, using better visibility, scenarios, and decision rights to protect continuity and patient access, even when it creates short-term margin pressure. An alternative is reactive choices that may feel safe in the moment, such as expediting orders, over-ordering, or pausing critical investments, but these can distort inventory and costs for quarters after the disruption passes. In medtech, faster stabilization can also limit downstream regulatory exposure and reporting risk when disruptions escalate into medical device shortages.8 Digitally enabled recovery can turn disruption into an advantage by helping companies stabilize faster and limit financial fallout.

Survey results also suggest that supply chain transformation contributes to measurable improvements across several enterprise value areas (figure 3).

What fast-recovery organizations do differently

1. Coordinated, cross-functional transformation

Coordinated transformation is a key differentiator for organizations that recover as an enterprise versus those that recover in silos. Among respondents, fast-recovery organizations are more likely to transform across multiple supply chain areas rather than run isolated projects: Coordinated transformation is reported by about 60% of fast-recovery organizations, compared with 35% of moderate-recovery and 20% of slow-recovery organizations.

That difference is structural. Disruptions such as supplier failures, quality events, or cyber incidents can quickly cascade into allocation decisions, production replans, logistics constraints, and customer commitments. Coordinated transformation can help to reduce “handoff lag” by aligning priorities, decision rights, and data flows end-to-end. An advantage is that leaders can make systemwide trade-offs, rather than optimizing one function at the expense of another.

2. Digitally enabled recovery capabilities

Digital enablement is emerging as a separator between organizations that regain control quickly and those that rely on improvisation. While about half of executives say they use digitally enabled capabilities to guide recovery, 48% still depend on basic tools and ad hoc approaches, which can limit how fast they can sense change, test response options, and act with confidence.

The divide is sharper among performance leaders. Our survey revealed that 74% of fast-recovery organizations use advanced digital tools for scenario modeling and simulation. By contrast, slower performers remain largely spreadsheet-driven: 68% of slow-recovery and 56% of moderate-recovery organizations still rely on manual forecasts and reactive coordination.

Fast recovery is possible when teams compress the decision cycle from signal to choice to execution. As Peter Smith, vice president for global supply chain at Terumo Blood and Cell Technologies, puts it, “AI’s value is noise cancellation. You’ve got all these thousands of transactions going on in the world, but which are the critical few that my team needs to act on today? That’s what makes AI interesting for supply chain.”

