How regional banks could help drive the next wave of partnerships with private credit

Deloitte analysis shines a light on the ways partnership strategies can benefit regional banks’ balance sheets and expand the reach of private credit

Partnerships between regional banks and private credit firms should continue to grow as both sides seek the benefits of cooperation: banks can expand their service offerings while reducing balance sheet exposure, and private credit firms can secure lending opportunities. The Deloitte Center for Financial Services has been monitoring this trend to understand the structure and impact of these partnerships. Such partnerships could benefit both industries, as well as non–sponsor-backed companies that have not traditionally been private credit borrowers.

The dynamic between banks and private credit firms is often characterized as one of competition versus cooperation. Our August 2024 report on how banks are adapting to private credit discussed some of the forces driving these trends and their impact.1 One example is the need for banks to retain capital when making loans, a regulatory requirement. This article will focus more closely on the cooperative strategy to form origination partnerships, one of the seven strategies discussed in the prior report.

The continued growth of private credit could encourage some banks to focus on arranging deals rather than financing them, especially as bank lending remains tepid. US commercial bank loan growth was 2.7% in 2024, slightly higher than in 2023.2 This happened during a period of falling interest rates, slowing inflation, and greater expectations of deregulation. As reported, prior periods in such a positive economic environment would normally have led to higher loan growth. Yet, commercial and industrial (C&I) loan growth was only 1% from 2023 to 2024.3 A longer-term strategy change can be seen as larger banks expand their fee-income businesses by arranging borrowing for clients. For example, Goldman Sachs Group Inc. created the Capital Solutions Group to bring together teams focused on alternative sources of financing, including private credit, to increase the number of services for clients.4

To private credit firms, partnerships with banks may provide a strategic advantage in sourcing deals. A PitchBook LCD survey released in the first quarter of 2025 found that “sourcing assets is considered the greatest challenge for many market participants.”5 Furthermore, the continued growth of private credit and accumulation of dry powder, that is, uninvested commitments from limited partners, have led to more competition among private credit firms, resulting in reduced spreads for loans.6 Regional banks may be well positioned to create opportunities for private credit firms by providing access to relationships with midmarket companies that are too small for public markets and do not already have relationships with the largest banks.

table of contents

- Emerging trends show more categories for partnerships

- What could the future look like for partnerships?

