Meaningful private capital exposure to reach 1 in 6 US retail investor funds by 2030

Structural shifts across demand, competition, regulation, infrastructure, and partnerships are driving scalable adoption

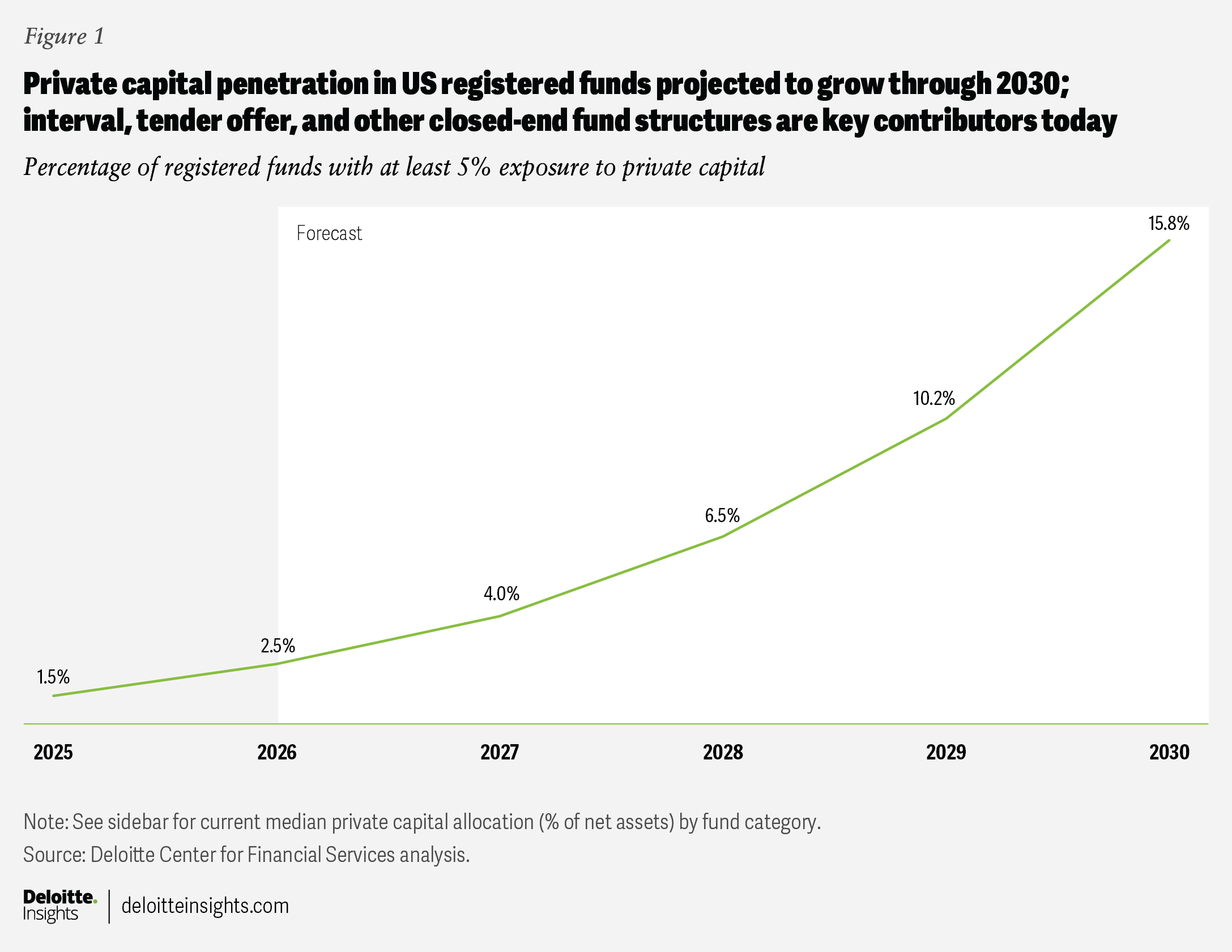

Retail investors’ access to private capital—including private equity and private credit—typically occurs through registered fund structures. However, as of year-end 2025, only about 1.5% of US-registered funds (excluding business development companies, small business investment companies, and money market funds) allocated 5% or more of their portfolios to private capital.1 The Deloitte Center for Financial Services predicts that the share of registered funds allocating 5% or more to private capital could increase to just under 16% by 2030 from today’s 1.5% (figure 1; see “About this prediction”).2

