Health tech investment trends: Technology and platform-enabled ecosystems could change health care

Despite the economic trends affecting the broader tech market, health tech is expected to continue to disrupt health care.

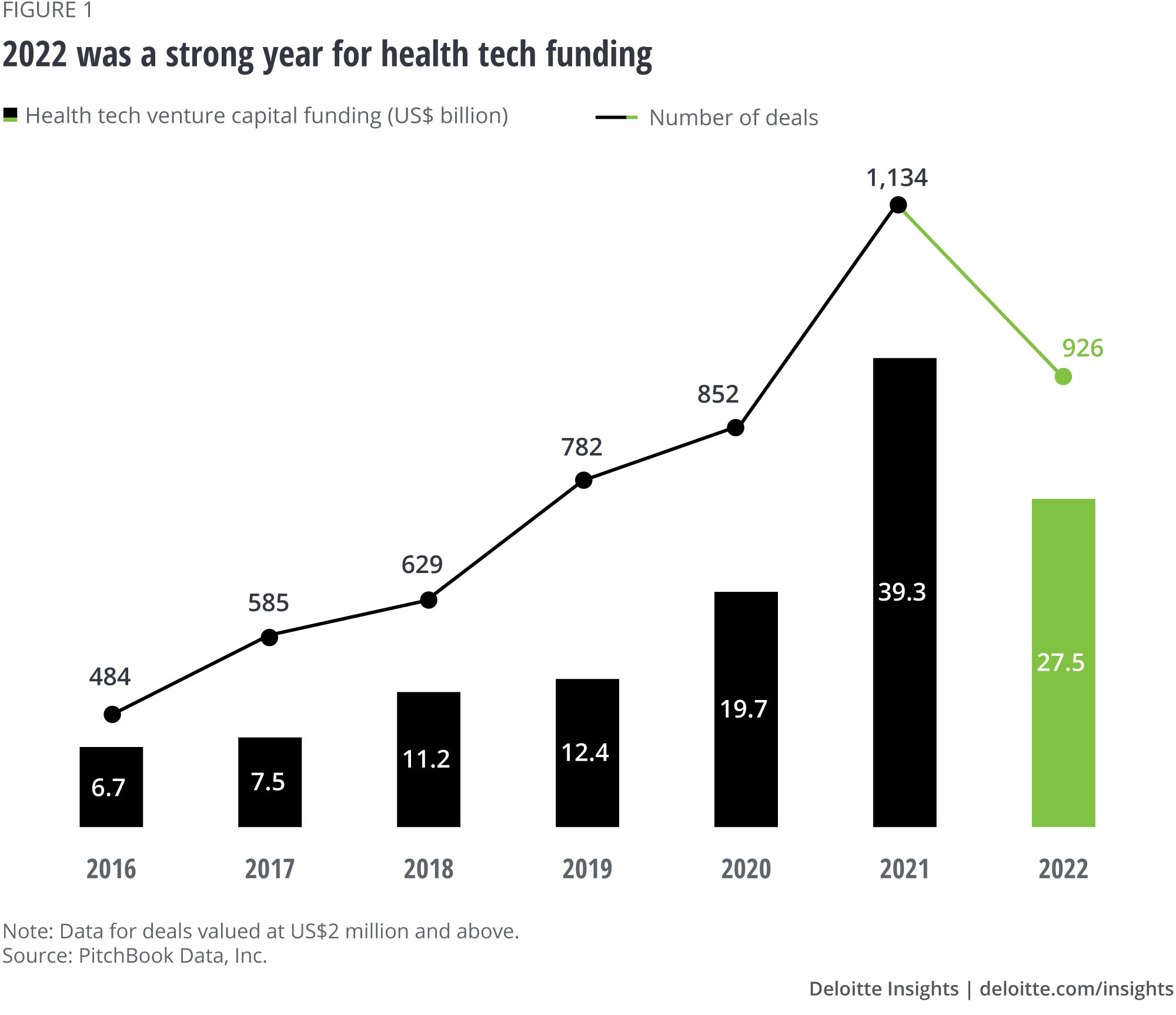

As the dynamics of the 2022 and early 2023 macroeconomic environment swept across the United States, the health tech market felt a cooling effect. The health tech sector’s 2022 venture capital funding fell short of 2021, dropping about 30% from US$39.3 billion in 2021 to US$27.5 billion in 2022 (figure 1). However, 2022 investments were still approximately 30% higher than in 2020, and more than doubled from 2019. As the overall venture capital funding continues to trend up, interviewed health tech experts remain optimistic about the opportunities to bring innovation to health care in 2023 and beyond. To keep pace, innovators that have been primarily focused on growth are also finding ways to bridge longer funding cycles.

