Insolvency trends and the uneven road to recovery

Tax Alert - March 2026

By Rob Campbell, Amy Sexton, Lily Choun & Luke Cameron

Inland Revenue’s renewed focus on reining in tax debt, combined with ongoing economic pressure, has been a key driver to formal insolvency appointments reaching their highest level in 15 years. As Inland Revenue is the largest petitioning creditor in court‑appointed insolvencies, this outcome is unsurprising and signals sustained stress across the business sector and a slow, uneven recovery.

In this article Rob Campbell from Deloitte’s Restructuring and Turnaround team examines the insolvency data, its implications, and the outlook for recovery.

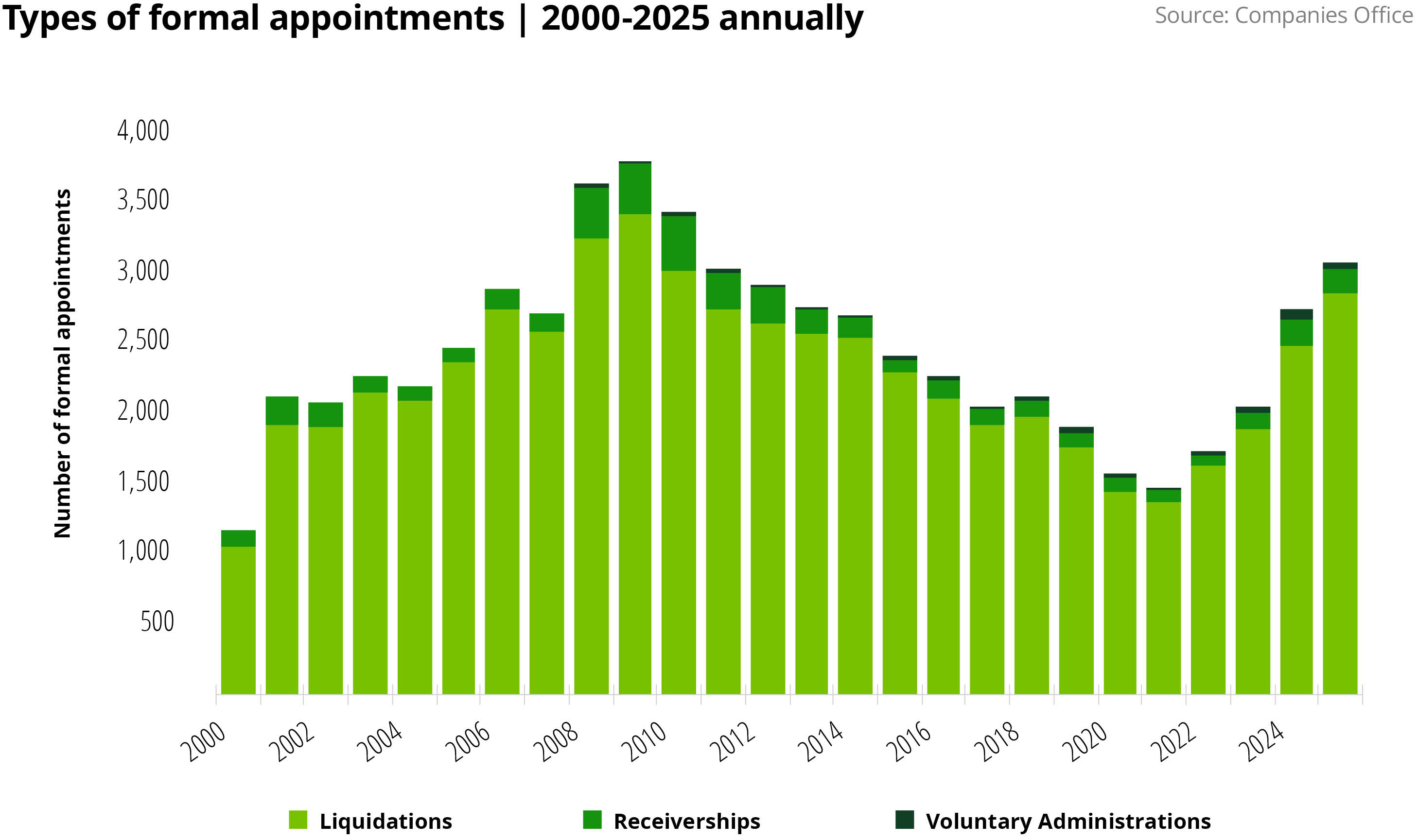

Increases in formal insolvency appointments

Formal insolvency appointments include liquidations, receiverships and voluntary administrations and Deloitte has studied the data on these appointments since 2000. Since 2021, appointments have increased steadily, reaching 3,080 in 2025, the highest level in 15 years.

