Implications of the Middle East conflict for the US economy

Higher oil prices may weigh on US consumers and economic growth even as energy firms and AI investments show resilience

The conflict in the Middle East is expected to slow US economic growth relative to a no-conflict scenario. While this may seem counterintuitive, given the United States is the world’s largest oil producer, higher oil prices are often transferred from consumers back to producers, and the net effect on economic growth tends to be mostly negative.

Yes, US shale producers may ultimately increase investments to drive higher production—anecdotal evidence suggests some are already doing so. But there is no evidence of this in the US oil-rig count data yet.1 It’s likely that most shale producers require more assurance that oil prices will remain elevated for an extended period of time, before ramping up investment significantly.2

Other beneficiaries of higher oil prices would comprise individuals who own stock in oil-production companies. As of the time of writing, energy companies in the S&P 1500 added roughly US$475 billion in market capitalization since the start of 2026. Although composite US stock indices fell in the early days of the conflict, they have since recovered those losses and some.3 This suggests that consumers who are sensitive to financial-market fluctuations, such as those at the top of income and wealth distributions, may no longer be experiencing a negative wealth effect, which would otherwise drag consumer spending.

Still, consumers bear the largest negative impact as higher oil prices quickly translate into higher gasoline prices: Every 20% gain in crude-oil prices is estimated to directly raise inflation by roughly 0.3 percentage points.4 This excludes secondary effects of higher input costs—such as higher prices for transportation, food, and airfare—which can amplify inflation further.