A year ago, our report showed a spectrum of reactions to the concept of platform-enabled ecosystem, which deviates from the traditional pipeline business model. Some industry leaders were bullish on the idea while others expressed skepticism about ecosystems as a future business model. However, our latest analysis of 2022 later-stage venture funding shows that eight of the top 10 funded health tech innovators are, by our definition, platform-enabled ecosystems (See sidebar, “What is a platform-enabled ecosystem?” for more information.), and we expect platform-enabled ecosystems to continue to gain traction in the market.

To understand what the macroeconomic environment could mean for the health tech market moving forward, the Deloitte Center for Health Solutions continued its annual look at US health tech investment trends. To understand the current and future landscape, we conducted a data analysis of venture capital deals in the health tech1 space and interviewed nine executives from investment and startup companies between November 2022 and January 2023.

"Macro markets are where ingenuity, resilience, and perseverance pay off. Many of the best inventions happen during market downturns. The most sustainable and impactful solutions can emerge over the next three years. It is a challenging environment, and many startups will not make it, but it’s a healthy part of the innovation cycle.”

{kind=link}

What 2022 health tech investments can tell us about the health of the sector

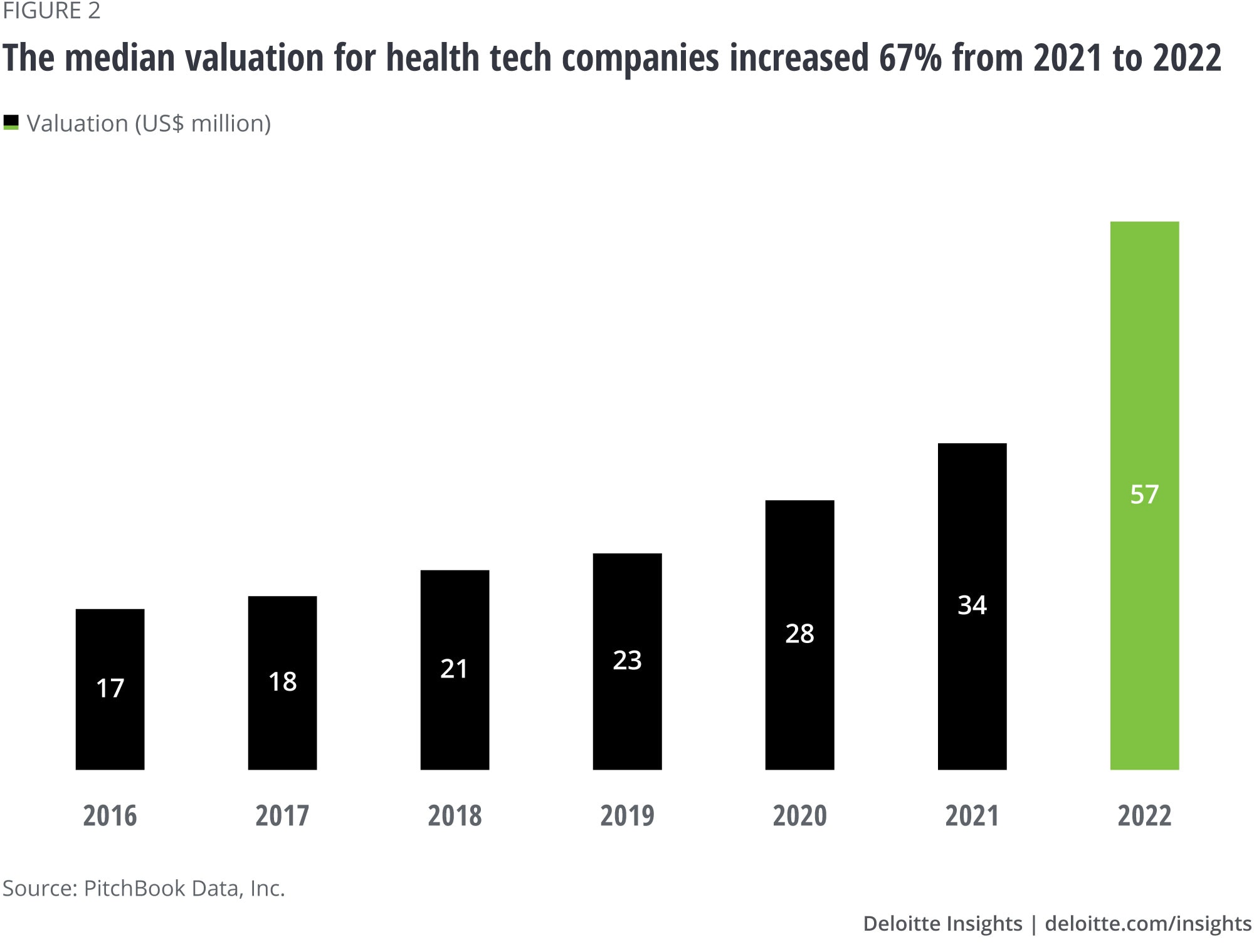

Interviewees believe that the health tech market holds much opportunity moving forward and the sector continues to show strong signs of growth to disrupt health care. For example, the median health tech deal in 2022 fetched a valuation of more than US$57 million, which was substantially higher than the 2021 median (US$33.9 million) and that of years prior (figure 2).

"We've deployed more into health care this year than last year and deployed more last year than the year prior. We are growing our health care practice."

{kind=link}