- How regional banks can prepare for partnerships

Emerging trends show more categories for partnerships

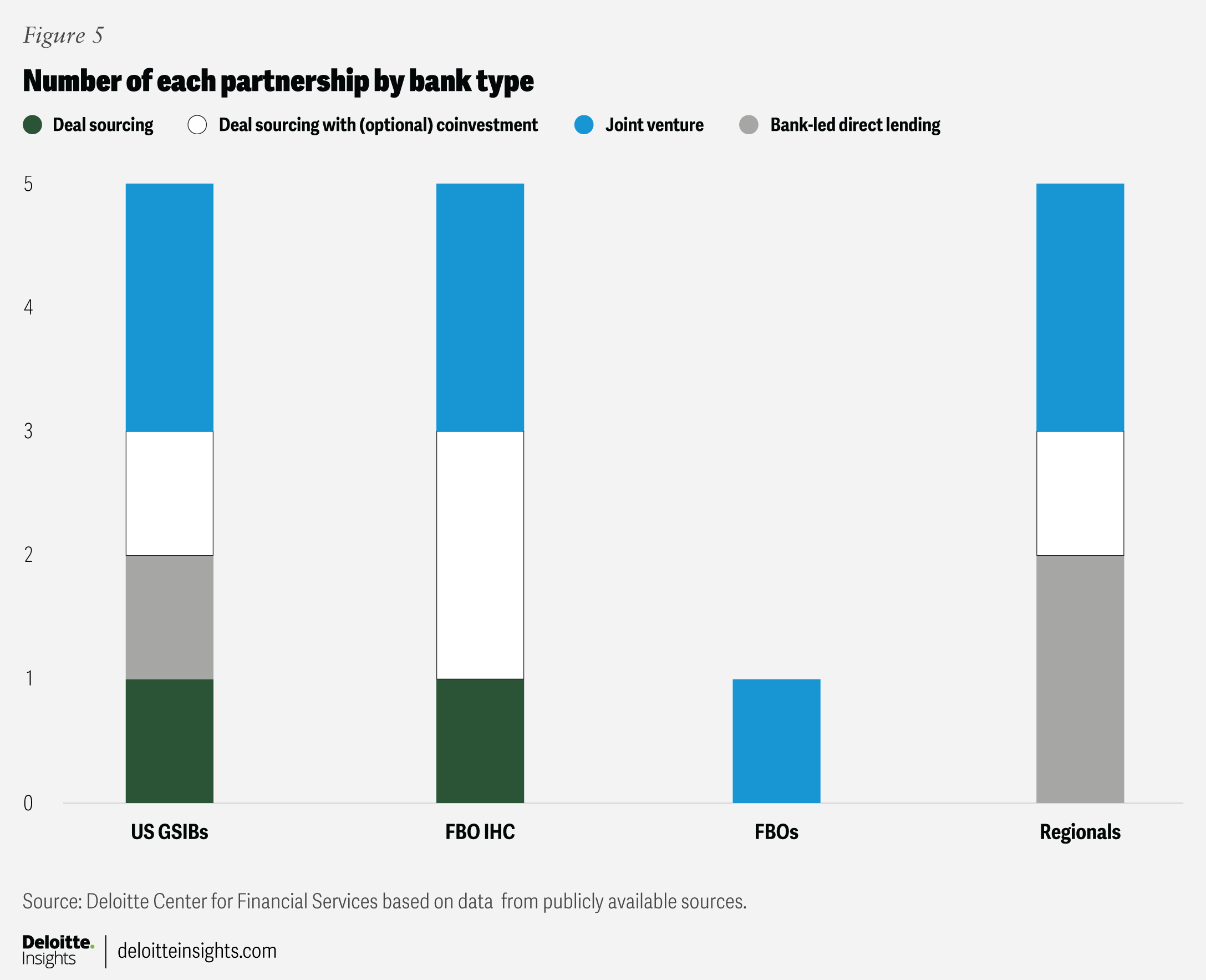

Our market analysis of the 50 largest banks in the United States found 16 partnerships between banks and private credit firms where investments have a predominant US focus.7 Our research categorized these partnerships into four types: deal sourcing, deal sourcing with (optional) coinvestment, joint venture, and bank-led direct lending.