3. Digital maturity (the foundation beneath recovery speed)

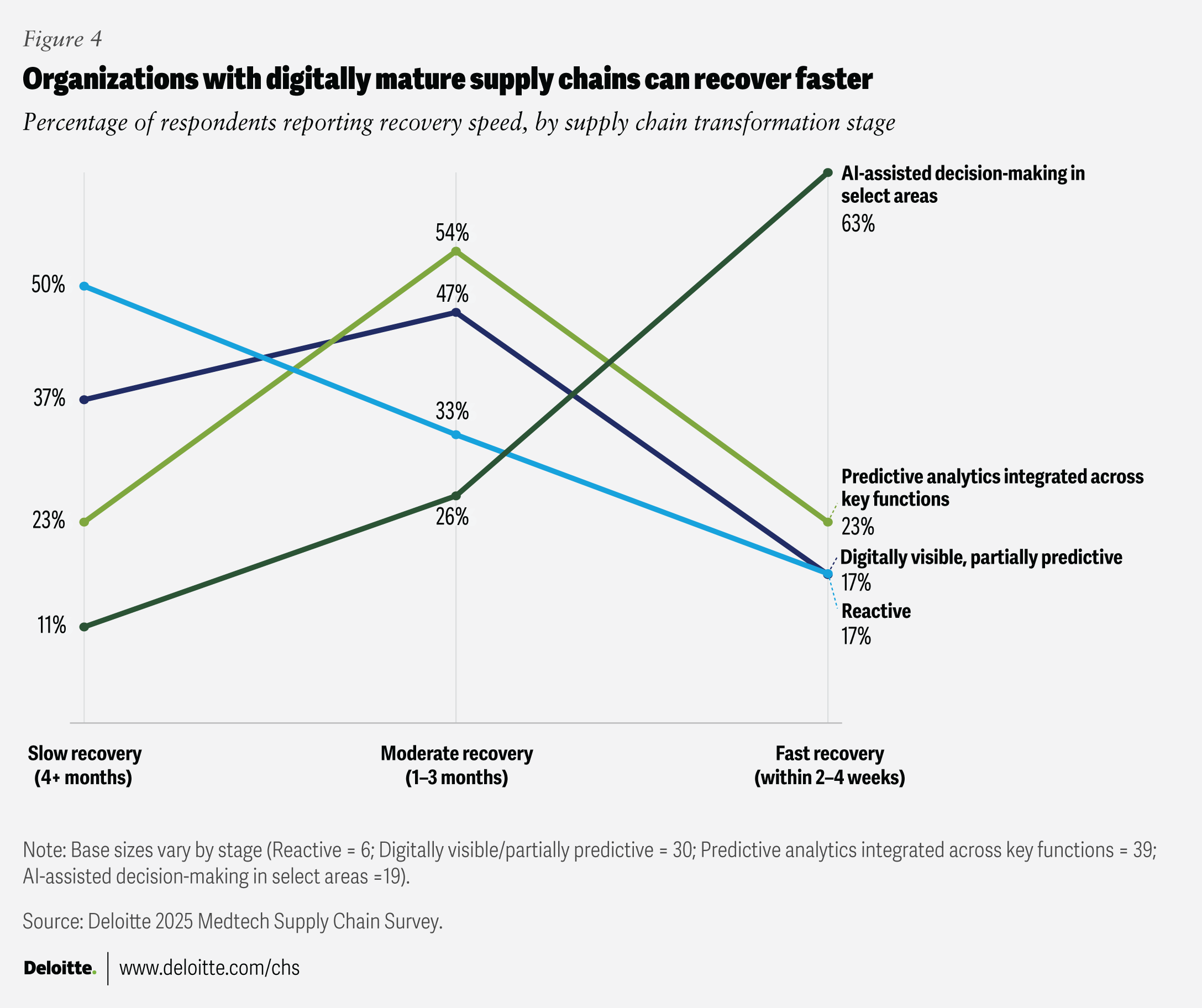

Digital maturity tends to correlate with recovery speed because it changes how reliably organizations can move from signal to decision to execution under pressure. Our findings show that as organizations progress from reactive approaches to integrated predictive analytics and artificial intelligence-assisted decision-making, the share of organizations reporting fast recovery rises, while reactive organizations skew toward slower recovery timelines.

The contrast is especially visible at the extremes, as 63% of organizations using AI-assisted decision-making report fast recovery, while 50% of reactive organizations report recovery timelines of four to six months or longer (figure 4). A key is having decision-ready data and integrated processes that allow insights to translate into coordinated action. Without that foundation, analytics can surface more exceptions without speeding the response; with it, teams can replan faster, prioritize better, and execute changes consistently across functions.

4. Formalized governance and clear decision rights

Formal governance with clear decision rights and escalation paths is a keystone that allows the other capabilities to operate at speed, especially under disruption. Yet only 43% of respondents surveyed report their organizations have this level of governance in place. Within this segment of respondents, performance and enablement concentrate: 42% qualify as fast-recovery organizations, and 74% rely on digitally enabled recovery capabilities. By contrast, none of the organizations operating with ad hoc governance report fast recovery.

There is a leadership implication to consider: Recovery performance is a governance outcome as well as an operational outcome. Boards and executive teams should treat disruption readiness as an enterprise risk priority by strengthening oversight of critical external partnerships, clarifying who decides what in a crisis, and focusing governance on the high-impact events that can cost organizations hundreds of millions when decision-making is slow or unclear.9

