When is a repair, not a repair? The debate continues…

Tax Alert - November 2025

By Hiran Patel & Navroz Singh

Capital or revenue expenditure? If only it were that easy. Taxpayers and accountants often spend countless hours analysing (and debating!) whether expenditure incurred carrying out work on tangible property is a repair and therefore tax deductible, or capital expenditure and as a result, non-deductible (but potentially depreciable).

Fortunately, Inland Revenue has released draft guidance (Income tax – deductibility of repairs and maintenance – general principles) looking to update and replace IS 12/03 Deductibility of repairs and maintenance expenditure (IS 12/03). This is a positive development given IS 12/03 was issued in 2012, and there have been a number of developments on this topic, particularly in relation to buildings which are currently subject to a 0% depreciation rate.

The new draft guidance draws heavily from IS 12/03, developing on established capital/revenue principles. At its core, the draft guidance is centred around the analysis of the capital limitation rule (s DA 2(1) of the Income Tax Act 2007). The capital limitation denies a deduction for repairs and maintenance expenditure that satisfies the general permission, but is capital in nature. For completeness, the general permission (s DA 1(1)) outlines that a taxpayer must incur repairs and maintenance expenditure in deriving their assessable or excluded income (i.e., there must be a nexus between the expenditure and the income earning process of the taxpayer), or be incurred in the course of carrying out its business for the purposes of earning assessable income or excluded income.

The significance of this is that repairs and maintenance expenditure that satisfies the general permission can be fully expensed in the year the work is completed. However, any capital expenditure will be considered non-deductible, and instead will need to be depreciated over the life of the asset (if there is an applicable tax depreciation rate). While not covered in the draft guidance, any improvements to existing assets may qualify for a 20% Investment Boost deduction.

So, how do I know what is capital expenditure?

The two-step approach adopted by the courts in determining whether expenditure is capital or revenue in nature, has been continued in the draft guidance, consistent with IS 12/03:

- Identify the relevant asset that is being repaired or worked on; and

- Consider the nature and extent of the work done to that asset.

The courts have emphasised that each situation is unique and the specific facts must be considered carefully. This emphasises the fine lines that these tests often operate in, and how important the facts are in an assessment of this nature.

Step 1: Identify the relevant asset

Courts have provided guidance that the relevant asset is physically distinct from a wider asset of which the item may be a part of, is functionally complete, or varies the function of another item.

Earlier this year Inland Revenue issued guidance which explains how taxpayers should identify the relevant asset being worked on.

Step 2: Nature and extent of the work done to the asset

When considering the nature and extent of the work done to the asset, there are two key questions:

- Has the work led to the asset’s reconstruction, replacement or renewal - either entirely or substantially? If yes, the cost is considered capital expenditure; and

- If the work does not involve an entire or substantial reconstruction, replacement or renewal, has it gone beyond repairs and changed the asset’s character. If yes, the cost is also considered capital in nature.

Relevant factors to consider include changes to the asset’s value, earning capacity, useful life, function or operating capacity, whether intended or not as a result of the work done.

That all sounds business as usual, so where’s the complexity?

While the principles are generally well established, application of these principles requires careful thought. The nature and extent of the work carried out is an important step in the analysis and is not something that is always clear-cut.

The draft guidance discusses assets that are damaged because of an inherent defect. For example, leaky buildings (where there has been a lot of debate in relation to the capital/revenue distinction in recent years). In such cases, work carried out to remediate the weathertightness of the building will involve large parts of the building and substantial work, At first glance, such work appears of a repairs and maintenance nature to have the building operate as intended. However, in some cases, this work changes the character of the building from its original defective state and is likely to be capital in nature in most cases.

For owners of commercial buildings, this analysis is important as expenditure incurred on the building could either be 100% deductible (as repairs and maintenance) or depreciable at 0% (if it is capital expenditure). In light of the contrasting outcomes and the complexity of the rules, it is important to ensure all analysis is carefully thought through in this area and the Inland Revenue guidance is considered (taxpayers may wish to consider seeking a binding ruling when spending material amounts).

