Employment tax reminders for a new tax year

Tax Alert - April 2025

By Robyn Walker

When it comes to employment taxes, 1 April is the first day of new year. Payslips reset to zero, employer superannuation contribution tax (ESCT) rates are checked to make sure they make sense based on the prior year earnings, odometer readings are taken by those who do lots of business mileage reimbursements, and of course, it’s the first day of a new Fringe Benefit Tax (FBT) year. In this article we’ll cover some employment tax matters to have top of mind.

FBT

The flipside being that a year has just ended and so begins the countdown to complete fourth quarter FBT returns by 31 May. The level of dread that accompanies the fourth quarter FBT return depends on the FBT attribution approach being adopted (if any) and the level of pre-work that has already been completed in quarters 1-3. Before getting into calculations, its also crucial to understand what FBT applies to in the first instance. Some common mistakes we see include:

- Not using GST inclusive values. This is an easy mistake to make because financial information will normally be exclusive of GST. For FBT purposes everything needs to be grossed up to include GST.

- Getting the taxable value formula wrong for motor vehicles when claiming exempt days.

- Claiming exempt motor vehicle days which don’t qualify for an exemption.

- Not understanding when a car park can benefit from the “on premises” exemption from FBT.

- Misunderstanding how the $22,500 de minimis rule works.

- Linked to the above, assuming something is subject to FBT and exempt under the above-mentioned de minimis rule, when the employer is actually dealing with an allowance or reimbursement which is taxable through the PAYE regime (without exemption).