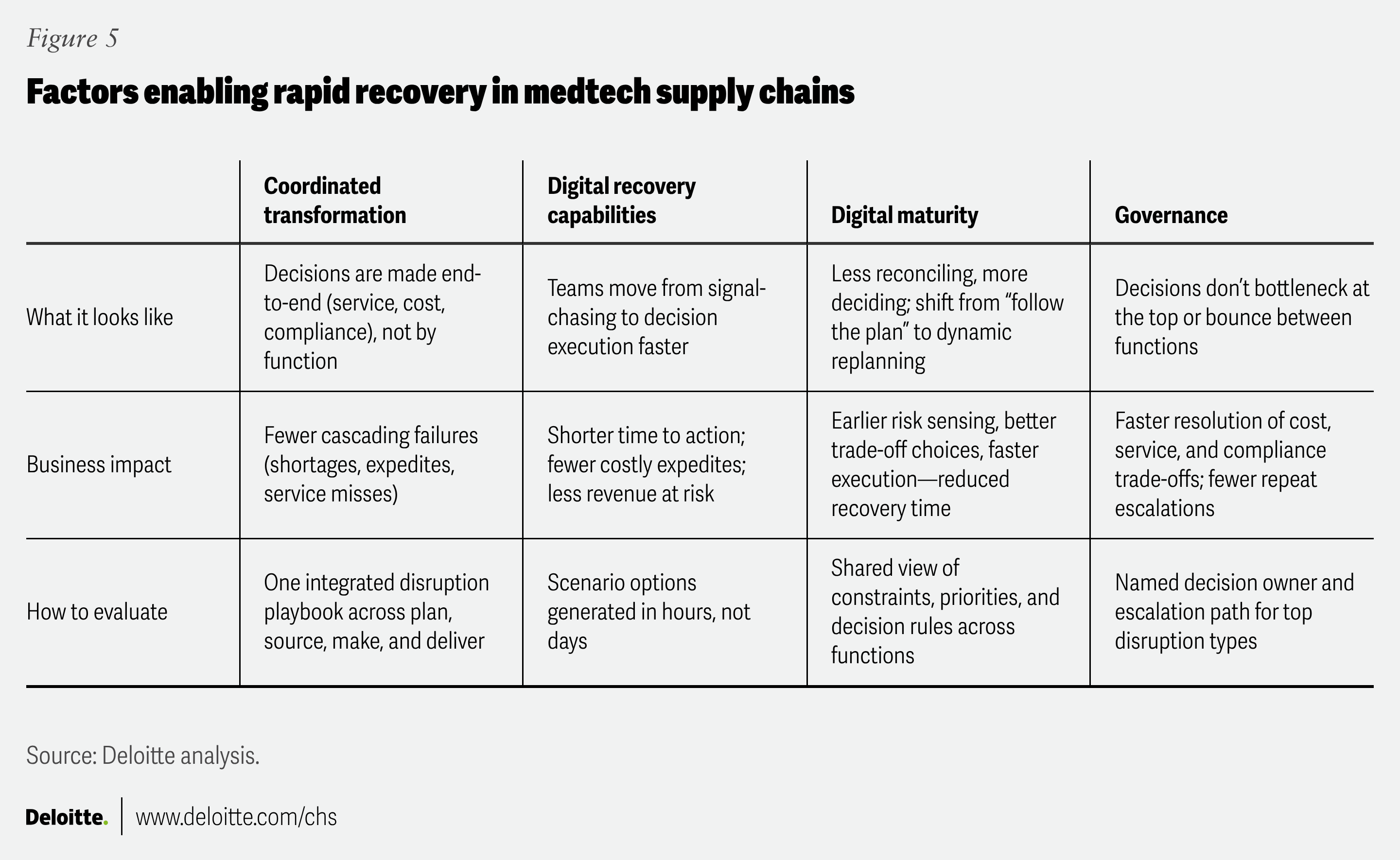

Together, these capabilities represent core signals of a fast-recovery supply chain (figure 5). Take our three-minute self-assessment to see where your organization is strong and where it may be exposed during disruption (see “Are you a smart navigator?”).

Are you a smart navigator?

Use this quick self-assessment to gauge how “disruption-ready” your organization’s supply chain is.

How to use it

Score each statement 1 = true today, 0 = not consistently true. Score “1” only if it’s in place for most critical products and has been used in the last 12 months. Total points (0 to 8).

Sensor network coverage (sense earlier)

- We have visibility (within 24 hours) across key suppliers, manufacturing, and distribution for critical products.

- We receive automated risk alerts (for example, supplier, logistics, and regulatory risks) with clear owners.

Command center enablement (decide faster)

- We operate a cross-functional disruption “command center” with a defined cadence when disruption occurs.

- Decision rights, thresholds, and escalation paths are preset (for example, allocation, supplier switching, expedited spending).

Real-time rerouting (respond faster)

- We can shift suppliers, routes, or sites within hours or days for our most critical products (with quality and regulatory considerations built in).

- Digital tools and platforms suggest or automate rerouting options, rather than relying solely on manual decision-making.

