Sizing the brain

Segmentation and growth factors of the global neuroscience market

Introduction

When our brains go awry, it can create disabling misery for the sufferer and long-term distress in their relationships with loved ones, friends and colleagues. It also imposes significant costs upon the wider society. Brain disorders are the leading cause of disability worldwide and a cause of death second only to cardiovascular diseases.1

According to the Global Burden of Disease, 12 mental health disorders affect 970 million people globally. That is one in eight of the planet’s people. And the prevalence of these disorders has increased by 48% since 1990 as the population has grown.2

Science should be coming to the rescue, but innovations in neuroscience essentially stalled in the latter half of the last century. In the early 20th century, a combination of hard work and luck produced three broad types of psychiatric drugs: antidepressants, antipsychotics and anxiolytics. But psychopharmacology developments petered out, and few new drugs reached the market during the last four decades. Further, the treatments on offer today often only delay the progression of the disease without recovering lost brain function.

However, with advancements in brain disorders lagging behind treatments in other fields, such as cancer or treatments for the heart, new energy and ideas are flowing into neuroscience. There is now hope that new treatments will arise to overcome the limitations of existing therapies and relieve the millions of patients suffering worldwide. To help new capital form investment decisions, Deloitte has studied the global neuroscience market (GNM) across segments and regions. Our report provides a comprehensive analysis of available diagnostic and treatment options (as a proxy for the neuroscience market size) to estimate the revenue-based valuation of the GNM until 2026.

The analysis indicates the GNM was worth $612 billion in 2022 and could grow to $721 billion by 2026, returning an aggregate compound annual growth rate of 4.2 percent across segments (ranging from 3.5 percent for behavioural therapy services to 27.8 percent for digital health).

We also conducted segment-specific correlation analysis that identifies an inverse relationship between current revenue levels and future growth rates. This could reflect that smaller value segments have the potential to gain more ground as nascent technologies emerge, sparking investor interest and confidence in novel therapeutic approaches. Further, different segments will drive GNM growth depending on the region.

In summary, we have developed a holistic framework to help guide investment decisions across neuroscience segments. The intention is to identify where patient demand will drive growth and where investments will most readily lead to effective market solutions.

Table of contents

- Introduction

- Brain disorders and their impact on patients and society

- The findings

Brain disorders and their impact on patients and society

Our central nervous system (CNS) is a sophisticated biological conglomerate formed of billions of neurons and glial cells distributed throughout the brain and spinal cord. Any dysfunction of the molecular, cellular or circuit underpinnings of the CNS triggers (referred to here, for simplicity) brain disorders. There are two main types of brain disorders:

- Neurological conditions—those triggering cognitive and motor dysfunction from damaged neurons and nerves (for example, Alzheimer’s disease, Parkinson’s disease and multiple sclerosis).

- Neuropsychiatric conditions—those characterised by disturbed behavioural and emotional states (for example, anxiety, depression, addiction). The concepts of mental health and mental illness are often applied to neuropsychiatric conditions, although mental illness may also appear as a comorbidity in neurological disorders.

The societal burden of brain disorders

Brain disorders are a significant global health problem and the second largest source of deaths worldwide. Neurological and neuropsychiatric disorders are responsible for 9 million and 8 million annual deaths, respectively. This is over 30 percent of deaths,3 which means every third person on this planet is likely to lose a family member to brain disorder.

Globally, this imposes a high cost on societies. The Global Burden of Disease Study calculates disability-adjusted life-years (DALYs) by summing years lost and years lived with disability for the global population with brain disorders. The annual DALY count is 276 million years for neurological disorders and 184 million years for neuropsychiatric conditions, adding up to 460 million years. Collectively, this represents the leading cause of disability worldwide.4

These DALY and fatality metrics indicate that current treatments for brain disorders leave much room for improvement. They also highlight the desperate need for more resources to be devoted to brain disorders to elevate the standards of care.

Roadblocks to the development of effective brain therapies

The limitations of current treatments arise from three factors. First, we have a limited understanding of the biological basis of brain disorders. These disorders affect an organ characterised by ‘emergent properties.’ These are properties that cannot be explained by the addition of functionalities shown by individual building blocks (for example, higher cognitive functions or consciousness). This adds a layer of complexity that is not present in other therapeutic areas and ultimately hinders the development of effective therapies.

Second, traditional pharmacological treatments are not enough to address brain disorders. If we conceive of the brain as an experience-dependent organ shaped by behaviour, we ultimately need to emphasise interventions beyond pills.

Lastly, the limited availability of early diagnostic tools generates a situation where clinically observable symptoms often only appear once the molecular signatures of the disease are at an advanced stage. This diminishes the efficacy of available treatments in reverting the course of the disease (that is, repairing the brain).

About this report

The negative impact of brain disorders is expected to worsen over the coming years as the COVID-19 pandemic served as an unprecedented global stress test. During the years of lockdowns, people were deprived of social interaction to an extent never before seen in recorded history.

Psychological and neuroscience research has few observations about mass isolation. Still, large-scale studies on social deprivation amongst the elderly show cognitive capacity, mental and physical well-being, and longevity can all be negatively affected.5 As social isolation escalates the risk of depression and dementia,6 the lockdowns are expected to spike the rate of brain disorders.

Reversing this must be a priority, particularly as social isolation increases loneliness among vulnerable people, including those who are disabled, poor or from culturally and linguistically diverse backgrounds. Furthermore, because we are increasingly a ‘Brain Economy’ where most new jobs demand cognitive, emotional and social skills, we need to ensure people are mentally healthy, so our societies continue to be productive. Neuroscience investments are fundamental to achieving such long-term economic resilience.

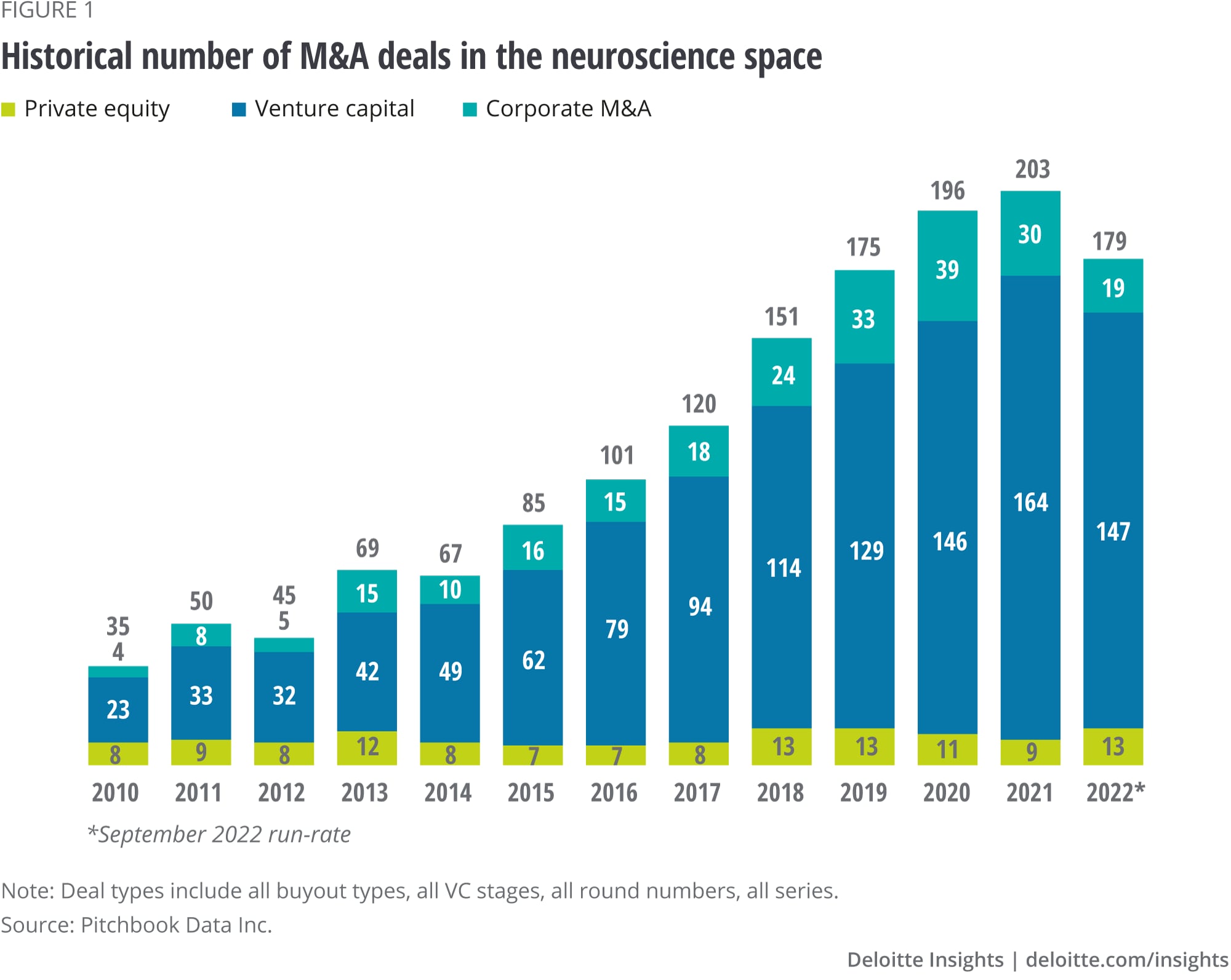

Over the last decade, investment bodies such as private equity, venture capital and corporate M&A divisions have been increasing the amount of capital dedicated to M&A deals in neuroscience (figure 1). However, further and more sizable investments are required if the Life Sciences Industry is to meet the needs of patients suffering from brain disorders worldwide.