Example 19 in the draft guidance draws out the complexities in this area. The example discusses a taxpayer undertaking work to earthquake strengthen a commercial building and completely refurbish the rundown building at the same time. The relevant asset identified was the commercial building. The draft guidance suggests that the work undertaken involves the reconstruction of the building or a substantial part of it or otherwise alters the character of the building. As such, all expenditure incurred is capital as it forms part of one overall project and cannot be apportioned.

In contrast, example 23 discusses a commercial building that was superficially damaged in an earthquake. While it was in excellent condition when purchased, overtime it had become run rundown. This meant following the earthquake, more repairs were required than would have been otherwise needed. This included re-plastering and repainting the interior walls, repairing the stairwells and roof as well as replacing broken windows and painting the exterior walls.

On these facts, the guidance indicates that the work does not reconstruct, replace or renew the whole or substantially the whole of the building nor does it change its character as it merely restores the building to its original condition. As such, the expenditure is revenue in nature and deductible as repairs and maintenance.

Residential property

Residential property owners, undertaking work on their properties should also be wary of the draft guidance and ensure it has been worked through (note, Investment Boost does not apply to residential property). This is highlighted in the contrasting outcomes below.

In example 16, kitchen renovations are being undertaken during a vacant period between tenancies due to damage from water leaks and a minor flooding incident. The damage is remediated in a comprehensive manner with the kitchen and sink unit removed to access the water damaged flooring with a new unit, bench and sink to the same specifications installed. In addition, other joinery units are refurbished and the free-standing oven is replaced with a modern equivalent. Given no structural changes have been made, the layout of the kitchen has not been altered or improved – the work amounts to repairs and maintenance as it does not go beyond restoring the original functionality of the kitchen and all new items are like for like replacements.

In contrast, example 17 discusses owners that decide to fully renovate a dated kitchen to achieve premium rents by creating an open-plan kitchen and dining area by removing an internal wall. In this process, the owners gut the kitchen, install underfloor heating, and retile both the kitchen and dining room with new kitchen joinery installed and relocating plumbing and range hood ventilation as well as installing double glazing.

Here, the relevant asset is the rental property. The nature and extent of the work does not amount to a reconstruction, replacement or renewal of the whole or substantially the whole of the rental property, however the work goes beyond mere repairs. The key point is the work has resulted in an improvement to the original asset and has changed the character of the rental property and its functionality. As a result, the costs will be capital in nature with only the chattels being able to be separately depreciated, with all other costs being an improvement to the building structure and depreciable at 0%.

Further, example 22 discusses a rental owner deciding to add two new bedrooms and a bathroom, as well as repainting the entire property and new extension. In this example, while the goal was to extend the property, apportionment between the two projects is available. As such, all costs extending the property are capital in nature (including painting the extension). While painting the existing premises were considered revenue in nature. The key distinction is that it is possible to separate the two projects. The contrast in approaches, illustrate the fine lines that operate in analysing the deductibility of repairs and maintenance expenditure.

