2020 Chief Strategy Officer Survey

Evolving the corporate strategy function for a world of disruptive change

Despite ambiguities around their role, CSOs are uniquely positioned to see around the corner, help their organisations navigate uncertainty and position their businesses for long-term success. It’s time for CSOs to rise to the occasion.

Strategy as a corporate function: Then, now and tomorrow

WITH its roots in ancient military traditions, Strategy only started to solidify itself as a management discipline in the 1980s. It took another decade for Strategy to become a feature in corporate structures of large enterprises, as companies began to realise the importance of developing strategic foresight and of coordinating planning activities more effectively, well beyond the financially oriented mechanics of the annual budgeting process. Since then, Strategy has evolved as a corporate function. It has attracted former consultants into corporate jobs, become a cradle for growing and cross-pollinating talent and currently plays a multitude of roles, particularly in helping the organisation see around the corner, navigate uncertainty and position the business to win in a world of accelerated change.

Learn more

View the Infographic here

Explore the leadership collection

Learn about Deloitte's services

Go straight to smart. Get the Deloitte Insights app

Not surprisingly, the chief strategy officer (CSO) role is also a relatively new addition to the C-suite. And although CSOs have been progressively carving out their space, shaping the CEO agenda and positioning their organisation for long-term success, the breadth and ambiguity of their roles remain a key challenge.

To better understand the evolving role of the Strategy function, the multiple (new) demands on CSOs and their challenges, expectations and aspirations, Monitor Deloitte, the Strategy practice of Deloitte Consulting LLP and the Kellogg School of Management recently joined forces to conduct a survey of nearly 100 CSOs and other senior Strategy executives. We surveyed executives from large and midsize companies across a wide range of industries, in the United States and Western Europe (for details, see sidebar “About the survey”).

The 2020 CSO Survey findings—combined with Monitor Deloitte’s direct experience of working with Strategy organisations and CSOs around the world—provide important new insights into how the Strategy function can evolve to meet new business challenges and about the CSOs’ own perspectives on their role and career ambitions.

In particular, five key themes have emerged from the survey findings:

- Unlocking disruptive growth is a strategic capability gap—CSOs recognise that the ability to generate disruptive growth in a fast-changing market environment is their organization’s most critical strategic capability gap. The 2020 CSO Survey revealed that while 70 per cent of CSO respondents rate disruptive growth as critical for their companies’ success, only 13 per cent of CSOs believe their company is capable of delivering on this strategic priority. CSOs are ideally positioned to help their organisations meet the disruptive growth challenge by architecting a systemic competence, based on a fit-for-purpose model, that promotes a more entrepreneurial mindset, novel ways of sensing emerging trends and opportunities, higher rate of experimentation, greater risk tolerance, better calibrated expectations, well-aligned funding and incentives and creation of an expanded ecosystem of partners.

- Winning (today and tomorrow) requires fluency in technology as a strategic enabler—There is still insufficient understanding among CSOs of the role technology plays in enabling new strategic possibilities; for example, step-changing productivity across the enterprise, creating new sources of competitive advantage, enabling new business models and unlocking new growth opportunities. The 2020 CSO Survey shows that only a small percentage of CSOs believe that their organisations are capable of fully leveraging the potential of digital transformation/e-commerce (26 per cent), analytics transformation (24 per cent) and automation/robotics/AI (17 per cent). CSOs should not only seek to advance their understanding of new technologies, but also (and most importantly) develop a personal point-of-view on how these technologies can help them solve their most pressing strategic challenges. Partnering with their C-suite technology peers, the chief information officer (CIO) and/or the chief technology officer (CTO), is a great starting point to help ensure alignment and help build momentum. External advisers can also be an invaluable resource to guide CSOs in this journey.

- Strategic planning must become more dynamic—The traditional strategic planning process does not match the speed with which the market is moving and likely needs to be reinvented. The process is too infrequent and it takes too long to complete. Most Strategy executives (45 per cent) report that their companies refresh their strategy on an annual basis, while others only go through that exercise every two years (23 per cent) or three years (22 per cent). In addition, the annual strategic planning process typically takes 3–4 months to complete (according to 40 per cent of respondents). Scenario planning is a great technique to create optionality into an organisation’s strategy, arming it with a playbook to quickly react to changes in market conditions or in competitive dynamics—however, only about half of the time (52 per cent) do companies use scenario planning to help “future proof” their strategy.

