Fringe Benefit Tax - options for change

Tax Alert - April 2025

Fringe Benefit Tax (FBT) was introduced on 1 April 1985, and its therefore fitting that its 40th birthday is marked by the release of an FBT policy review and Q&A document. The policy review contains options for change to freshen up the regime to ensure it remains fit for purpose after all these years.

The policy review has been well signalled by the Minister of Revenue, Hon Simon Watts, who had heard countless concerns about the high level of compliance costs associated with the tax. It is compliance costs which are the driver of the proposals, revenue raising takes a back seat as the reforms are intended to be cost neutral overall.

The intention is to create rules which adopt a ‘close enough is good enough’ approach and in turn are better accepted as being a reasonable approximation of the ‘remuneration value’ of a benefit, which in turn results in a higher level of compliance. FBT has been notorious for not being complied with, so it’s expected that whatever changes emerge from the review, they will be better enforced by Inland Revenue. These issues were all raised in a stewardship review of FBT.

The review isn’t proposing wholesale changes to FBT, instead it is targeting some key areas which have been identified as problematic. We think it should be fair to assume that everything else not mentioned (including exemptions, rates and calculation methods are off the reform table for now).

The key focus areas are motor vehicles and unclassified benefits. As a surprise entry, the entertainment regime, which currently sits within the income tax return is proposed to move into FBT, consistent with the approach in other countries. The proposals also suggest some discrete changes to aspects of the regime, positively that includes breaking down the confusing distinction between when PAYE and FBT applies and allowing taxpayers to put more benefits in the FBT return. FBT returns will also be modified to collect some additional data points.

The proposals

Motor vehicles

There have been at least a couple of long held concerns with how FBT applies to motor vehicles, including:

- Vehicles are taxed on ‘availability’ rather than use, so a vehicle which is available to an employee for full private use as part of their package is taxed in the same way as a vehicle with high restrictions (such as only home to work travel).

- To reduce FBT costs it is necessary to keep logbooks to claim exempt days, which in turn causes countless headaches for the employees responsible for getting employees to complete and return logbooks. Likewise, the FBT rules subtract exempt days from the total number of days in a quarter (which varies), resulting in regular errors and in some cases no benefit being received from exempt days.

- The Work Related Vehicle (WRV) rules were being misunderstood, with an assumption a double-cab ute was just exempt from FBT. The restriction that a ‘car’ could not be a WRV also meant that more fuel-efficient vehicles were effectively shut out from the exemption. Likewise, the WRV definition has a mandatory requirement for sign-writing the vehicle, which some employers in sensitive professions could not comply with.

Positively, the policy review seeks to address these concerns, by suggesting some options for change, some more significant than others:

- FBT currently differentiates vehicles based on weight (the motor vehicle rules apply to vehicles with a weight less than 3,500kg, and the unclassified benefit rules apply to heavier vehicles), it is proposed to either increase or remove the weight limit.

- To fully exempt emergency vehicles owned by certain organisations from FBT (e.g. police cars, ambulances and fire engines).

- Removing the WRV definition, as part of a change in approach for classifying all vehicles.

- Simplifying the rules by removing the ability to calculate taxable value based on the tax book value of the vehicle if this option is not used by taxpayers.

- Introducing differentiated taxable value formulas for vehicle types to reflect the different running costs. The current 20% per annum cost base would be replaced by separate rates for petrol/diesel fuelled vehicles, hybrid vehicles, and electric vehicles, with the rates being 26%, 22.4% and 19.4% respectively (these rates follow a review of vehicle costs using AA and MBIE data).

- Taking a ‘remuneration approach’ to classifying vehicles.

