Operational transfer pricing: real time efficiency and compliance tailored for your business

Tax Alert - August 2025

By Bart de Gouw, Liam O'Brien, Lucy Scanlon & Sam Thomlinson

The year end Transfer Pricing panic...

It’s post-balance date, and your finance team has almost wrapped up its year-end accounting and financial statement preparation. You remember that the transfer pricing position should be considered. In a folder somewhere sits the company’s transfer pricing policy, which maps out how the Group’s various cross-border intragroup transactions should be structured and priced. Following its creation a number of years ago, some thought was given to how it should be implemented in the company’s financial statements but implementation always fell to the bottom of the to do list and no action was taken. Instead the policy and documentation has become a year-end afterthought, a “check the box” document ready to be handed over to the local tax authority. You sigh, transfer pricing always holds up the year-end process.

Sound familiar?

There is a better way – Operational Transfer Pricing

Transfer pricing does not have to be, and should not be, a year-end only process. Instead, transfer pricing can, and should, be incorporated as part of the operational business processes undertaken during the year. Integrating transfer pricing as part of the business cycle makes the year end process for confirming the transfer pricing approach and treatment a far smoother and far less time consuming process.

What is Operational Transfer Pricing?

Operational transfer pricing (OTP) is the real time implementation of the transfer pricing approach/policy into the operational processes of a business. OTP can be implemented across all sizes and stages of a business, from start-up to large and mature multi-national enterprise.

OTP is more than a compliance exercise; it's about understanding the business’s transfer pricing approach (i.e., what is the approach, why is this the appropriate transfer pricing approach and how can this approach be implemented effectively within the business process, using the existing data, processes and controls in place to make transfer pricing a real time business consideration). This ensures alignment of international transactions with strategic business goals, and mitigates tax risks.

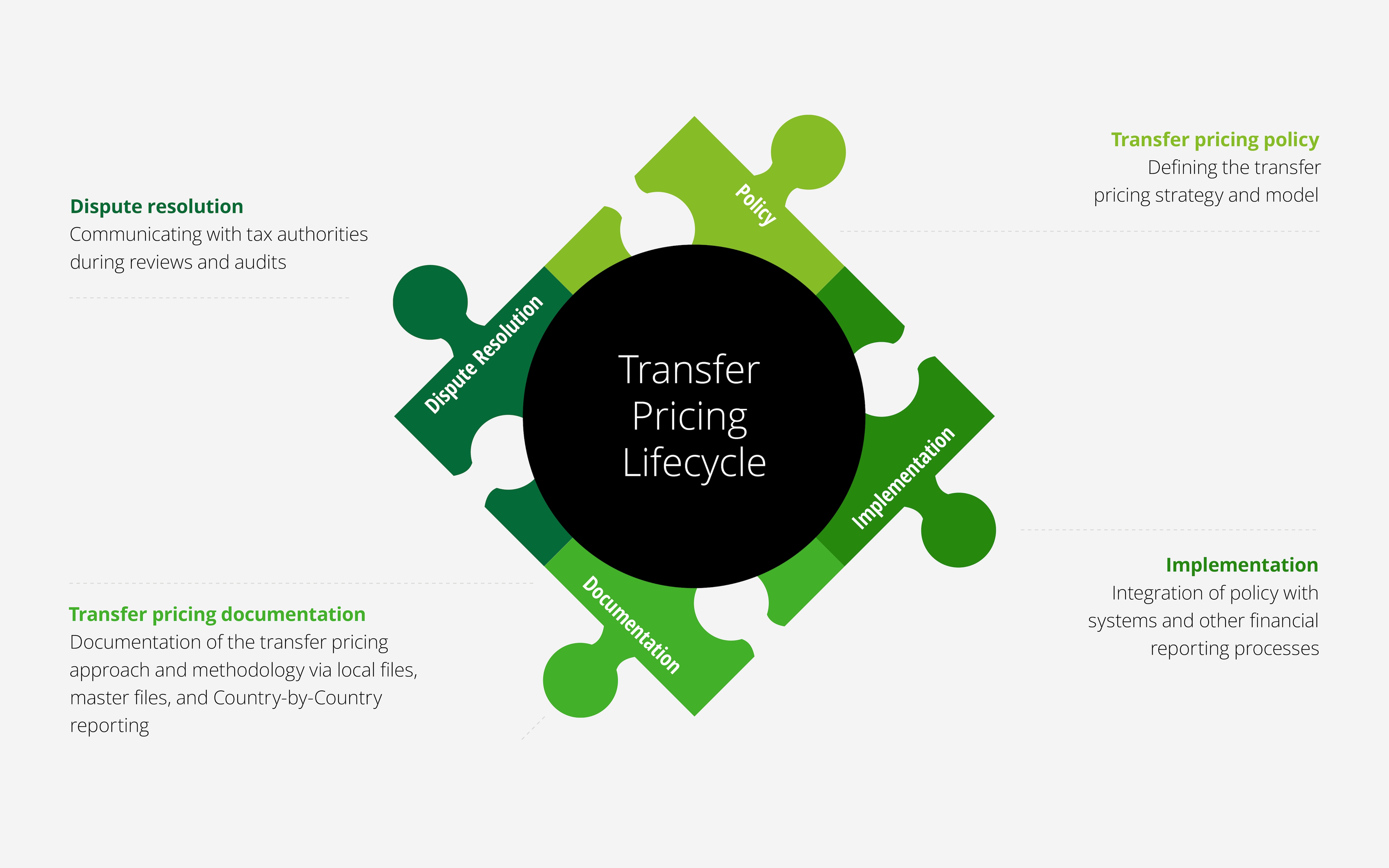

The role of OTP in the transfer pricing lifecycle

Transfer pricing conscious businesses routinely action the policy and documentation phases of the lifecycle by engaging transfer pricing specialists to assist with the development of an appropriate model to remunerate the relevant parties for their contributions and then preparing annual documentation to support the results as being arm’s length.

