CEO compass: Deloitte Global’s 2026 Airline CEO Survey

Steady hands, far horizons: Airline CEOs are managing the moment while positioning for the competitive landscape ahead

Introducing our CEO survey findings

Dear aviation colleagues,

It is our pleasure to share Deloitte Global’s 2026 Airline CEO Survey. Drawing on insights from chief executive officers around the globe, this report captures how airline leaders are navigating one of the most challenging operating environments in recent memory.

The survey was fielded as the impact of the Iran conflict was rippling through fuel markets, airline P&Ls, and network plans. What emerged was not panic—but focus. CEOs are tightening their grip on costs, sharpening their use of technology, and rethinking what they need from their organizations and their leaders. The defensive instinct is strong, and in many ways appropriate. But within these findings, there are also signals of something more forward-looking—airlines beginning to position not just for operational continuity, but for what comes after.

Throughout this report, you’ll find an industry recalibrating in real time—balancing the urgency of today’s cost pressures against the strategic investments that will define tomorrow’s competitive landscape. From AI’s rapid rise to the evolving sustainability agenda to the leadership traits this moment demands, these findings offer a window into how the industry’s most senior leaders are thinking about what’s next.

We extend our gratitude to the CEOs who shared their time and perspectives, and to you for your continued engagement.

Sincerely,

Yvonne Rene de Cotret

Global transportation, hospitality and services sector leader

Deloitte Global

The airline industry entered 2026 with real momentum. Early projections pointed to record passenger volumes, all-time high load factors, and US$41 billion in global net profit for the year.1 By mid-year, that optimism feels like a distant memory.

Fuel costs have surged, inflation continues to push up labor and maintenance expenses, and aircraft delivery delays are keeping older, costlier fleets in the air longer than planned.2 Together, they’ve turned what was supposed to be a record year into a fight for margin. Industry-defining shocks have become a familiar pattern, and for airline CEOs, managing through disruption is no longer an occasional challenge; it’s the job.

That reality comes through clearly in this year’s survey of 21 airline CEOs (see methodology). Airline CEOs are pulling toward financial discipline, and it’s not a subtle shift. Cost control has become the organizing principle for nearly every strategic decision, from how airlines grow to how they invest in technology to what they ask of their workforce. The aspirational priorities of recent years—customer experience, innovation, culture—haven’t disappeared, but they’re being weighed against a harder question: Does it protect margin?

In an environment this unforgiving, that instinct may be the right one. But the airlines that have historically emerged strongest from periods of disruption aren’t the ones that only played defense; they’re the ones that found ways to invest and reposition while others retrenched. Competitive landscapes don’t get redrawn after a crisis. They get redrawn during one. This report explores how CEOs are navigating that tension, protecting the airline today while building the foundation for what comes next.

From macro risk to margin pressure

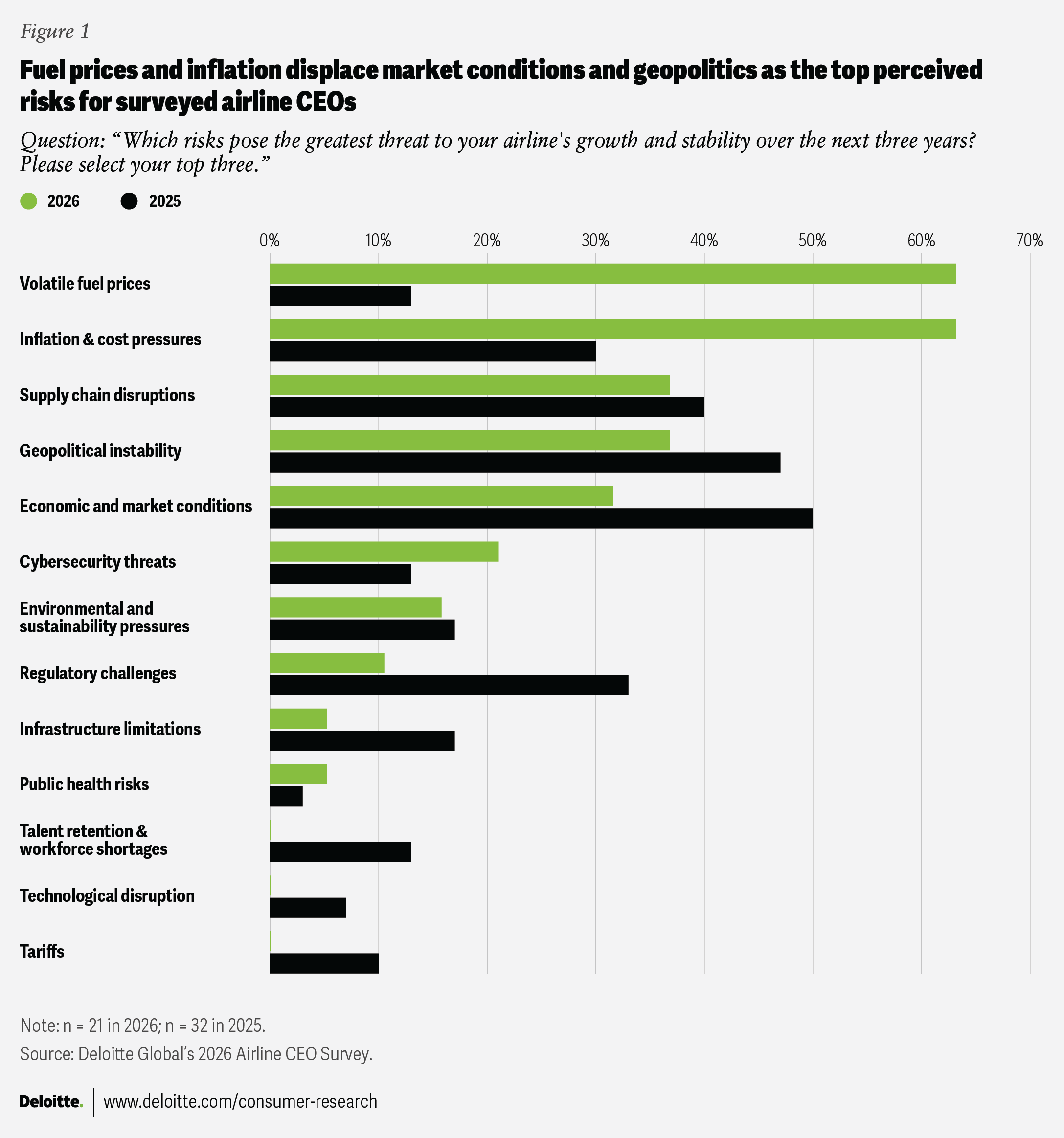

The cost pressures are not theoretical. Major carriers are cutting capacity, slashing profit forecasts, and raising fares in direct response to a fuel environment that has deteriorated since the start of the year.3 Fuel price volatility and inflation now sit at the top of the risk agenda—both surging dramatically from last year (figure 1). Meanwhile, last year’s top concerns—economic conditions and geopolitical instability—have fallen.

Table of Contents

- From macro risk to margin pressure

- Making existing capacity pay

- Technology as the efficiency engine

- CEOs get pragmatic about sustainability

- Leading through headwinds

{kind=link}

The drop in geopolitical concern may seem counterintuitive given ongoing global conflicts. But the challenges haven’t faded; they’ve likely been overtaken by cost pressures that demand attention now. And after years of rolling crises, there may be something more fundamental at play: disruption simply what the industry has come to expect.