The remuneration approach

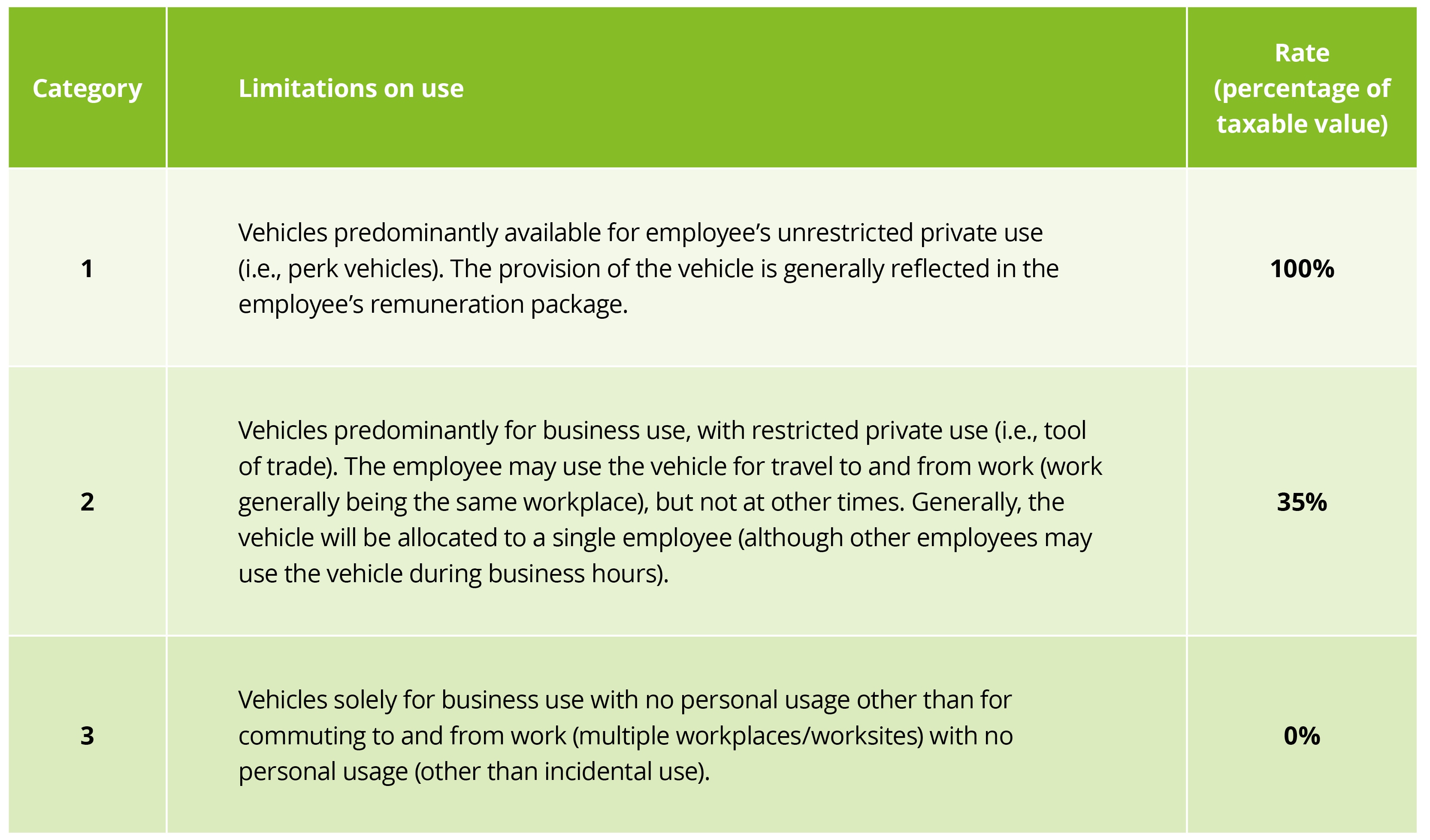

It’s proposed to move the current approach to vehicles to one where the intended remuneration value of the vehicle is a determining factor in how FBT applies. For example, a vehicle which is built into an employee’s package as a ‘perk car’ remains subject to full FBT, whereas a vehicle which is essentially just a ‘tool of trade’ with no private use would not be subject to FBT. There would be a category in the middle where some private use is available, but it falls short of being a ‘perk car’, those vehicles would be subject to FBT at a rate of 35% of the taxable value (i.e. the taxable value is discounted by 65%, and is equivalent to 4.5 days business use and 2.5 days private use). Under the ‘close enough is good enough’ approach, true incidental use of a vehicle would be disregarded.

Below are the proposed descriptions of the 3 vehicle categories:

The difference between category 2 and 3 vehicles is in essence the workplace of an employee. Vehicles which are routinely taken to variable work sites (for example, tradespeople, sales staff, project workers, community workers) would fall into category 3, but a vehicle which is routinely taken to the same worksite (for example, office workers) would fall into category 2. The inherent logic is to take into account that there is some benefit to an employee in not having to fund the cost of home to work travel. Home to work travel is considered a private cost; however, employees who are routinely going to different locations are more likely to be considered ‘on work’ from the time they leave home for the first job of the day and would have more difficulty in organising alternative transportation if a work vehicle was not provided.

