Flight or fold: 2026 Deloitte Summer Travel Survey

Travel enthusiasm faces a new cost reality, keeping some home and compelling others to dig deeper into their pockets

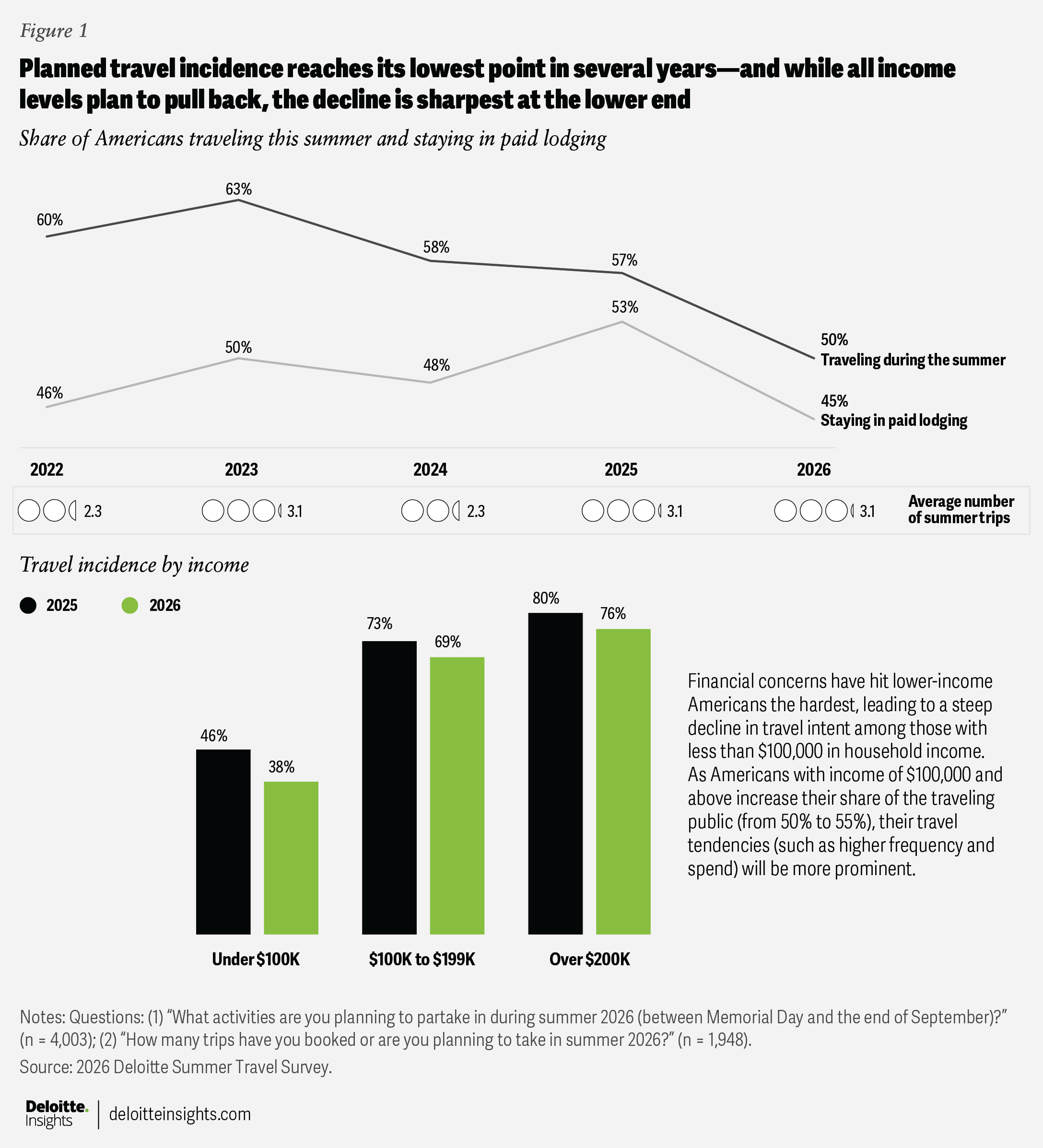

This summer, sticker shock is sidelining some travelers, while others are determined to get away even if it means digging deep into their pockets. According to Deloitte’s survey of 4,003 Americans, fielded from April 2 to April 9, 2026, 45% of respondents are planning vacations (with stays in paid lodging), the lowest in the last six years (figure 1). General affordability is a major concern for non-travelers, but a growing number of those staying home specifically highlight the high cost of travel. Also compounding matters somewhat are creeping concerns about safety and trip disruptions.

Those still planning trips show a promising willingness to invest in great experiences regardless of rising prices. Planned trip frequency (figure 1) and length are similar to 2025, and intended budgets are up. These positive trends are somewhat driven by the makeup of the traveler pool. With more Americans at the lower end of the income spectrum saying they will stay home, those with income of $100,000 and above will account for 55% of the traveling public, up from 50% in 2025.