Closed-end funds are helping expand retail access to private capital

Of the funds that allocate 5% or more to private capital, more than three-quarters are closed-end fund structures such as interval funds and tender offer funds, which are operationally designed to accommodate private capital and manage investor liquidity demands.3 In fact, for interval, tender offer, and other closed-end funds that allocate at least 5% to private capital, the median allocation is nearly 38% of net asset value. A smaller number of mutual funds and exchange-traded funds (ETFs) also provide access to private capital, typically with more limited allocations.4 Fewer than 50 mutual funds and ETFs, out of more than 10,000 available, allocate 5% or more to private capital, and the median allocation among these funds is approximately 8% of NAV.5 Although business development companies are not captured in this analysis, they are also important structures for expanding retail access to private capital and are influenced by similar trends as other registered fund structures.

The above statistics suggest that retail access to private capital remains limited, with only modest integration into mainstream registered fund portfolios. However, continued favorable developments across several factors—including growing investor demand, competitive pressures, higher manager acceptance, innovations, evolving regulations, and expanded partnerships—will likely support broader retail adoption.

Factors driving greater retail private capital exposure

Higher adoption of private capital across registered funds will likely transition from initial participants, to forward-looking adopters, and finally to mainstream adoption by 2030. Several supportive tailwinds for this transition are explored below.

Increasing investor demand and rising industry comfort

Retail investors currently have less exposure to private capital investments than institutional investors, limiting the opportunity for optimized portfolio construction.6 At the same time, the correlation between equity and bond markets has increased in recent years, reducing the diversification benefits of the conventional 60/40 portfolio.7 Even modest allocations to private capital can have a measurable impact on returns. For example, replacing a portion of equity with a 5% to 10% allocation to private equity can increase portfolio returns by 15 to 30 basis points annually and reduce volatility by 39 to 81 basis points.8 As awareness and education about these benefits increase, the demand for private capital will likely rise.

Investor demand for private-market exposure remains heavily influenced by adviser-led distribution. In many cases, wealth channels are not simply responding to demand; they are helping create it. This trend is expected to persist, as many wealth managers signal intentions to further increase allocations to private capital in the near term.9 Another adviser survey also indicates that access to private capital strategies can strengthen client relationships by expanding the range of differentiated solutions advisers can offer.10 Given the importance of the advisory relationship, firms should partner with wealth management firms that equip advisers with integrated tools, real-time insights, and streamlined workflows to enable more personalized and high-value client interactions at scale.11

Gen X and millennial investors are both likely more familiar with private capital than previous generations.12 With a combined US$85 trillion wealth transfer to Gen X and millennials estimated through 2048, this generational shift is expected to drive an increase in private capital allocations as capital moves toward investors with greater comfort with these asset classes.13 These trends suggest that demand for private-market exposure through registered fund vehicles is likely to continue rising. As allocations to private capital as a percentage of portfolio tend to increase with investable wealth, firms should align distribution strategies with higher-touch channels such as registered investment advisers, banks, and full-service wirehouses for high-net-worth and ultra-high-net-worth clients.14 Broker-dealers and digital platforms, on the other hand, may be more effective at reaching mass-affluent and first-time private capital investors.

More private capital in retail-focused funds may offer help to an industry facing margin pressures and fundraising challenges. Such strategies can command higher management fees and attract new investors. These factors could gradually increase adviser acceptance of private capital within registered portfolios, while reducing fund managers’ hesitancy about deviating from traditional allocations.

