Enterprise energy strategy: Securing electrons to power company performance

As energy becomes an increasingly critical factor for growth, margins, and resilience, it should be included on the C-suite agenda

While energy management and the use of distributed energy resources have long been important for a subset of companies,1 some businesses could, until recently, afford to treat energy as part of the operating background. Power was generally available when needed, predictable enough to budget, and managed largely through procurement, facilities, or sustainability functions. Energy mattered, but it did not always shape larger strategic choices.

That model is facing challenges. In many markets, power can no longer be assumed to be timely, affordable, or sufficient in the locations companies want to grow. Costs are becoming more uncertain and location specific.2 Reliability pressures are increasing. Expectations around electricity sourcing and emissions claims are becoming more demanding.3 As a result, energy is starting to influence where companies expand, how margins perform, and how resilient operations remain under stress.

This is why energy strategy should have a place in the C-suite. The set of relevant issues is expanding from “how to buy power” to encompass how much exposure the business carries, how much control it needs, and how early energy enters growth decisions. For boards, chief executive officers, chief financial officers, and business unit leaders, energy should be seen as a cross-functional management issue tied to growth planning, cost competitiveness, capital allocation, operational resilience, and enterprise risk.

Exactly what that strategy consists of can vary widely, from relatively narrow contracting approaches to broader infrastructure partnership models to partial energy independence or sovereignty via behind-the-meter solutions. Companies may secure long-term fixed-price power contracts to reduce exposure to market volatility. Or they may become direct offtakers of new-generation resources, either grid-connected or off-grid, and play a more active role in shaping underlying energy infrastructure. Across these models, important questions include how fuel supply, energy availability, and price risk are allocated, and at what scale those risks are managed across the enterprise. The objective is to establish the right level of control for the company’s exposure, criticality, and growth strategy.

Table of Contents

- A complex corporate energy landscape

- The scope of enterprise energy strategy

- Three strategic drivers

- An energy readiness check for leaders

The new corporate energy landscape: More volatile, uncertain, and complex

Energy markets have always been dynamic and subject to disruption. However, until recently, that dynamism existed within a broader window of relative stability. Shifts in demand were modest, pricing was predictable, and infrastructure operated largely within the tolerances it was designed for.

For many corporate energy users today, that stability appears to be gone. Pricing is more volatile, regional, and sensitive to rate design, demand charges, congestion, local market structure, and energy-contracting approach. Two facilities with similar loads can face different economics depending on location and operations. Energy can influence margin, site competitiveness, and capital planning.

Power availability itself has become a challenge. In the United States, there were about 10,300 active interconnection requests at the end of 2024 in the regions with available data.4 Long interconnection timelines can delay new supply, and accelerating data center demand shows how power availability can stall expansion plans. One estimate suggests that 30% to 50% of the planned 2026 data center pipeline may not get built, due largely to constraints in securing power.5 In some markets, energy access is now a gating condition for expansion.

Utilities can still be important partners in developing an enterprise strategy. Utilities and regulators should balance new large-load requests against obligations for safety, reliability, affordability, and equitable cost allocation for existing customers. For some companies, engaging earlier, with clearer load forecasts, more realistic timelines, and a willingness to evaluate partnership structures that protect both growth and customer affordability can be an important approach.

Cost predictability has weakened. Energy economics can diverge by geography and usage profile: Prices vary across US states, and facilities relatively close to each other can face very different delivered rates.6 From 2020 to 2025, one analysis of commercial electricity rates indicates that most commercial facilities experienced rate increases, with a median five-year compound annual growth rate above the traditional 3% budgeting escalator.7 Energy can be harder to manage through standard budgeting assumptions and periodic sourcing cycles alone. Geopolitical risk adds the potential for additional uncertainty.