A transfer pricing policy is only as good as its implementation

However, what is often missed (and what leads to the transfer pricing panic scenario outlined upfront) is effective implementation of the transfer pricing policy into a business’s existing financial processes to ensure that transfer prices are determined accurately and on a timely basis. Businesses often view transfer pricing as an activity that forms part of its year-end compliance process (often adding time to the process and leading to adjustments), rather than as a key part of its everyday financial management function and general Tax Governance Framework. A transfer pricing policy is only as good as its implementation, and documentation is only a valuable defence mechanism if the underlying results it is aiming to support are correctly calculated (i.e., you cannot support and document a policy that has not been implemented).

Tax authorities generally appreciate that transfer pricing solutions should be proportionate to a business’s operations and transfer pricing risk. However, it is still important that the calculation of cross-border related party transactions is appropriately implemented into a company’s routine processes.

What does OTP look like for a business?

OTP is scalable to every business size and maturity with the approach dependent on where a business is in its business cycle and the complexity of related party transactions.

For large multi-nationals, OTP can gather the appropriate information across multiple sources and implement/automate robust processes and checks to ensure real time implementation. For start-ups, firstly the Transfer Pricing Policy is determined in alignment with the strategic growth goals. Once the rationale and purpose of the Transfer Pricing Policy is understood, the appropriate calculations are explained and incorporated into the business cycle in a manner appropriate for the business.

The importance of OTP

Out of date OTP can quickly become an issue for a business, for a number of reasons, including Inland Revenue risk reviews/audits, statutory audits for financial reporting, or through interest from other external stakeholders, particularly in regulated industries.

OTP is particularly important to cross-border businesses because of:

- Inland Revenue’s increased compliance activity- like anything in the world of tax, it is always better to get ahead of any potential issues before becoming the focus of review/audit activity. As part of the general increase in Inland Revenue funding, Inland Revenue’s specialist transfer pricing team has also been reinforced with additional case leads and technical specialists.

- Widespread availability of information - tax authorities, both in New Zealand and overseas, have never been in a better position to perform transfer pricing audits and to process information, including information obtained through the exchange of Country-by-Country Reporting and other automatic information exchanges between tax administrations.

- Customs and indirect tax impacts - Importers who need to change the value of goods after importation (due to quarterly or annual transfer pricing adjustments which effect cost of goods sold) can be subject to fines and penalties on underpaid GST and customs duty (noting that the Provisional Values Scheme is a useful tool for mitigating such exposure from a New Zealand perspective). As such it is important that transfer pricing has been considered early and followed throughout the year to ensure no unexpected customs problems arise later.

- Issues can be long lasting and difficult to unwind – issues arising from the improper implementation of a transfer pricing policy can create unforeseen consequences, such as:

- Tax deductibility – the deductibility of intercompany expenses relies on expenditure being allocated to the correct entity in line with a business’s transfer pricing policy. The risk of not implementing a transfer pricing approach in real-time is that a revenue authority could consider that there is no actual legal transaction, or that expenditure recognised in an entity has no nexus with its income generating activities, potentially leaving deemed transfer pricing income in one jurisdiction but no deduction in the other jurisdiction.

- Tax losses trapped– if processes have not been put in place to ensure the accurate implementation of transfer pricing policies, then tax losses may be recognised in the wrong jurisdiction. To the extent a profitable return is expected by the foreign jurisdiction but the entity has returned losses, these losses may not be allowed to be utilised, effectively trapping the losses offshore. Alternatively, paying too much tax offshore (and not enough in New Zealand) could lead to double taxation.

- Tax obligations missed – if a business does not think about intercompany transactions upfront, it might miss some tax obligations in relation to those transactions. An example is the inappropriate payment of a business’s final instalment of provisional tax where, instead of performing timely transfer pricing calculations, year-end transfer pricing adjustments are made post instalment date leading to potential exposure to interest and penalties. Another example is royalties and interest transactions, both of which have withholding tax obligations on payment and likely penalties for late payment.

- Sale and exit – if the ultimate goal is to eventually exit, transfer pricing will likely come up as part of the due diligence process. Potential acquirers will want to see that an appropriate transfer pricing approach has been implemented and documented. Not accurately implementing the transfer pricing policy can be identified as a tax risk that can impact the purchase price.

- General operational inefficiencies – clearly defined, established and (most importantly) a well understood OTP process can help businesses spot potential issues in real time, reduce retrospective adjustments, reduce manual efforts, reduces the risk of manual errors through process controls and support business continuity where team members responsible leave a business. This can help reduce payroll/consulting costs and exposure to interest or penalties where errors cause tax shortfalls.

So, what next?

A transfer pricing policy is only as good as its implementation. Ignoring transfer pricing can be a year-end headache and lead to far reaching consequences that are often unforeseen and costly to mitigate. OTP incorporates the transfer pricing policy as part of the business processes, transforming transfer pricing to a real time process and keeping a business (whatever the size and stage) ahead of errors and surprises.

If you are ready to swap “afterthought” for action, please contact your usual Deloitte advisor.