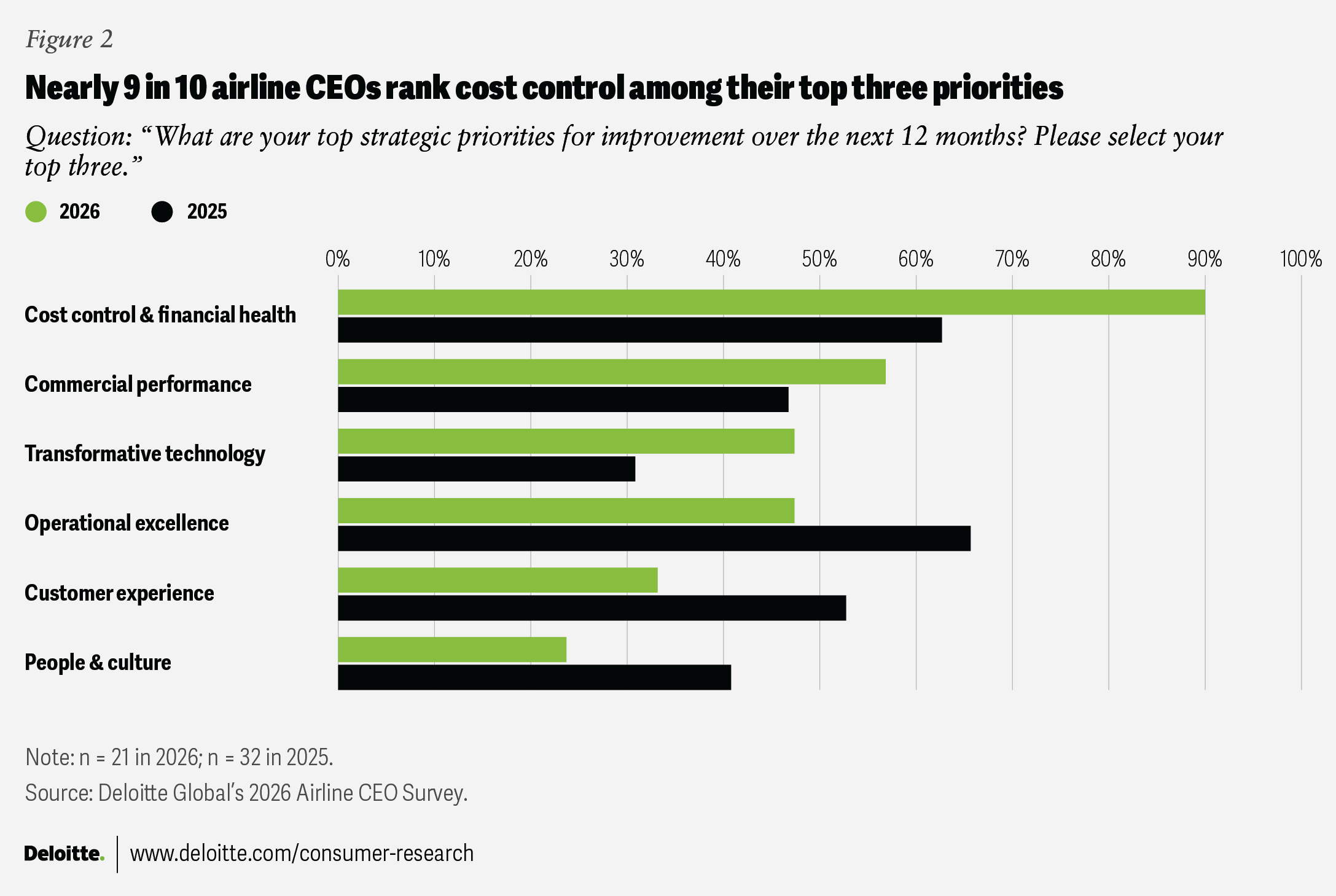

The strategic response is unambiguous. Cost control & financial health has surged to the top of the agenda, and no other priority comes close (figure 2). The scale of the shift signals something beyond a routine reprioritization; it reflects an industry in a defining cost moment, and one where financial discipline is likely the thread running through every decision CEOs are making right now.

{kind=link}

In tandem with this focus on cost control comes a renewed emphasis on transformative technology. Last year it ranked last among strategic priorities; this year it’s tied for third. The rise isn’t coincidental. In an environment this focused on margin, technology is being valued less as an innovation engine and more as a means to help drive efficiency, sharpen pricing, and take cost out of the operation. Later sections bear this out.

What’s falling is just as telling. Customer experience, and people & culture—both high priorities last year—have dropped. That doesn’t mean they’ve been abandoned. But in an environment so focused on margin, the priorities that feel less immediately tied to financial survival are the ones giving way.

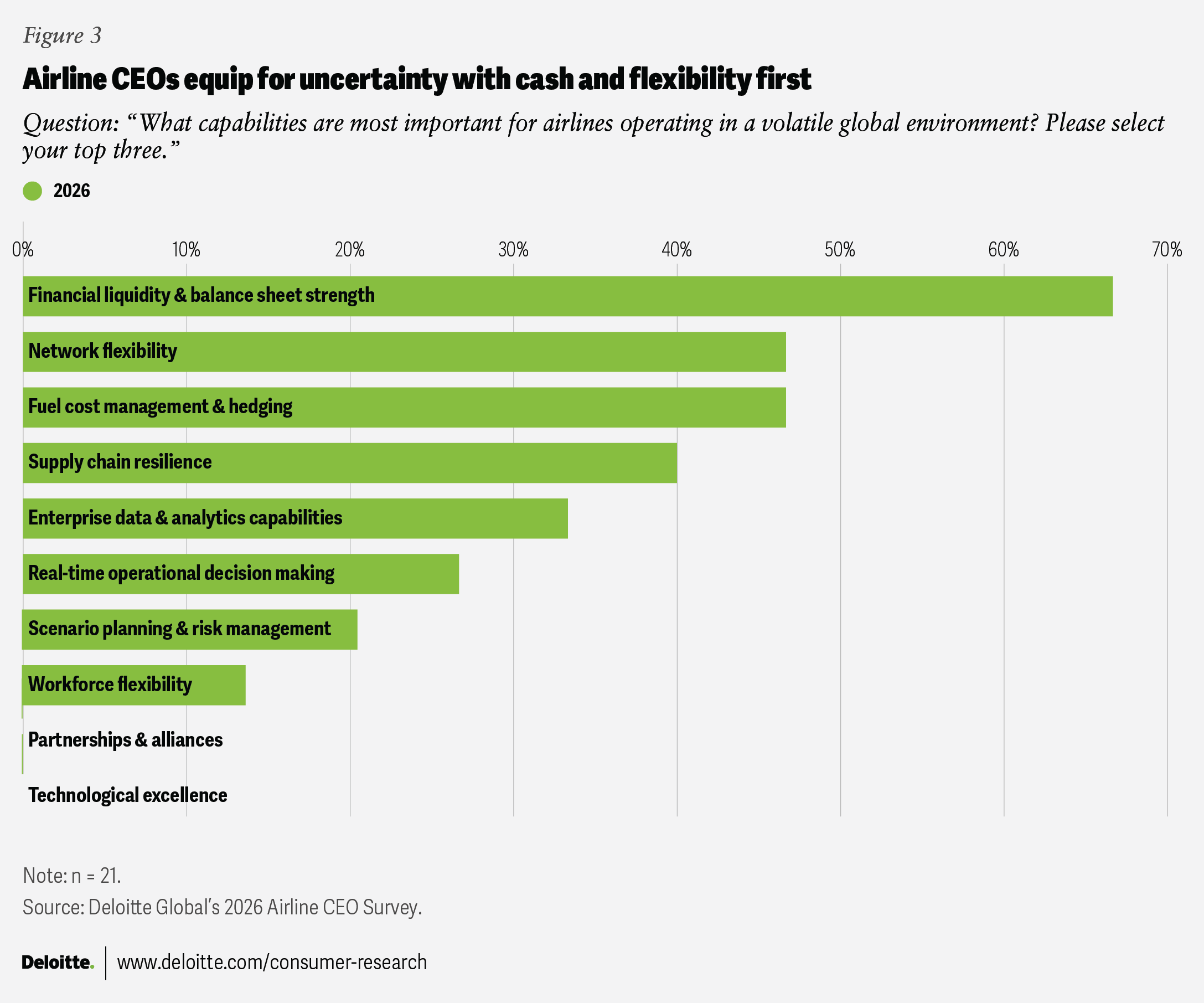

The defensive instinct runs deeper than strategic priorities. When asked what capabilities matter most in a volatile environment, CEOs reach for the most basic lever: cash. Liquidity and balance sheet strength leads the list—well ahead of scenario planning, data capabilities, and workforce flexibility (figure 3). In a crisis this immediate, the playbook is operational continuity first—a posture built for absorption, not prediction.

