How banks can turn AI-assisted customer service into a business advantage

Deloitte research reveals four key considerations to ensure that AI helps reduce friction in customers’ experiences with banks’ contact centers—rather than exacerbating it

Banks are investing heavily in AI and, as one former bank executive recently told us, “Contact centers are the biggest unlock for AI right now.”

Customers’ experiences with banks’ contact centers are often defining moments in their relationship with those institutions. They can make or break customer loyalty. And AI is poised to reshape banking contact centers, enabling a more connected service model in which routine work gets easier, customer friction declines, and human agents focus on the moments that matter to consumers.

But according to recent Deloitte research, many US banks could be at risk of unintentionally eroding trust in those key moments due to a potential blind spot banking executives could have regarding their customers’ experiences with contact centers—and AI could exacerbate those existing issues if not implemented properly. Our research uncovered four key considerations for banking executives leading AI-driven contact center transformations.

Getting a clearer line of sight on contact centers’ transformation needs

When a customer makes the effort to call their bank’s contact center because they need to discuss a complex, stressful, or costly issue, they often experience a common pattern: They’re asked to verify their identity and explain the problem to a customer service agent. Then they get transferred and have to explain it all again, often multiple times without resolution.

This “repeat yourself” problem is more than an annoyance for customers. It’s a business risk for banks, and a potential blind spot for many banking executives, according to Deloitte’s 2026 Global Contact Center Survey of 100 banking customers and 30 banking executives in the US—plus seven interviews with executives from US banks and credit card issuers.

When the customers were asked about their top three most important factors when receiving customer support, 71% of respondents valued ease of resolving issues, followed by fast response times (63%) and a positive support experience (52%). Moreover, 51% of customers said they recommended their bank after positive service experiences. But after repeated negative contact center experiences, 28% reported that they reduced spending with the bank—and 31% said they stopped doing business with the institution altogether.