As in past years, late-stage companies continued to see more investments (75%) than early-stage companies (25%).2 This trend may be due to many of the typical factors, including an investor focus on proven value propositions, but could also be attributed to fewer companies choosing to go public in 2022.3 According to the executives we interviewed, some investors decided to pause new investments or shift to earlier-stage investments to adapt to today’s economic climate. The shift in focus seems to have resulted in a “back to basics” approach that may continue into 2023. In addition to focusing on growth, innovators may be looking to achieve stability, to help them bridge longer funding cycles, and, potentially, provide meaningful value to their clients.

“Industry has shifted its focus toward unit economics, capital efficiency, and long-term sustainable value. All our portfolio companies have strong balance sheets. They're all focused on sustainability versus hyper growth.”

According to interviewees, today’s investors are less focused on telehealth and general mental health, as have been the focus during the past few years. Instead, investors are more focused on specific areas of mental health (e.g., populations like the elderly and women), hands-on care delivery approaches, and value-based care solutions. Back-office efficiencies continue to be of interest, particularly those that show a quick return on investment. Health equity is gaining attention, both through investing in startups founded by racially and ethnically diverse people and/or women, as well as solutions focused on Medicaid populations and drivers of health (social determinants of health), such as housing and food.

Some startups are tackling these investment areas with a platform-enabled ecosystem approach. According to Deloitte analysis of data available in PitchBook’s health tech funding database, eight of the top 10 later-stage funded companies in 2022 are aligned to platform-enabled ecosystems. Our analysis indicates that this investment trend could continue to grow.

What is a platform-enabled ecosystem?