{kind=link}

Making existing capacity pay

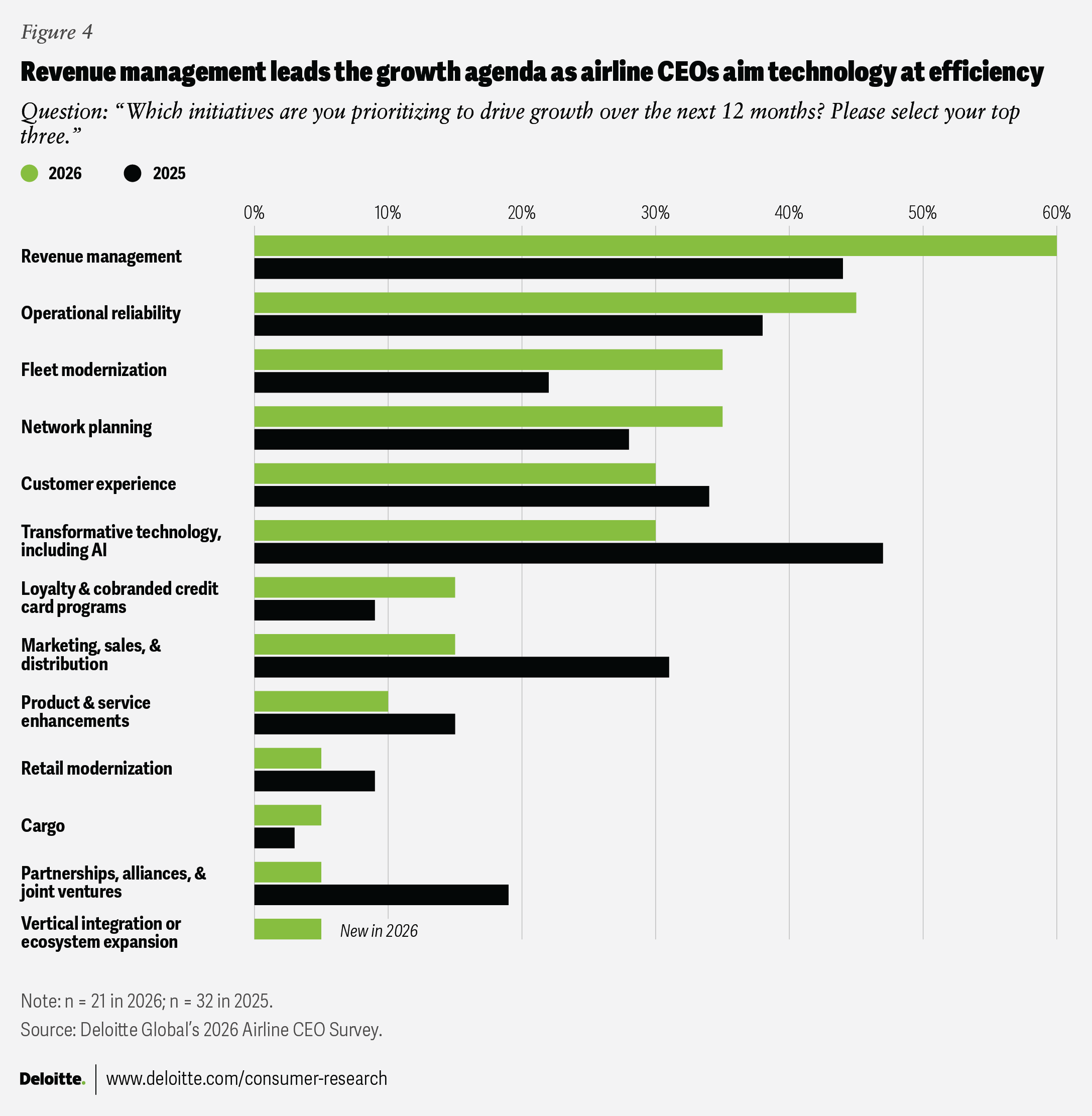

With margins under pressure and over 5,300 aircraft deliveries delayed, airlines are largely working with the capacity they have—and need to make it pay.4 That reality is reshaping how CEOs think about growth. The emphasis has shifted from expansion to extraction, getting more value from existing routes, existing aircraft, and existing operations.

Revenue management now leads the growth agenda, rising from last year (figure 4). It’s the most capital-efficient growth lever available: no new planes, no new routes, no new hires—just better pricing, better segmentation, and better yield from every seat that’s already flying. Longer-cycle investments like partnerships and marketing fell, while technology dropped as a standalone growth initiative, increasingly being aimed at efficiency rather than growth for its own sake.

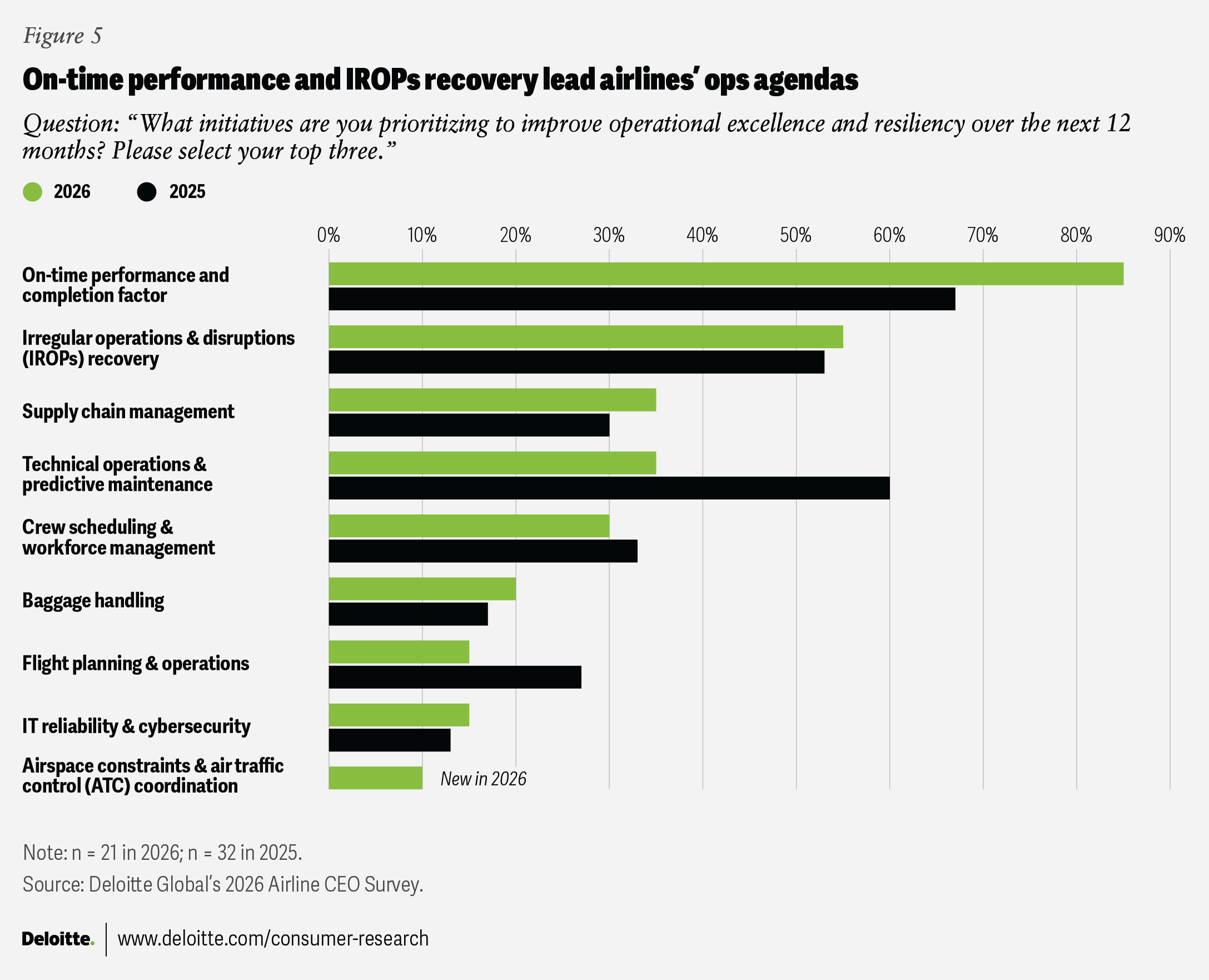

The same logic can extend to operations. On-time performance surged to the top of the operational agenda, with irregular operations and disruptions (IROPs) recovery close behind (figure 5). CEOs are focused on the metrics that passengers and regulators see most directly—and that can carry financial consequences when they slip. Technical operations, last year’s second-highest priority, dropped sharply. The likely explanation: the industry’s post-pandemic maintenance, repair, and overhaul catch-up cycle has largely run its course, freeing attention to shift toward schedule discipline and disruption recovery.5