This Deloitte report supports the decisions of investment bodies with the means to provide funds to companies focused on the development and commercialisation of solutions for brain disorders. By revealing the global neuroscience market's collective revenue potential in all significant segments and regions, we aim to facilitate capital access in the neuroscience space. New investments will enable the development of new therapies, alleviating the suffering of many and supporting a mentally healthy workforce and a fully functional economy.

{kind=link}

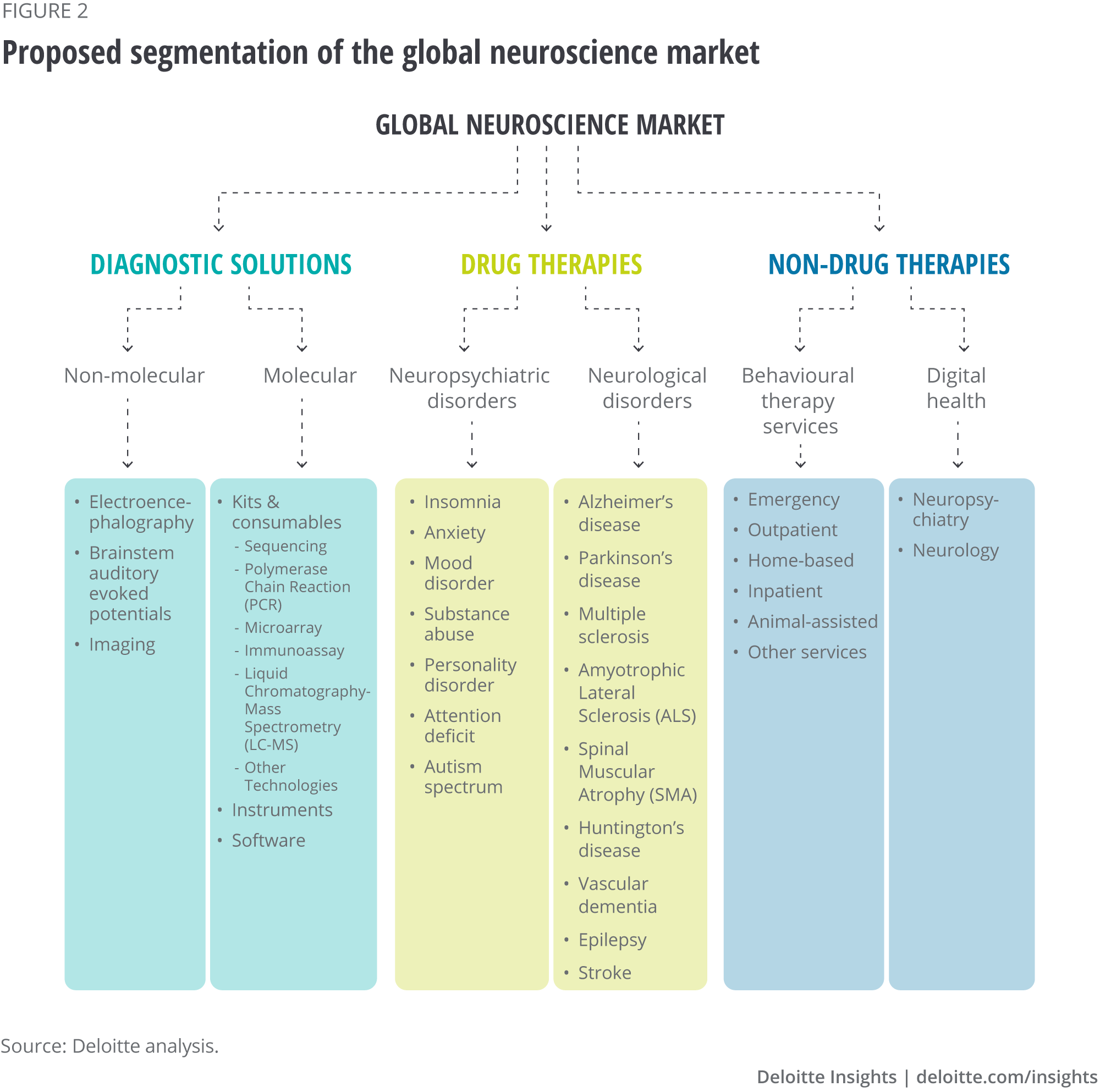

To create this report, we segmented the global neuroscience market (GNM) to account for traditional and novel solutions to tackle brain disorders (see figure 2) across three areas:

- diagnostic solutions (to accommodate the value of technologies facilitating the early diagnosis of brain disorders)

- drug therapies (to include conventional pharmacological methods and refined therapies targeting newly discovered molecular targets)

- and non-drug therapies (to account for the importance of behavioural interventions in treating brain disorders)

{kind=link}

Each area was further subdivided:

- Diagnostic solutions were subdivided into two segments. Molecular diagnostics are precision tests designed to detect biological markers at the genomic, transcriptomic, or proteomic level to accurately diagnose brain disorders. Non-molecular diagnostics are techniques to detect the presence of brain alterations based on electrophysiological (for example, EEG) or structural data (CT, MRI).

- Drug therapies were subdivided according to the nature of the disease they are intended to treat into neurological conditions and neuropsychiatric conditions (including mental health disorders).

- Non-drug therapies were subdivided into behavioural therapy services and digital health. Therapy services are a range of psychotherapies delivered across the entire continuum of care—from hospital settings to home—to address mental health issues. Digital health is software-based technologies and platforms designed for the prevention, monitoring, management or treatment of brain disorders.

With these subdivisions as the basis for our analysis, we conducted market research to estimate the revenue-based valuation of each GNM segment. We also analysed consistent market metrics to define which segments and regions will drive GNM growth until 2026.

