2026 Engineering and Construction Industry Outlook

In the face of a dynamic mix of challenges and opportunities, resilience and a willingness to innovate can help companies position themselves for success in 2026

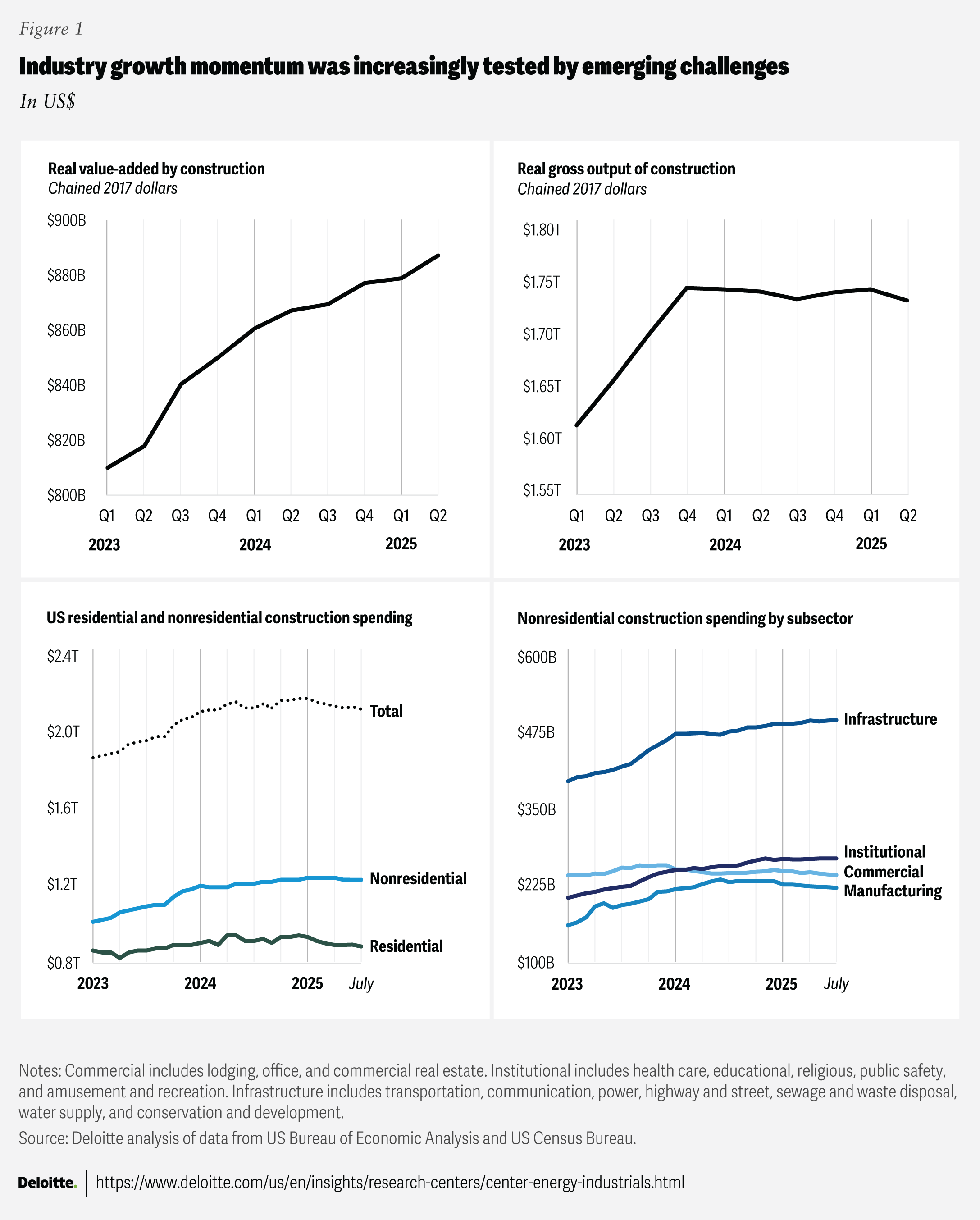

In 2025, the engineering and construction industry’s early growth momentum was increasingly tested by emerging challenges as the year progressed: Real value added climbed to US$890 billion in the second quarter—a 1% increase year over year—while real gross output reached US$1.732 trillion, reflecting a 0.6% fall.1 By July, total construction spending declined almost 3% year over year, primarily driven by downturns in commercial (–8.2%) and manufacturing (–7%) construction (figure 1).2 At the same time, firms grappled with persistent inflation, elevated interest rates, tariff uncertainty, acute labor shortages, supply chain disruptions, and material price spikes, contributing to tightened margins and stretched schedules.

Despite challenges, there were notable areas of optimism: A surge in artificial intelligence–driven data center construction and associated focus on energy infrastructure led to segment growth. Advanced manufacturing, health care, and defense activities hinted at selective growth opportunities.3 Investment in structures is projected to pivot from a 2025 decline to modest growth (nearly +1.8%) in 2026, with AI-related data center outlays continuing to support engineering and construction (E&C) work.4

The E&C industry enters 2026 confronting rising material costs, persistent labor shortages, and shifting project demand. Meanwhile, digital transformation, data center expansion, and strategic mergers and acquisitions are reshaping project sourcing, financing, and delivery.

Against this backdrop, E&C firms may consider focusing on four key trends when planning their growth strategies.

- Evolving tariffs: Building resilience against supply chain disruptions and rising material costs

- Shifting priorities: Growing focus on data centers and energy infrastructure to drive E&C’s next wave

- Embracing digital transformation: Innovating to optimize capacity, cost, and competitiveness

- Persistent talent shortage: Leveraging digital and workforce innovation to unlock opportunities

1. Evolving tariffs: Building resilience against supply chain disruptions and rising material costs

Recent tariffs, especially on steel and aluminum, reaching up to 50%5—have sharply raised construction material costs.6 The effective tariff rate for construction goods climbed to a 40-year high of 25% to 30% in 2025.7 The financial impact is evident: Material prices have risen steadily from May through August 2025.8