{kind=link}

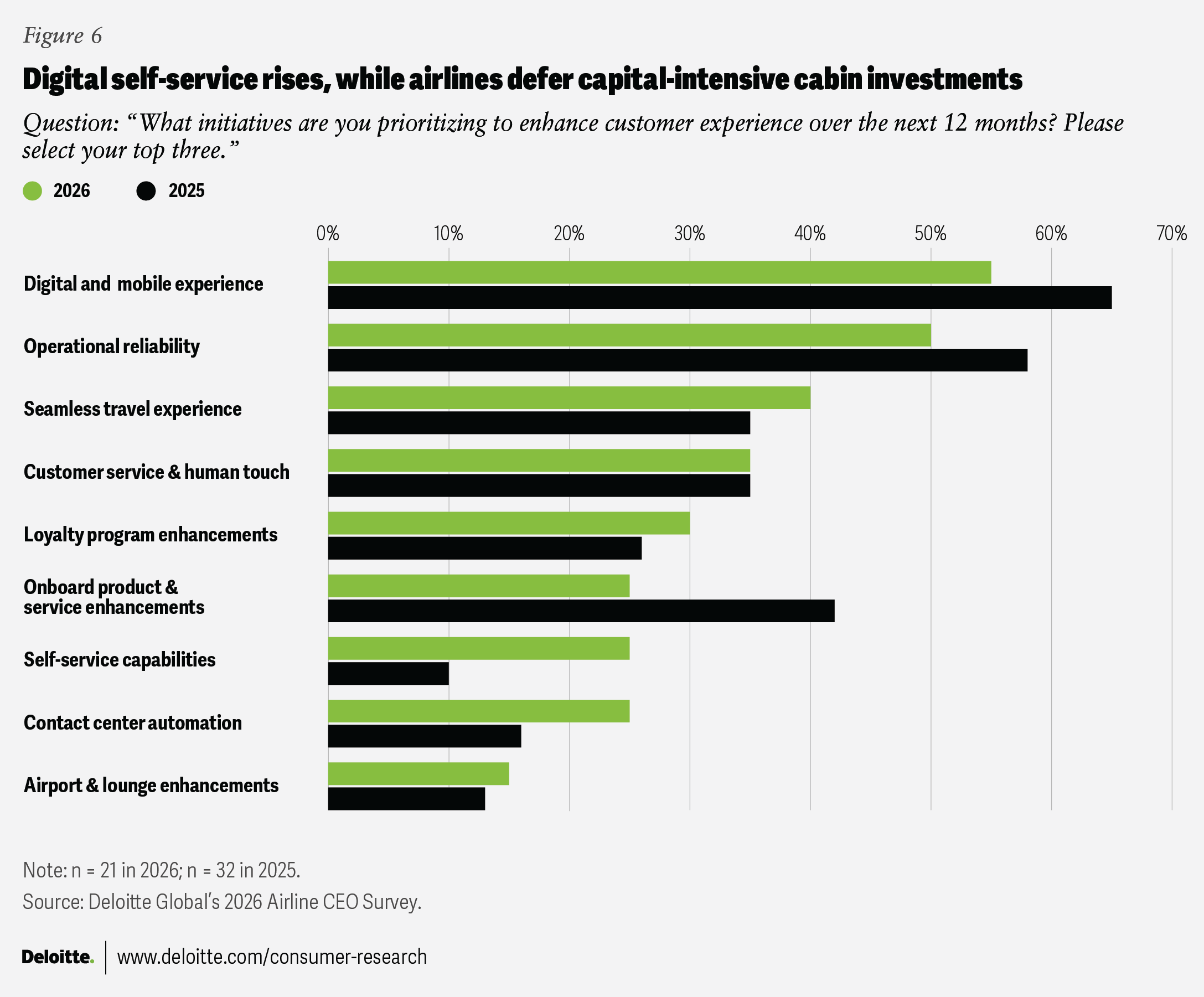

Even within customer experience (itself a declining strategic priority) CEOs are making choices that reflect the cost environment. Digital and mobile experience and operational reliability hold firm at the top. They’re baseline expectations at this point, not differentiators. But beneath that, the agenda is splitting. Self-service capabilities and contact center automation are gaining ground—investments that improve the passenger experience while simultaneously deflecting cost. Onboard product enhancements, often capital-intensive, saw one of the sharpest drops in the survey (figure 6). For airlines willing to invest where others pull back, that gap could become a source of competitive separation.

{kind=link}

There may be an intuition at work. Deloitte research across 1,250 European travelers found that what passengers increasingly value aligns with where CEOs are placing their bets: Digital basics like in-app flight alerts, mobile boarding passes, and transparent pricing matter far more to purchase decisions than loyalty perks or cabin amenities.6 But the larger point is strategic: Customer experience shouldn’t be a trade-off against financial discipline; it should be a lever for it. Digital-first carriers are already trimming 1 to 2 margin points from costs while adding $5 to $10 in ancillary revenue per passenger.7 The airlines treating customer experience as a cost to manage rather than a capability to build may find themselves falling behind carriers that recognized the connection earlier. In customer experience, as in so many areas right now, delay is the most expensive option.