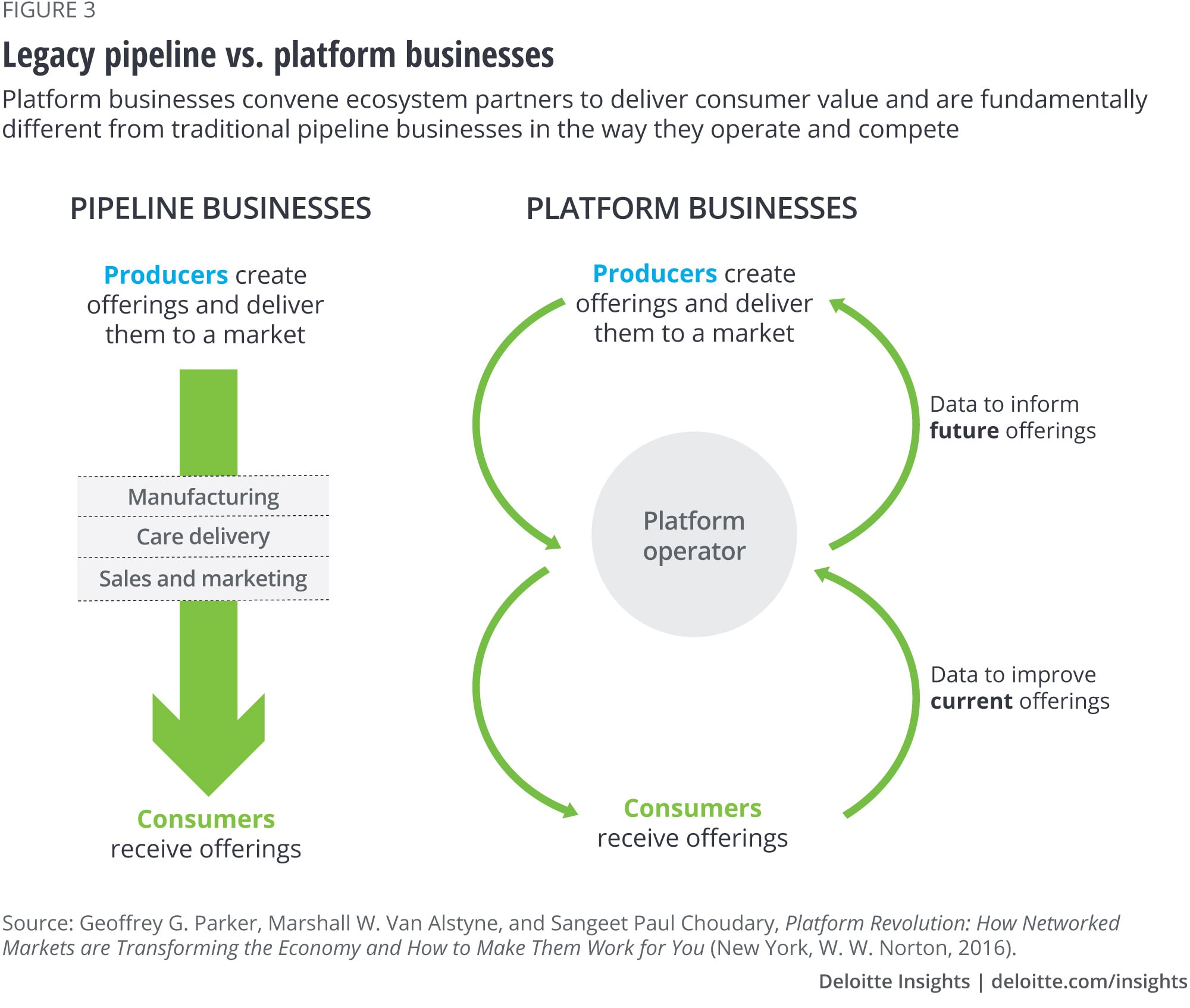

Unlike traditional pipeline businesses, which focus on selling a specific product or service to customers and competing on cost, quality, or market share, platform-enabled ecosystems, or platform businesses, compete on network effects that focus on an improved customer experience and differentiated offerings (e.g., ridesharing companies). Platform businesses develop an ecosystem through a network of users and partners who exchange information, services, or goods with each other. By leveraging the collective power of their users and partners, platform businesses can create more value for consumers than traditional pipeline businesses (figure 3).

{kind=link}

{kind=link}

Platform-enabled ecosystems, in particular, can be well-aligned to help the transition to value-based care. Here are a few examples:

- Memora Health is a complex care delivery platform that can empower care teams to better monitor and support patients by automating clinical and administrative workflows.4 Memora Health’s platform integrates with electronic health records, embeds into existing workflows, and offers tools such as remote patient monitoring, scheduling, virtual care, and outcomes management, to help enhance the patient and clinician experience. The platform uses natural language processing to automate follow-up communication with enrolled patients and categorize care management tasks.