- Global economic prospects are a major concern—Even prior to the COVID-19 pandemic, the looming threat of a global economic downturn was a real concern for Strategy executives. At the time the survey was conducted (November to December 2019), forty-three per cent of CSOs were pessimistic (or very pessimistic) about the direction of the global economy, while only 10 per cent were optimistic. A recent analysis shows that previous recessions have favoured the prepared—only 14 per cent of companies were able to grow both revenue and earnings before interest and taxes (EBIT) during the economic slowdown, creating a 700 bps EBIT spread between “winners” and “losers”.1 CSOs play a critical role in leading downturn planning efforts to help ensure that their organisations will be able to not only weather the storm but also thrive in volatile times.

- Aspiration to become a CEO—When reflecting on their own career ambitions, a meaningful portion of experienced CSOs (44 per cent) aspire to become a CEO within the next five years. While they are confident about their ability to ascend to the top, they also recognise that they face some significant challenges in preparing themselves to achieve this professional goal, including their general lack of direct operational experience. Leading a meaningful unit of business (e.g., a business unit, a regional operation, a global brand), with direct P&L ownership, or an executive rotation through operating roles in Finance or Commercial, can be effective ways of closing the CEO readiness gap.

About the 2020 CSO Survey

The 2020 CSO Survey was conceived, designed and conducted jointly by Monitor Deloitte, the Strategy practice of Deloitte Consulting LLP and the Kellogg School of Management. It was fielded between November 6 and December 6, 2019 and targeted senior Strategy executives (directors and above) at companies with annual turnover above US$500 million across a variety of industry sectors in the United States and Western Europe. A total of 99 respondents participated in this inaugural survey. The sample includes for-profit businesses (both public and privately held) and not-for-profit organisations.

The dawn of a new era for Strategy

Volatility, uncertainty and disruption have become the norm in today’s business world. The ability to navigate these undercurrents and to succeed in these conditions are becoming critical sources of competitive advantage.

As such, it may no longer suffice for Strategy groups to limit their impact to coordinating an annual strategic planning process that takes months to complete and that mobilises precious resources throughout the enterprise, or to spending time working on internal presentations and board updates, or to dedicating their energy and attention to “special projects” with little-to-no strategic relevance.

Insights from the 2020 CSO Survey suggest that the successful Strategy teams of tomorrow will operate with a focus on seeing around the corners and positioning their companies for sustained success, driving their organisations’ growth agenda in much bolder ways and guiding enterprisewide transformations that will help build today the capabilities required to compete in the future. To do this, they will need to harness the power of digital technology, advanced analytics and scenario planning techniques to explore new strategic possibilities, such as step-changing productivity to reset cost structures, building new sources of competitive advantage, identifying new market opportunities with greater level of precision, identifying valuable partnerships with complementors and competitors and enabling new business models.

The dawn of a new era for Strategy as a corporate function is here. What can CSOs do to help their organisations thrive in this transformative setting? Here are our perspectives:

The state of Strategy as a function

Strategy is still comparatively young as a corporate function. While Strategy first surfaced in organisational charts in the 1990s and has existed for several decades at many large multinational companies, companies today continue to stand up Strategy groups as new additions to their corporate structures. In fact, 39 per cent of CSOs surveyed report that Strategy has existed as a formal function for less than five years at their organisation.

The Strategy function plays a critical role within the modern corporation, directly advising CEOs on critical issues and shaping the strategic agenda. That is evidenced by the direct line CSOs often have to their CEOs–69 per cent of CSOs surveyed report directly to their company’s CEO. However, only 29 per cent of top Strategy executives are awarded a C-level title of either chief strategy officer (27 per cent) or, much fewer, chief growth officer (2 per cent).

From an operating model perspective, more than half of Strategy teams are centralised (55 per cent), serving all parts of the business, while only 9 per cent are decentralised. Interestingly, however, roughly a third (35 per cent) are a hybrid with both centralised and decentralised elements. In our experience, hybrid federated models can be an effective way to ensure that strategy capabilities are leveraged at scale while bringing those same capabilities closer to operating units, particularly if the company has a diverse corporate portfolio (e.g., geographic regions, product categories).