Technology as the efficiency engine

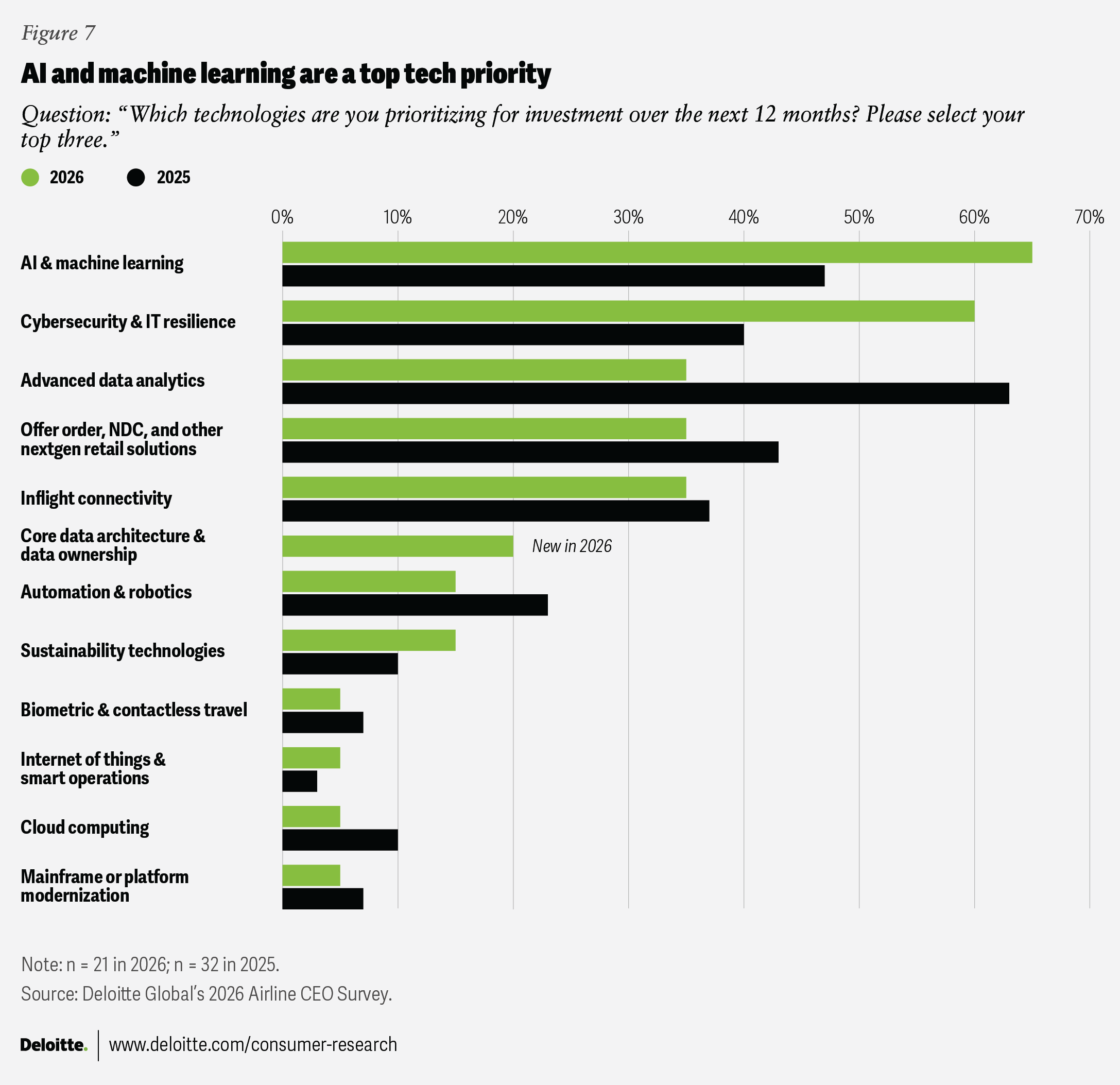

AI is no longer a debate for airlines. It’s become a priority. Not as a future bet or a boardroom talking point, but as the central technology priority for an industry under pressure. In just one year, AI & machine learning has gone from trailing data analytics to leading the technology investment agenda, and it represents one of the few areas where CEOs are leaning forward, not just playing defense (figure 7).

{kind=link}

The sharp decline in advanced data analytics doesn’t signal a loss of confidence. For many airlines, the foundational data work is far enough along that the conversation has moved to putting AI to work on top of it. Others, as later findings show, are still managing the legacy infrastructure that can make that leap difficult. Cybersecurity’s parallel rise reflects the other side of the equation: As digital capabilities expand, so does the imperative to protect them.

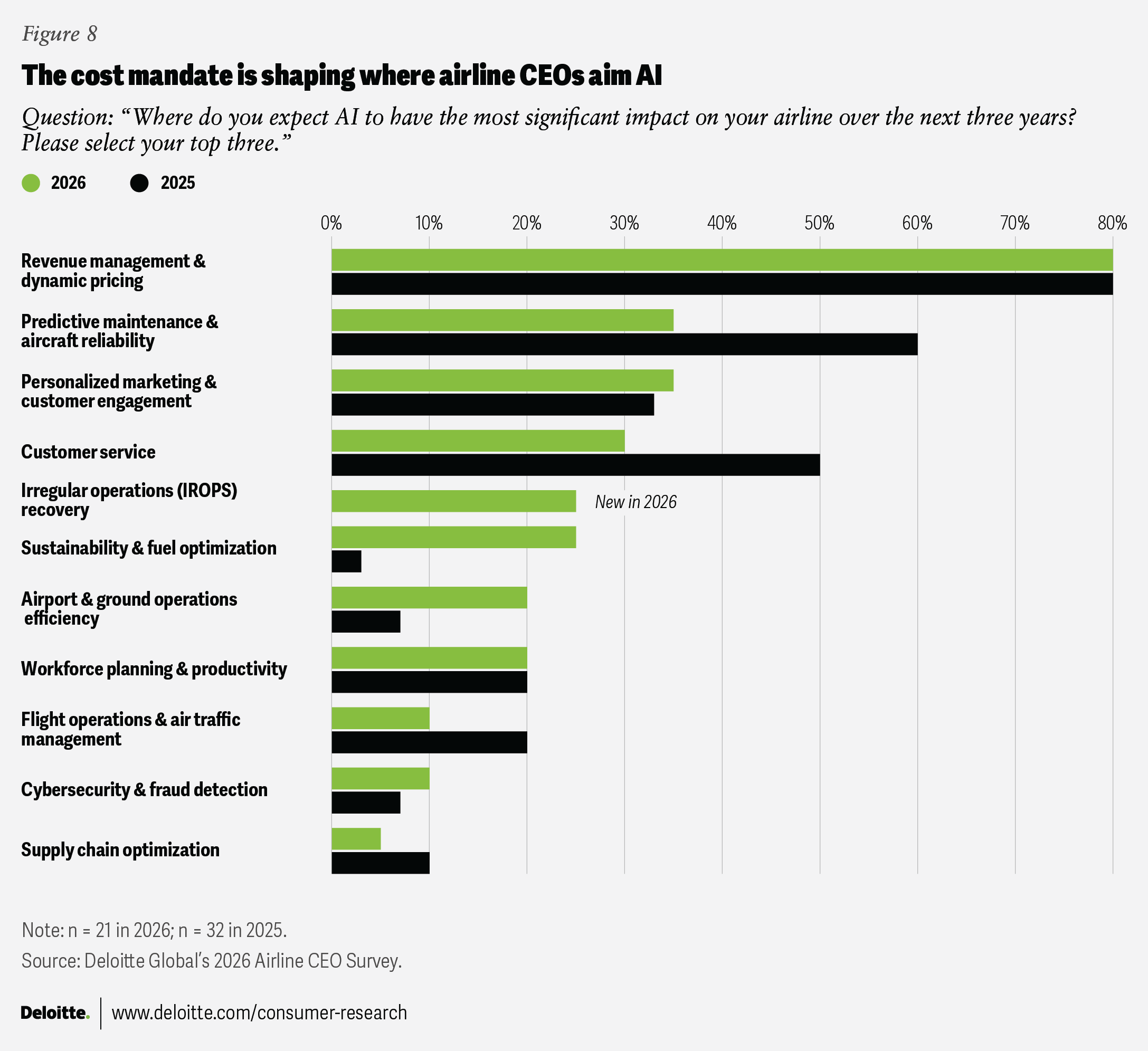

Revenue management & dynamic pricing has led as AI’s top use case for two consecutive years, at over 80% (figure 8). That consistency signals traction—and in the current environment, it’s no coincidence that the dominant use case is the one most directly tied to margin. Pricing optimization is measurable, immediate, and proven. AI’s first act in aviation is clear.

{kind=link}

The cost mandate is visible in other AI use cases gaining ground: sustainability & fuel optimization and airport & ground operations efficiency. The ones losing ground (predictive maintenance and customer service) are more closely tied to quality and reliability. That doesn’t mean CEOs don’t see the opportunity in those areas. It’s that in a moment focused on margin, the use cases that survive the prioritization are the ones closest to the cost line.