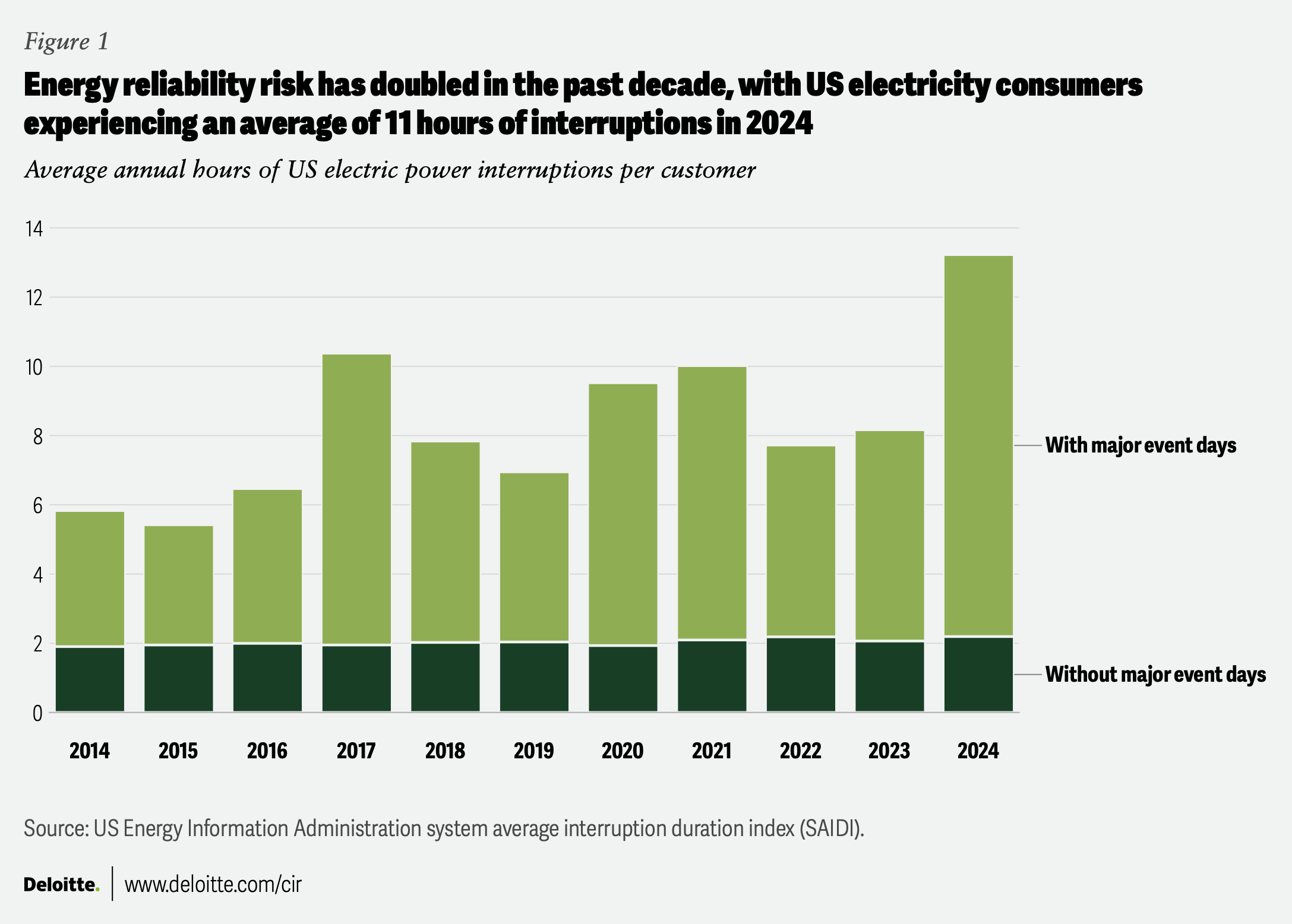

Finally, reliability risk is also rising. US electricity customers experienced an average of about 11 hours of interruptions in 2024, nearly twice the annual average of the prior decade, with major events—those exceeding normal operating conditions, like strong storms—accounting for most of those hours.8 Berkeley Lab estimates that sustained power interruptions cost the United States about US$44 billion annually, with most of that burden borne by commercial customers.9 More frequent and severe storms, wildfires, and periods of high heat may compound outage exposure in vulnerable regions.10