The December quarter of 2025 recorded 932 appointments, making it the second‑highest December quarter on record, exceeded only by Q4 2008 during the global financial crisis.

Sector hotspots and trends

Construction

Construction accounted for 24% of all company failures in 2025 and remains the most affected sector, with 747 formal appointments. This represents a 14% year-on-year increase. Q4 2025 recorded 197 appointments, the highest quarterly figure for this sector since Deloitte began collecting sector-specific data in 2022.

The sector continues to face weak demands, elevated build costs, cashflow pressure and a thinning project pipeline. Insolvency risk remains concentrated among smaller contractors, with subcontractor failures amplifying stress across the supply chain.

Implications and outlook

Strong project oversight and robust due diligence remain essential. This includes credit and reference checks, understanding group structures, reviewing up‑to‑date financial statements, and assessing GST and PAYE compliance, particularly given increased Inland Revenue enforcement. Best practice also includes securing bank performance bonds, confirming retention funds are held in trust and obtaining appropriate guarantees where relevant.

Despite interest rates easing from mid-2024, construction GPD declined from Q4 2023 following earlier OCR tightening that reduced consents and elevated costs. As activity typically lags monetary policy, recovery is expected to be gradual and uneven, favouring larger, well-capitalised businesses.

Accommodation and food services (hospitality)

Accommodation and food services recorded a sharp rise in formal appointments with 380 appointments in 2025, a 53% year-on-year increase. Q4 2025 recorded 149 company failures, around 80 percent higher than recent quarters. While these figures were inflated by the collapse of a group of 50 related companies, insolvency levels remained elevated even when this group is excluded, reflecting sustained sector‑wide pressure.

Implications and outlook

Smaller and highly leveraged operators are most exposed. High fixed costs, ongoing wage and input inflation and limited pricing power leave many businesses vulnerable to modest demand shocks or seasonal downturns. Rising insolvencies have increased risk exposure for landlords, suppliers and financiers. Tighter credit and leasing conditions may further constrain weaker operators and accelerate closure and consolidation.

Improving consumer confidence towards late 2025, largely in Auckland and Wellington, may offer near-term optimism in a recovery for this sector. However, confidence remains modest by historical standards and cost pressures persist. Insolvency risk is expected to remain elevated in the near term, with a recovery likely to be slow and uneven, led by larger, better capitalised businesses.

Other sectors of note

Rental, hiring and real estate services recorded 326 formal appointments in 2025. A sustained improvement is unlikely until property market confidence stabilises and demand for commercial leasing and equipment hire returns to more normalised levels.

Retail trade recorded 230 formal appointments in 2025. While easing inflation and interest rate relief may provide some stabilisation in late 2025, insolvency risk is expected to remain elevated, with recovery uneven and skewed toward larger, well capitalised retailers with greater pricing flexibility and scale.

Transport, postal and warehousing recorded 174 formal appointments in 2025. While demand may improve as economic conditions stabilise, a sustained recovery is likely to require stronger freight volumes and easing cost pressures. Insolvency risk is expected to remain elevated in the near term, with recovery favouring scale operators and integrated logistics providers.

Read the full New Zealand Insolvency Trends report here.