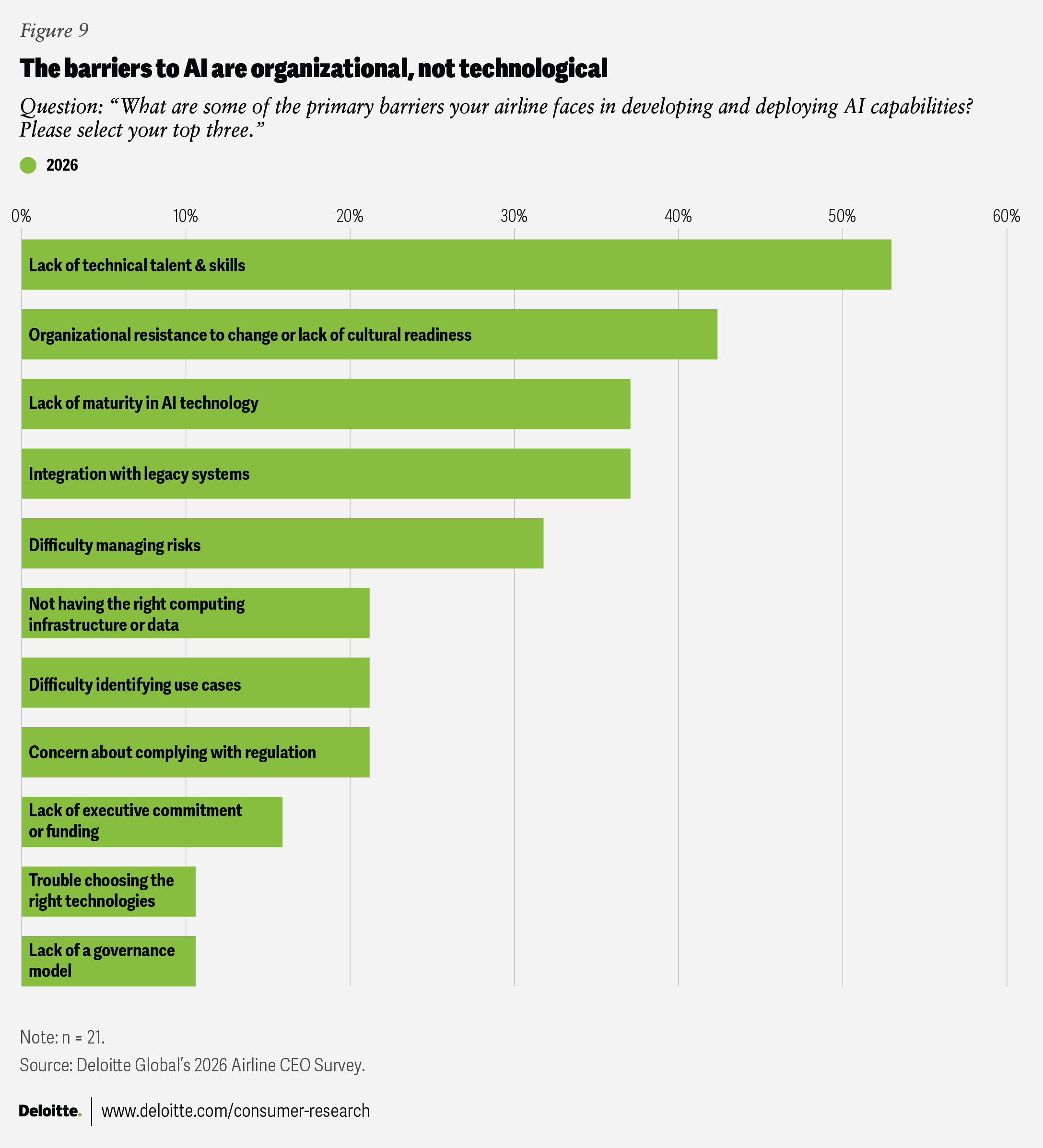

If the appetite for AI is clear, so are the obstacles. The barriers CEOs cite are not about the technology itself, nor about executive commitment or funding—both rank near the bottom (figure 9). The real friction is organizational: talent shortages, cultural resistance to change, and the difficulty of integrating AI into legacy systems. The C-suite is bought in. The challenge is pushing AI through the layers of the organization where it actually has to work.

{kind=link}

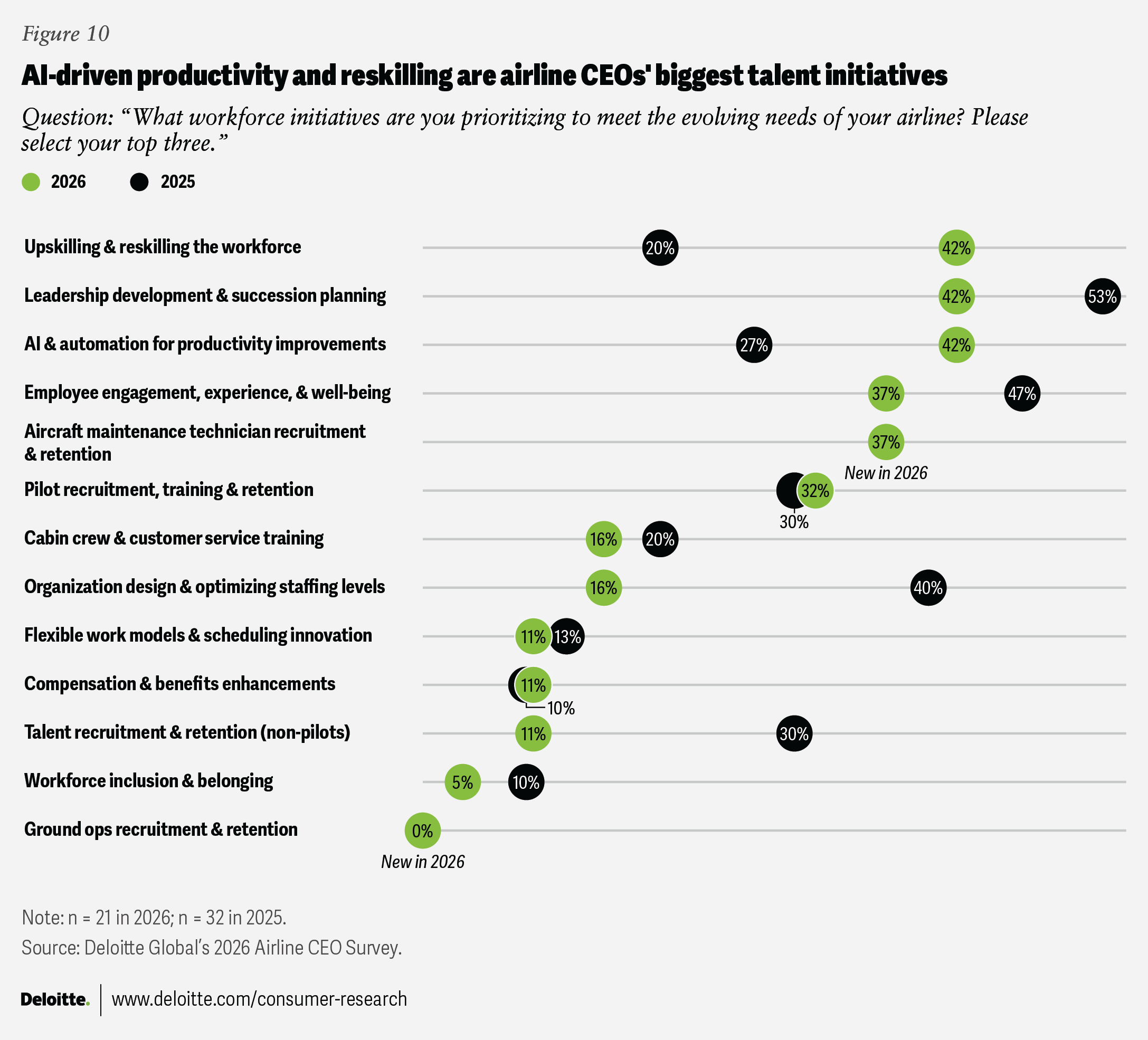

The surest sign of AI’s ascent may not be in the technology itself—but how it’s shaping the broader workforce agenda. AI-driven productivity tools and upskilling/reskilling are this year’s biggest talent initiatives—two sides of the same coin: deploying the tools and preparing the people to use them (figure 10).

Meanwhile, organization design and non-pilot recruitment both fell, suggesting the post-pandemic right-sizing and rehiring cycles are largely complete and that current capacity rationalization may be easing near-term workforce pressure. It’s no longer about whether airlines have enough people. It’s about whether their people can do what’s coming next. Human-machine collaboration—the premise at the heart of future-of-work conversations for the past decade—may be starting to show up in how airlines build their teams.

{kind=link}

What this year’s data makes clear is the sheer breadth of AI’s potential footprint in aviation. Across revenue management, fuel optimization, ground operations, disruption recovery, customer service, and workforce productivity, CEOs are identifying AI applications that touch virtually every dimension of the business. Most airlines are still capturing value in only one or two of those areas. The gap between where AI is delivering today and where it could is a measure of the opportunity ahead.

The airlines closing that gap fastest share a common trait: They’ve connected AI to specific business outcomes from the start. Rather than pursuing AI as a capability-building exercise, they’ve worked backward from the P&L—identifying where margin is being lost, where inefficiency compounds, and where automation can deliver measurable returns. For carriers still wrestling with legacy infrastructure and talent gaps, that discipline likely matters even more. The business case has to lead; the technology follows.

The next frontier is already in view. AI systems that don’t just recommend but act—adjusting pricing in real time, rerouting networks autonomously during disruptions, initiating maintenance actions before a human flags the need. The shift from advisory AI to Agentic AI won’t happen overnight, but for an industry generating this volume of operational data under this level of cost pressure, the economics of autonomous decision-making are becoming hard to ignore.