Taken together, these shifts can amount to a structural reset rather than a temporary disruption. Power constraints are influencing where growth can happen. Electricity costs are becoming more location-specific and harder to absorb through routine budgeting. Reliability, regulatory, and reporting pressures are raising the cost of getting energy decisions wrong. And the available solution set is widening. Energy decisions may no longer be just about buying supply; they can increasingly require portfolio design across procurement, infrastructure, operations, and capital allocation. The market itself is increasing the need for energy to be part of business planning.

The scope of enterprise energy strategy

Enterprise energy strategy is the deliberate management of how a company secures, uses, and governs energy to support growth, control costs, and bolster resilience. It can begin with a simple question: How exposed is the business to the energy market, broadly defined? For some companies, exposure can show up as constrained power availability or long interconnection timelines. For others, it can appear in power tariff complexity, price uncertainty, outage risk, load growth, regional concentration, or pressure around decarbonization claims and scope 2 reporting. Some large companies can face several of these pressures at once.

That exposure profile can help guide your enterprise’s strategy. A company whose expansion depends on timely access to power will likely need to bring energy into site selection and capital planning earlier. A company with mission-critical operations may need resilience investments, backup capacity, storage, or more structured supply arrangements. Consider building control, flexibility, and foresight so that the business is not managing energy purely as a reaction to market conditions.

Enterprise energy strategy is broader than procurement. Power purchase agreements remain an important tool, but they are only one lever within a wider portfolio that can include tariff optimization, demand management, efficiency, storage, self-generation, microgrids, resilience investments, and stronger governance over forecasting, contracting, and claims. That broader response can be more viable because capital is moving into the enabling system itself and the economics are shifting rapidly. The International Energy Agency expects total worldwide energy investment to reach US$3.3 trillion in 2025, with about US$2.2 trillion going to clean energy technologies and infrastructure, including grids, storage, efficiency, and electrification.11 At the same time, the economics of some solutions, especially renewable energy and storage, have improved. The costs for commercial (non-utility) solar installations in the United States fell nearly 80% from 2010 to 2024.12 And stationary battery storage costs dropped 45% in 2025 from a year earlier.13 A strategic question for executives to consider is determining which combination of approaches best supports growth, controls cost, and protects operations, while managing tradeoffs among those priorities.

Likewise, pursuing energy sovereignty—itself a spectrum of approaches with the broad aim of increasing control and decreasing dependency—should be considered. It does not mean that every company should aim for full self-supply or asset ownership. It means pursuing a level of direct control over sourcing and usage that is justified by the business’ exposure, criticality, and growth plans. For some companies, that may mean limited on-site generation or storage in a few critical locations. For others, it may mean a more active contracting and governance model rather than physical ownership. Every company should have an energy strategy, but the degree to which energy sovereignty is needed will vary.

Three strategic drivers of enterprise energy strategy

Once a company understands its exposure, a strategic question becomes how energy affects three linked business outcomes: growth, cost, and risk. The same energy decision can accelerate expansion, change margin profile, and alter operational exposure at the same time. One task for management is to weigh those trade-offs deliberately rather than let them emerge through isolated procurement, facilities, or sustainability decisions.

Growth can increasingly be shaped by energy considerations, influencing whether expansion can happen on schedule, at the required scale, or at all. For large-load projects, new sites, and capacity additions, access to power is becoming part of the investment case itself. Energy is moving from a downstream utility question to an upstream decision in site selection, footprint planning, and capital allocation.

Cost can be affected by more than the contract price of electricity. Consider total energy economics: power tariff design, demand intensity, load shape, congestion exposure, efficiency, flexibility, and the cost of the assets needed to support continuity. CFOs and budget-minded executives should understand how energy can affect margin stability and long-term cost predictability.