The findings

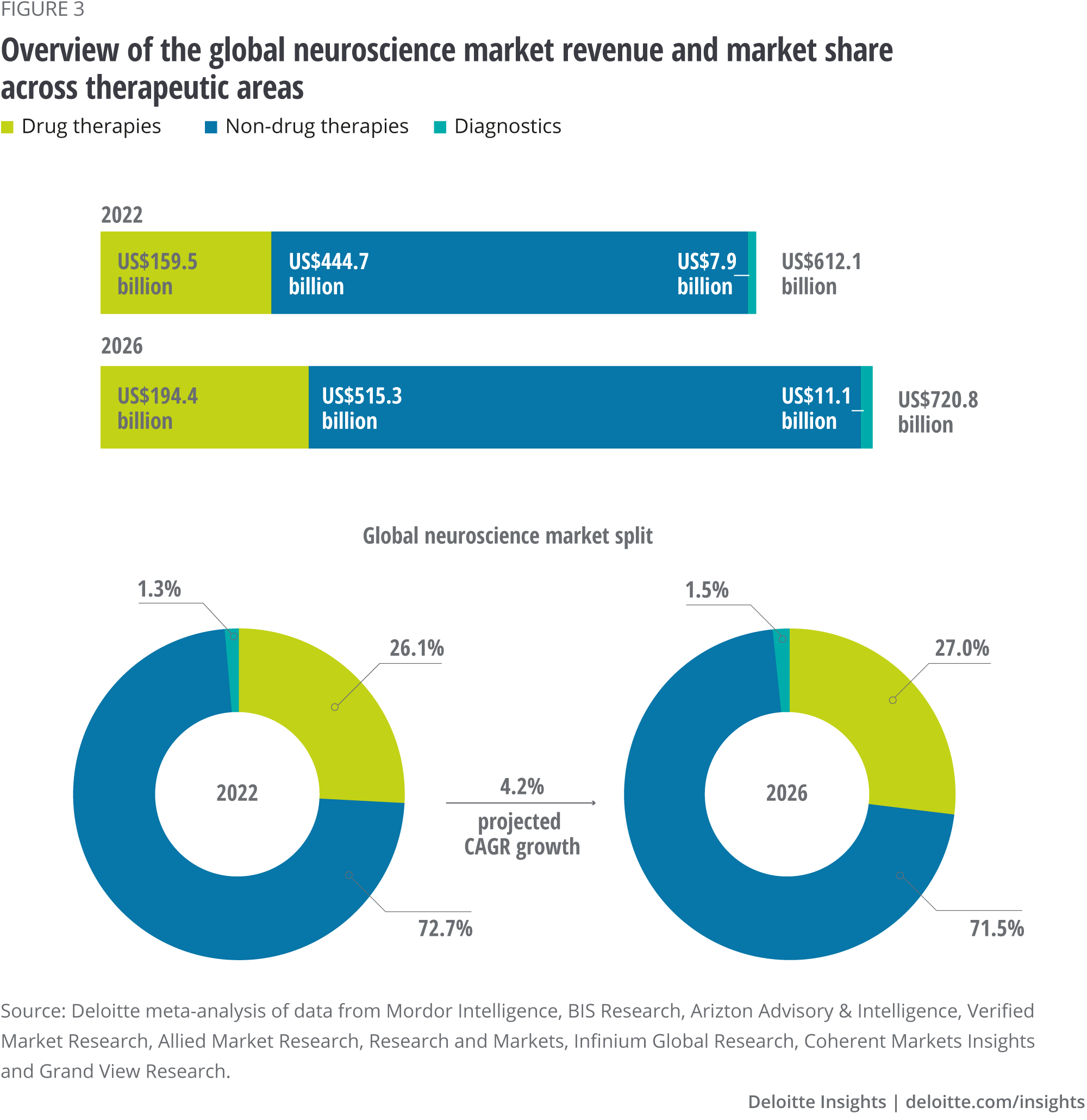

The GNM is a half-a-trillion-dollar market dominated by behavioural therapy services

The GNM had a value of $612 billion in 2022, with an outstanding 73 percent derived from non-drug therapies (figure 3). Such a predominance comes as no surprise if we consider how prevalent mental health problems are in modern societies, with 264 million people suffering from depression, 284 million from anxiety and 178 million from alcohol or drug abuse disorders.7

These patients need psychotherapy services involving a wide range of medical professionals, including doctors, emergency physicians, nurses, psychiatrists, psychologists and social workers. These conditions are typically chronic and require protracted interventions with recurrent service delivery, which explains the pronounced weight of behavioural therapy services in the GNM.

{kind=link}

The GNM is forecast to grow at a relatively low rate in the coming years, featuring a compound annual growth rate (CAGR) of 4.2 percent until 2026 with a valuation of $721 billion. However, CAGR estimates are biased towards high-value segments to the extent that more significant segments influence the metric more than smaller counterparts. So, the observed 4.2 percent CAGR could hide significant differences across segments.

Indeed, calculated growth estimates range from the high-growth digital health segment (CAGR 27.8 percent) to the low-growth behavioural therapy services segment (CAGR 3.5 percent).

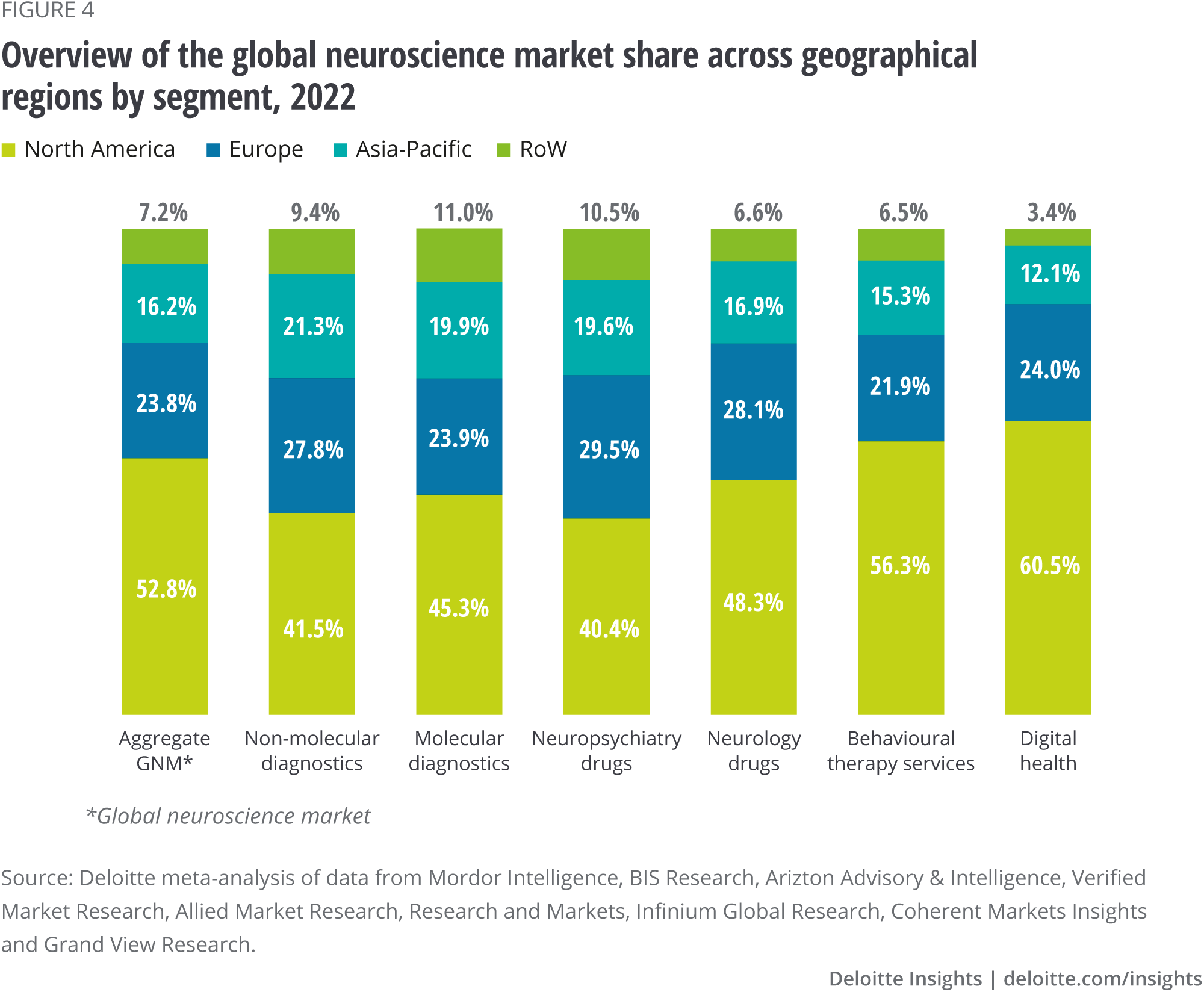

Over 75% of the GNM value stems from North America and Europe

Figure 4 shows the calculated distribution of GNM share across regions. Over 50 percent of the revenue arises from North America, while approximately a quarter stems from the European market. The remaining share is accounted for by Asia-Pacific and, to a lesser extent, the Rest of the World (RoW).

This regional split is consistent across all analysed segments, with North America ranging from 40.4 to 60.5 percent and always the major region. Europe ranges between 21.9 and 29.5 percent and is systematically the second leading region. Asia-Pacific varies between 12.1 and 21.3 percent.

It should be noted that this analysis reflects market size at current patient access levels. If patients in low-to-middle-income regions, particularly in emerging markets such as Africa, begin accessing therapy in increasing numbers, the market has much potential to grow.

{kind=link}

The neuroscience diagnostic market is primarily driven by medical imaging and next-generation sequencing technologies

Effective implementation of early diagnosis is paramount for the optimal intervention and management of brain disorders.8 A wide array of technologies enables the detection of disease-specific signatures based on molecular and non-molecular data, the latter including electrophysiological and structural data.9