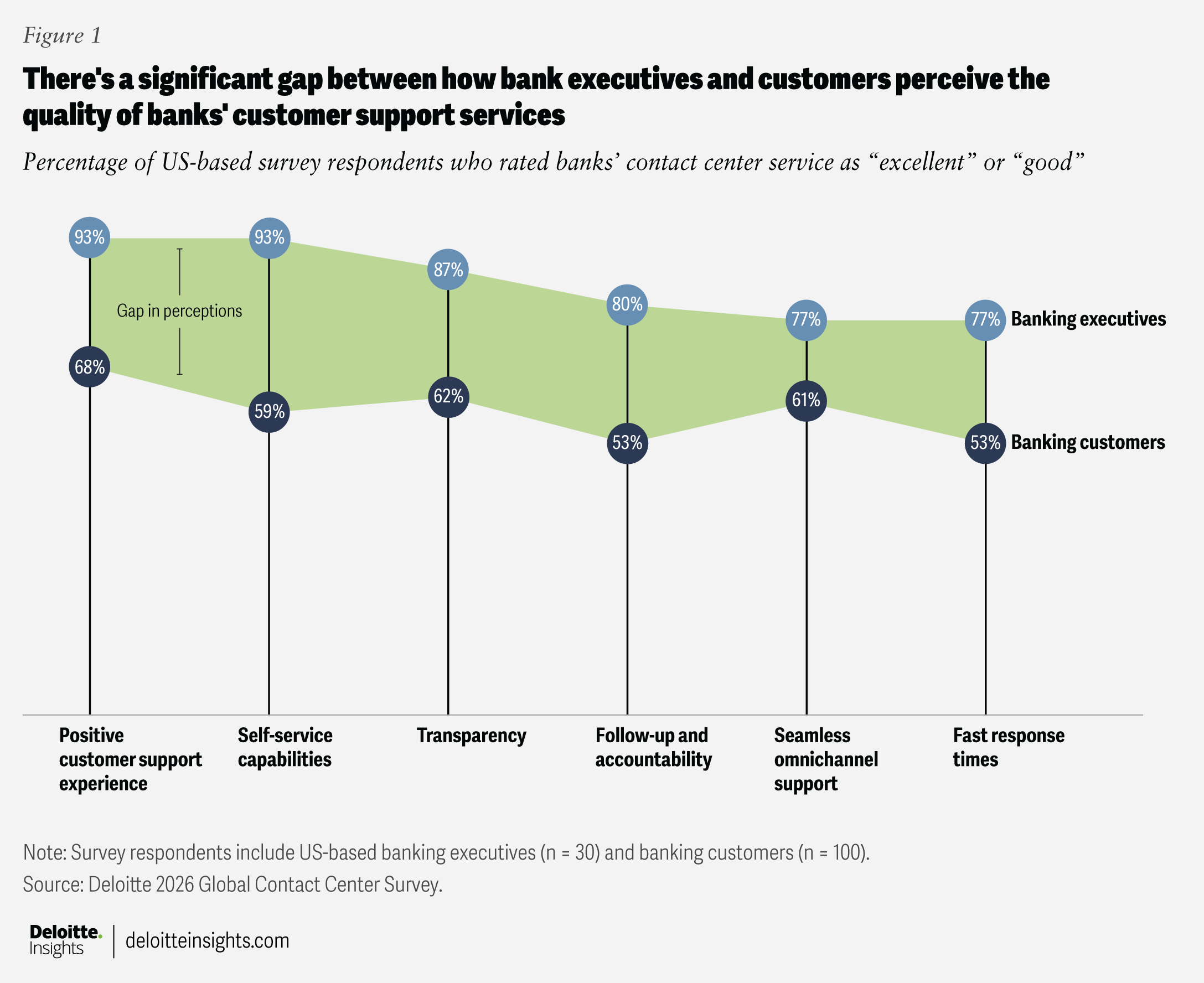

The survey also found that bank customers consistently rated banking support experiences lower than banking executives rated their own institutions’ performance, indicating a potential—and potentially costly—blind spot for banking execs (figure 1). The gap was particularly pronounced in areas such as overall customer support experience, follow-up, transparency, self-service effectiveness, and response speed. While banks may believe they’re delivering strong experiences, customer feedback suggests that many institutions are not performing as well as they think. This blind spot can become a barrier to transformation because organizations often struggle to improve problems they don’t fully recognize.

And despite customers’ prioritization of contact center experiences, 40% of the banking executives we surveyed didn’t rank improving the customer experience in their top three priorities for contact center strategy.

Four key considerations when using AI to transform banks’ contact centers

Many banks are directing a significant amount of their AI investments to improving their contact centers’ efficiency and effectiveness, yet four out of 10 banking executives surveyed might not be dedicating the necessary time and attention to resolving related issues with customer experience. As a result, there’s a risk that AI could exacerbate rather than ease customers’ frustrations. Here are four considerations that might help improve outcomes.

1. Prioritize quick wins while tackling complex tech issues. Deloitte’s survey found that 77% of responding US banking executives cited integration of new technologies with other systems and tools as a major challenge to modernizing contact center operations. Related systems often are fragmented or their use is unclear, but they’re too intertwined with other systems to remove. Plus, executives are trying to integrate AI into 24/7 operations built on technology that is, in some cases, decades old.

The complexity created over decades of operations across systems, platforms, data definitions, workflows, and service rules shouldn’t be underestimated, according to a former enterprise AI and data modernization leader at a super-regional bank who participated in our study. Even when leaders agree on the destination, aligning on a single taxonomy alone can take years, he said.

AI integration into banks’ contact centers is likely to be a long haul, but banks could build momentum by making short-term fixes along the way. Start with a few high-volume, high-friction problem areas, such as fraud alerts, disputes, payment issues, address changes, or loan servicing, and identify the exact moments where context breaks.