The intelligent, scalable platform enables clinicians to focus on serving patients throughout the entire care journey in areas including cancer, surgical, gastrointestinal, chronic, maternal, population health, and more. It can reduce clinician burnout by reducing repetitive, manual administrative tasks and decreasing the number of patient portal messages that need to be answered. According to Memora Health, the platform has reduced inbox messages by 40%.5 Furthermore, it has reduced emergency department visits, increased patient education and screening rates, and improved medication adherence.6

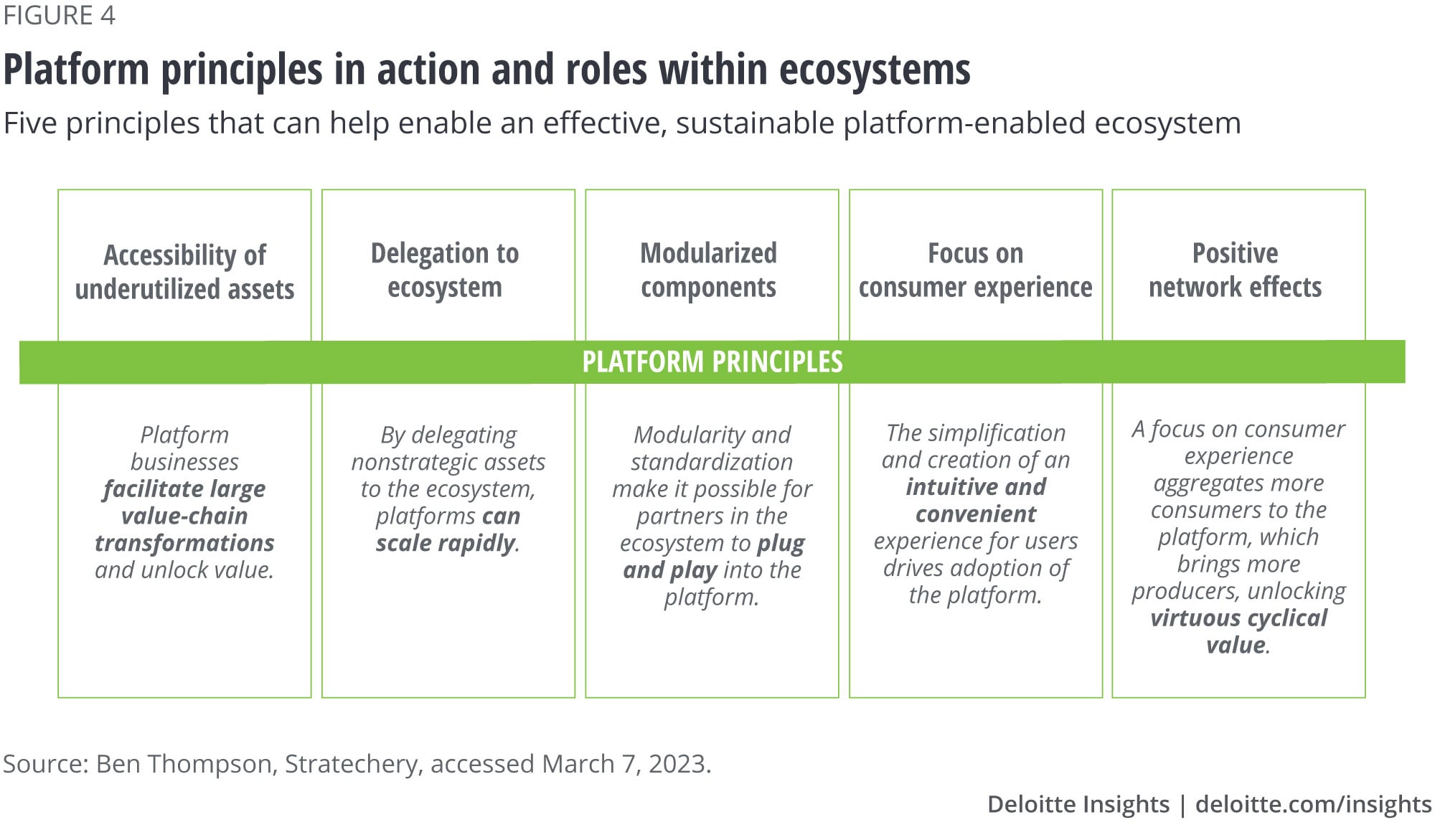

Our assessment of platform principles:

o Underutilized asset: Gives nurses more time to spend on patient care.