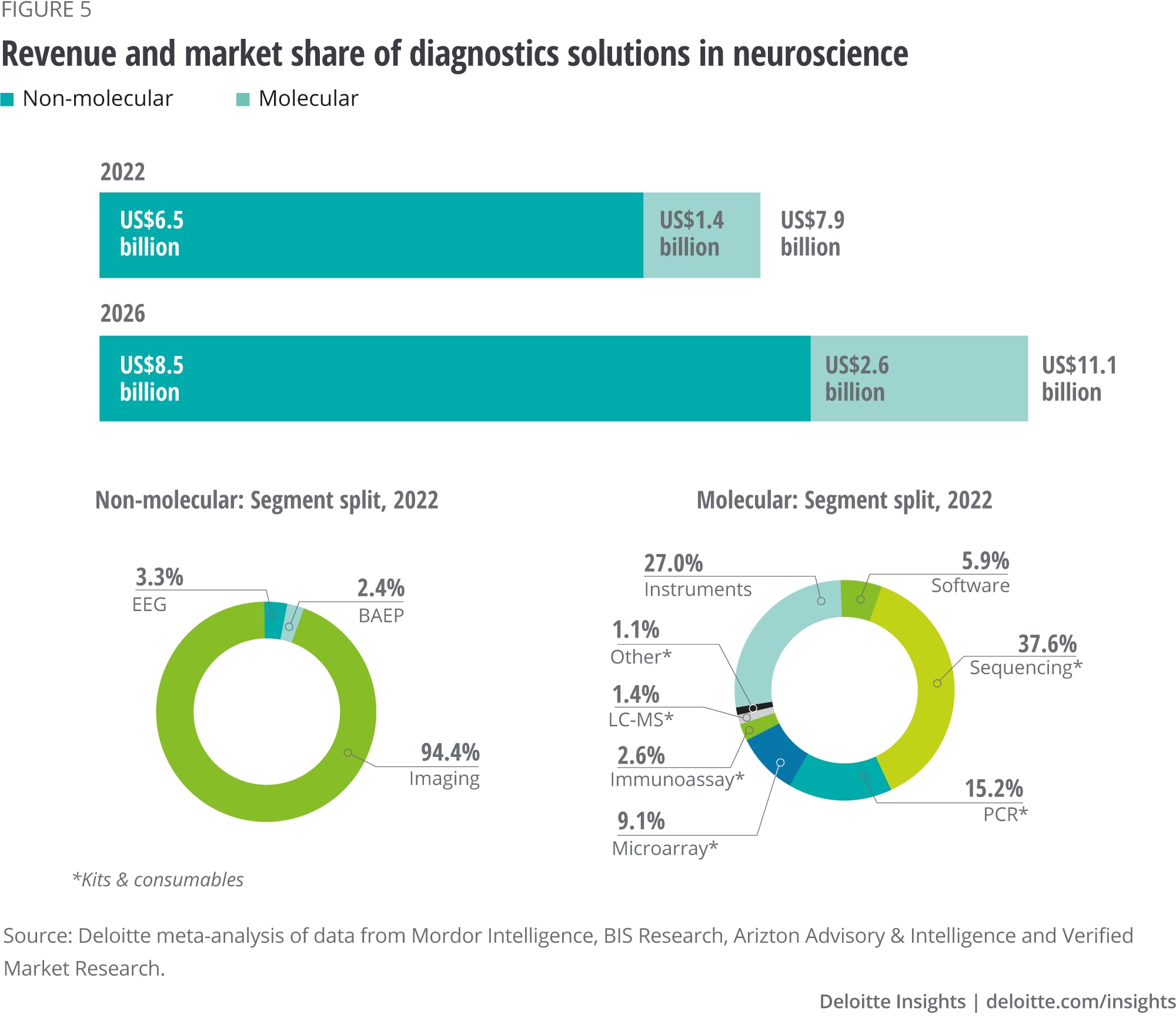

A total of $7.9 billion in revenue was generated in 2022 for the diagnosis of brain disorders, with 83 percent stemming from non-molecular diagnostic solutions, including electrophysiology and imaging techniques such as electroencephalogram (EEG) or MRI. The remaining 17 percent resulted from molecular counterparts (for example, PCR and immunoassay) (figure 5).

The growth of the molecular segment is expected to be 2.5 larger than the non-molecular, with CAGR values of 17 and 7 percent, respectively. The neuroscience diagnostic market is forecast to grow with a CAGR of 8.9 percent, reaching a valuation of $11.1 billion in 2026.

{kind=link}

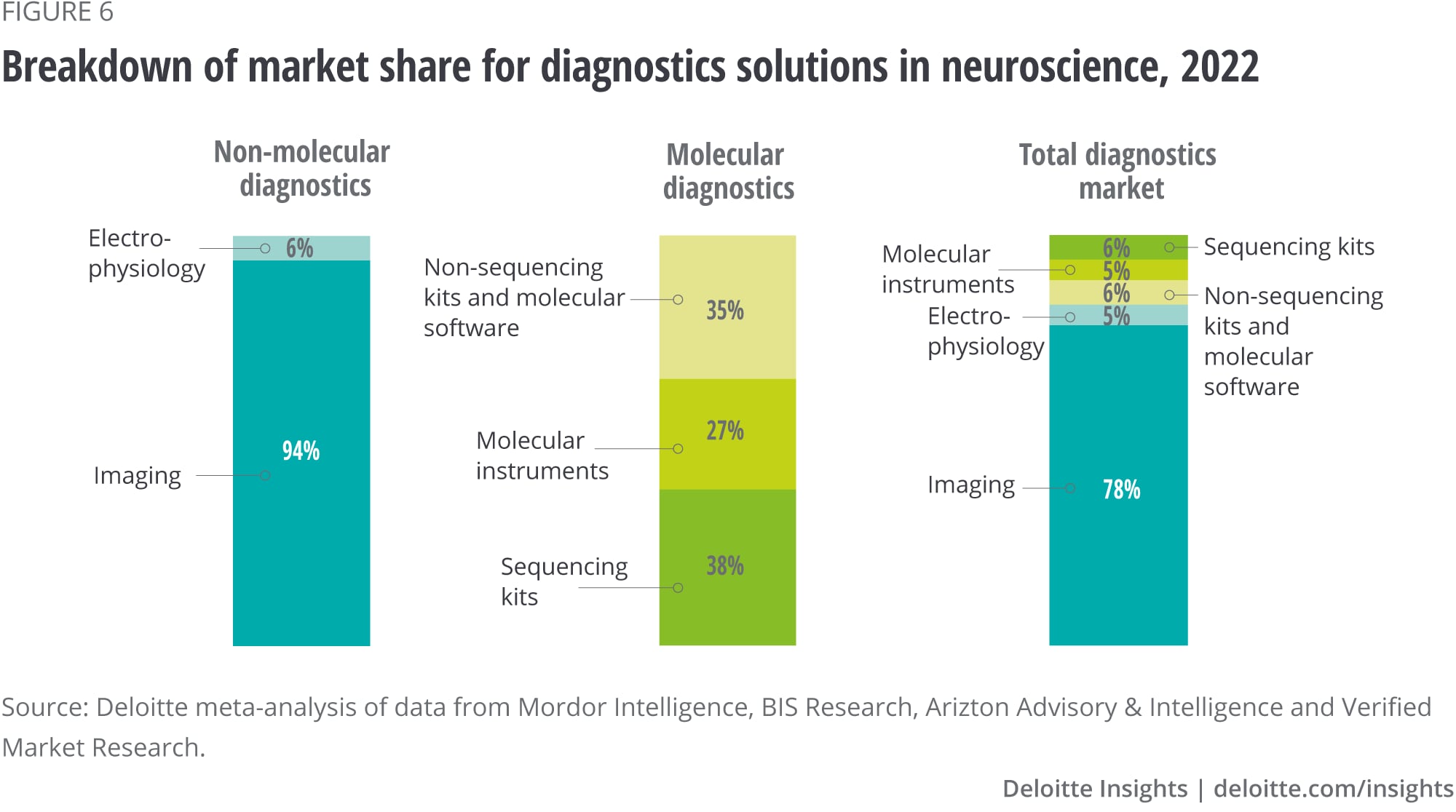

Imaging technologies accounted for 78 percent of the total neuroscience diagnostic market revenue in 2022 and up to 94 percent of the revenue generated by non-molecular diagnostics (figure 6). The main advantage of techniques such as Computed Tomography (CT) or magnetic resonance imaging (MRI) is their non-invasiveness—albeit some require patient exposure to small doses of radiation—while still allowing physicians to evaluate brain structure and inform the diagnosis of brain disorders.

Physicians increasingly demand hybrid technologies combining various imaging techniques to improve diagnostic accuracy, a trend expected to drive future market growth. Moreover, technological advances have enabled the transition from 2D to 3D analysis. This results in clearer images with higher resolution and less background noise, and optimised workflows with faster acquisition parameters and reduced radiation exposure.

Together with rising investments in AI-based imaging by health care companies and high-tech players, these trends support the growth projection. Medical imaging is expected to represent 73 percent of the total revenue from neuroscience diagnostics in 2026 and up to 95 percent of the revenue generated by non-molecular diagnostics.

{kind=link}

Kits and consumables dominate the molecular diagnostic segment of GNM. These are needed for sequencing technologies (38 percent of total segment revenue) and instruments required to run diverse molecular techniques such as sequencing, polymerase chain reaction (PCR), microarray and immunoassay (27 percent of total segment revenue) (figure 6). The prominent weight of sequencing technologies is explained mainly by increasing market adoption resulting from decreasing costs.

Technological advancements over the last decade, particularly in next-generation sequencing, have enabled genome sequencing to become much faster and cheaper than ever. Between 2009 and 2020, the cost per sequenced genome decreased by 99.8 percent, while the production volume increased approximately 3,000-fold over the same period.10

The forecast change for the 2020-2025 period is equally impressive, with a projected annual retraction rate of 19.7 percent for sequencing costs and an estimated CAGR of 117.2 percent for production volume.11 These metrics are expected to drive revenue growth from sequencing kits and consumables in brain disorders. The projected CAGR is 17.9 percent until 2026.