Then fix the channel handoffs where customers experience the “repeat yourself” problem most, whether it’s the handoff from app to phone, chat to agent, interactive voice response to specialist, fraud to disputes, or contact center to branch. As a director of contact center solutions at a foreign banking organization told us: “The customer doesn't care about how many channels you have, at the end of the day. They care that you care about them and they don't need to explain the problem again and again."

In addition, focus on making steady progress on structural changes required to support AI at scale, such as rationalizing knowledge bases, standardizing critical data definitions, connecting customer relationship management and case history, simplifying routing logic, and modernizing servicing workflows. The goal is not to replace every core system at once. It’s to more seamlessly share customer context, case history, and next steps across the systems that already exist.

2. Focus on customer retention as a critical success metric. Despite their critical impact on the overall customer experience banks deliver, contact centers still are often seen as cost drivers and measured by a limited set of metrics, such as customer satisfaction and net promoter scores, average handle time, cost per contact, and call deflection. “Most organizations are saying, ‘I just want to reduce my cost,’” according to a study respondent who formerly served as a director of customer experience and a director of contact center integration and optimization at a super-regional bank.

Beneath these metrics lies a deeper issue: No single leader owns the entire customer experience. Fraud, disputes, servicing, digital channels, branches, and contact centers often operate with different goals, systems, and performance measures. As a result, each team optimizes its piece of the customer experience, but no one is accountable for resolution.

This lack of clear ownership and narrow performance metrics can create unintended consequences. Banks’ customer service teams optimize speed, volume, and channel efficiency, while customers often care about resolution, continuity across handoffs, and follow-through.

Banks should therefore consider rethinking both ownership and measurement. High-friction areas such as fraud, disputes, payments, complaints, and account access should have clear owners accountable for outcomes across channels. Success should be measured through first-contact resolution, repeat contacts, customer effort, the number of complaints, the cost per resolved issue, and customer retention, not just handling time.

With customer retention as one of the end goals, AI can be used to reduce friction, improve follow-up, and help contact center agents deliver more personalized next best actions. Such superior service can help drive retention-based growth, with fewer churn moments, stronger trust, and deeper customer relationships—potentially opening up opportunities for upselling down the road.

3. Delegate service tasks thoughtfully. AI can help make contact centers’ routine work easier, but it’s not the answer to all customer service needs—at least, not in and of itself.

Bank customers are increasingly comfortable using messaging and self-service for simple issues, but phone calls with human agents remain critical for complex or emotional situations. About 70% of the customers surveyed said they used self-service in the past year, yet only 25% of them say self-service resolves 50% or more of their issues without a human agent.

AI’s strongest perceived benefits are convenience and speed: 61% of survey respondents cited 24/7 availability and 40% cited faster response times as benefits of AI. Far fewer associated AI with accuracy, fewer transfers, or better personalization. Many customers see AI as fast, but not yet fully trustworthy.

