Inland Revenue position on rebates and gift cards finalised

Tax Alert - May 2025

By Robyn Walker

Kickbacks and other incentive schemes are in Inland Revenue’s sights with the finalisation of its draft guidance “What is the income tax treatment of gift cards and products provided as trade rebates or promotions?”. This guidance was issued following concern that practices in certain industries had moved away from cash rebates (i.e. discounts on product once certain targets were purchased) to the provision of gifts, free products, vouchers and other gift cards, for which the tax outcomes were misunderstood. Examples came out of the woodwork of trade customers being given gifts as significant as cars and jet skis as rewards for repeat business.

While cars and jet skis may be the exception rather than the norm, it was clear there was a need for clarification that non-cash rebates were not a way to reward customers without any tax consequences.

The finalised guidance also provides important information for all employers on whether Inland Revenue thinks fringe benefit tax (FBT) or PAYE applies to gift cards and vouchers (see below).

What arrangements does the guidance apply to?

There are a wide range of ways in which businesses try to inspire loyalty in customers, and this guidance focuses on business-to-business trade rebate arrangements, including where employees and shareholders may be the benefactors of the schemes. The statement does not apply to consumer loyalty schemes (so you don’t need to consider the consequences of your buy nine get one free coffee loyalty card).

How are trade rebates treated?