Pharmacological interventions dominate the neuroscience drug market against multiple sclerosis, anxiety, mood disorders and substance abuse disorders

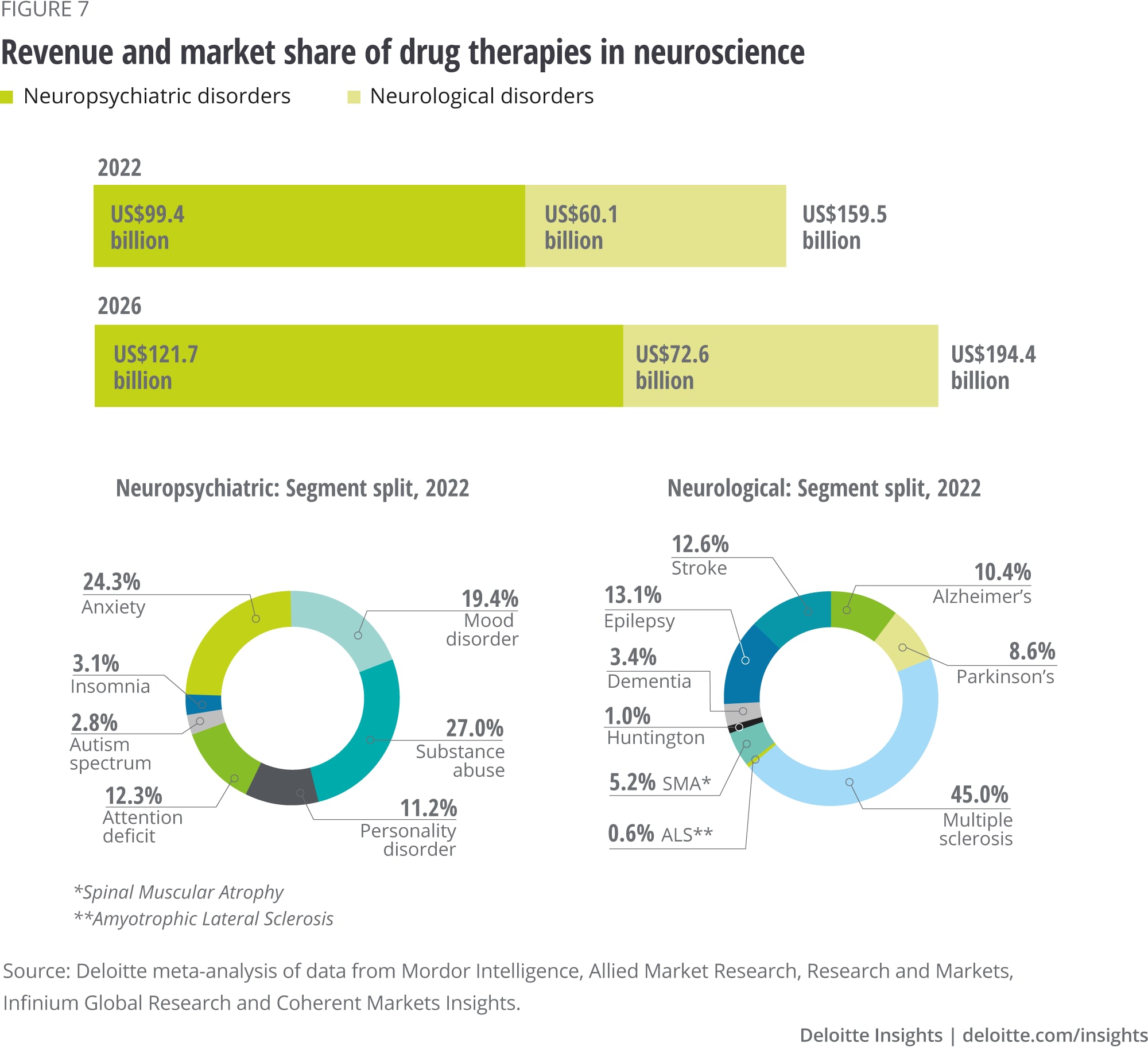

We analysed the market size of pharmacological interventions for 16 brain disorders, which we subclassified as either neurological or neuropsychiatric conditions12 (figure 7). The former accounted for $60 billion in 2022 (38 percent of the total), while the latter generated $99 billion during the same year (62 percent of the total). The projected growth for neurological and neuropsychiatric disorders is relatively similar (4.8 percent versus 5.2 percent, respectively), returning a compound CAGR of 5.1 percent.

{kind=link}

Two important observations highlight the poor distribution of drug availability across brain disorders. First, multiple sclerosis, anxiety, mood disorders and substance abuse amount to 61 percent of the revenue from neuroscience drugs. The remaining 12 brain disorders generate 39 percent of the total segment value.

It should also be noted that the patient population for a given disease is often not proportional to the size of the corresponding drug market. For example, Alzheimer’s disease has 55 million patients,13 and the annual drug revenue is $6.3 billion (2022). In comparison, 2.8 million patients14 suffer from multiple sclerosis. The annual drug revenue (2022) is $27 billion.

This difference is partly explained by the earlier onset of multiple sclerosis (20-to-40 years) compared to Alzheimer’s disease (60-70 years). However, it also stems from the substantial gap between the number of marketed drugs for the former (441 brands worldwide) and the latter (189 brands worldwide). This gap might narrow in the coming years as the global clinical pipeline for Alzheimer’s disease is larger than for multiple sclerosis.15 Nevertheless, these data imply that the current allocation of drug innovation does not represent patient needs, leading to an underserved CNS drug market.

The premature state of the neuropharmacology landscape is explained by the historically low efficiency of clinical development in CNS compared to alternative therapeutic indications. Until 2013, approvals for CNS drugs took, on average, 13 months longer than non-CNS drugs.16 Moreover, time-to-approval after regulatory submission in CNS was 31 percent longer.17

Lastly, approval rates for neuroscience drugs were less than half of those for alternative therapeutic areas (6.2 versus 13.3 percent).18 This gap was maintained as of 2021 when CNS drug approval rates for Phase II, Phase III and Filing were 26, 17 and 4 percent lower than the average of non-CNS drugs, respectively.19 These metrics emphasise the challenges pharmaceutical companies face when allocating R&D resources in neuroscience and highlight the need to broaden the therapeutic offering beyond drug treatments (see case study).

However, it is important to note that the relative inefficiency of clinical development in CNS is partly compensated by:

- The larger number of clinical trials in CNS compared to other therapeutic areas (except for oncology, which accounts for the largest share of clinical trials).20

- Clinical trial cycle time (the time lag between the start of Phase I and completion of Phase III), which is in line with the average across therapeutic areas (except for oncology, where cycle times are longer).21

These factors explain why, despite the lower inefficiency of clinical development, the number of novel active substance launches in CNS was only surpassed by infectious diseases and oncology in the 2012-2021 period.22

CASE STUDY—Exemplifying the struggles of drug development in brain disorders

In June 2021, the Food and Drug Administration (FDA) granted regulatory approval to the first-in-class Alzheimer’s treatment Aducanumab, developed through a joint clinical endeavour by Biogen and Eisai.23 Aducanumab’s novel mechanism of action—attachment to beta-amyloid plaques and subsequent removal by immune brain cells—had set high expectations within the Life Sciences Industry by targeting a best-described molecular hallmark of Alzheimer’s disease.

However, Aducanumab’s clinical development faced important blockers. In 2019, Biogen discontinued two Phase III trials after an external committee considered it unlikely the sponsor would meet the intended primary endpoint. Later the same year, Biogen claimed one of the two trials had indeed met the primary goal of a decrease in cognitive decline.24

The FDA approved Aducanumab in 2021 based on a surrogate endpoint with probable clinical benefit to patients (the ability to reduce amyloid plaques).25 However, there is no established relationship between the degradation of amyloid plaques and improvement in cognitive function, which is the intended endpoint of Aducanumab’s action. Casting further doubts on the rationale to approve Aducanumab, the scientific integrity of the seminal paper supporting the amyloid hypothesis—linking amyloid plaques to cognitive decline—was questioned in 2022.26

After Aducanumab’s approval in 2021, the European Medicines Agency denied commercial authorisation.27 Aducanumab’s price in the US fell by half from $56,000 to $28,000,28 and US insurers decided to cover the treatment only for patients enrolled in qualifying clinical trials.29

Despite the excellent profile of Aducanumab and the potential to raise the standards of care for patients with Alzheimer’s disease, this example highlights how tedious clinical development can become for drugs in the field of brain disorders.