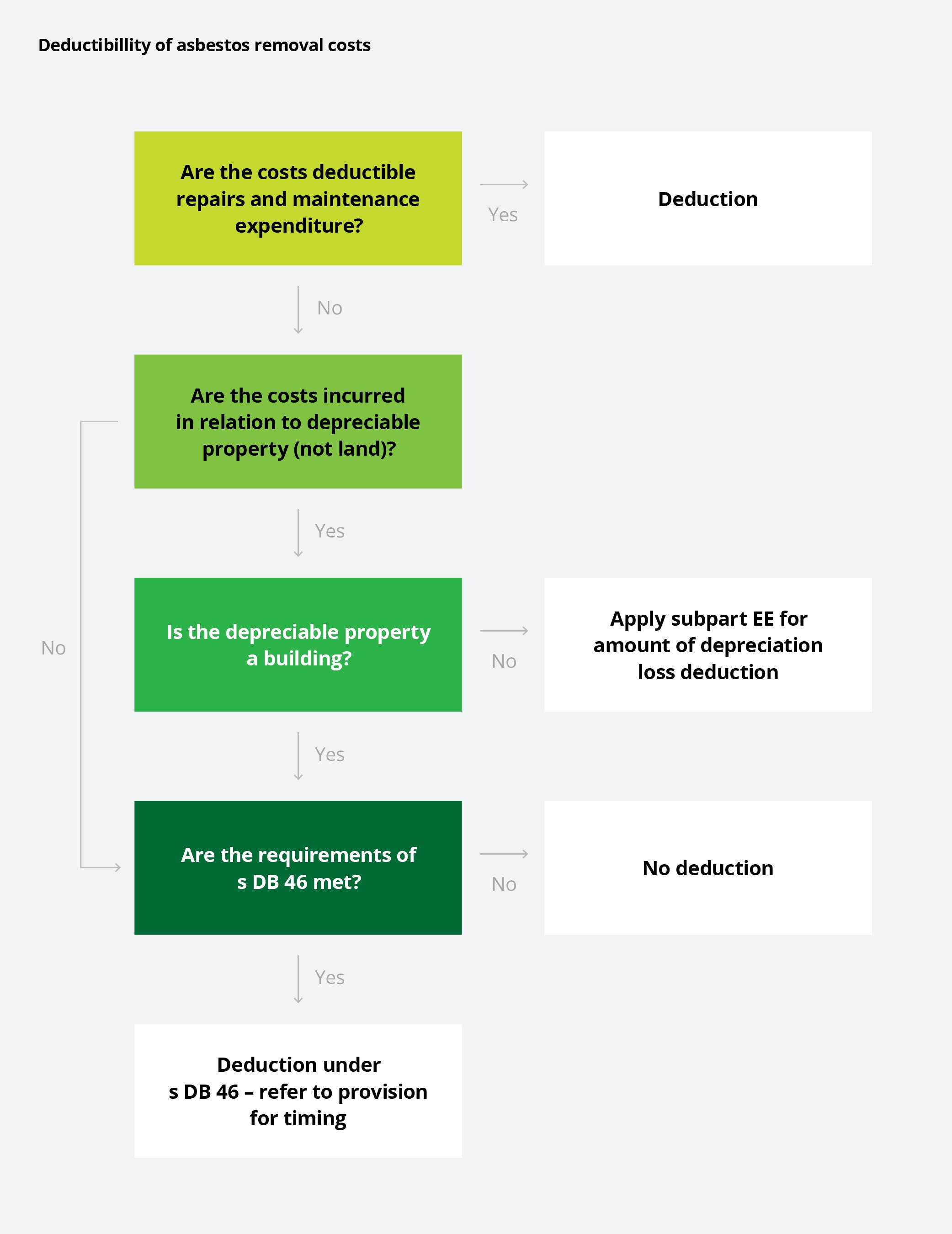

Hot off the press - Can a deduction be claimed for asbestos removal costs?

Continuing with the deductions theme, Inland Revenue has also released for consultation a draft Questions We’ve Been Asked (QWBA): Can owners of commercial property, residential rental property or other assets used in deriving assessable income claim income tax deductions for costs they incur in removing asbestos? The quick answer is yes – generally.

The QWBA looks at the circumstances in which the costs can be treated as repairs and maintenance (and deductible), when a deduction for depreciation loss will be available for capitalised asbestos removal costs, and when a deduction will be available under s DB 46 (a specific deduction provision for avoiding, remedying or mitigating effects of a discharge of contaminants).

The timing of a deduction will depend on the nature and extent of the asbestos removal work and the asset to which it relates and has been summarised in the QWBA in a flow chart:

The QWBA also includes a number of examples that illustrate the tax treatment of the costs incurred in removing asbestos.

Submissions on both the Income tax – deductibility of repairs and maintenance – general principles draft guidance and the asbestos QWBA close on 28 November 2025.

In light of the complexities in this area, we recommend reaching out to your usual Deloitte tax advisor the next time you undertake work on asset or if you would like to discuss making a submission on these guidance documents.

November 2025 - Tax Alerts