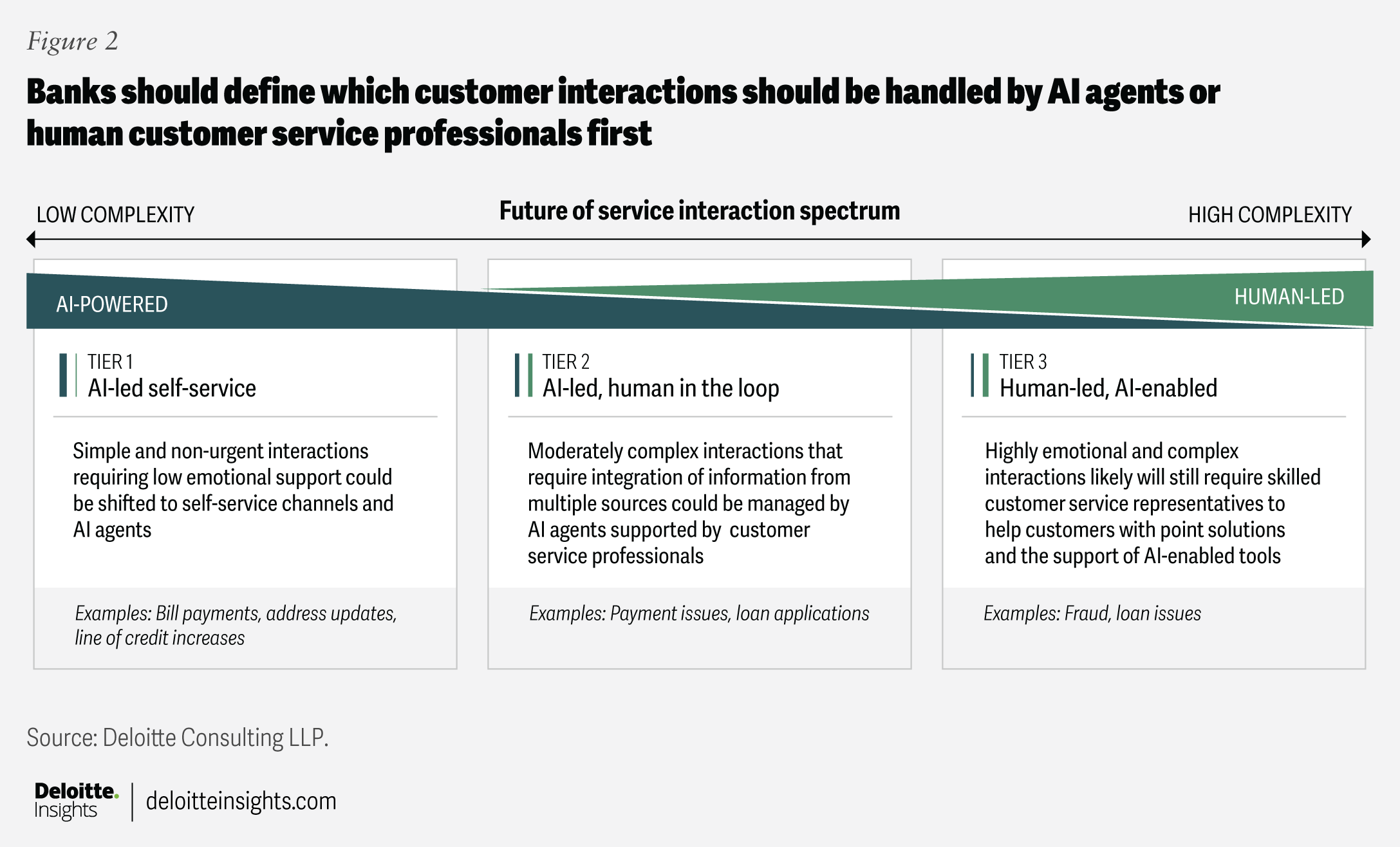

Therefore, simple, low-risk requests can move toward AI-led self-service, and moderately complex customer needs might be handled by agentic AI with human oversight. But high-stakes interactions, such as fraud, disputes, hardship, complaints, and complex lending, should remain human-led and AI-enabled (figure 2).

When customers reach a human contact center agent, that agent should have the authority, context, and tools needed to resolve the issue. In those moments, AI should help the human agent understand customer history, identify relevant policies, recommend next actions, and provide more personalized insights. Human agents should remain accountable for judgment, empathy, and resolution.

Overall, 70% of the banking executives surveyed said AI will shift human agents toward higher-value roles, while 53% expect increased technical or analytical capabilities. Our research indicates that human agents will become resolution specialists and increasingly supervise AI agents to approve the latter’s decisions, train them on building judgment, and guide them when they encounter unfamiliar situations. Meanwhile, quality assurance could shift from manual sampling to continuous monitoring of human and AI interactions.