The neuroscience non-drug market is dominated by the low-growth segment of behavioural therapy services, while the low-value segment of digital health is expected to experience sizable growth over the coming years

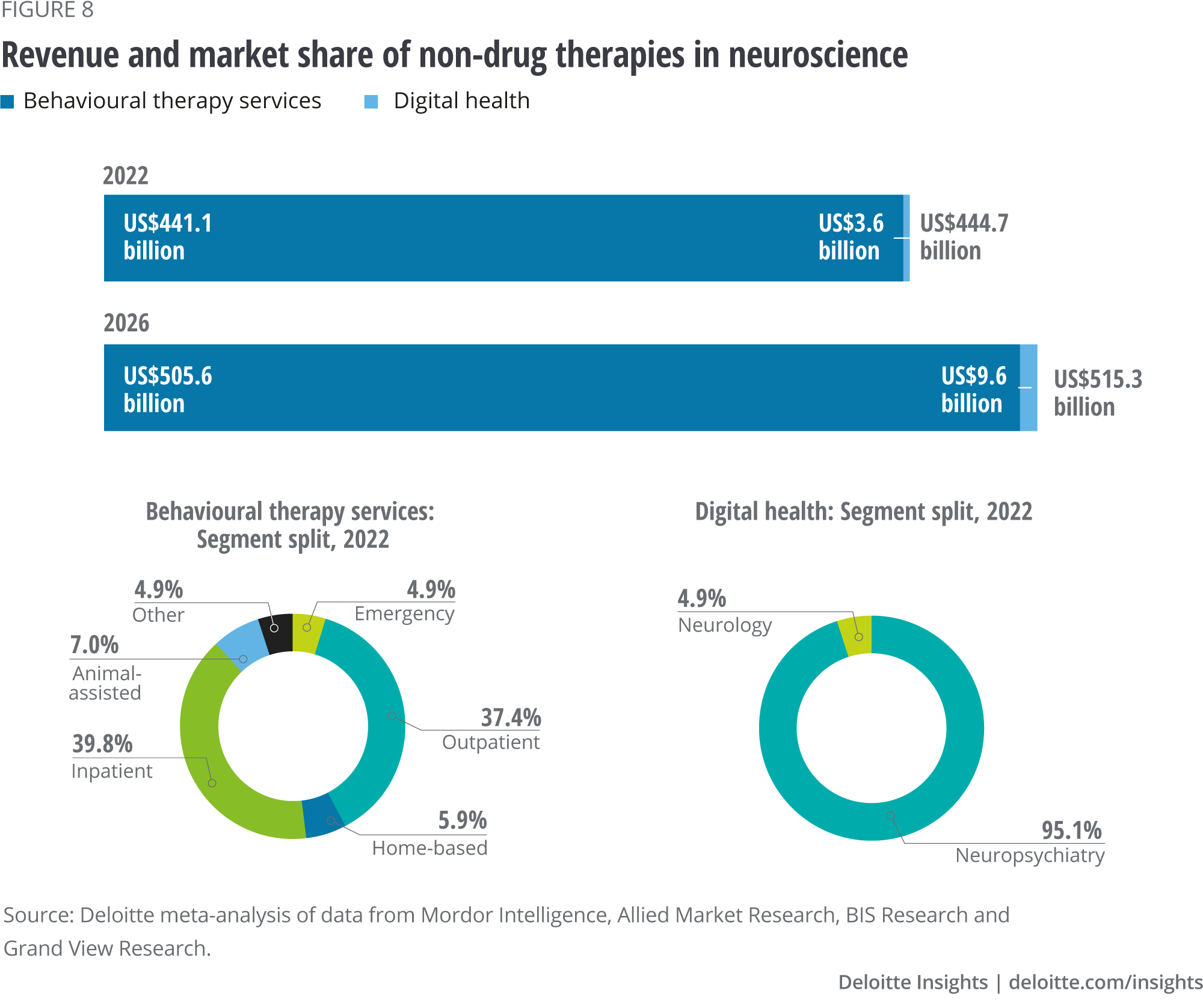

The brain is a plastic organ capable of recovering through behavioural experiences, highlighting the importance of non-pharmacological treatments. Figure 8 displays the revenue generated by behavioural therapy services (for example, psychiatric services or psychological counseling) and digital health over time.30 Out of $445 billion generated in 2022 by non-drug therapies, 99.2 percent ($441 billion) stemmed from behavioural services (predominantly in inpatient and outpatient clinical settings), while only 0.8 percent of revenue ($3.6 billion) was due to digital health interventions, primarily for neuropsychiatric disorders ($3.4 billion).

Significant value differences are mirrored by an equally sizable gap in growth estimates. While the high-value segment of behavioural therapy services is forecast to grow with a modest CAGR of 3.5 percent ($505.6 billion in 2026), the low-value digital health segment is expected to grow 27.8 percent annually ($9.6 billion in 2026). The market value of the non-drug segment in 2026 is projected to be $515 billion, with an aggregate CAGR of 3.7 percent.

{kind=link}

Despite limited growth projections, behavioural services will likely maintain a central role in treating brain disorders. The prevalence of mental health problems is expected to continue increasing as it has over the last decade. Global cases of anxiety, depression, and drug abuse disorders (for example, caused by the opioid crisis) increased from 14.9 to 18.4 percent between 2005 and 2015, boosting the need for the delivery of psychotherapies.31

Additional factors contributing to the central role of behavioural services are the increase in awareness of the importance of stress management at the workplace (a situation accentuated during the COVID-19 pandemic) and the surge in educational programs to de-stigmatise mental health disorders and advocate for the integration of susceptible individuals.

Digital health companies are developing non-pharmacological approaches to prevent, monitor, manage or treat brain disorders by combining diverse technological components, including software, hardware or artificial intelligence. Examples include cloud-connected devices for diagnosing or monitoring mental health, telehealth platforms offering remote medical consultations or software-based therapeutics acting as active interventions to improve the motor and cognitive function of patients with neurological disorders.

These digital solutions provide two advantages over traditional drug treatments.32

- They are cost-effective from an R&D perspective: Digital solutions have shorter development and approval timelines than drugs and offer great potential to optimise the return on investment.

- They facilitate patient centricity by increasing users’ involvement in treating and managing their diseases and enabling personalised recommendations based on monitored data.

The demand for telehealth and remote medical consultations has lately been fueled by the COVID-19 pandemic, after lockdown and social distancing measures compromised physician-patient interactions in person (for example, Teladoc acquired Livongo in 2020 through a multi-billion-dollar transaction).33

Moreover, the total investment value in digital health increased with a CAGR of approximately 30 percent from 2015 to 2020. The average deal size grew from $31.5 million in 2020 to $45.9 million in 2021, indicating increased investor confidence in digital technologies.34 Lastly, an increasing number of codevelopment and commercialisation partnerships between pharmaceutical companies and digital health players in the neuroscience space is expected to hasten the adoption of digital solutions for brain disorders (for example, Boehringer Ingelheim and Click Therapeutics, Sanofi and Happify Health).35