Still, several signals of spending are up across income levels. Those who decide to travel seem largely unwilling to make significant compromises to rein in budgets. More travelers say they plan to increase marquee trip budgets (24% versus 19% in 2025) and fewer plan to decrease them (11% versus 14% in 2025). The pattern holds for lower as well as higher earners.

One key to understanding the mindset of American travelers this summer is that the share of budget increasers who cite high prices and the share who say travel has become more important to them have both risen sharply. Travelers are resisting compromise and spending more to keep up with rising prices. That posture exists across income levels.

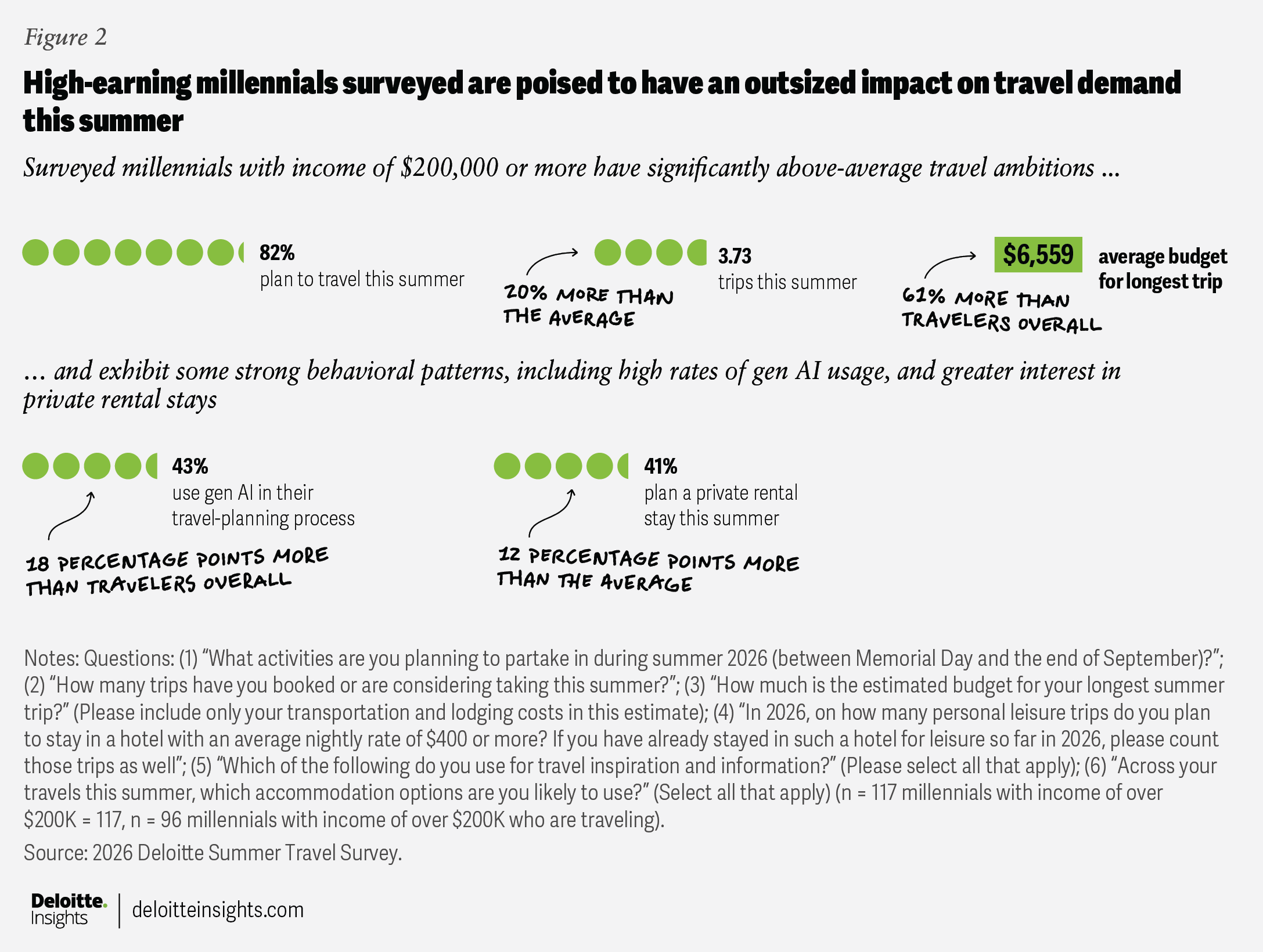

A significant pocket of opportunity might be found in high-income millennials (figure 2). More than 8 in 10 respondents in this group plan to travel, at about 1.2 times the frequency of others, and with 1.6 times the budget for their marquee trips. Connecting with this group increasingly requires a strong gen AI strategy, as 43% say they use it in their trip planning.

In a possible signal of uncertainty or price-wariness, travelers have made less progress booking their trips compared to 2025. Travelers in the $100,000 to $199,000 income group exhibit the biggest booking-progress gap (37% fully booked versus 45% in 2025). They may be experiencing the greatest conflict between their travel preferences and their ability to afford them.