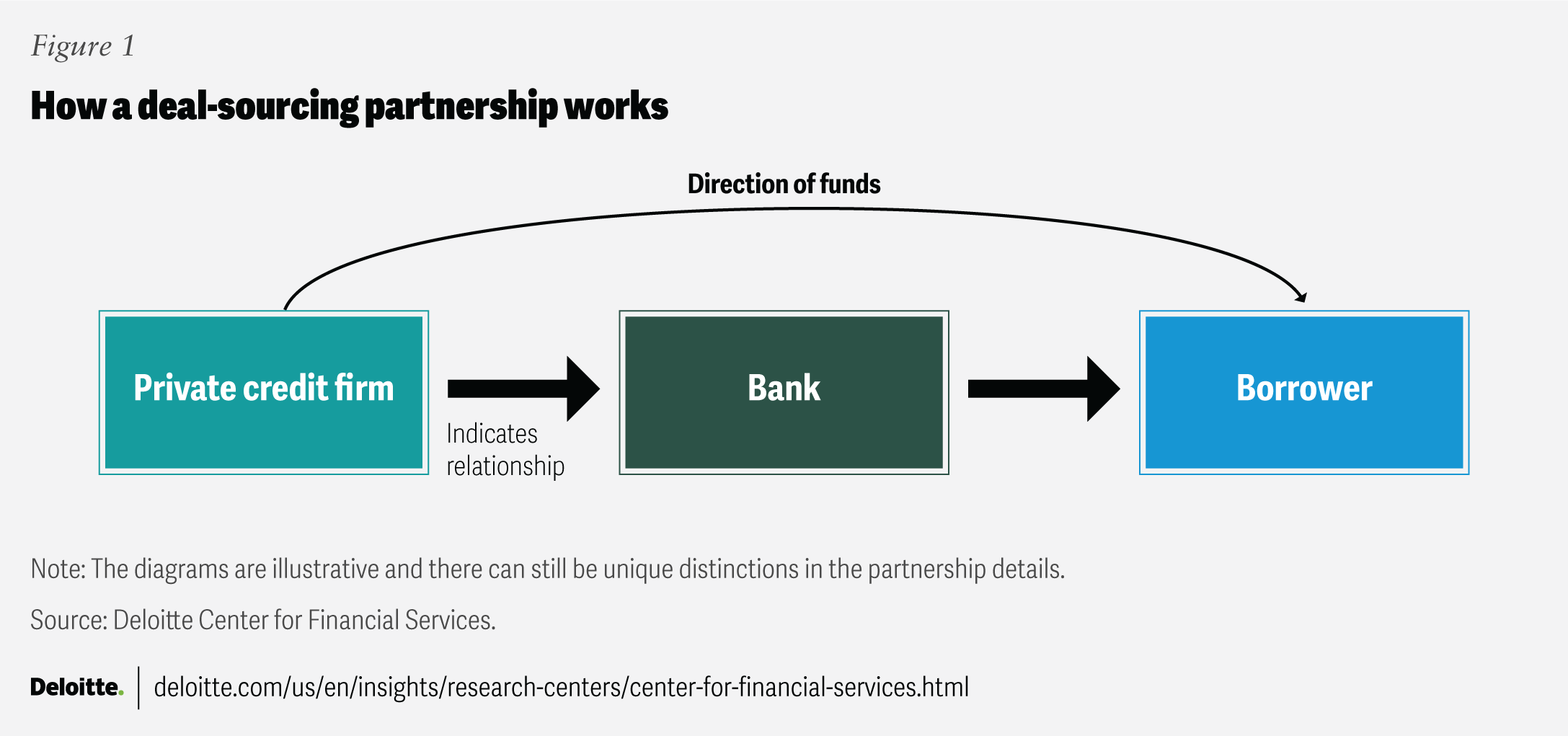

Deal sourcing

An important characteristic of a deal-sourcing partnership is that the bank does not use its funds but acts as an intermediary between a private credit firm and a borrower. This arrangement creates a pipeline from the private credit firm to the borrower, with the bank acting as an intermediary (figure 1). The bank can benefit from the arrangement as it generates fee income from structuring the deal and maintains the relationship with the borrower. These arrangements are likely to include predetermined criteria that the private credit fund is looking for in an investment, such as loan size and industry.

Citigroup Inc.’s partnership with Apollo is an example of a deal-sourcing strategy. Citi will open its large number of client relationships to Apollo’s capital base. As a result, Citi can earn fee income and offer more services to clients without holding the debt on its balance sheet. This can allow Citi to avoid an increase in risk-weighted assets.8