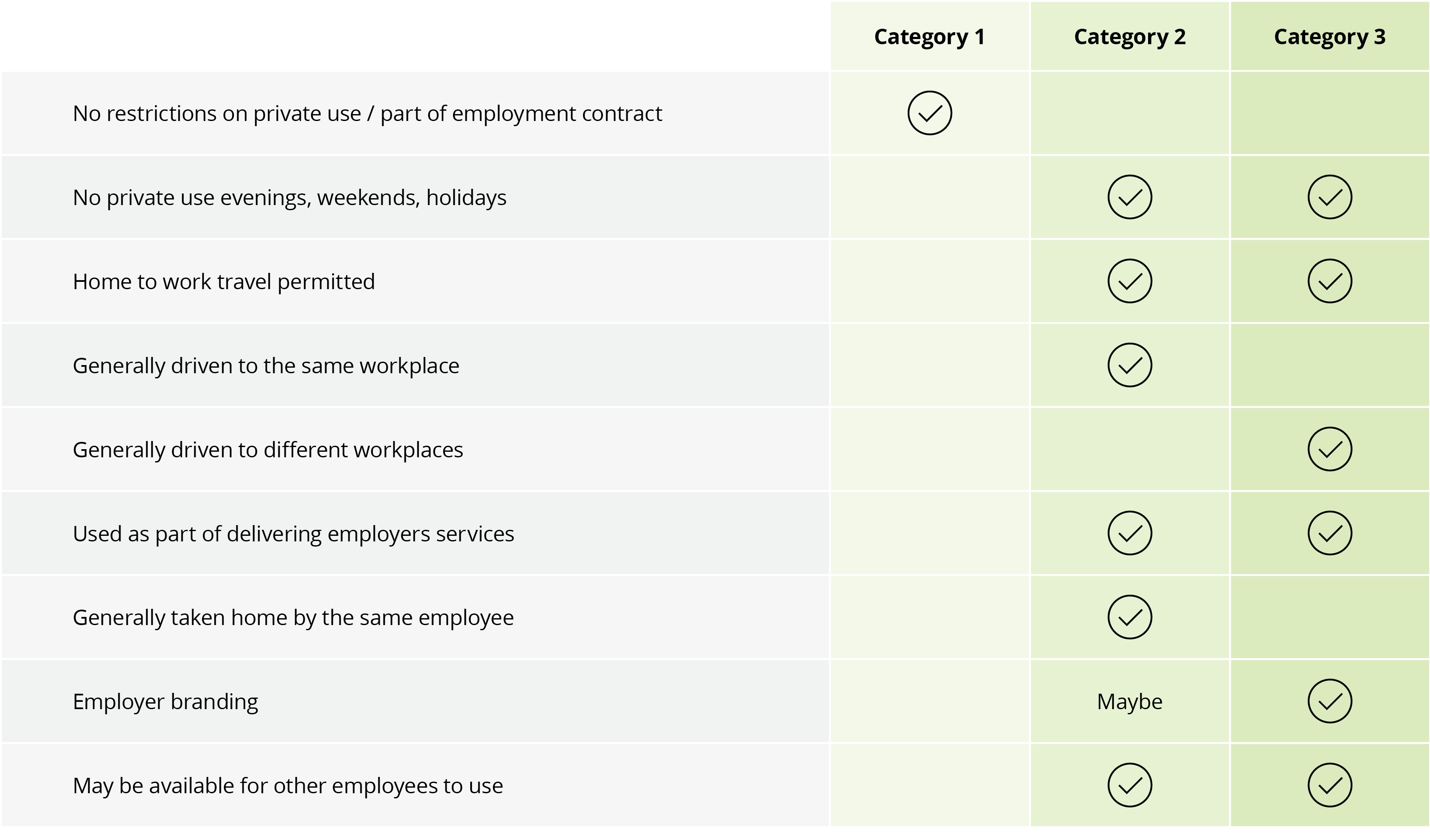

The policy paper provides further guidance on how to place vehicles into the three categories, with the following being a summary of the hallmarks of each category:

The categories, and in particular the category 2 rate, are designed to take into account potential concessions under the existing rules, and therefore it is proposed to remove all current ‘exempt days’ (i.e. business trips away, emergency calls), with the consequence being the removal of the need to keep logbooks for FBT purposes (employers may want to retain these for other purposes). A vehicle would be put into one of the categories based on best estimates of how the vehicle is intended to be used. It is expected that a vehicle will be able to change categories if there is a substantial change to how it is being used (for example a perk car being reassigned to being a pool vehicle due to staff changes).