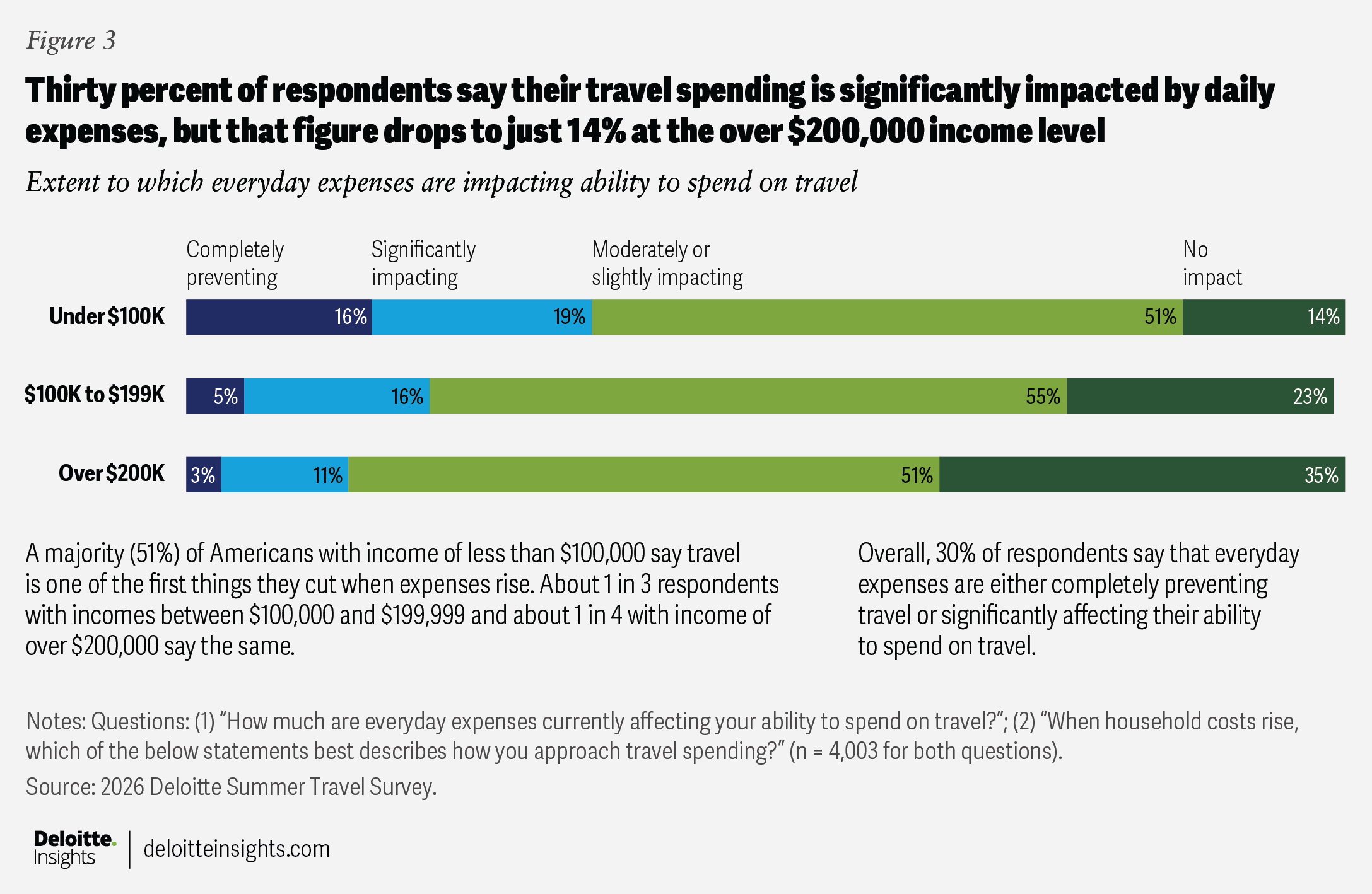

If perceptions of high household costs persist beyond the summer season, travel demand could face ongoing challenges. A majority (51%) of Americans with income of less than $100,000 say travel spend is one of the first things they cut back on when expenses rise (figure 3). About a third of respondents with incomes between $100,000 and $199,000 say the same, and about a quarter of those with incomes of $200,000 and above.

Beyond the dip in overall travel incidence, there are few concerning signals for travel providers in the upcoming summer season. Travelers are not shying away from any particular types of lodging or showing resistance to upgrading their flights. Suppliers targeting lower-income levels could face some challenges, but they may be able to coax demand up with well-constructed deals.

BY

Kate Ferrara

Eileen Crowley

Matt Josephson

Matt Soderberg

Maggie Rauch

Upasana Naik

The authors would like to thank Sanjay Vadrevu for his contributions to this report.

Editorial (including production and copyediting): Rithu Thomas, Preetha Devan, and Anu Augustine

Design: Natalie Pfaff, Sofia Laviano, and Harry Wedel

Cover image by: Sofia Laviano; Adobe Stock, Getty Images

Knowledge services: Rohan Singh

Visit the Deloitte Consumer Industry Center

Access more insights for the automotive, consumer products, food, retail, wholesale and distribution, airlines and hospitality, and transportation sectors.