{kind=link}

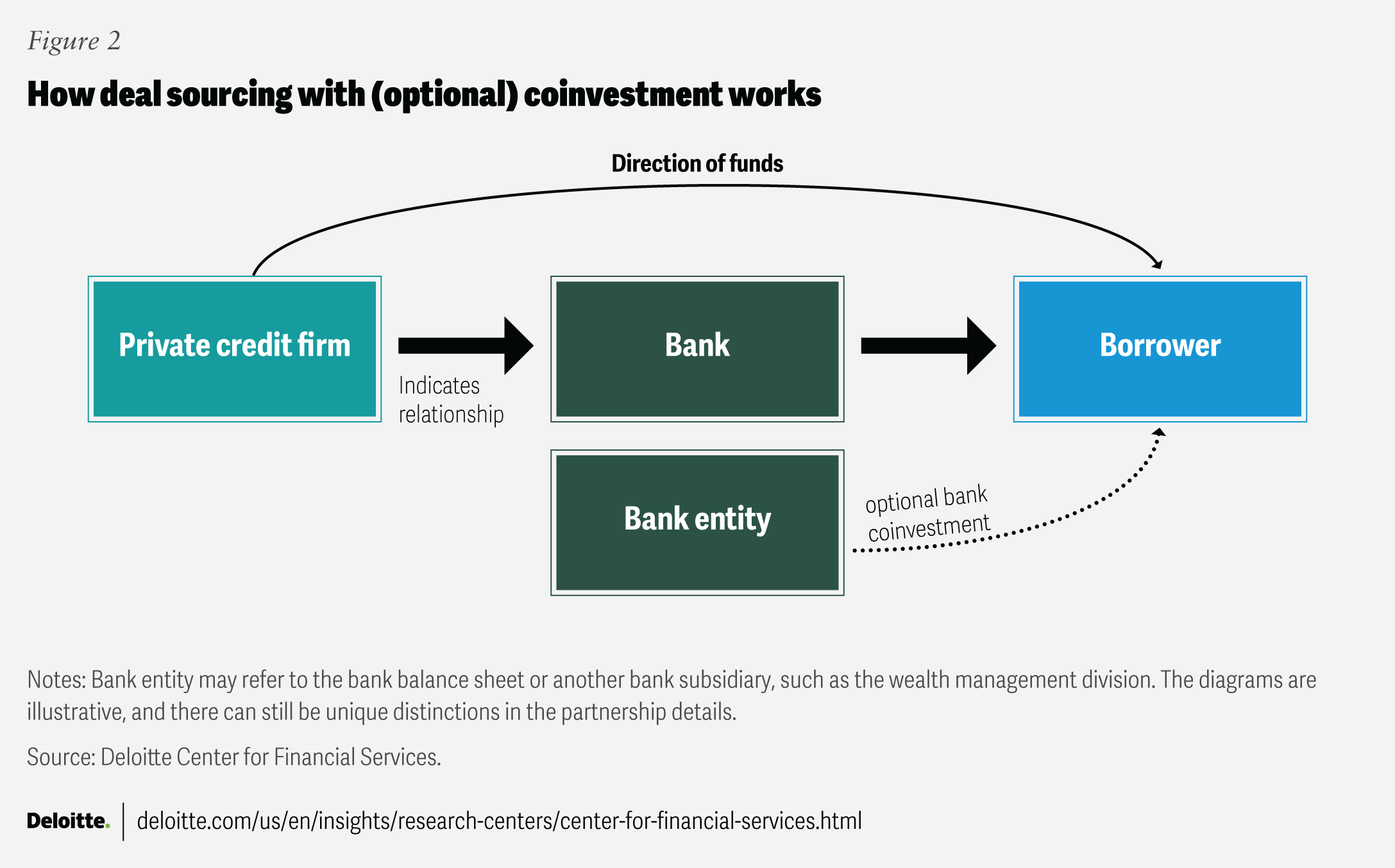

Deal sourcing with (optional) coinvestment

There are also several instances where banks have deal sourcing arrangements with an option to coinvest alongside the private credit firm (figure 2). In such cases, a bank can make the loans using its balance sheet or another bank entity, such as its wealth management division.

This type of deal sourcing with an optional coinvestment may have additional balance sheet implications for the bank. For example, if the bank is using its balance sheet to make a loan alongside the private credit firm, it may need to retain capital, just as it would when making other loans. Furthermore, the lending could be tranched so that the bank owns the senior portion of the loan, which may receive more favorable capital terms. Given the bank’s role in sourcing the deal, it could include a provision about keeping the senior portion in the partnership agreement.