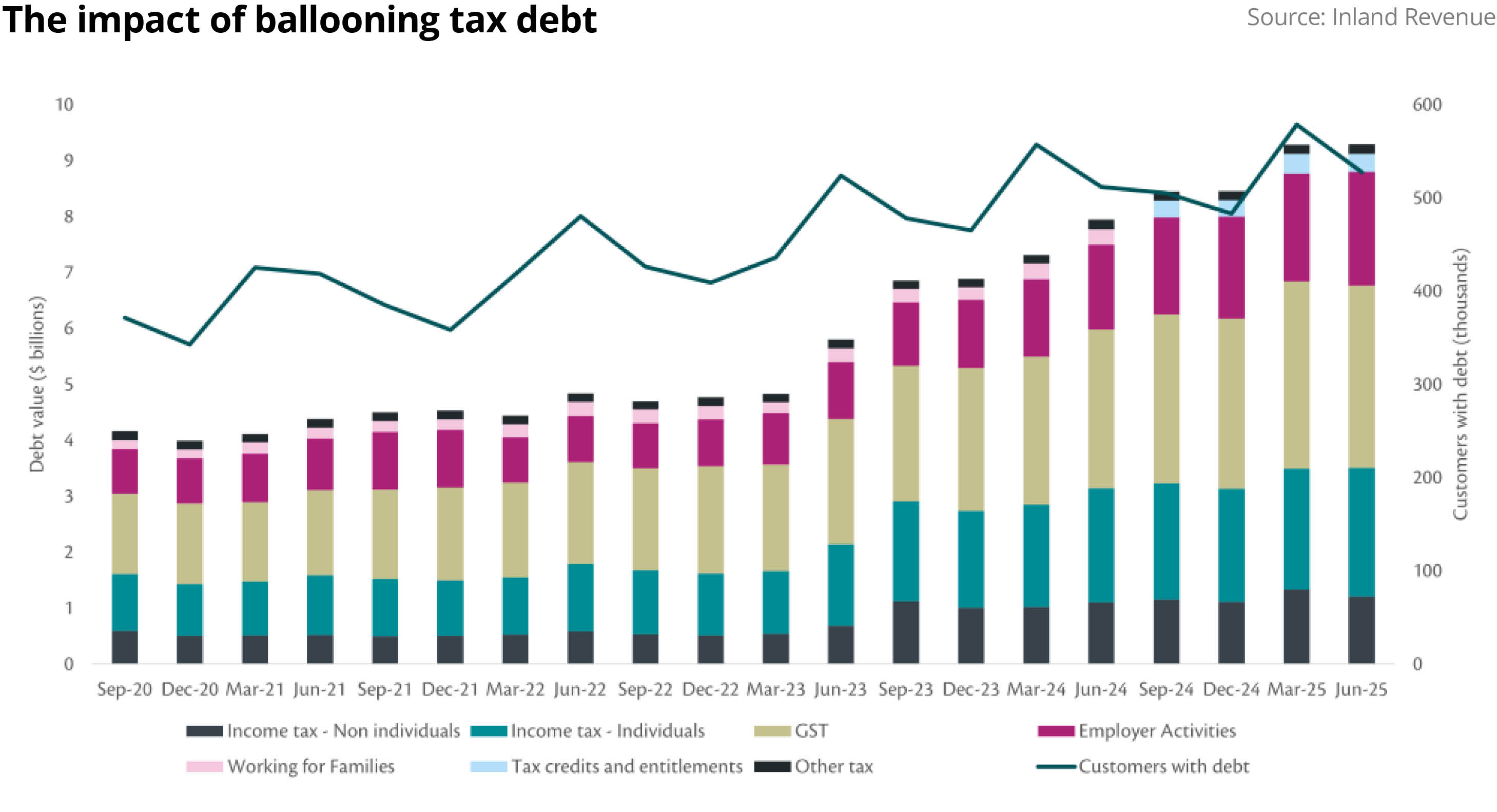

The impact of ballooning tax debt

Following the withdraw of pandemic-era support, Inland Revenue tax debt has risen significantly, reaching over $9b as at June 2025. While 94% of taxpayers continue to pay their tax on time, maintaining the fairness and integrity of the tax system and supporting New Zealand’s broader economic outlook will, in part, depend on Inland Revenue’s prompt response to this growing issue.

Inland Revenue has indicated that is intensifying enforcement activity, supported by increased resources, expanding the use of automated enforcement decision making tools, and encouraging taxpayers with outstanding debt to enter into instalment arrangements at an early stage.

Deloitte welcomes Inland Revenue’s recognition of the scale of the issue and the steps taken to improve public reporting of tax debt defaulters and increasing enforcement activity. Inland Revenue is not intended to serve as a lender of last resort and should not be used as such by businesses that are no longer economically viable.

Recovery will be uneven and slow

While easing inflation and prospective interest-rate relief may support conditions later in 2026, insolvency risk is expected to remain elevated in the near term. Recovery is likely to favour larger, better-capitalised businesses and consolidation is likely to be observed across several sectors.

Renewed Inland Revenue enforcement and investigation activity is expected to remain a key driver of insolvency appointments, reinforcing a slow and uneven recovery.

Deloitte supports businesses to reduce risk and maximise value. Navigating change, whether driven by growth or financial stress, is critical to sustainable performance. Please contact your usual Deloitte adviser to discuss how we can help.

March 2026 - Tax Alerts

- End of tax year decisions that matter

- Insolvency trends and the uneven road to recovery

- Finalised guidance on repairs and maintenance

- A win for first-home buyers: Inland Revenue confirms PIEs

can develop housing for sale - Employer Superannuation Contribution Tax – set and regret

- Snapshot of recent developments