A question which arises is how to treat vehicles where the employer and employee have currently agreed to restrictions Monday to Friday, with private use permitted at weekends (which would generally only apply to WRVs at present as home to work travel is taxed for all other vehicles). Our expectation is these are likely to fall within category 1. If the proposals are legislated, employers ought to take a fresh look at vehicle fleets and how they are used to ensure the FBT outcomes are suitable and look to amend fleet policies if needed.

It is proposed that because major shareholder-employees (25%+ shareholding) may have more control over vehicle selection, that there be an additional restriction over the use of Category 2 and 3 to avoid “luxury” vehicles falling into these categories (just for those shareholder-employees). As such, a maximum cost base of $80,000 is proposed.

It is proposed that category 2 and 3 cars ought to have an employer’s signwriting on it (much like the current WRV definition), this is partly to assist with enforcement of the rules as it allows the identification of vehicles which may be being used in a manner that suggests it ought to be a category 1 vehicle (e.g. if it is regularly seen down at the boat ramp). The proposals acknowledge that sign writing is not appropriate in all circumstances so it will be possible to apply for an exemption, which is not something the current rules allow.

Unclassified benefits

When FBT was first introduced, there were a plethora of non-cash benefits being provided to employees as a substitution for cash and therefore it was necessary to have a catch-all category of benefits. Fast-forward 40 years and wide-spread benefits are less of a feature of employment agreements. Instead, unclassified benefits are more likely to be ad-hoc, small value items which have no real remuneration value – for example flowers on a bereavement, a gift on the birth of a child or a wedding, Christmas gifts etc. These items can be difficult and time consuming to identify and attribute to individual employees.

A de minimis rule currently exists to remove some small benefits from the FBT net, but this caps out at $300 per employee per quarter and $22,500 of annual benefits meaning larger employers often can’t use it, and it still requires identification and tracking of benefits to prove that it applies.

The policy review puts forward two options to try to refocus FBT back to true remunerative benefits:

- A remuneration test with a cap per benefit (remuneration test)

- A list of non-remunerative benefits (list approach)

The remuneration test draws on a similar test in Australia and would exempt benefits with an individual cost of less than $200 provided they were not provided in substitution for remuneration. This would look at whether something is provided frequently or regularly and whether it is something that an employee can expect as part of their employment agreement. Under this approach, things like flowers, low value Christmas gifts, occasional recognition for performance, casual sports club fees and employer branded merchandise would likely be exempted, whereas gifts costing over $200, gym memberships, and non-work related travel benefits would remain subject to FBT.

The intended outcome from this test is that ad hoc small benefits can be ignored, providing a material saving in compliance costs.

Under the list approach, there wouldn’t be a need to apply judgement like with the remuneration test, instead a defined list of benefits would be specifically exempted, with everything else being subject to FBT (with the existing de minimis rule remaining in place). Exempted items could include:

- Flowers for one-off events

- One-off prizes with a cost less than $200 (e.g. an employee of the month style award)

- Token gifts (e.g. a box of chocolates or a branded drink bottle)

In addition to the above options, the policy paper notes that a different approach could apply to ‘points accrual reward schemes’. These are generally purpose built to allow employers to reward employees with points which are accumulated and exchanged for benefits. Because they are inherently part of a remuneration package its proposed these schemes would remain subject to FBT. The scheme is likely to track and report on benefit values per employee, meaning that there is less of a compliance cost reason to exclude these benefits from tax. It’s proposed that the fringe benefit will arise at the time the points accrue to the employee rather than when the points are spent by the employee.

Finally, perhaps in an attempt to check who’s paying attention, without referring to carparks directly, the policy review poses the question of whether the “on-premises exemption” is still required if the other suggested changes are required. Ultimately the paper summary proposes that the exemption be retained.