An example of this coinvestment partnership is KeyCorp’s forward flow agreement with Blackstone Inc. The partnership supports Key’s Specialty Finance Lending group.9

{kind=link}

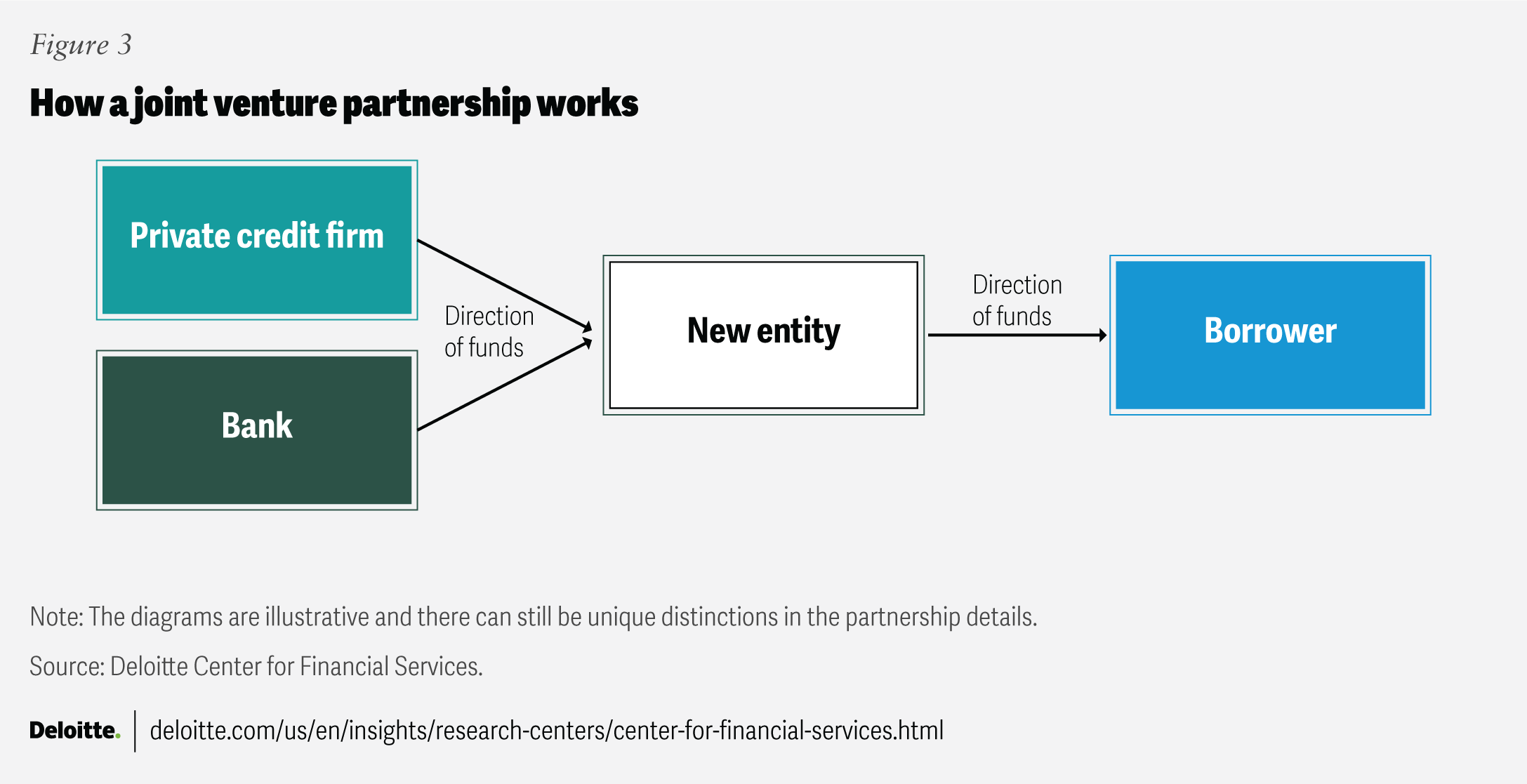

Joint venture

In this type of partnership, the bank and private credit firm create a separate legal entity that originates, funds, and retains loans. Therefore, the loans are not on the bank’s or the private credit firm’s balance sheets (figure 3). The bank and private credit firm each contribute capital, expertise, and relationships to the new entity. The bank may coinvest in the new entity as an equity partner, or could make a debt investment in the new entity (see “Banks can abet private credit by lending directly to funds”).