CEOs get pragmatic about sustainability

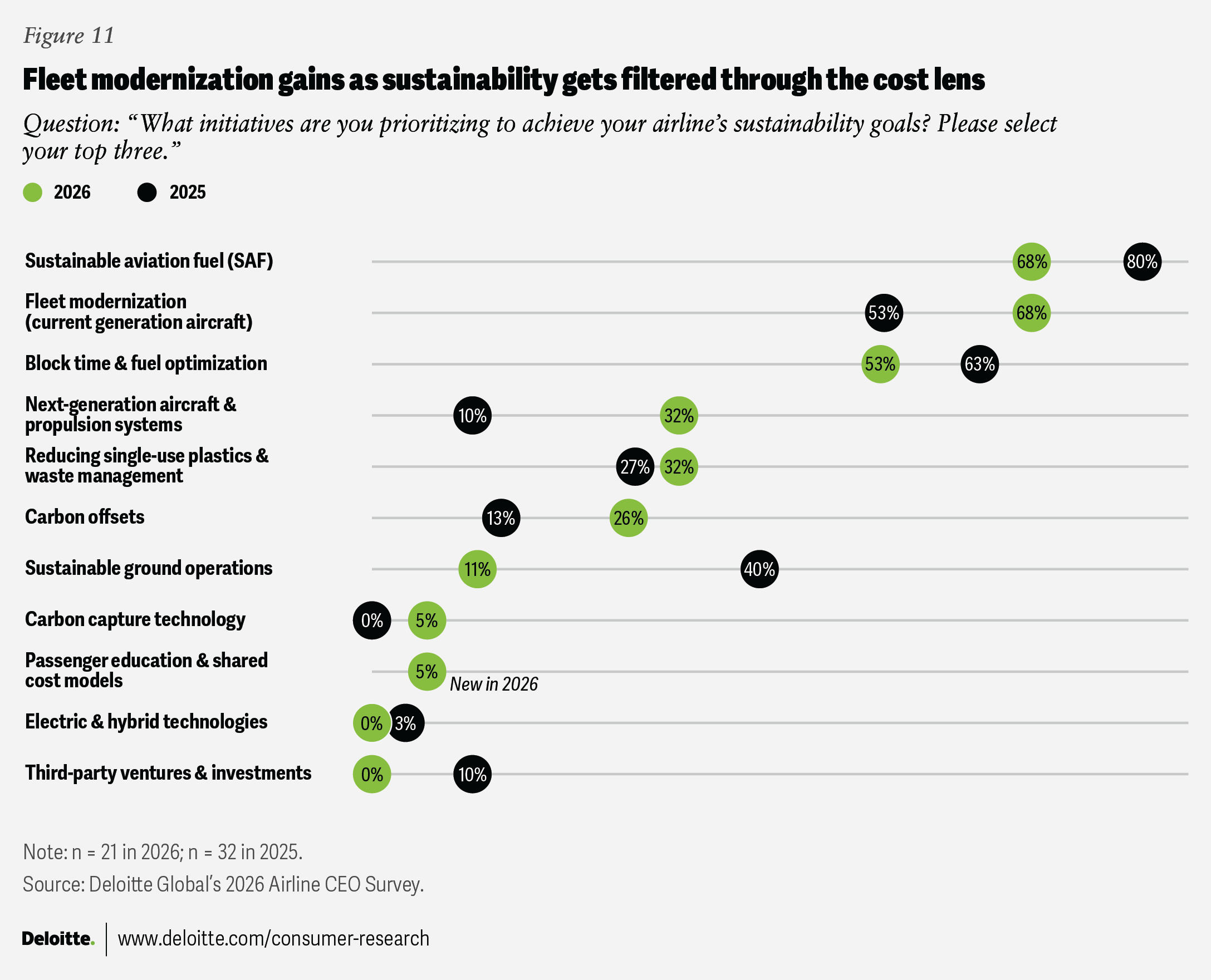

Sustainability hasn’t left the CEO agenda, but it’s being run through the same cost filter as everything else. With sustainable aviation fuel (SAF) historically priced at two to five times conventional jet fuel—a gap that may be narrowing as fuel prices rise—and the appetite for long-horizon bets cooling, CEOs are concentrating on the sustainability levers that also deliver financial returns.8

Fleet modernization (both current-generation and next-generation propulsion) saw the biggest gains from last year (figure 11). That’s no surprise given the fuel environment. With over 5,300 aircraft deliveries delayed and the global fleet operating roughly two years older than the historical norm, airlines are flying less efficient aircraft at precisely the moment fuel costs have surged.9 The urgency to modernize hasn’t been dampened by delivery delays; it’s been sharpened by them. Every older aircraft in service is a compounding cost problem that adds urgency to the fleet renewal conversation.

{kind=link}

Sustainable ground operations, by contrast, dropped sharply. The pattern is consistent: CEOs are gravitating toward the levers with the largest emissions impact and the most direct operational payoff, and pulling back from smaller-scale initiatives that are harder to justify when every dollar is being scrutinized.

SAF remains central, but its decline from last year’s dominant position may reflect a growing realism about supply constraints, feedstock limitations, and the cost of scaling production. Carbon offsets rose, potentially serving as a near-term bridge while airlines wait for fleet deliveries and SAF supply to catch up.

Leading through headwinds

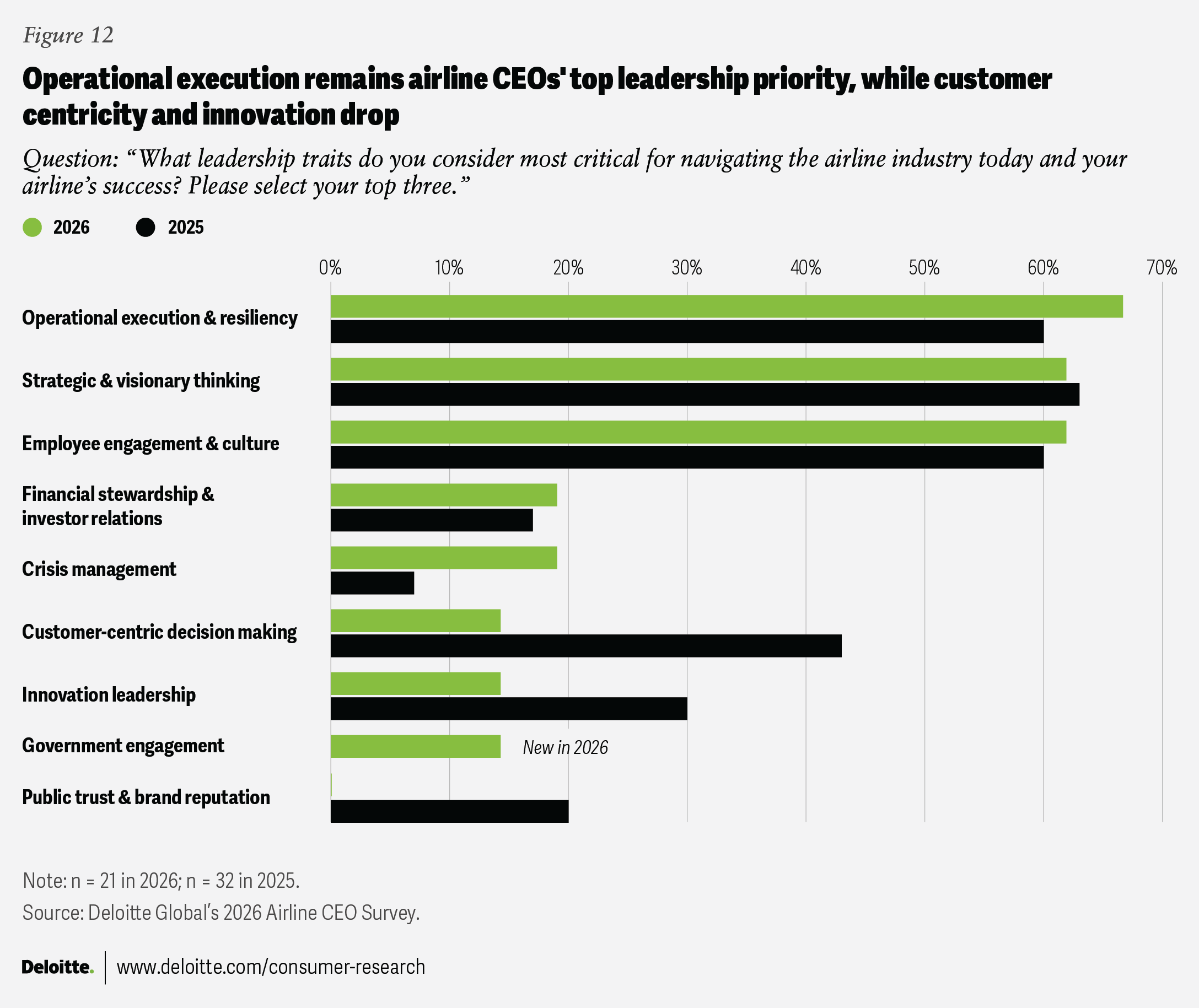

Every environment produces the leadership profile it demands. In this one, the traits CEOs value most are the ones that keep an airline running under pressure: operational execution, strategic thinking, and employee engagement, all holding firm at the top (figure 12).