Evolving regulation and infrastructure

Investor demand alone is not enough to drive meaningful adoption in the absence of clear guidance and well-defined rules, as firms may remain cautious about launching products in this space. Following the global financial crisis, private funds were brought under greater oversight through reforms such as the Dodd-Frank Act and Form PF, which are meant to enhance reporting and monitoring of systemic risk. In recent years, the regulatory focus has shifted toward expanding access to private capital for a broader set of investors. This includes measures such as widening the definition of accredited investors, increasing flexibility in closed-end fund structures, and exploring the inclusion of private assets in 401(k) plans. While regulators continue to emphasize transparency and investor protection, the overall direction appears to be toward greater accessibility and standardization for retail investors.

The infrastructure required to launch and manage products with exposure to private capital is also evolving. For example, if a small firm wants to quickly test a strategy combining ETF structures and private equity exposure, it can do so through ETF-as-a-service platforms without building complex operational and regulatory infrastructure in-house.15 These turnkey platforms can level the playing field between small and large firms in ETF product development efforts. The ETFs can support liquidity by partnering with other private capital managers that specialize in originating and managing such investments.16 They can also enhance valuation processes by engaging third-party valuation specialists, leveraging data management systems, incorporating increasingly available alternative data, and taking advantage of advances in AI.17 Performance can be assessed against blended benchmarks that incorporate both public and private market exposures.18 These technological advancements and product innovations will likely act as a strong enabler for the launch and scaling of private capital through registered funds.

Partnership emerging as a scale mechanism

When firms sought to enter a new segment in the past, they typically built capabilities in-house or acquired them through mergers and acquisitions. Today, many firms are turning to strategic partnerships as a preferred entry strategy. About 17% of funds that allocate at least 5% to private capital are engaged in partnerships.19 Partnerships allow companies to test new markets by leveraging the complementary strengths of both parties, without committing to the significant capital investment, time, and operational complexity required to build infrastructure independently.

Firms pursue partnerships for three main strategic reasons: expanding distribution, strengthening deal origination, and enhancing product structure. On the distribution side, firms are increasingly partnering with wealth technology and managed-account platforms to deliver private capital strategies through adviser-facing investment systems, expanding access to a wider pool of investors.20 They also partner with other firms to distribute products through advisory channels, as well as with retirement plan record keepers to embed products within retirement offerings.21 In addition, partnerships between traditional managers and alternative managers may raise confidence levels on the part of retail investors, helping increase participation in private capital.

For deal origination, firms work with banks and other financial institutions to build and scale investment pipelines for new products.22 These partnerships provide access to differentiated deal flow, enhance sourcing capabilities, and accelerate capital deployment. Firms also work with banks to distribute these private capital products through their wealth channels.

In terms of structuring and product innovation, firms partner to improve liquidity features—such as enabling private capital to be included within ETF structures—and to work with index providers to create appropriate benchmarks for private capital strategies.23 Many firms also codevelop products to combine complementary expertise. In certain structures, one partner may assume primary responsibility for managing and distributing the vehicle, while allocating a significant portion of assets to the other partner’s strategies. This framework can align economic exposure among the partners while also helping address technical and operational considerations.

The direction of travel for private capital adoption is increasingly clear, supported by forces across demand, competition, regulation, innovation, and partnerships. As these dynamics play out, retail investors are set to gain greater access to opportunities that were once the exclusive domain of institutional capital.

Understanding a new set of challenges

Retail access to private capital can introduce a new set of challenges that firms entering this space should consider. Recent increases in redemption requests among private credit managers illustrate how such risks can emerge.