One example of this strategy is Wells Fargo & Company’s partnership with Centerbridge Partners. The two firms created Overland Advisors, a business development company (BDC). Wells Fargo originates the loans, and both Wells Fargo and Centerbridge are funding the BDC.10

{kind=link}

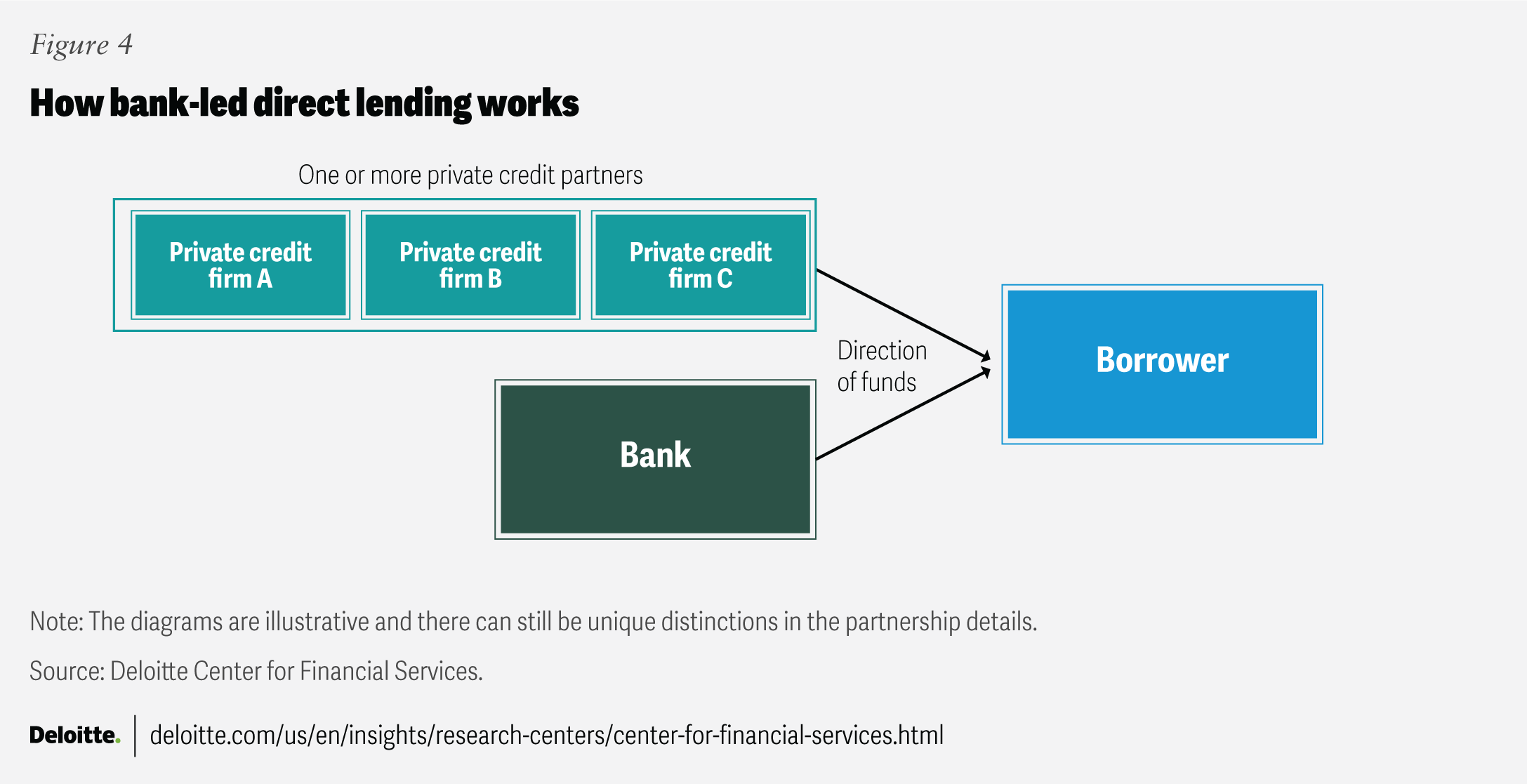

Bank-led direct lending

In bank-led direct lending, the bank has a partnership with a private credit firm, or multiple private credit firms, to coinvest in loans to borrowers, as shown in figure 4. This is similar to syndicated loans, where banks work with other banks to fund a loan. However, in these partnerships, one bank works with one or more private credit firms.

JPMorgan Chase & Co. is adopting this strategy with a consortium of private credit firms.11 It originates loans with its partners and retains the senior portions while private credit partners commit to funding the rest of the loan.

These types of partnerships may have advantages over traditional syndication, such as more customizable loan terms to address borrower needs and faster financing. This can provide a borrower with certainty and speed in execution, knowing that the bank has already lined up lenders. Importantly for banks, this type of partnership may require the most capital retention as loans will be on the bank’s balance sheet.

{kind=link}

What could the future look like for partnerships?

Our analysis found an emerging stratification of the types of partnership strategies pursued by banks and private credit firms. While banks may pursue partnerships for multiple reasons, such as expanding financing offerings and maintaining relationships with borrowers, one overarching consideration includes how much credit risk the partnering bank wants to retain and its subsequent implications for the bank’s balance sheet.