Entertainment

If taxpayers were to rank least favourite tax rules, entertainment rules would be right up there with FBT. It’s for this reason that these rules have been incorporated within the scope of the policy review.

The current entertainment rules are a regular source of confusion and frustration, with many taxpayers conservatively treating anything that could be entertainment as subject to the 50% deduction limitation, rather than seeking to analyse every coffee or meal consumed by employees.

It is instead proposed to subsume entertainment into the FBT regime (this approach is taken in other countries like Australia and the UK), with a new “entertainment” category created. This would be taxed at a flat rate of 49.25% (like a pooled benefit) and would apply to entertainment provided to both employees and non-employees. “Entertainment” would be redefined from the current eclectic list to one of two options:

- Using a de minimis rule (the existing rule or the remuneration test, above), to exclude any non-remunerative entertainment with a per person cost of less than $200.

- Excluding food and drink from the current types of entertainment, except for food and drink provided at parties, social functions or celebrations (i.e. excluding things like coffees and working lunches from the rules).

Other proposals

The policy review makes a number of other suggestions:

- Amending the subsidised transport rules (not to be confused with the public transport exemption).

- Allowing employers to treat ‘open loop’ cards as subject to FBT rather than PAYE (this is in response to a recent Inland Revenue interpretation about trade rebates and gift cards).

- Providing employers with a rule on how to treat global insurance schemes – Officials are seeking preferences between dividing the total cost by the number of employees versus deeming the policy to be pooled benefit.

- To put an end to the confusion about whether PAYE or FBT applies to a particular benefit, providing a rule to allow benefits to be treated as fringe benefits (for example reimbursing employees for the cost of a benefit, which currently is technically subject to PAYE). This approach would not apply to accommodation or motor vehicles.

- Requiring employers to provide more details about benefits provided with FBT returns (this is a restoration of the approach before 2000 where total benefits provided by category were part of the return).

- Allowing FBT returns to be filed electronically through FBT software.

- Allowing the option for FBT in quarters 1-3 to be paid on the basis of 25% of the prior year FBT liability, with a square up completed in quarter 4. This would be optional as some employers would prefer to spread the compliance burden more evenly across the year.

- Requiring businesses claiming income tax deductions for motor vehicle expenses to have to declare in the income tax return whether they have complied with FBT obligations (if any) in relation to vehicles owned by the business.

Conclusion

It’s not often that we see tax officials releasing such pragmatic policy proposals, so they should be commended for this. The adoption of a ‘close enough is good enough’ approach is a refreshing change from the micro precision that we normally see in tax rules.

There is a lot to digest in the paper, and the potential that while the Government doesn’t anticipate collecting any more FBT revenue overall, some employers may find themselves needing to pay more FBT than under the status quo, while some may be paying less. Those employers who haven’t been correctly complying with FBT rules will invariably find that their FBT liability is likely to be higher.

Other positive aspects of the proposals include the neutralising of any perceived tax preference for double-cab utes. The fact that electric vehicles can now potentially also benefit from a 0% FBT rate, or a lower taxable value calculation if they are subject to FBT is a positive move for more sustainable vehicle fleets.

The policy review is only touching discrete parts of the FBT rules, so it should be safe to assume that other tax exemptions, such as the new exemptions for public transport and bikes, and the long-standing other exemptions, such as in relation to health and safety, business tools, distinctive work clothing etc will remain untouched – however it wouldn’t hurt to put in submissions on aspects of FBT that are working well (or not).

The policy review only provides a fairly short period for consultation in order to try to incorporate any changes into legislation to be tabled in Parliament later this year. Submissions close on Monday 5 May.

Ultimately the proposals are about reducing compliance costs, so feedback on whether these proposals should achieve that aim will be important. It is when employers start considering the practical details of how the new rules might apply to their fact patterns that issues may emerge.

For more information on any of the proposals or to discuss how they may impact your business please reach out to your usual Deloitte contact.

April 2025 - Tax Alerts

- Fringe Benefit Tax - options for change

- A step in the right direction? The revenue account FIF method is coming—what we know so far

- Employment tax reminders for a new tax year

- Is the debate over? GST and fund manager fees

- Importing goods? Will the Provisional Values Scheme help you?

- Snapshot of recent developments