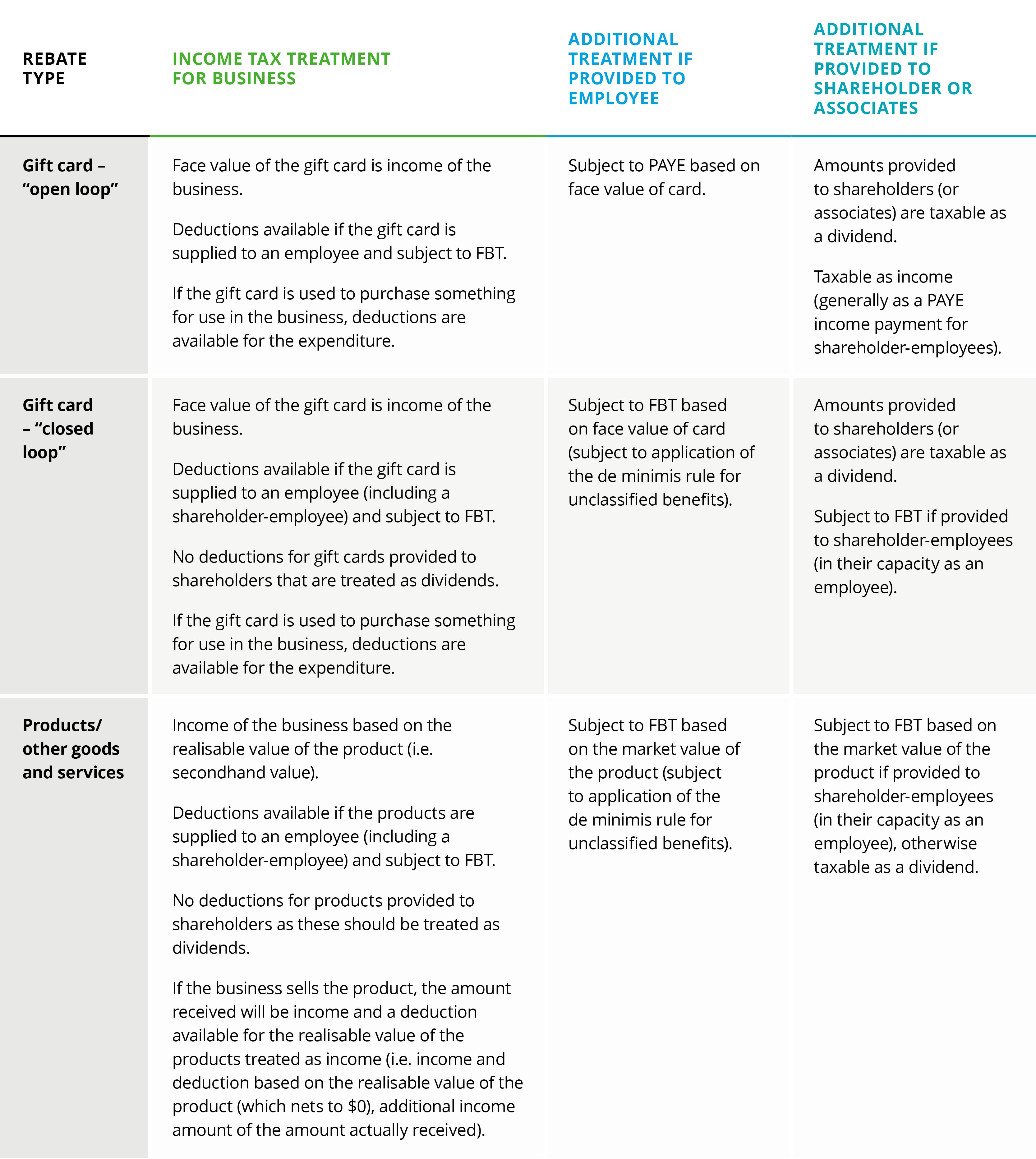

The receipt of a trade rebate, in any form, should be treated as an amount of income by the recipient. The exact treatment may vary depending on the form of the rebate and who the recipient is.

The conclusions in the statement can be summarised by the following table:

What’s the difference between open loop and closed loop cards?

In its interpretation Inland Revenue have revealed that gifts cards come in different forms and the tax treatments differ depending on whether the card is “open loop” or “closed loop” (which includes network and semi-open/closed cards). This treatment applies for all purposes, not just scenarios where there has been a trade rebate. Inland Revenue’s definitions are:

Open loop card means a prepaid card co-branded with a credit card (or other payment network) processor that is accepted for payment by merchants anywhere the network processor’s brand is accepted (that is, in the world, in-store or online) and can be used until the pre-loaded monetary value is depleted or the card expires.

Closed loop card means a prepaid card that is accepted for payment by only a specific merchant or multiple merchants at the same location (such as a shopping mall) and can be used until the preloaded monetary value is depleted or the card expires.

The distinction between the cards is something that many taxpayers would have never given a thought to before, with all gift cards generally being viewed as fringe benefits and tax through FBT returns.

However Inland Revenue conclude that open loop cards are sufficiently widely accepted that they are essentially money and should be taxed through the PAYE regime. Other forms of gift cards are still considered to be vouchers and are taxed through the FBT regime. A common example of an open loop card cited in the statement are Prezzy Cards.

In an acknowledgment that employers have previously taken the view that open loop cards are fringe benefits, Inland Revenue propose that this treatment is corrected on a go-forward basis and won’t be looking to review the past if the FBT rules have been applied:

“The Commissioner acknowledges that some employers have been incorrectly treating open loop cards provided to employees as fringe benefits (and subject to the FBT rules) and not the payment of money (and PAYE income payments). The Commissioner will not apply resources to correct previous tax positions taken in return periods ending on or before the date of this statement where an employer has incorrectly treated the provision of an open loop card to an employee as a fringe benefit and returned FBT on that basis.”

The requirement to tax open loop cards through the PAYE regime will be an unwelcome conclusion for many employers as there can be practical difficulties and additional compliance and tax costs associated with making payroll adjustments. The FBT return is viewed by many employers as logistically simpler. Potential relief is on the horizon, with Inland Revenue’s FBT policy review proposing a law change to allow the cards to once again be included in the FBT return. However, any such change is still subject to Government approval and legislative processes, so may still be some time away.

For more information, please contact your usual Deloitte advisor.

May 2025 - Tax Alerts

- Axing the admin: Will slashing compliance costs be a focus for Budget 2025?

- Inland Revenue’s compliance activity momentum keeps building

- Inland Revenue position on rebates and gift cards finalised

- Popular employment tax questions

- Tax Governance – new Inland Revenue guidance

- Off-market share cancellation and dividends in lieu, could you be caught?

- PPPs are back, but should they still be structured the same?

- FATCA and CRS update – are you prepared for Inland Revenue activity

- Now Live: Inland Revenue works with tax advisors to launch Participating Advisor framework

- Snapshot of recent developments