The deal-sourcing strategy and its adjacent strategy, deal sourcing with (optional) coinvestment, appear to be popular partnership models (figure 5). Since these partnerships do not require banks to use their balance sheets and retain more capital, they may be useful for banks that are looking to expand their fee income while limiting credit risk. Additionally, when this strategy includes the option for banks to coinvest in a deal, such as through a wealth management division to broaden access for retail investors or on their balance sheet, it gives banks more flexibility to earn interest income.12 However, the trend also provides further evidence of some banks moving away from their traditional role of holding loans on their balance sheets toward a more capital-light business model.

Although it appears that regional banks have not been engaging in deal-sourcing partnerships, this research only counted publicly announced partnerships. There may be some that are unannounced. Additionally, banks and private credit firms have engaged in non-partnership, ad-hoc transactions that have some similarities with deal sourcing, such as asset sales and credit risk transfers. These smaller deals may foreshadow more partnerships in the future.

{kind=link}

Joint venture model–based partnerships could see increased adoption. By creating a separate entity, banks do not use their balance sheets to retain loans and can, therefore, avoid the need to hold more capital. However, according to Deloitte’s analysis, these entities may have equity investment and debt financing from banks, which would mean the banks would be required to hold capital, a potential drawback for them.

This strategy may continue to grow. Recent research found that one reason some banks prefer lending to non-bank lenders—rather than conducting the lending themselves—is that over-collateralized loans get relatively more favorable capital treatment.13 Therefore, the industry should consider the potential impact of BDCs’ growth, as their role in partnerships may become more commonplace.