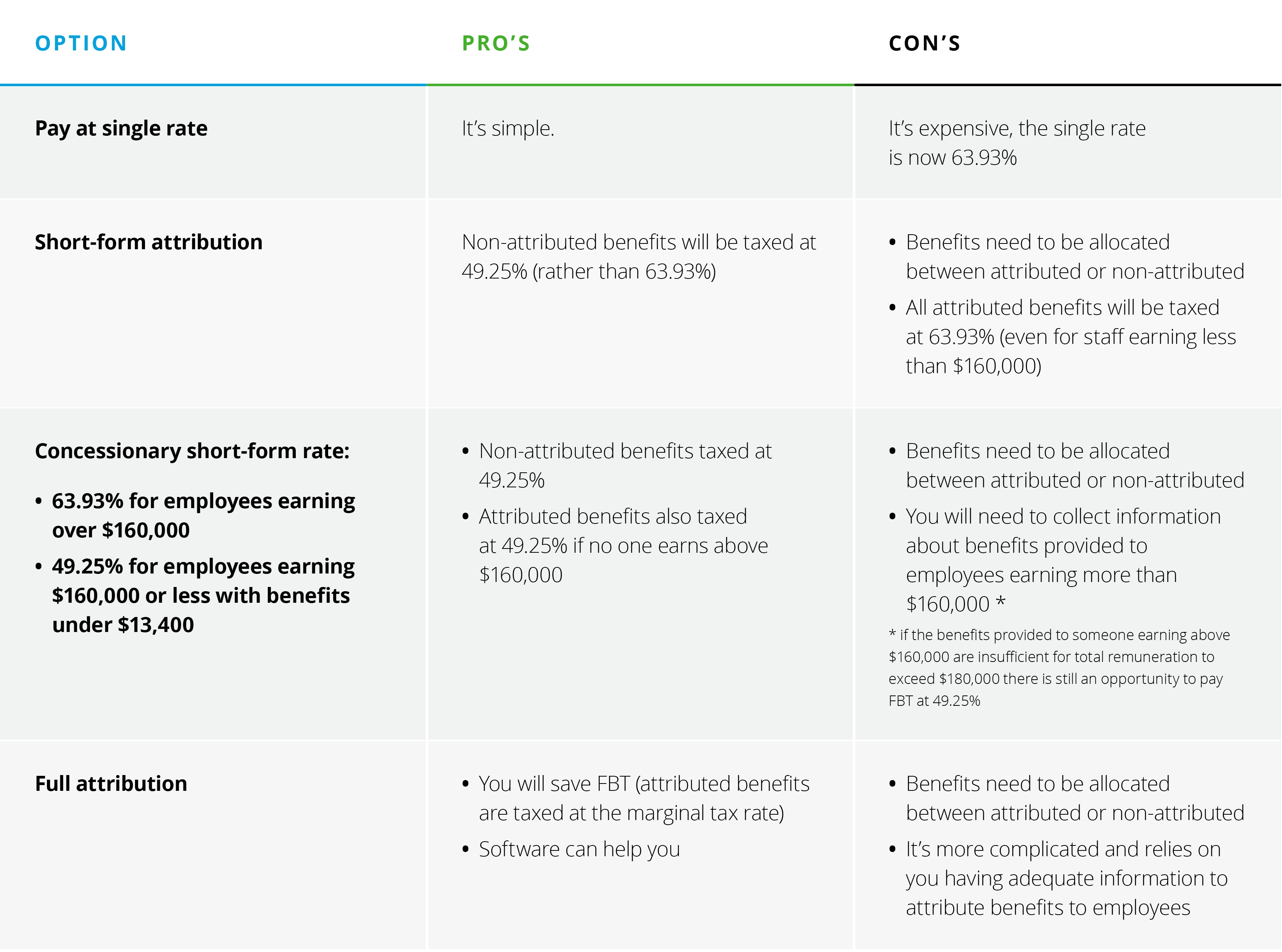

Attribution options

The simplest, but most expensive approach is to just pay FBT on everything at the flat rate of 63.93%; the most complicated but most accurate option is to determine what benefits were received by each employee and undertake a full attribution so all benefits are taxed at the FBT equivalent of the employees marginal tax rate. Between these are a couple of short-form options, which reduce the accuracy of the calculations but can strike a balance between making some tax savings without incurring excessive compliance costs. We summarise the four options below.

A complicating factor to the 2024/25 FBT calculation process is the change to tax thresholds which were announced in Budget 2024. The tweaking of tax thresholds part way through the year has changed the approach to FBT attribution calculations for the 2024/25 year, with those rates changing again in 2025/26. Unfortunately, the timing of when the thresholds changed meant that this is more complicated than necessary, with a new formula designed to ensure personal tax rates and FBT rates work in harmony. The formula is:

tax on all-inclusive pay − FBT on net cash pay

Where:

- all-inclusive pay is the sum of net cash pay and the value of taxable fringe benefits received by the employee

- net cash pay is the cash left in hand of the employee after tax, i.e.:

cash pay − tax on cash pay

This presents a critical risk, particularly for taxpayers who rely on spreadsheets and manual formulas rather than a software tool like TaxLab FBT.