Risk can include price volatility, outage exposure, interconnection delays, structured contract risk, regulatory change, tariff design, carbon and emissions claims regimes, and rising scrutiny around electricity sourcing and scope 2 reporting. These risks touch operations, finance, legal, sustainability, and corporate strategy at the same time. For some companies, locally managed or functionally siloed energy decisions may no longer match the scale of the exposure.

One driver may receive greater emphasis than the others, depending on a company’s competitive position and broader strategy, but the challenge is to balance all of them intentionally. A strategy that lowers cost but constrains future growth may be too narrow. A strategy that secures capacity but ignores resilience or contract exposure may be incomplete. Enterprise energy strategy becomes a source of competitive differentiation when leadership treats growth, cost, and risk as one management problem rather than three separate conversations.

Enterprise energy strategy in practice

Some companies are already moving to take greater control of their energy futures. Prominent examples are in the artificial intelligence and data center space, where the seemingly insatiable need for power is driving innovation and new approaches to energy generation and management. Google has developed a variety of strategies for powering its data centers. These include a contract with Xcel Energy to bring two gigawatts of clean power online.14 It’s also funding net-new off-the-grid natural gas generation in Texas15 and supporting a deal to bring an Iowa nuclear power plant back online.16 Rather than relying solely on utilities, hyperscalers are increasingly steering generation development and structuring supply to match expansion timelines, an example of how company growth plans are shaping—and being shaped by—energy considerations.

Some companies are also using energy strategy to manage cost and risk through deeper value chain collaboration. The recent renewable energy partnership between Mars and one of its major suppliers, Cargill, demonstrates how organizations are extending beyond their own operations to influence supplier energy use, pooling demand and structuring procurement to achieve both energy transition and economic outcomes.17

Enterprise energy strategy can also mean going beyond being a power consumer and instead thinking about energy as an asset class that can provide flexibility and resilience—but might also open up avenues for new revenue generation.

An energy readiness check for leaders

Leadership can start to look at how energy is strategic for different customers, assets, and parts of the operating footprint. For new large-load growth, energy may be a gating factor: power availability, interconnection timelines, grid capacity, tariff design, and supply options can influence where and how expansion occurs. For existing operations, the priority may be different: maintaining reliability and affordability, improving resilience, reducing avoidable consumption, and managing exposure to outages, rate changes, and long-term commitments. In some portfolios, these issues coexist, but they do not affect every site, customer class, or region in the same way.

A starting point is to understand the exposure clearly: Where is energy a growth constraint, where is it a cost or resilience issue, and where can it create a reporting or contracting risk? From there, a more focused set of management questions should be considered.

- Is there an enterprise energy strategy, or a collection of local and functional decisions?

- Is ownership clear at the executive level, including who has authority to make trade-offs among cost, resilience, decarbonization, and speed to market?

- When are energy considerations integrated into capital planning, footprint decisions, and site selection? Should they be integrated earlier?

- Does leadership have sufficient data to understand the financial effects of volatility, outages, tariff exposure, long-term supply commitments, and claims risk?

- What exposure or investment thresholds should trigger executive committee or board visibility?

From here, leaders can define the specific outcomes they are optimizing for—growth, cost, and risk—and in what combination. Assuming power will be available, reliable, and affordable appears to be a weaker planning premise. Energy strategy should become a standing input to enterprise planning, with named ownership, risk metrics, data visibility, and capital-allocation rules. Companies that build those mechanisms early can shape energy outcomes rather than simply respond to constraints.

By

John Mennel

Geoff Tuff

Robert Bui

Mitchell Cook

The authors would like to thank Derek Pankratz, David Novak, Nirmal Kujur, Aditi Vashishtha, and Alura Vincent for their help in developing this article.

Editorial (including production and copyediting): Elizabeth Ryan, Rithu Thomas, Shyamili M, Pubali Dey, and Anu Augustine

Design: Harry Wedel, Molly Piersol, and Pooja Lnu

Cover image by: Pooja Lnu

Knowledge services: Agni Wagh

Visit the Deloitte Center for Integrated Research

Access more insights on some of the most complex issues facing businesses today.