o Ecosystem delegation: Delegates tasks appropriately to different types of clinicians as well as administrative departments (e.g., billing) and partners with other patient and clinician experience platforms including remote patient monitoring systems, billing services, and telehealth tools.

o Modularized components: Uses a single platform to customize experience for providers; provides ability to turn care modules on and off.

o Focus on consumer experience: Reduces the friction in patient interactions by using a convenient and easy mode of communication: text messages.

o Positive network effects: Allows clinicians to spend more time with their patients, deepen the provider-patient relationship, and build trust. This allows clinicians to drive medical interventions that produce better outcomes, reduce costs, and help health systems transition to risk.

- Transcarent aims to make health care simple, accessible, transparent, and trusted.7 Users can access health care information and services at any time of day through an app. They are either connected with a health guide who helps provide the information and services they need, or directly with a clinician through text or video. At-home and in-person visits are also available, with Transcarent steering users to vetted physicians.

Through its merger with BridgeHealth, Transcarent providers its users with access to surgery centers of excellence that offer high-quality surgery at contracted rates, though Transcarent also partners with other surgery centers.8 Transcarent also recently announced plans to partially acquire 98point6, an AI-powered primary care startup.9 This will give Transcarent access to 98point6’s physician group and software. Transcarent is offered through some employers and is paid based on how much it saves employers, aligning incentives and moving toward value-based care.10 According to Transcarent, the platform has reduced unnecessary urgent care and emergency department visits by 40% and reduced readmissions and complications by 80%.11

Our assessment of platform principles:

o Underutilized asset: Provides multimodal (virtual, in-home, on-site), asynchronous, convenient care and reliable health care knowledge through a health guide as well as access to primary care physicians and surgery centers of excellence.

o Ecosystem delegation: Partners with employers, clinicians, pharmacy, behavioral health, surgery centers of excellences, and chronic condition management apps.

o Modularized components: Uses a single platform to triage users, assist with navigation and engagement with the health care system, and address multiple care needs ranging from urgent care and primary care to specialty care.

o Focus on consumer experience: Enables users to quickly access care from pre-vetted sources with the assistance of a health guide, all from their smartphone.

o Positive network effects: Attracts more employers by understanding which interventions are improving health outcomes the most.

- StartUp Health, an investment company, has funded several health moonshots aimed at “accelerating the pace of progress in health innovation.”12 One of its moonshots focuses on access to care and includes startups focused on value-based care such as Cityblock.13 Cityblock focuses on community-based care for underserved patients using a tech-enabled delivery model that includes virtual, in-home, and on-site care. Practicing compassionate care that offers medical and behavioral health, as well as addressing drivers of health (social determinants of health), Cityblock has reduced inpatient hospital admission rates, improved quality outcomes, reduced costs, and increased revenue.14

Our assessment of platform principles:

o Underutilized asset: Provides multimodal, compassionate, holistic care.

o Ecosystem delegation: Focuses on drivers of health as well as behavioral health, while working with health plans, community-based organizations (including shelters and food pantries), local providers, and paramedics and EMTs that provide urgent care at home.15,16

o Modularized components: Leverages their own tech-enabled delivery model.

o Focus on consumer experience: Places the focus on patients first; for example, additional specialties are brought in while the patient is being seen, rather than scheduling follow-up appointments.

o Positive network effects: Provides compassionate care that has improved outcomes and decreased costs.

Platform-enabled ecosystems can use data to automate predictions and/or change care pathways. They can also expand their reach beyond the initial core business and move into either disease areas or focus areas, all while continuing to help improve the end user’s experience and provide value.

BY

Peter Micca

Boris Kheyn-Kheyfets

Simon Gisby

Christine Chang

Madhushree Wagh

Project team:

The authors would like to thank Maulesh Shukla for his expertise throughout the research process and insights on data analysis.

The authors would also like to thank Wendy Gerhardt, Rebecca Knutsen, Prodyut Ranjan Borah, Laura DeSimio, Zion Bereket, and the many others who contributed to the success of this project.

This study would not have been possible without our research participants who graciously agreed to participate in the interviews. They were generous with their time and insights.

Cover image by: Sonya Vasilieff.