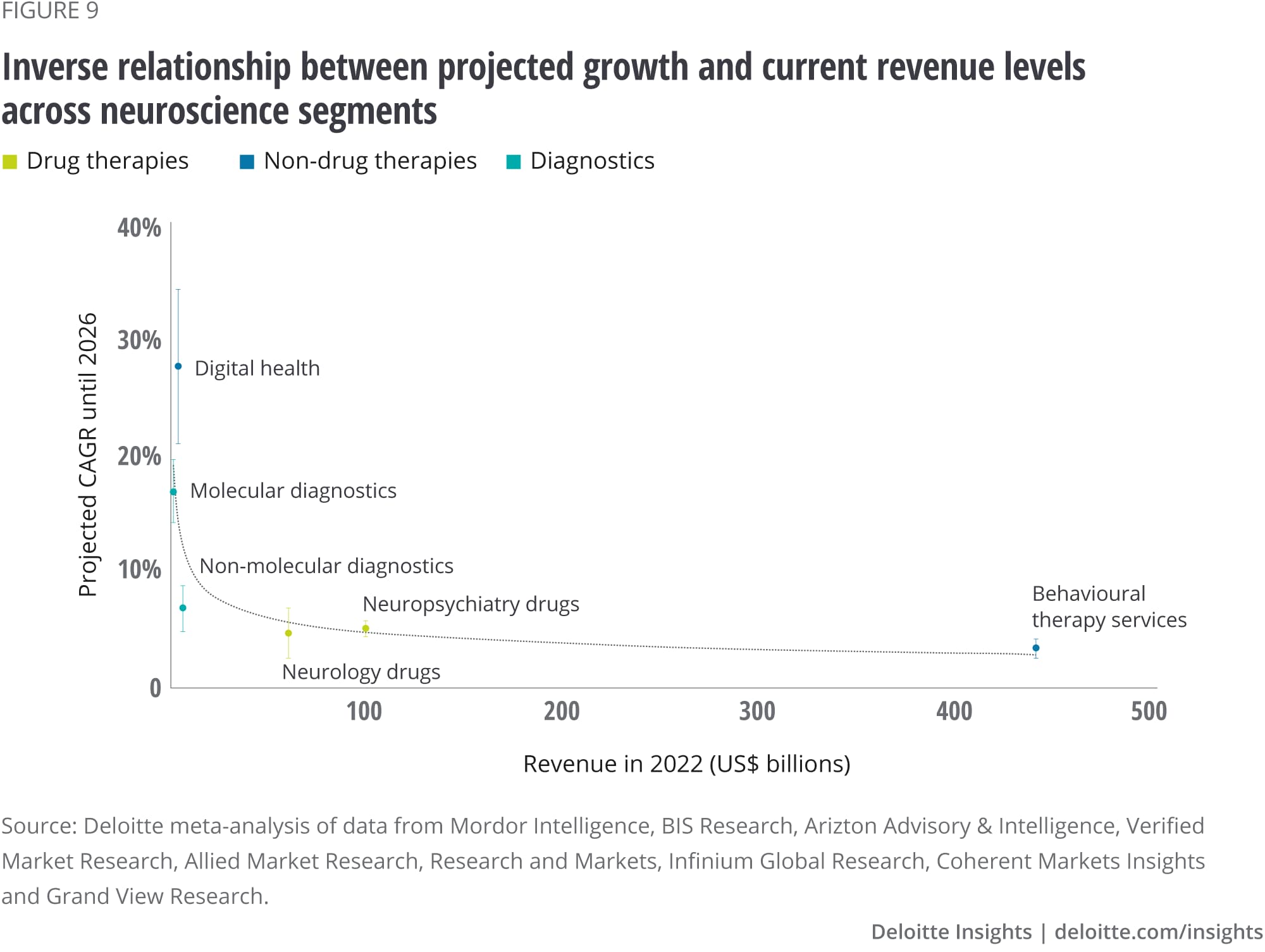

Current revenue levels and future growth rates negatively correlate across GNM segments

Having separately assessed the value and growth of the GNM across different segments, we performed a correlation analysis to gain further insights into the relationship between these two metrics. We found an inverse correlation by which high-value segments display low CAGR forecasts, while low-value segments have significant growth potential (figure 9).

Two factors can explain this inverse relationship. First, from a purely numerical perspective, the same revenue increment represents a more significant growth starting from a small revenue base than from a larger one. Moreover, lower revenues at present tend to be associated with recent technologies (for example, digital health, molecular diagnostics or advanced imaging techniques). As nascent technologies arise, investors are more willing to dedicate the available capital to developing state-of-the-art solutions that could offer a higher return on investment.

{kind=link}

According to this analysis, we can differentiate three clusters of segments:

- Digital health and molecular diagnostics: These segments display low value at present—below $4 billion—but are expected to grow with a fast CAGR of 27.8 and 17 percent until 2026 to reach $9.6 billion and $2.6 billion, respectively.

- Behavioural therapy services: This segment exhibits the largest revenue share—$441.1 billion—while projecting the lowest growth rate with a CAGR of 3.5 percent.

- Drugs and non-molecular diagnostics: These segments currently generate intermediate revenue levels between $7-99 billion, while exhibiting modest growth projections between 4.8 to 7 percentage points.

High-growth and high-value clusters will likely face challenges of different natures. Challenges faced by digital health and molecular diagnostics, both emerging technologies with high R&D activity,36 will revolve around optimisation of R&D processes, effective management of clinical trials, technical validation processes and definition of value proposition and go-to-market strategies.

On the other hand, the challenges of behavioural therapies (long-standing services with little innovation) will instead focus on operational initiatives to avoid entering diseconomies of scale. The conservation of competitive advantages by increasing either the differentiation or the cost-effectiveness of their offering will also be critical.

