Nordic Banking Outlook 2025

After two years of record profitability, 2025 will be defined by macroeconomic headwinds

Now that the year 2024 is in the books, we wanted to take a look at the Nordic banking sector to see where the banks currently stand and what lays ahead of them in 2025. Many of the global trends we highlight in our 2025 Banking & Capital Markets Outlook apply also in the Nordics but there are regional differences that we will discuss below.

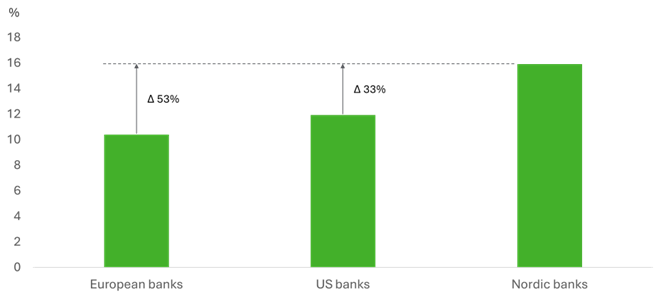

First of all, the starting point here is much stronger. When comparing the performance of the region’s largest banks in 2024 with their peers in the rest of Europe and the US we observe significantly higher profitability in the Nordics, +33% (measured by return-on-equity, ROE) compared with the US banks and a staggering +53% compared with the European banks.

Average ROE of largest banks in each region

The average ROE of 16% delivered by the large Nordic banks in 2024 is outstanding and gives them an excellent starting point to enter the more malign operating environment in 2025. The challenges ahead are mainly related to macroeconomics, lower interest rates and elevated expense levels. We elaborate all of these in our global outlook in detail and hence, will here expand our analysis only on the latter two where we identify specific regional differences.

[*] https://www2.deloitte.com/us/en/insights/industry/financial-services/financial-services-industry-outlooks/banking-industry-outlook.html

[*] All performance data in this article is from the sample banks’ Q4/2024 interim reports.

[*] European banks include: UBS, Santander, BNP Paribas, ING, Intesa Sanpaolo, Deutche Bank, HSBC. US banks include: JPMorgan Chase, Bank of America, Citigroup, Wells Fargo, Goldman Sachs, Morgan Stanley. Nordic banks include: Nordea, Danske, SEB, DNB, Handelsbanken, Swedbank

One of the banks’ revenue engines will stall in 2025

Most banks have benefitted greatly of rising interest rates during the past two years and the Nordic region is no different. The average ROE of the large Nordic banks jumped from ~10% in 2022 to ~16% in both 2023 and 2024, an increase of 60%. The improved profitability has predominantly been a result of higher net interest income (NII) enjoyed by the banks in 2023 and 2024 but that will come under pressure this year. For the Nordic banks the impact of this will be more pronounced due to their higher reliance on this income line compared with their global peers.

Revenue breakdown of largest banks in each region.

Two thirds of total revenue of the large Nordic banks in 2024 was net interest income, 32% more than their European peers and 53% more than their US peers. Lower central bank policy rates will squeeze the banks’ net interest margins putting pressure on this income line, thus driving a need for the banks to find alternative revenue streams in 2025. As we also suggest in our global outlook, one such area could be wealth management.

In our recent article we point out that a massive wealth transfer will occur in the next five years creating opportunities but also threats to the current players in the market. Given that the large Nordic banks are also the leading wealth managers in the region, they should take note of this and gear up to seize the opportunity.

[*] https://www.deloitte.com/fi/fi/Industries/financial-services/perspectives/wealth-management-trends-in-finland.html

Intelligent cost management

Wage inflation and additional investments in new technologies and risk management enabled by higher profit margins have resulted in the operating expenses of the large Nordic banks creeping steadily higher. On aggregate the banks’ expenses have risen by 15% in local currencies since 2022.

Expense development of Nordic banks, indexed.

Given that the Nordic banks’ aggregate revenue rose by more than 30% during the same time period the higher expense levels are well justified and no cause for major concern – at least immediately. But the pressure on the banks’ revenue generation in 2025 will require renewed focus on cost management.

As we point out in our global report, majority of banks globally report failing to achieve their targets set for their cost reduction plans. To avoid this, we recommend a more strategic approach to cost management by tying it to other initiatives pursued by banks to improve their operations. We see lots of promise especially in better use of data and implementation of new technologies, such as GenAI.

In our recent study of the COO function in European financial firms we observed that data and new technologies are already high on the agenda within the industry and not only for cost management purposes but also e.g. to improve the firms’ operational resiliency and for more effective talent allocation.

We believe that this kind of approach to cost management will be more sustainable as it is not singularly focused on cost reduction but also on delivering tangible business benefits.

[*] https://www.deloitte.com/fi/fi/Industries/financial-services/perspectives/the-next-gen-coo.html

Conclusion

The Nordic banks have had extraordinarily strong two years and thus, enter 2025 in a strong position. They will, however, face headwinds this year due to the more challenging macroeconomic environment and should explore new revenue streams and refocus on cost management. For the first, we consider wealth management as one potential solution and for the latter believe in the promise of new technologies, especially GenAI.

If you’d be interested in hearing more, feel free to contact us.