Investment in predictive intelligence (learn continuously)

- We have dedicated funding (at least 15% of our supply chain technology budget) for analytics, automation, or AI/machine learning (not just core systems and maintenance).

- We run scenario simulations or stress tests at least quarterly to assess the impact of environmental changes (for example, regulatory shifts, supplier failure, cyber incidents, etc.).

Scoring

- Smart navigator (6 to 8): Your supply chain is relatively advanced in sensing, deciding, and responding. Focus on fine-tuning and scaling what already works.

- In motion (3 to 5): Your supply chain has important building blocks in place, but gaps in either governance, data integration, or predictive intelligence still limit recovery speed.

- At risk (0 to 2): Disruptions are likely to be managed reactively. Priority should be given to building basic visibility, decision infrastructure, and predictive capabilities.

What good can look like: From improvement mode to connected modernization

With leaders split between enterprise modernization and incremental fixes, “good” can be seen as modernizing in a connected way that improves time to recover—not just adding point solutions. Day-to-day variability can be constant; resilient supply chains tend to absorb it through disciplined governance and decision processes. When disruptions occur, leading medtech organizations can scale the same operating model with higher cadence, broader visibility, and tighter cross-functional coordination. Our analysis points to a connected modernization10 blueprint to consider.

1. Start with governance and decision rights

Governance is the backbone of recovery. Organizations should:

- Define decision rights and thresholds for common disruption scenarios, including who decides, when, and based on which triggers

- Establish a cross-functional command center that can activate quickly with a clear decision cadence and escalation path

- Standardize playbooks for high-probability situations such as regulatory inquiries, cyber incidents, and critical supplier failures

2. Integrate data around the decisions that matter

All organizations have data, but fewer have decision-ready data. Leading practices include:

- Connect internal operational data (inventory, capacity, lead times, and quality) with external signals (regulatory alerts, supplier financial risk, trade flows, or geopolitical indicators)

- Create a unified visibility layer for a small set of disruption key performance indicators, including time-to-recover and time-to-survive indicators

- Strengthen data governance and master data management so definitions, hierarchies, and critical master data keep pace with decision speed

3. Build digitally enabled recovery capabilities, not just dashboards

Visibility is necessary, but recovery requires decision-making and execution. Fast-recovery organizations typically:

- Model scenarios and trade-offs to choose responses quickly, not just to report status

- Embed “what if” capabilities into planning, sourcing, and logistics tools to empower teams to act within their daily workflows

- Automate alerts and recommended actions for common disruption triggers, with clear ownership for exceptions

The objective is to move from seeing the disruption to rehearsing and executing responses.

4. Move AI from pilots to scaled, decision-linked use

With pilots widespread and scaled use rare, an opportunity is to tie AI to measurable recovery outcomes. Practical moves include:

- Prioritizing use cases that reduce time to recover such as disruption ETA prediction, dynamic safety stock, or supplier anomaly detection

- Integrating AI outputs into formal governance mechanisms through exception-based approvals, automated triage, and human-in-the-loop controls

- Measuring impact on recovery speed and profit and loss to justify scaling and sustain adoption

5. Elevate cyber and regulatory readiness as core supply chain capabilities

Cyber and regulatory risks are embedded in the supply chain through OT/IoT exposure, compromised integrity of quality data, supplier compliance failures, and logistics partner posture. Survey findings also indicate that many medtech organizations still:

- Only assess cybersecurity posture annually or on an ad hoc basis

- Only review supplier contracts for cyber and data clauses annually or during contract renewal cycles

This can be a structural blind spot, especially as AI and connected devices expand the threat surface. Organizations should treat cyber and regulatory readiness as integral to supply chain design and follow continuous/real-time monitoring.

From insight to action: New considerations for medtech supply chain leaders

As we think about what’s actionable, one interviewee’s perspective is both thought-provoking and closely complements what our research suggests: Recovery speed should be built before the crisis hits. As one global deliver leader at a large medtech company explains, “Over time, crisis moments—back orders, allocation, supply constraints—encouraged us to mature our analytics to better support our customers. That’s how we created segmentation, allocation logic, and better visibility across our global network. The improvements were needed fast and under pressure, but they’re now part of our capability set.”

To help them set their organizations up for success, supply chain leaders should think about whether the supply chain is built to recover at the pace the market and patients demand. Leaders can ask themselves:

- How fast could we recover from the disruptions most likely to affect our business?