The Strategy function is also highly diverse in terms of scope. The most common areas of responsibility include: long-range strategy planning and development (95 per cent), ad hoc presentations (79 per cent), special projects (78 per cent), M&A/JVs/partnerships (71 per cent), insights/analysis (66 per cent), market research/scenario planning (61 per cent), innovation (49 per cent) and programme management/strategy execution (49 per cent). With such a broad scope, Strategy functions must learn to balance their strategic mandate with the different tactical demands on their time—and that’s not a trivial thing to do, as the survey results indicate.

Strengthen your ability to identify, unlock and capture disruptive growth

The vast majority of CSOs in our survey (96 per cent) recognise the critical importance of their roles in generating organic growth at the core of their businesses—and they feel generally confident in their abilities, with 76 per cent of respondents acknowledging that they feel capable to deliver on this mandate.

Nonetheless, while 70 per cent of CSOs have identified the ability to generate disruptive growth (beyond the core) as critical for their organisations, only 13 per cent of Strategy executives feel confident in their ability to do so (figure 1). This is a huge strategic capability gap that the survey results have highlighted.

Most of the high-growth opportunity spaces are forming on the outskirts of mature markets where disruptive growth is the norm. These opportunity spaces tend to be more fragmented, faster-moving, more fluid and harder to grasp—and large organisations are just not wired that way. The modern enterprise has been generally built for mass-market consumption, scale and operational efficiency. Many large companies generally lack the sensing mechanisms to identify opportunities at the fringe, as well as the speed, the entrepreneurial drive, the risk appetite required to experiment and the patience to succeed in the disruptive innovation game. In addition, they often suffer from the “burden of expectation,” which deems unorthodox and innovative ideas too small to be worthy of their time.

Not surprisingly, many small entrepreneurial ventures have thrived where large multinational companies have struggled. In fact, it is estimated that large consumer products companies have collectively lost billions in sales gains to more nimble players in the past few years alone. We see those market-shifting dynamics play out across various categories, including craft beer, hard seltzer, better-for-you snacks, ethical beauty products, etc. Many large companies have tried to respond to this threat by snapping up small businesses. But those same large companies have quickly figured out that they likely won’t be able to buy their way out of this challenge. Integrating those small acquisitions successfully has also proven to be difficult and deal valuations are becoming too high to justify the capital investment. Being a “fast follower” can become risky and costly.

This is where the Strategy function can help these organisations. How? By architecting a fit-for-purpose model that creates the necessary conditions for identifying, pursuing, capturing and managing new opportunities.

Shape and drive the disruptive technology agenda

We live in fascinating times where technology is exponentially changing human potential, progressively pushing the boundaries of what is possible and unlocking new amazing opportunities. Winning organisations of tomorrow will be faster, able to target opportunities more granularly and more connected (figure 2). The Strategy function must play a central role in bringing this vision to life as an orchestrator of strategic actions across the enterprise.

The survey results show that CSOs largely understand the critical strategic role that disruptive technologies play. However, only a small percentage of CSOs believe that their organisations are capable of fully leveraging the potential of digital transformation/e-commerce (26 per cent), analytics transformation (24 per cent) and automation/robotics/AI (17 per cent). Why the disconnect?

First, the technology agenda in most companies is owned by the IT organisation under the chief information officer’s or the chief technology officer’s leadership. On the surface, that seems to be a logical fit. But in our experience, the mastery of the “ingredients” should be matched with inspired “recipes.” While IT can help the organisation gain knowledge of and build capabilities in different technologies, either internally or through an extended ecosystem, their business partners should be the ones driving the identification of the priority use cases that those technologies enable. The Strategy function is in a unique position to lead the application of new technologies in consonance with its strategic mandate, including step-changing productivity across the enterprise (and reshaping key elements of the cost structure), enabling new sources of competitive advantage, identifying market opportunities with a greater level of precision, unlocking disruptive growth, etc.

Second, many CSOs lack a baseline understanding of new disruptive technologies and their potential applications. Our interaction with CSOs has revealed that they still feel somewhat uncomfortable with all the nuances, jargon, acronyms and complexity associated with the technology universe. Building a basic level of fluency is a necessary step for CSOs to not only understand the new possibilities before them but also engage in a productive dialogue with their counterparts in IT. As part of their learning process, CSOs can certainly find valuable support from internal IT personnel. In addition, CSOs should look to educate themselves on the basics of the underlying technologies, illustrate their applications through case examples and demos and help open the aperture to new possibilities through “art-of-the-possible” ideation sessions.