Elevated redemption requests and gating do not by themselves signify failure; they are pre-agreed mechanisms to handle liquidity, as discussed in our recent paper on semi-liquid funds. Strengthening liquidity frameworks and robust valuation practices may help bring greater clarity and ease investor concerns. Moreover, retail investors may not fully understand the risks associated with private capital exposure, as these assets have not been tested under sustained stress conditions. To build long-term investor trust, firms should consider prioritizing educating investors and advisers about the diversification benefits, return characteristics, and risks attached to private capital, including its long-term investment horizon, limited liquidity, and relatively lower transparency. Leading firms will likely establish reasonable, well-documented processes to ensure investor eligibility and suitability. Investor awareness and clear, prominent disclosures will be critical to mitigating reputational, regulatory, and litigation risks—especially as private capital products expand into retirement plans.

The regulatory framework governing this space remains in flux and is likely to continue evolving over the coming years. In this environment, firms should adopt a prudent approach when designing and implementing compliance processes.

Private capital becomes a structural retail allocation only if innovation is matched with governance rigor

Firms should consider focusing on a set of no-regret actions as they expand into private capital. They should consider evaluating fund structures—such as ETFs, mutual funds, interval funds, tender offer funds, business development companies, and real estate investment trusts—and review asset categories, including private equity, private credit, real estate, real assets, and infrastructure. They should consider adding those that align with the fund’s objectives, liquidity profile, and available infrastructure. Firms should also identify the appropriate distribution channels—such as wealth platforms, registered investment advisers, broker-dealers, and retirement plans—to ensure products reach investors with the required level of education and awareness. As such, many firms may need to update their operating models to support liquidity management, transparency, valuation frequency, investor reporting, regulatory compliance, and partner relationships.

When firms launch products in response to investor demand without adequately addressing governance considerations, they risk creating challenges that can build over time. These issues may emerge in the form of liquidity mismatches, erosion of investor trust, litigation risks, compliance gaps, and potential conflicts of interest. At the same time, firms that build strategic partnerships and proactively strengthen their operating and risk management practices will likely be better positioned to benefit from rising investor demand and supportive regulatory developments.

About this prediction

To estimate how many US-registered funds (including closed-end funds, tender offer funds, interval funds, mutual funds, and ETFs) had exposure to private capital at year-end 2025, we analyzed the most recent N-PORT filings, which disclose portfolio holdings of registered investment management companies. Business development companies not subject to N-PORT reporting were excluded.

We define a fund as having meaningful private capital exposure if at least 5% of its portfolio is allocated to private assets. Assets classified as fair value level 3 in N-PORT filings are treated as a proxy for illiquid private capital exposures, as these assets are typically valued using unobservable inputs and lack active secondary markets, aligning closely with the characteristics of private investments. This threshold is intended to distinguish strategic allocation from incidental or de minimis holdings. As of 2025, approximately 1.5% of registered funds meet or exceed this level.

To project adoption through 2030, we apply a diffusion-based framework (the S-curve, the cumulative version of the bell curve) that assumes a long-run adoption ceiling of 90% of registered funds. Adoption is modeled using a composite maturity index constructed from five factors: regulatory development, investor demand, manager acceptance, product innovation, and technology enablement. These factors are weighted in descending order to reflect their sequential importance—regulatory clarity enables demand; demand supports allocation decisions; and product and technology advancements accelerate adoption once foundational conditions are established.

Under this framework, we estimate that 16% of registered funds will allocate at least 5% to private capital by 2030.

By

Eric Fox

Amanda Nelson

Doug Dannemiller

Mohak Bhuta

The authors wish to thank the following Deloitte professionals for their insights and contributions: Patricia Danielecki, Sean Collins, Neerav Shah, Sumant Maharaj, Paul Kraft, Diana Torres, Jeff Stakel, John Labate, and Karen Edelman.

Editorial: John Labate, Hannah Bachman, Karen Edelman, Cintia Cheong, Stacy Wagner-Kinnear, and Anu Augustine

Design: Sofia Laviano, Sylvia Chang, and Guido Agüero Gonzalez

Audience development: Maria Martin Cirujano and Kelly Cherry

Cover artist: Sofia Laviano

Knowledge services: Agni Wagh

Visit the Deloitte Center for Financial Services

Access more insights for the banking & capital markets, commercial real estate, insurance, and investment management sectors.