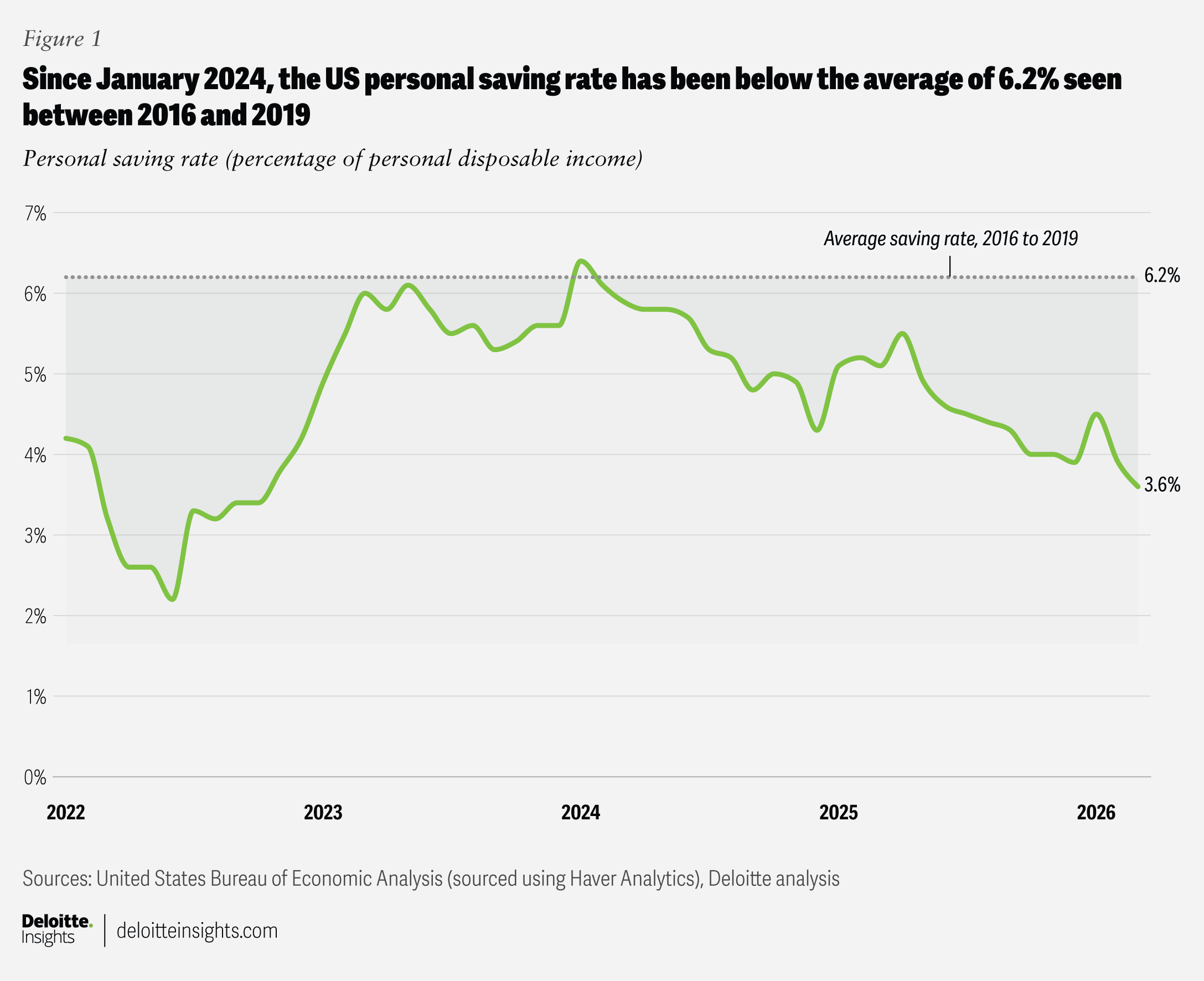

Households may initially absorb higher gas prices by reducing their rate of saving rather than consumption. However, this buffer appears to be limited. The US personal saving rate, which measures the percentage of income that people save after taxes, was already low prior to the conflict, which raises the probability of consumers lowering spending to accommodate higher gas prices. For reference, the saving rate in February was 4%—well below the average of 6.2% recorded between 2016 and 2019 (figure 1).5

In addition, rising health insurance premium costs are weighing on household budgets, with more than 1 million people opting out of Affordable Care Act marketplace insurance plans, altogether.6 On the plus side, higher tax refunds may offer a buffer against energy and health insurance price shocks.7

To illustrate the macro impact, consider that the price of oil was roughly 50% higher between December 2025 and April 2026, even after the announcement of a temporary ceasefire. If the conflict were to persist for a year, inflation would likely rise by at least 0.75 percentage points. Assuming consumers do not reduce their savings further, real consumer spending would fall by the same magnitude.8 If second-round effects are added, some estimates show inflation could be a lot higher.9 In our most recent US economic forecast, we had estimated real consumer spending would grow by 2.1% in 2026 and just 1.7% in 2027.10 Using the same assumptions, US consumer spending growth could dip below 1%.

There are other effects as well that could restrain economic growth, notably the rise in interest rates following the oil price spike. Higher rates weigh on interest-sensitive sectors such as durable goods consumption, housing, and residential investment by raising the cost of debt servicing. Business investment will likely also face headwinds from higher interest rates and a more cautious consumer.