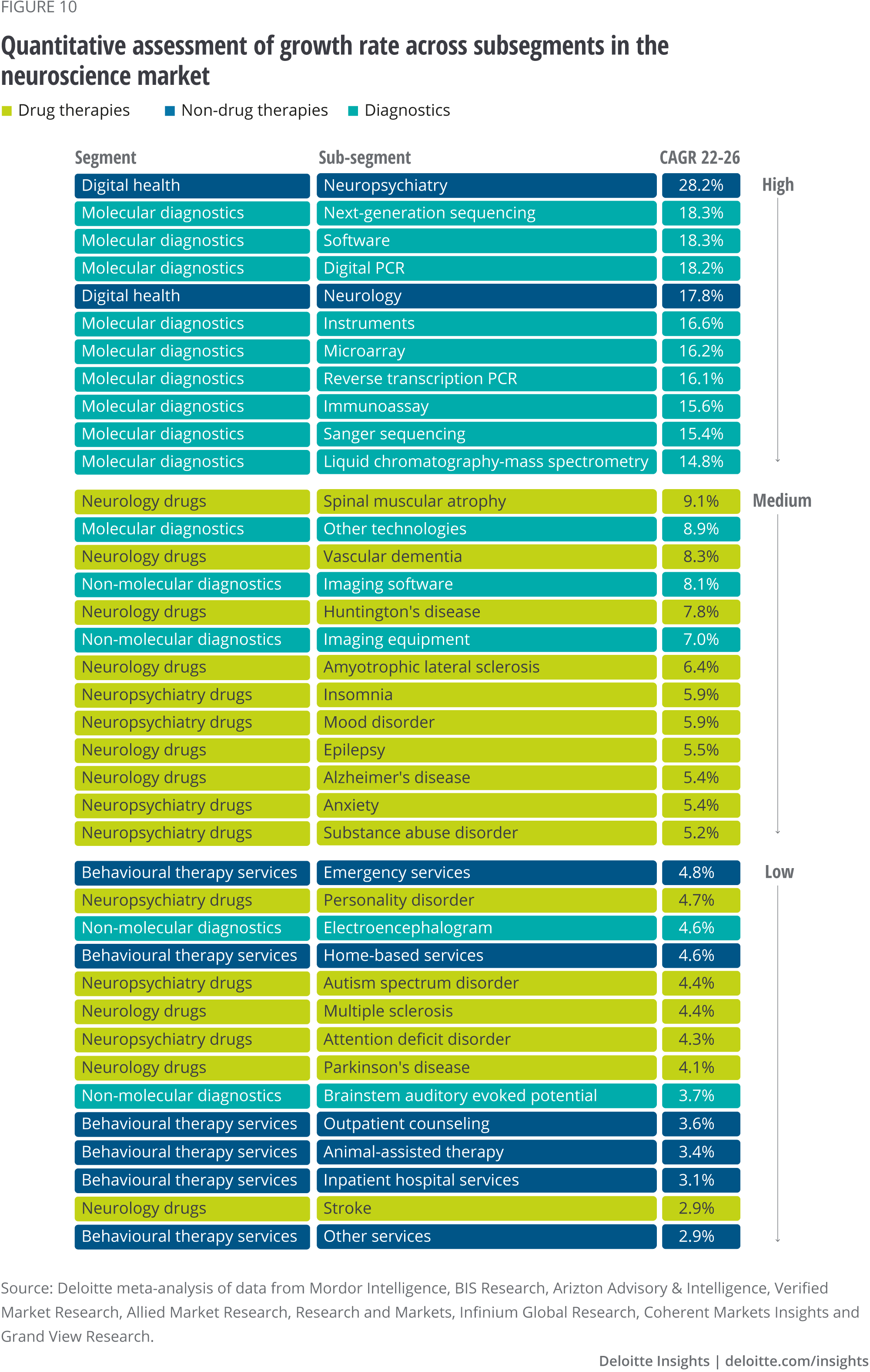

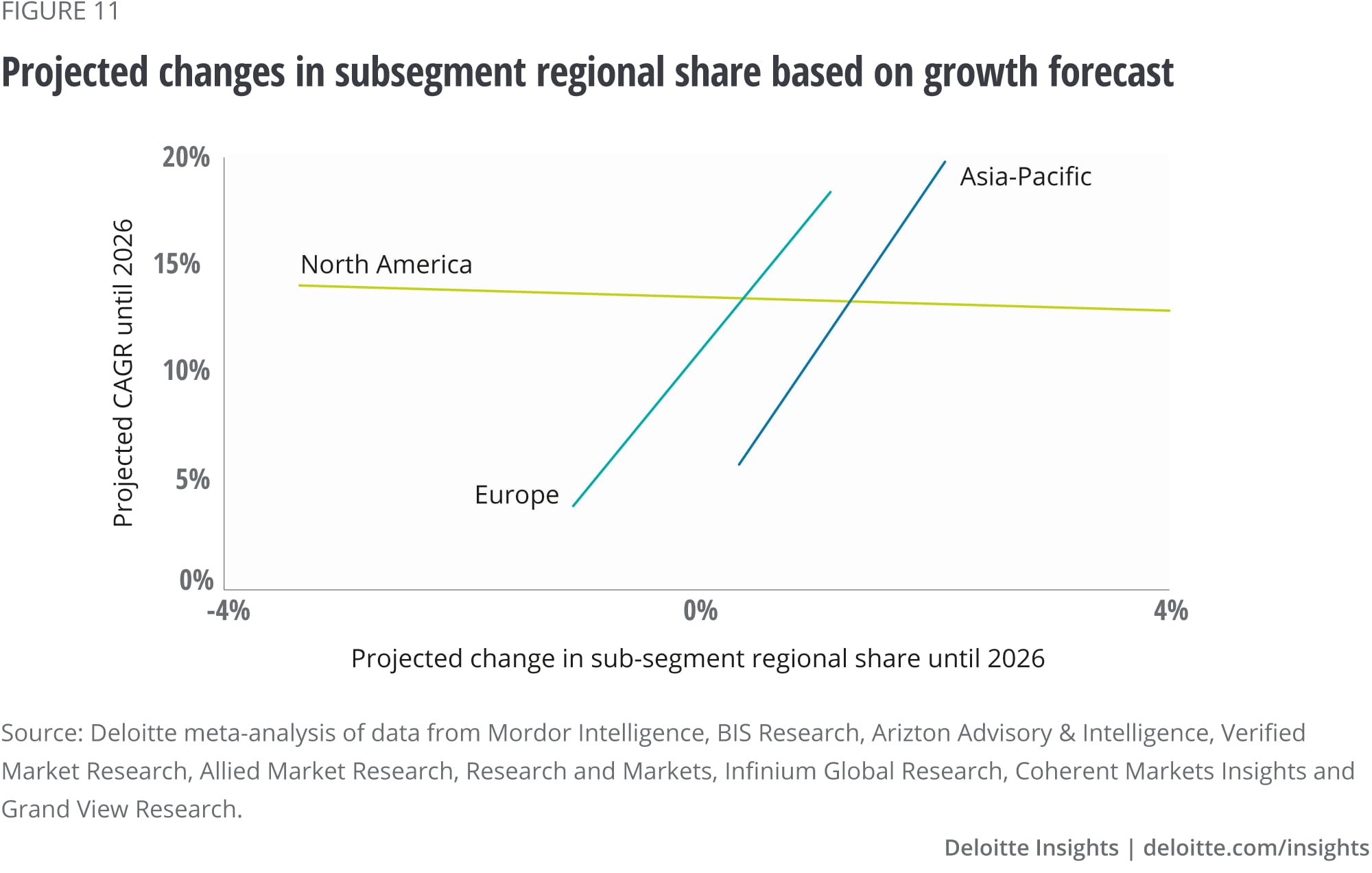

Different GNM segments will drive future growth depending on the regions

Lastly, we analysed the forecast CAGR for each subsegment (figure 10) and compared these data against the change in the regional market share each subsegment is expected to undergo between 2022 and 2026. Interestingly, this approach revealed that Europe and the Asia-Pacific are forecast to increase their market share in high growth subsegments (such as digital health for neuropsychiatry and neurology, and kits and consumables for molecular diagnostics). In contrast, in North America, the projected CAGR of a given subsegment does not seem to provide any information about the expected change in regional market share, as highlighted by the absence of correlation between these two parameters (figure 11).

These results align with our earlier observation that over half of the GNM revenue is generated in North America (as shown in figure 4). Accordingly, regions such as Europe and the Asia-Pacific, where the market could be more consolidated from a commercial perspective, might be more willing to fill the revenue gap by preferentially investing in the latest technological advancements (digital health, molecular diagnostics). This is not to say North America will not invest in digital health and the latest diagnostic tools. However, local investors will also aim to preserve the revenue base from long-standing, high-revenue segments such as behavioural therapy services.

{kind=link}

{kind=link}

Conclusion

The brain has been described as the most complex structure in the known universe, so it is no wonder then that medicine has struggled to solve its many varied disorders. The causes of neurological disorders vary but include genetics, congenital abnormalities, accidents and infections.

They can also stem from lifestyle or environmental health problems. Aging is a primary risk factor for most neurodegenerative diseases, including Alzheimer's, Parkinson's and Huntington's. As the populations of the west rapidly age, the rates of these diseases are expected to increase.

Add the stress of modern lifestyles, the opioid crisis, plus the mass isolation imposed by COVID-19 lockdowns. Mental exhaustion, chronic time pressure and the loss of work-life boundaries in the wake of the pandemic have left many emotionally exhausted and burnt out.

All this could lead to a surge in conditions like depression, anxiety, schizophrenia or bipolar disorders. Any increase in people with such brain disorders will place a heavy demand on societies and their health care systems.

The analysis reflects Deloitte’s current view on potential investment opportunities in neuroscience by presenting a selection of segments, their forecasted returns, and estimated growth rates, based also on regional differentiators and local developments. However, Deloitte does not provide any representations to the accuracy or completeness of any analysis, estimates and projections included in this document.

Three critical takeaways emerge from this report:

- The global neuroscience market offers attractive return potential. The market is valued at $612 billion (2022) and is forecast to grow at a compound annual growth rate of 4.2 percent over the coming years. The calculated growth estimates range from the high-growth digital health segment (CAGR 27.8 percent) to the low-growth behavioural therapy services segment (CAGR 3.5 percent).

- Investment bodies may infer future growth, and therefore projected return on investment based on current revenue levels across segments of the global neuroscience market. Our analysis reveals an inverse correlation between the current value and future growth, by which high-value segments display low-growth forecasts and low-value segments have significant growth expectations. These findings might be anticipating an increased investor appetite for nascent, state-of-the-art solutions that—although posing a higher investment risk at present—might translate into significantly higher returns in the future.

- Private equity, venture capital and corporate M&A organisations may adjust their investment strategy according to the target region. Our analysis shows that the regional share of GNM subsegments will evolve differently depending on geographical location. Europe and Asia-Pacific are expected to capture market share in high-growth segments (such as digital health and molecular diagnostics). In contrast, the absorption of market share in North America seems to be independent of the projected subsegment growth. These findings might reflect an increased willingness in Europe and Asia-Pacific to preferentially target investments in the latest technologies. Moreover, our results indicate that the market in North America will likely evolve uniformly across growth rates, potentially preserving the large revenue base of more traditional solutions such as behavioural therapy services.

The high growth of digital health and molecular diagnostics is positive from a patient perspective. As discussed, the standards of care provided by current pharmacological treatments leave ample room for improvement due to two factors—first, the inherent propensity of the brain to respond predominantly to behavioural experiences. Second, the delayed diagnosis of brain disorders leads to drug regimen commencement only after the symptoms are advanced.

The growth of digital health and molecular diagnostics is expected to address the former and latter challenges, collectively elevating the standards of care for brain disorders and benefiting millions of patients worldwide.

Glossary

Behavioural therapy: form of psychotherapy that applies the principles of learning, operant conditioning and classical conditioning to eliminate symptoms and modify ineffective or maladaptive behavioural patterns. The focus is on the behaviour itself and the contingencies and environmental factors that reinforce it, rather than the exploration of the underlying psychological causes of the behaviour.

Cardiovascular disease: general term that describes a condition of the heart or blood vessels.

Glia: type of cells which are non-neuronal and are located within the central and peripheral nervous system to provide physical and metabolic support to neurons (for example, neuronal insulation and nutrient and waste transport).

Molecular signature: biological molecule found in blood, other body fluids or tissues that is a sign of a normal or abnormal process or of a condition or disease. A molecular signature may be used to see how well the body responds to a treatment for a disease or condition. Also called biomarker and molecular marker.

Neurodegenerative disease: neurodegenerative disorders encompass a wide range of conditions that result from progressive damage and loss of cells and nervous system connections that are essential for mobility, coordination, strength, sensation and cognition.

Neuroscience: branch of the life sciences that deals with the anatomy, physiology, biochemistry or molecular biology of nerves and nervous tissue and especially with their relation to behaviour, learning and pathology.

Neurological disease: neurological disorders are medically defined as disorders that result in structural, biochemical or electrical abnormalities in the brain and the nerves found throughout the human body and the spinal cord.

Neuron: the basic working unit of the brain, a specialised cell designed to transmit information to other nerve cells, muscle, or gland cells.

Neuropsychiatric disease: neuropsychiatric disorders are clinically recognised conditions in which an individual's thoughts, perceptions, emotions and/or overt behaviour cause suffering and interfere with the individual's daily life.37

BY

Álvaro Nuno Perez

Michel Le Bars

Jose Suarez

The authors would like to thank Jurga Mituzaite and Moritz Waelchli of Deloitte Switzerland for their support on data analysis, as well as Karen Taylor of the Centre for Health Solutions for her comments on earlier versions of the manuscript.

Cover image by: Stephanie Sciberras