Adopt more agile and dynamic strategic planning practices

Current strategic planning cycles do not match the speed with which the market is moving and may need to be reinvented. The process is largely sequential, takes months to complete, consumes lots of valuable (and scarce) organisational resources and only happens in long cycles (e.g., annual, biannual, or even less frequently). In fact, the vast majority of CSOs (71 per cent) report spending more than three months on their strategic planning process and nearly a third (31 per cent) spend more than four months. In addition, the survey results reveal that most companies (45 per cent) refresh their strategy on an annual basis, while others only go through that exercise every two (23 per cent) or three years (22 per cent).

In today’s fast-moving world, the current strategic planning cadence is not nearly fast enough to avoid incoherence between a company’s strategy and the evolving realities of the marketplace. Strategy should become a continuous discipline, not a periodic exercise. How do you keep your strategy current if market dynamics change meaningfully in monthly or quarterly (versus annual or biannual) cycles? How do you adopt a more forward-looking perspective during the strategy development process (versus grounding your strategic choices on a diagnostic of past performance issues)? How do you introduce new orthodoxies to help ensure that myopic beliefs and “groupthink” don’t cloud your judgment? How do you build flexibility and option value into your strategy (versus architecting a monolithic plan)? How do you maintain the right level of fluidity to adapt in real time as market conditions change or new material events occur? These are all important questions CSOs have been asking in their search for a more dynamic and adaptable strategic planning process. Without that evolution, companies run the risk of being blind-sided by unanticipated (or faster-than-expected) shifts in consumer attitudes, shopping behavior, competitive dynamics, industry structure, technology enablers, regulatory environment, etc.

In today’s fast-moving world, the current strategic planning cadence is not nearly fast enough to avoid incoherence between a company’s strategy and the evolving realities of the marketplace. Strategy should become a continuous discipline, not a periodic exercise.

The Strategy function should lead the way in reimagining the strategic planning process in its own organisation. Our recent experience working with Strategy organisations points to some emerging practices that CSOs should consider in evolving their strategic planning approach.

First, scenario planning has proven to be an invaluable tool to help companies “future-proof” their strategies, improving organisational preparedness if/once disruption happens, accelerating decision-making under conditions of uncertainty and enabling a greater level of agility in defending against new threats or capturing emerging opportunities. Scenario planning is a structured way of ordering perceptions about how the future may play out by determining what strategic decisions today could offer the best chance of success tomorrow. Scenarios help overcome the tendency that organisations have to oversimplify the future by planning for multiple futures. As a result, scenario planning challenges management to revisit its assumptions about the industry and to consider a wider range of possibilities about where the market may head. This exploration results in a broader, more innovative view about future growth opportunities and risks. The point of scenario planning is not to predict the most probable future; rather, the objective is to develop and test strategic choices under a variety of plausible futures and to challenge the assumptions underlying the strategic plan. Doing this exercise proactively—essentially, rehearsing for multiple futures—strengthens an organisation’s ability to recognise, adapt to and take advantage of changes in the market over time. Interestingly, according to the 2020 CSO Survey, scenario planning seems to be the more pervasive technique in Europe (63 per cent of respondents) than in the United States (46 per cent of respondents).

Secondly, technology offers many enhancement opportunities to create next-generation strategic planning capabilities. Digitising the process is a critical first (and necessary) step to unlock new possibilities. Cloud technology can bring disparate data together, keep it current, make it readily available and offer real-time, rich visualisations. No more Excel spreadsheets, PDF reports, PowerPoint slides to sift through. That enables the use of robotic process automation (RPA) to streamline laborious, repetitive tasks, such as creating reports or compiling planning submissions from different parts of the organisation. Digitisation also helps construct the data that can then enable the use of AI and machine learning. These tools can help discern patterns and meaning that are too subtle or nuanced for the human brain to process with speed and precision. Those technologies can help Strategy teams better track market trends and sense new developments, make sense out of those signals more effectively and quickly sort through options, for example, by using predictive analytics to simulate different strategic responses and their expected financial impact. In summary, while RPA can drive greater productivity and efficiency in planning activities, AI and machine learning can embed greater insight into and overlay greater intelligence onto the process.