That said, a critical issue when designing the service tiers is knowing how customers transition between tiers and when AI should step aside. When expanding self-service options, it’s essential to create smooth escalation paths so that customers don’t become trapped in loops where AI repeatedly insists it can solve a problem that clearly requires human intervention. Banks should establish clear guardrails that move customers to human agents when complexity, sentiment, or risk crosses predefined thresholds—and the context of the call should flow with customers through every step of their interaction.

4. Build in governance early. Even in a sector laser-focused on AI governance, many banks still involve separate model risk, compliance, legal, technology, operations, and customer experience teams when governing AI initiatives. These groups often have different priorities, timelines, and definitions of success. As a result, projects can stall at the approval stage even after the technology is ready.

Risk and compliance teams should remain independent in order to retain the perspective needed to challenge assumptions and provide oversight, but they need to be engaged early so that projects don’t stall while issues are reworked and approvals are secured. Overall, banks should embed governance early, not just through technical controls but through clear ownership, decision rights, review processes, and executive alignment. Banks should define who approves models, how models and risks are assessed, when and how humans override AI decisions, what escalation paths exist, and how teams work together throughout implementation rather than at the end of the project.

Timely and embedded governance can also improve productivity. AI-assisted quality assurance, script adherence checks, complaint detection, and compliance monitoring can make oversight faster and more comprehensive.

Taking a clear-eyed view of AI’s transformation potential

Thirty-seven percent of the US banking executives who participated in our survey said they currently use generative AI in their contact centers, and another 37% said they plan to use it in 2026. The main benefit they hope to achieve is higher customer satisfaction and net promoter scores (70%), followed by lower cost per contact and higher agent productivity (60%). Executives expect AI to improve experience and efficiency together.

This transformation takes commitment. Surveyed executives said real AI transformation will be a multi-year process and will go well beyond tech deployment. The executives we spoke with repeatedly cited fragmented data, cloud migration complexity, disconnected servicing platforms, and unclear ownership as barriers to scale. Moreover, the top modernization challenge for contact centers is integration of new technologies with other systems and tools, according to 77% of executive respondents to our survey, followed by data security and compliance (67%), legacy systems (63%), and cloud interoperability (40%).

But perseverance could pay off. Beyond efficiency, effectiveness, and experience improvements—resolving common friction points that can lead to customer frustration—our research indicates that AI could help banks build customer loyalty and trust by enabling more proactive customer support. Ninety-one percent of the bank customers we surveyed are moderately, very, or extremely interested in proactive support, and 71% agree companies should anticipate and solve problems before customers reach out. Yet only 37% said they’ve received proactive support in the past.

This gap is an opportunity. While many banks remain focused on keeping up with reactive support demands, AI may finally make proactive support more practical by helping institutions identify issues before customers need assistance. Fraud alerts, payment reminders, dispute updates, fee avoidance notifications, and account maintenance reminders can reduce inbound demand while simultaneously improving customer trust.

Continue the conversation

Meet the industry leaders

Lauren Littlefield

Anthony Downing

Victor Avakian

Val Srinivas

by

Lauren Littlefield

Anthony Downing

Victor Avakian

Val Srinivas

The authors would like to thank Richa Wadhwani for her extensive and thoughtful contributions to the development of this article.

They would also like to thank Georg Huettenegger and Babu K for their insights, and Lananh Nguyen, Patricia Danielecki, Elisabeth Sullivan, Cintia Cheong, and Molly Piersol for their contributions to this article.

Editorial (including production and copyediting): Elisabeth Sullivan, Cintia Cheong, Stacy Wagner-Kinnear, and Aparna Prusty

Design: Molly Piersol

Audience development: Pooja Boopathy

Cover image by: Sylvia Chang

Knowledge services: Vanapalli Viswa Teja

Visit the Deloitte Center for Financial Services

Access more insights for the banking & capital markets, commercial real estate, insurance, and investment management sectors.