Meanwhile, large banks could adopt the bank-led direct lending strategy using their balance sheets alongside a private credit firm or firms. This strategy has more balance sheet implications and may only be possible for the largest banks, that is, global systemically important banks (GSIBs) or large regional banks. As one senior executive stated, his firm could be “product agnostic” by providing direct lending in conjunction with private credit firms, alongside traditional lending products.14 Some GSIBs have committed tens of billions of dollars from their balance sheets to private credit strategies. The strategy will likely require banks to retain the senior tranche of the loan, while private credit firms hold the junior tranche. Banks can earn both interest and fees using this strategy. Similar approaches have already been adopted in the syndicated and private credit markets, where tiered debt structures allow banks and private credit funds to allocate expected risk and returns to respective investors.15

A further consideration is what type of partnerships may appeal to attract private credit firms. Many banks have differentiated capabilities that could appeal to private credit funds, such as expertise or relationships in a particular industry or geography, as well as complementary technology systems that make investing or monitoring assets easier for private credit funds.

Since this research focused on partnerships investing in the United States, it may not be surprising that US GSIBs and regional banks are heavily represented in figure 5. The rise of partnerships between banks and private credit funds is not unique to the United States, however. For example, Brookfield Corporation and Société Générale launched a strategic partnership in 2023.16 Partnerships in Europe are also likely to grow. Deloitte’s quarterly overview of the European debt market found “banks’ on-the-ground client networks” as a growth opportunity for private credit funds’ deal flow.17

Banks can abet private credit by lending directly to funds

Another area of cooperation between banks and private credit has been bank lending to private credit funds directly. Deloitte’s previous research on banks and private credit covered this lending model, and it has continued to grow since then.18

Recent regulatory disclosures have helped industry observers to understand changes in this business. Analysis of H.8 data shows that loans to non-depository financial institutions (NDFIs) accounted for almost 10% of all bank loans and leases in the United States.19 Further Deloitte analysis found that from Q1 2024 to Q1 2025, some regional and super-regional banks rapidly increased their exposure to this lending strategy, with several increasing their exposure by more than 100%.20 Note that these loans are not exclusive to private credit funds, and the data may also include other types of NDFIs.

This trend could continue as private credit becomes more entrenched in the economy. According to one report, private credit firms are operating more like banks, with relationship managers and industry verticals.21

How regional banks can prepare for partnerships

There is an emerging playbook for banks on ways to take advantage of the opportunity for partnerships with private credit firms. The growth in the number of partnerships shows that leading banks continue to innovate even as competition from private credit increases. Additionally, more partnership models may be created, such as a private credit fund working with a consortium of mid-sized banks. A partnership like this could allow for a shared technology platform as well as the pooling of loans into a larger deal that aligns with what a private credit fund may seek.

Regional banks are also forming these partnerships at a time when bank capital relief is likely. Regulators have signaled an interest in changing the supplementary leverage ratios.22 These changes could reduce the incentive for banks to form partnerships with private credit firms and lend more independently. Even so, partnerships with private credit could act as a force multiplier for bank lending, since they can allow banks to hold onto senior tranches and, therefore, increase exposure to industries without breaching risk limits.

Regional banks may be better positioned to offer private credit access to a pipeline of borrowers who traditionally did not have access to capital markets. While regional banks could lose some interest revenue to private credit firms, they may benefit in the long run by maintaining relationships with borrowers and earning fee income from arranging deals, as well as other banking fees, such as treasury services.

Regional banks looking to prepare for more partnerships should consider what value they can already offer private credit firms. Regional banks interested in partnerships will likely be competing with other regional banks to collaborate with private credit firms. While each regional bank is likely to have a unique geographic or asset presence, one differentiator may be the ease with which the private credit firm can work with the bank. In addition, technology platforms could be another distinctive feature if they allow the bank and private credit firm to work together seamlessly to originate and service loans.

As these partnerships continue to proliferate, they not only signal a new chapter for private credit, but also the expanded role regional banks could play in the evolution of corporate lending.

Continue the conversation

Tim Partridge

Mark Brindisi

Joshua Henderson

by

Tim Partridge

Mark Brindisi

Joshua Henderson

The authors would like to thank Richard Rosenthal and Jeff Levi for their contributions to the article.

Cover image by: Rahul Bodiga

Visit the Deloitte Center for Financial Services

Access more insights for the banking and capital markets, commercial real estate, insurance, and investment management sectors.