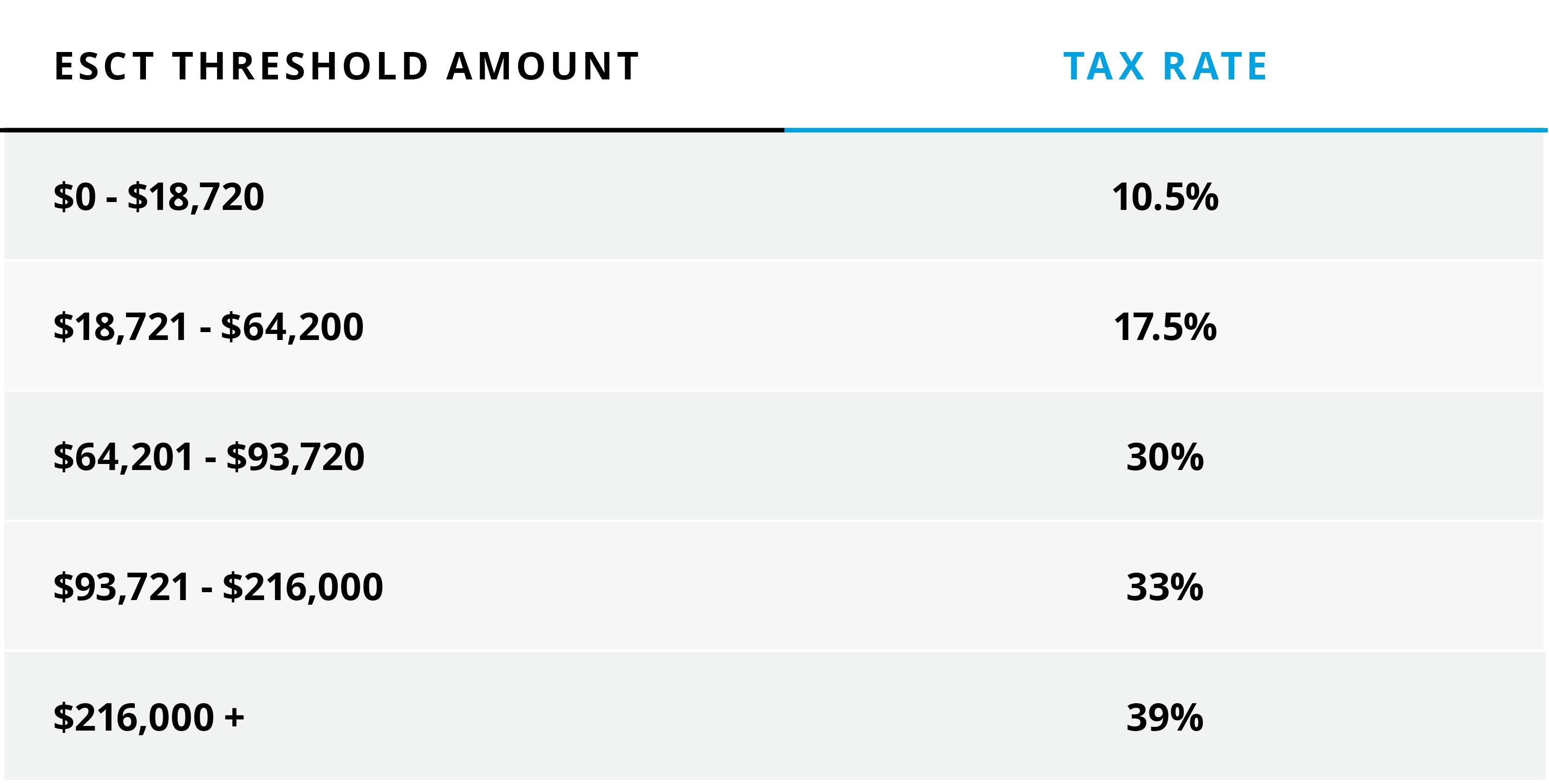

Employer Superannuation Contribution Tax (ESCT)

ESCT rates are designed to be revalidated each tax year. With the tax thresholds having changed, the ESCT bands have also changed, meaning that some employees may be able to qualify for a lower ESCT rate.

Mileage

An unusually popular tax topic is tax-free mileage reimbursement rates. With the tax year having just started, now is a good time for any employees expecting to do significant work related mileage to take an odometer reading as the rate of reimbursement available varies based on the total kilometres travelled since 1 April. You can read more about the mileage reimbursement rules in our June 2024 Tax Alert article.

What to know more?

Deloitte is holding our annual FBT and Employment Tax update webinar on 8 April 2025 at 11am. To reserve your spot for this popular webinar, register here.

April 2025 - Tax Alerts

- Fringe Benefit Tax - options for change

- A step in the right direction? The revenue account FIF method is coming—what we know so far

- Employment tax reminders for a new tax year

- Is the debate over? GST and fund manager fees

- Importing goods? Will the Provisional Values Scheme help you?

- Snapshot of recent developments