Finally, companies should seize the opportunity to utilise better and quicker access to data to monitor how their strategy is faring in the marketplace. Tools such as real-time monitoring and dashboards give companies the ability to quickly sense a disconnect between what they would have expected as a result of their strategy and their actual performance in the marketplace. This in turn enables the rapid evolution of strategy and facilitates holding executives accountable for playing their part in executing a company’s strategy.

Understanding CSOs: Who they are and what they aspire to achieve

The CSO position is a relatively new addition to the C-suite and remains one of the most ambiguous. Our previous research2 on CSOs reveals they typically play six roles (figure 3):

- The adviser—helping shape the long-range strategy

- The sentinel—sensing and interpreting market shifts

- The banker—driving deals and partnerships

- The engineer—designing and running the strategic planning process

- The aide-de-camp—performing as the CEO’s unofficial chief of staff

- The special projects leader—tackling miscellaneous high-impact initiatives

The CSOs of today and tomorrow

- Highly experienced—Sixty-six per cent have 15+ years of professional experience, 44 per cent have 20+ years

- Yet relatively new to corporate strategy—Seventy-four per cent have been in corporate strategy for less than 10 years, 41 per cent for less than five years

- Former consultants—Sixty per cent of CSOs have previous management consulting experience; of those with consulting backgrounds, 17 per cent have spent more than 10 years in consulting and 27 per cent have spent less than 3 years

The primary role for CSOs and the Strategy function, according to the survey respondents, is “the adviser” (27 per cent of the time) (see figure 4). This role revolves around strategic ideas and insights and the ability to craft those elements into a strategy that is coherent and actionable at the corporate and business unit levels. As an adviser, a CSO helps the company formulate its strategy by framing clear strategic choices, soliciting the perspectives of the organisation’s senior leaders, driving decision-makers to alignment and articulating the resulting strategy.

The second most common role for CSOs is “the special projects leader” (19 per cent of time), which involves leading critical projects that the organisation would not be able to address in the normal course of business. This role can be highly valuable, or it can distract the Strategy group from other more important roles if the nature, scope and volume of projects are not planned appropriately. Leveraging the Strategy team as “surge capacity” to tackle tactical initiatives is a poor use of valuable resources.

But is this time allocation good, bad, or indifferent? When asked about how they would prefer to allocate their time, CSOs wish they could spend more time in the more strategic “adviser” and “sentinel” roles. Conversely, CSOs wish they could spend less time in the “special projects leader” role, which is sometimes seen as a distraction. This dichotomy between long-range/strategic and near-term/tactical responsibilities requires CSOs to develop a wide range of skills and competencies.

Given the constantly competing needs and priorities of CSOs, as well as the limited resources often found within the Strategy function (particularly those with smaller teams and even less bandwidth), thoughtful and ongoing consideration should go into charting the CSO’s and Strategy function’s activities. Nascent Strategy functions should take the opportunity to clearly articulate the role they will play within the broader organisation, as well as answer the scope, skills, size and structure questions which will ultimately determine how members of the Strategy function (including the CSO) allocate their time.

CEO career ambitions: Good news, bad news

When reflecting on their own career ambitions, the overwhelming majority of senior Strategy professionals who currently hold either a chief strategy officer or a chief growth officer title (nearly 48 per cent) aspire to become a CEO within the next five years. This is a natural aspiration, as some of the best run Strategy functions that we have studied deliberately treat the CSO position as a grooming ground for general management talent and future CEOs. Moreover, there have been several high-profile examples of successful CSO-to-CEO transitions over the years, such as former PepsiCo CEO Indra Nooyi, who served as PepsiCo's senior vice president of corporate strategy and development for seven years before becoming chief financial officer and ultimately chief executive in 2006. And while CSOs believe in their ability to ascend to the helm, they also recognise that they face some significant challenges in preparing themselves to achieve this professional goal.