- Who has the authority to make critical trade-offs during the first hours of disruption?

- Do we have decision-ready visibility at the level required for medtech operations?

- Have we built the playbooks and rehearsed scenarios that reflect medtech realities?

Recovery speed is becoming a competitive capability in medtech supply chains. Organizations that sense risks earlier, make decisions faster, and coordinate responses across functions may be well positioned to maintain supply continuity and sustain performance during disruption. Achieving that capability can depend less on additional spending and more on building connected, digitally enabled supply chains that support faster sensing, decision-making, and execution.

Methodology

This article draws on a survey of 100 respondents across 15 countries. Respondents were based in the Americas (65 in the United States, one in Canada, and one in Brazil); EMEA (25 in Germany, Switzerland, Sweden, France, the United Kingdom, Denmark, Italy, the Netherlands, and Saudi Arabia); and Asia Pacific (eight in Australia, India, and Singapore). The research also incorporated in-depth interviews with two senior supply chain leaders from medtech organizations.

Survey measures and definitions

Several figures in the article use survey questions that assess 1) supply chain transformation maturity, 2) recovery speed after disruption, and 3) reported enterprise value outcomes.

Enterprise value outcomes (figure 3)

Respondents were asked how much supply chain transformation contributed to improvement in the following areas:

- Revenue growth: for example, faster recovery due to fewer stockouts, faster product launches, and improved customer service

- Operating margin: for example, lower inventory, logistics, and labor costs; improved production efficiency

- Asset efficiency: for example, improved working capital, plant and warehouse utilization, and inventory turnover

- Strategic expectations: for example, improved digital maturity, supply chain resilience, and regulatory compliance

Percentages shown represent respondents’ reported levels of improvement. Totals may not equal 100% due to rounding.

Supply chain transformation stages (figure 4)

To assess the relationship between digital maturity and recovery speed, respondents selected their organization’s current stage:

- Reactive: limited data integration and minimal digital visibility across supply chain functions

- Digitally visible or partially predictive: data integrated across some functions with early use of analytics to anticipate risks or demand changes

- Predictive analytics integrated across key functions: integrated data platforms supporting predictive analytics for activities such as forecasting, inventory planning, logistics optimization, and proactive risk management

- AI-assisted decision-making in select areas: advanced digital maturity combining integrated data platforms with AI applications that automate decisions in selected processes such as inventory replenishment or transport routing

Respondents also estimated how quickly their organization could recover from a supply chain disruption, enabling comparisons between transformation stage and recovery speed. Base sizes vary by transformation stage and are provided in the figure notes.

Continue the conversation

Meet the industry leaders

Dr. Laks Pernenkil

Luis Hakim

Dr. Jay Bhatt

by

Luis Hakim

Stephen Bradley

Alex Bredemus

Elizabeth Beck

Darshan Gosalia

Apoorva Singh

The authors would like to express their gratitude to those who contributed to this paper.

The authors thank Wendell Miranda, who served as an adviser on this project, helping drive our initial stakeholder discussions and survey design.

The authors are grateful to Rob Jacoby, Jay Bhatt, Laks Pernenkil, Russell Jones, Vijay Natarajan, and Ned Glattly for their subject matter expertise and review of survey tool and the draft. The authors would also like to thank Kevin Dougherty, Nicholas Anselmo and Kacie Boen for their input to the draft.

The authors wish to thank Rebecca Knutsen for her contributions to the editing and structuring of the paper. The authors extend their special thanks to Christina Giambrone for her strong marketing support and bringing novel ideas to life. Additionally, the authors would like to thank Julie Landmesser and Debra Pielack (Asay) and many others who contributed to this research.

Lastly, we would like to thank our interviewees for taking the time to share their invaluable perspectives with us.

Editorial (including production and copyediting): Rebecca Knutsen, Prodyut Borah, Shyamili M, Anu Augustine, and Cintia Cheong

Design: Harry Wedel and Meena Sonar

Cover image: Alexis Werbeck and Stephanie Lorig, Adobe Stock

Knowledge Services: Vanapalli Viswa Teja

Visit the Deloitte Center for Health Solutions

Access more insights for the hospital, health system and provider, pharmaceutical manufacturer, health plan and payer, medtech, and health tech organization sectors.