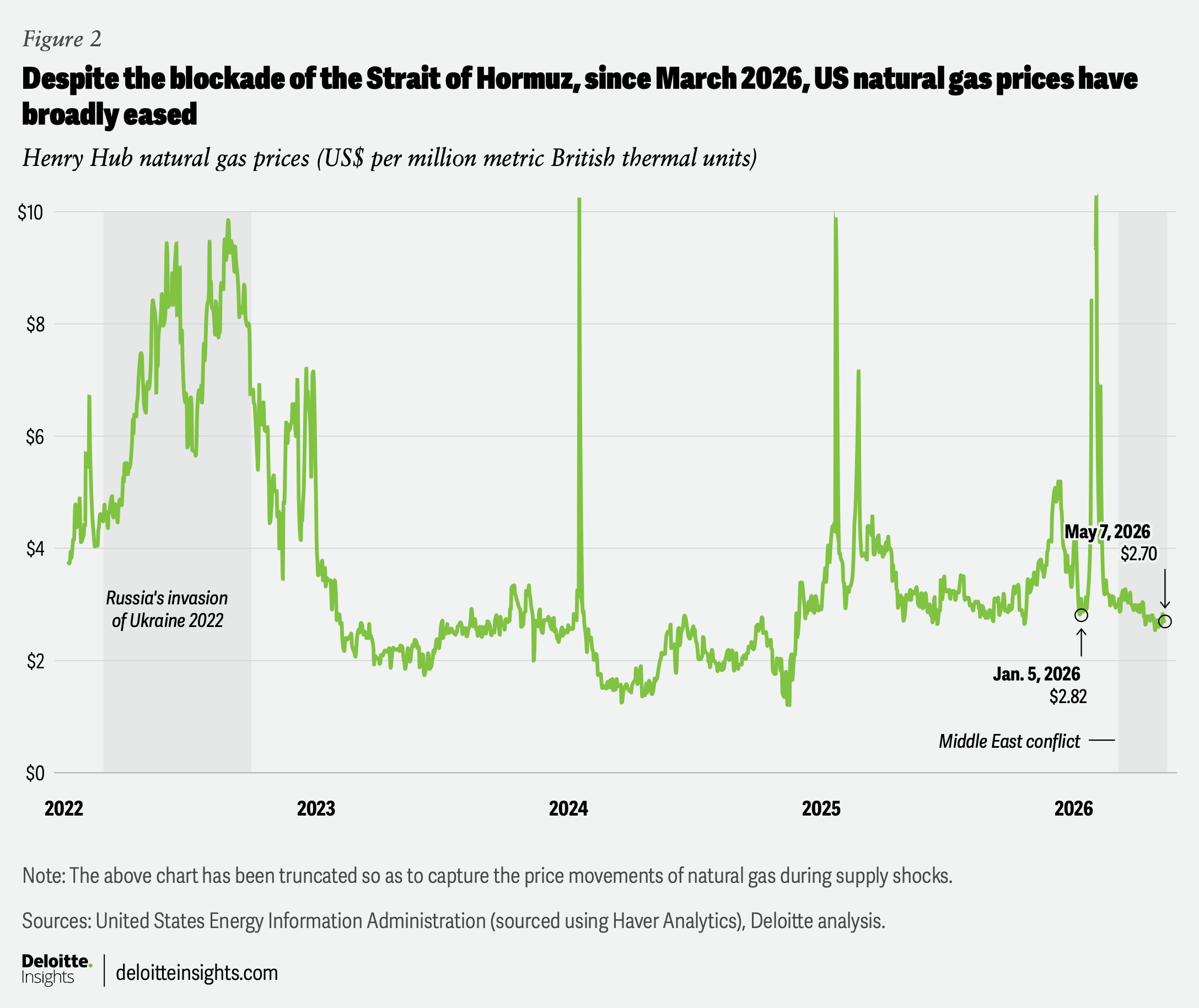

It is important to note that not all energy-intensive businesses in the United States will face much higher costs, however. US natural gas prices have not spiked since the conflict began, limiting upward pressure on electricity costs, given natural gas is one of the biggest inputs for electricity in the United States. This is critically important for energy-intensive sectors such as data centers.

In our most recent US economic forecast, we had anticipated that AI-related investments would drive overall business investment growth both in 2026 and 2027. These investments appear to be relatively insulated from near-term macroeconomic factors. Artificial intelligence is a new technology, and there is a perception that the winner of the AI race may capture a disproportionate share of the gains. Hence, firms are unlikely to scale back investment materially due to the conflict in the Middle East. If anything, it seems more likely that there could be more related investments in the United States, given the relative stability of electricity prices and security of data centers and other infrastructure compared to locations closer to Iran.

The final channel of weakness is through exports: Unlike the United States, Europe and Asia are facing much higher gasoline and natural gas prices, which will limit economic growth. This, combined with a stronger US dollar,11 will slow exports. However, the silver lining is that the relatively small role of exports in the US economy will limit the drag on overall growth.

By

Michael Wolf

Rohini Sanyal

Editorial (including production and copyediting): Arpan Kumar Saha, Preetha Devan, Shyamili, and Pubali Dey

Design: Harry Wedel and Natalie Pfaff

Audience development: Maria Martin Cirujano

Cover image by: Harry Wedel

Knowledge services: Agni Wagh

Visit the Deloitte Global Economics Research Center

Access more insights for the consumer spending, housing, business investment, globalization & international trade, fiscal & monetary policy, sustainability, equity, & climate, labor markets and prices & inflation sectors.