In their pursuit of the big office, CSOs can benefit from having a more strategic understanding of the various forces shaping the industry, a longer-range view of value creation, a more in-depth understanding of the strategic agenda and a more integrated cross-functional view of the business than other C-suite executives. Moreover, CSOs generally demonstrate the ability to think abstractly, operate with ambiguity, cut through the clutter and connect the dots, structure plans of action to tackle challenges and orchestrate actions across a wide range of stakeholders. On the surface, those characteristics should position CSOs competitively in the corporate race.

Yet at the same time, CSOs may face challenges in ascending to the helm. Some of these challenges are factual, while others can be merely perceptual. In general terms, it is not uncommon for CSOs, regardless of their tenure, to be seen as “outsiders” within their own companies. In fact, as the 2020 CSO Survey confirmed, most CSOs come into corporate strategy jobs after a stint in management consulting. As such, CSOs typically haven’t grown up in the heart of the business, are seen as lacking operational experience and many have never managed a P&L. In addition, the CSO role is sometimes seen as lacking teeth, since its long-term orientation tends to drive outcomes that might not be measurable for many years, making it much harder to demonstrate tangible impact in the near term.

Strategy executives seem to be aware of those challenges and misconceptions and understand what it takes to overcome them. So much so that the aspiration to run a meaningful unit of business (e.g., a business unit, a geographic region, or a product category), including owning a P&L, is the primary five-year career ambition for Strategy practitioners currently holding a VP of Strategy or director of Strategy title (52 per cent). These younger Strategy professionals are also aiming at the CEO job, but understand that gaining operational experience, earning internal credibility, demonstrating their ability to drive tangible impact and building their internal network are important necessary steps to help prepare them to ascend to the helm.

Future outlook through the eyes of the CSO: Dark clouds on the horizon

Even prior to the COVID-19 pandemic, the looming threat of a global economic downturn was a real concern for Strategy executives. At the time the survey was conducted (November to December 2019), forty-three per cent of CSOs were pessimistic (or very pessimistic) about the direction of the global economy, while only 10 per cent were optimistic. Similarly, only 39 per cent of CSOs were optimistic about how their industries will perform over the next year.

Unfortunately, it is impossible to know exactly when a downturn will strike, or what it will look like. Downturns are notoriously difficult to predict, as they are usually triggered by unexpected shocks to the economy, similar to what we are experiencing today with COVID-19. Moreover, the last two recessions were triggered by unexpected crises—the dotcom bubble burst in 2001 and the housing market collapse at the end of 2007. The amplitude and length of the next downturn will depend on initial conditions and the forces producing it.

Stakes are high during economic turmoil and previous downturns have significantly favored the prepared. History has taught us that executive teams who prepare themselves strategically, operationally, financially and psychologically can win. An analysis of the last three US recessions shows that only 14 per cent of companies emerge victorious, improving both revenue and EBIT margin during the downturn (the “winners”), while 44 per cent of companies suffer losses in both revenue and EBIT margin (the “losers”).3 The result: A 700 bps of EBIT spread between “winners” and “losers” during the downturn. In addition, most CEOs have not led an entire enterprise through a recession during their tenure—according to Harvard Law School’s “CEO Tenure Rate” report from February 2018, over 64 per cent of large-cap S&P 500 CEOs have been in their position for less than 10 years, with the average tenure slightly above seven years.4