What’s declining may matter more. Customer-centric decision making and innovation leadership both fell from last year. These aren’t fringe traits. They defined the aspirational, growth-era CEO. Their decline suggests something broader: The industry isn’t just adjusting its priorities. It’s adjusting what it asks of its leaders. Steadiness over vision. Delivery over inspiration.

That instinct—to protect, to tighten, to focus on what’s immediately in front of you—is understandable. In many ways it’s right. But if history offers any guide, the airlines that merely defend during a crisis rarely lead the recovery. Some of the industry’s most durable competitive advantages were built during downturns—carriers that locked in aircraft orders at steep discounts in the height of the great recession, or invested in technology infrastructure during the pandemic while others waited. Those bets didn’t just pay off in the recovery. They reshaped the competitive landscape years afterward.

The playbook isn’t defense or offense. It’s both sequenced deliberately. In the near term, protecting cash and managing costs is non-negotiable. But crises also create windows that may not stay open for long: competitors retreat from routes, airport slots come free, suppliers trade price for certainty, and corporate contracts become contestable. The airlines that move on those opportunities—while others are still retrenching—are the ones that exit the crisis in a structurally stronger position.

One of the most important leadership traits of this moment may not appear in the survey data at all. It’s the ability to hold two imperatives in tension—protecting the airline today while positioning it for what comes next. Defense can help keep you alive. It’s what you do alongside it that determines where you land.

Methodology

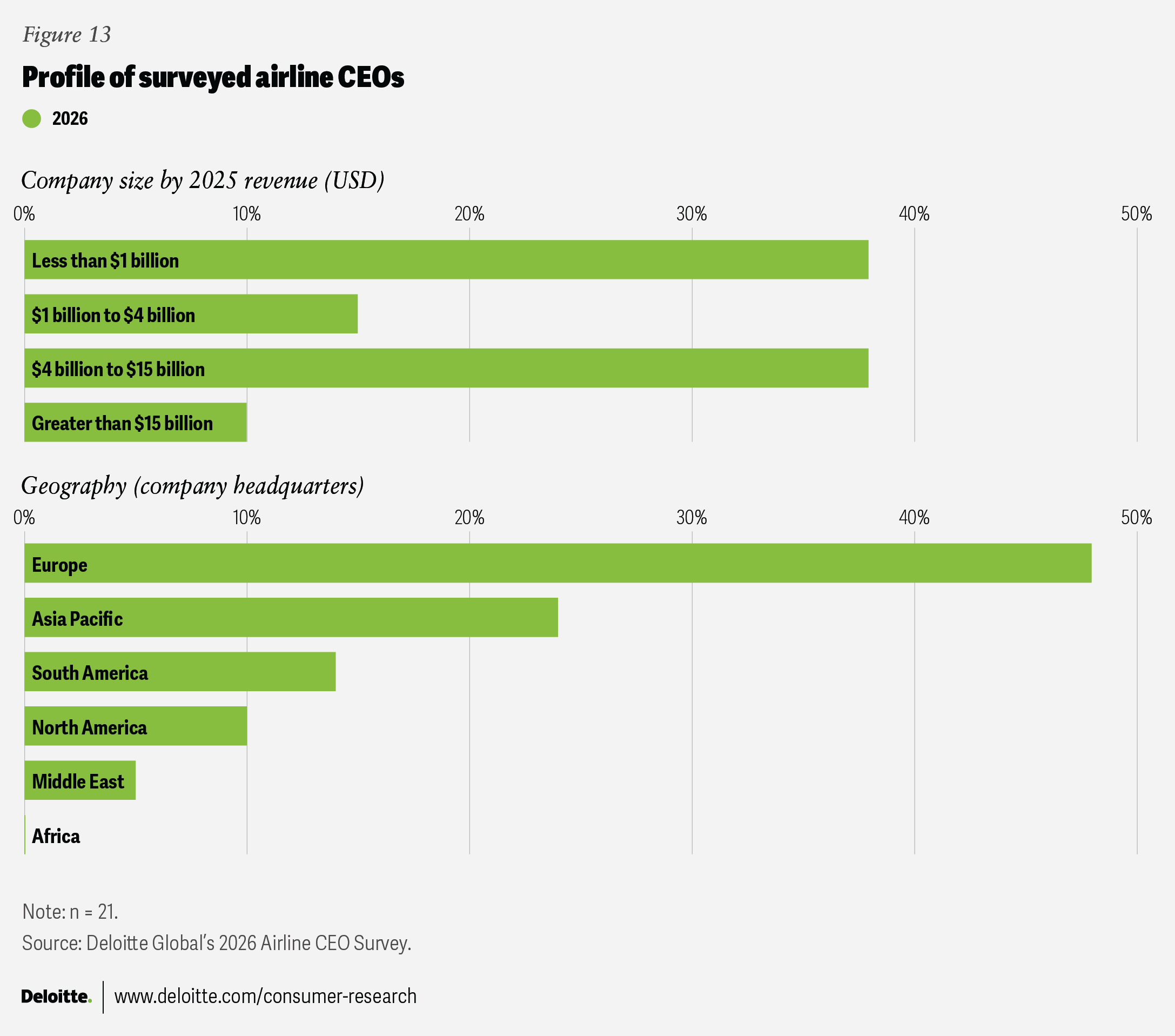

This survey was conducted by Deloitte Global’s Aviation group using an online questionnaire fielded from April to May 2026. Invitations were sent directly to airline CEOs and all responses are confidential. The participant group of 21 airline CEOs reflects a global mix of airline leaders representing a range of annual revenue sizes, geographic regions, and business models (figure 13). Responses reflect CEO sentiment at the time of fielding and represent the perspectives of participating airline leaders. They are not intended to be statistically representative of the global airline industry, but rather to capture the priorities, concerns, and strategic direction of a cross-section of its senior leadership. The 2025 survey included 32 participants.

Continue the conversation

Meet the industry leaders

Yvonne Rene de Cotret

Vicente Segura

by

Yvonne Rene de Cotret

Vicente Segura

Matt Soderberg

The authors would like to thank the following for their contributions to this article: Aloke Mukherjee, Canada aviation leader; Andy Gauld, UK aviation leader; Anurag Gupta, India aviation leader; Bird Ji, China aviation leader; Dejan Markovic, Central Europe aviation leader; Dorian Reece, Middle East aviation leader; Kaihei Torigoe, Japan aviation leader; Thomas Pellegrin, Asia-Pacific aviation leader; Marcello Gasdia, Maggie Rauch, Steve Rogers, June Ramos, and Albert Cagigos.

Editorial (including production and copyediting): Andy Bayiates, Annalyn Kurtz, Aparna Prusty, Preetha Devan, Anu Augustine, and Cintia Cheong

Design: Molly Piersel and Natalie Pfaff

Cover image by: Meena Sonar

Knowledge services: Agni Wagh

Visit the Deloitte Consumer Industry Center

Access more insights for the automotive, consumer products, food, retail, wholesale and distribution, airlines and hospitality, and transportation sectors.