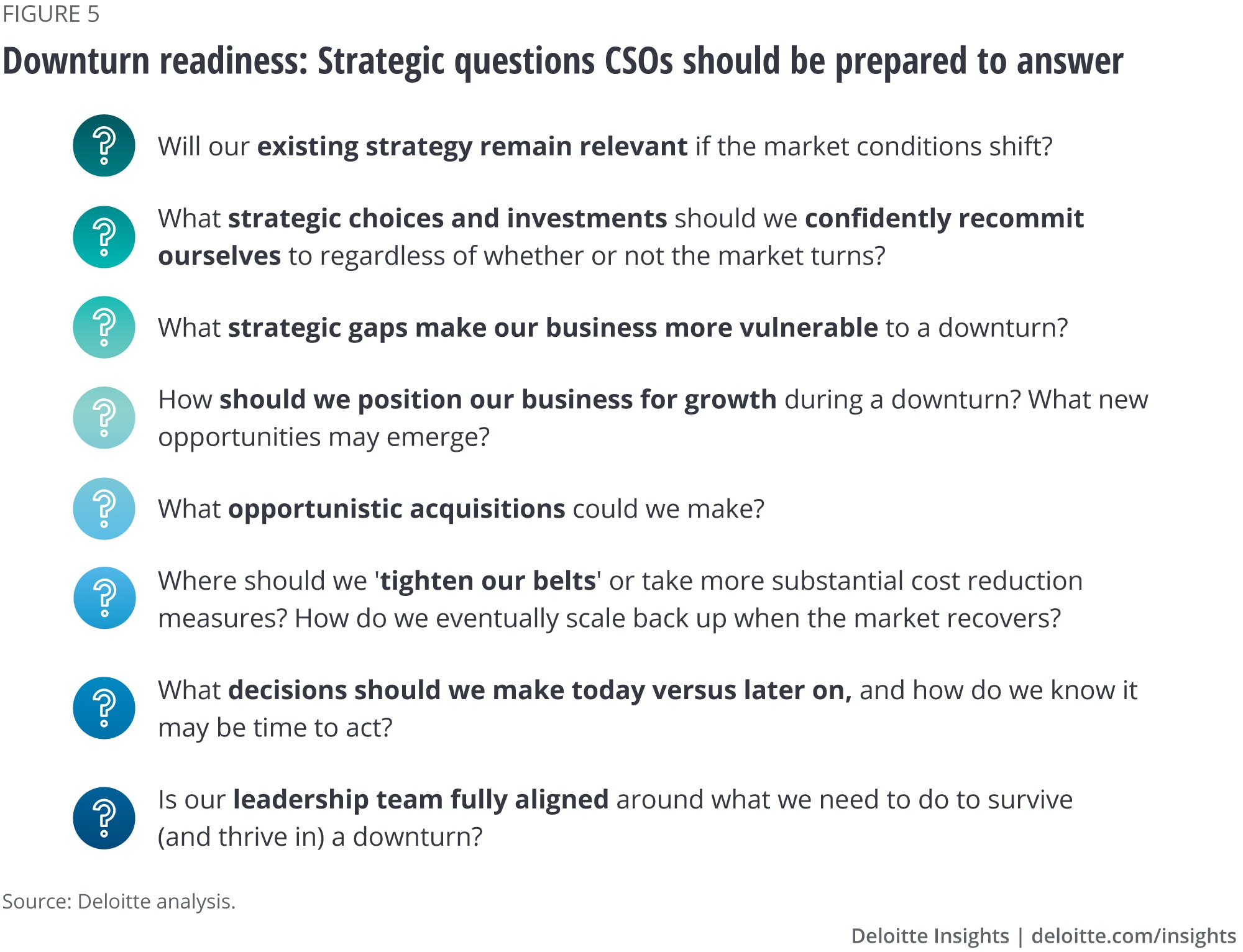

What role should CSOs play? Help their organisations prepare. Strategy organizations are uniquely positioned to help organisations not only navigate the rough seas, but also thrive in volatility. When questions on downturn readiness surface (figure 5), all eyes will likely turn toward CSOs for answers. Scenario planning, as discussed earlier, can be a great ally in helping CSOs plan for different ways in which a downturn may unfold, identify areas of vulnerability, uncover “blind spots,” explore new strategic options, gain greater clarity on when to act and align the management on a playbook to weather the storm as it forms in the horizon.

The good news, however, is that CSOs are largely bullish about their company’s ability to perform well in the next 12 months (60 per cent) and about their own ability to make an impact on their businesses (80 per cent).

The time is now for CSOs to lead the charge

Strategy as a corporate function has come a long way since it started surfacing in organisational charts in the 1990s, with the CSO role becoming more prominent in the C-suite in the 2000s. Yet both the function and the role remain ambiguous and sometimes misunderstood. Nonetheless, CSOs are uniquely prepared to help their organisations sense new market dynamics, understand disruptive shifts, navigate uncertainty and position the business for sustained, long-term growth. We are witnessing the dawn of a new era of possibilities for Strategy as a corporate function and for CSOs who have the drive and the foresight to seize the moment.

Monitor Deloitte

Monitor Deloitte's Strategic Growth Transformation offering helps clients architect strategies and transformation programmes for growth and value creation through levers such as strategic dialogue facilitation, innovation, portfolio optimisation, differentiation and business model transformation.

{kind=link}