With E&C firms already operating on narrow margins, facing customer price and schedule sensitivity, or both, these increases, and associated procurement delays are acutely felt. Tariffs have intensified this pressure, compelling firms to adopt new risk management and procurement strategies. Elevated costs are also affecting both ongoing and future projects—with an 88.2 % YoY increase in project abandonment activity for August 2025; this has led developers to revisit budgets and adjust financial projections.9 Industry research indicates that increased tariffs on building materials like lumber could pose additional challenges to affordability.10

According to a survey by Autodesk, nearly half of E&C firm executives classify their supply chains as “fragile due to geopolitical tensions,” a figure that continues to rise.11 In response to these challenges, E&C firms are shifting from ad hoc procurement to more systematic approaches. Many are pursuing “no-regret” strategies that deliver value regardless of how trade policies or market conditions evolve. These include:

- Strategic stockpiling to buffer against price swings

- Material substitution (for example, using cost-effective alternatives in place of traditional materials)

- Vertical integration and domestic sourcing to reduce exposure to tariff risk

- Supplier diversification and collaborative scenario planning to enhance resilience

- Outsourcing of procurement functions, often via engineering, procurement, and construction contracts or hybrid models, to leverage specialized expertise and improve cost predictability12

- Adopting advanced digital platforms that integrate tariff data, freight information, and material forecasts for predictive purchasing

Contract language is evolving as a resilience tool against tariff uncertainty. Many mid-market builders are incorporating tariff-adjustment or escalation clauses to pass cost increases directly to project owners.13 Where such clauses are absent, contractors operating under fixed-price agreements bear the full impact of tariff-related cost pressures, often resulting in project delays or redesigns.

With tariffs likely to remain elevated through 2026, firms are prioritizing strategies like increasing US sourcing, investing in cloud-based supply chain visibility, and using formal indexed pricing tied to published cost benchmarks. Tariffs are also affecting project timelines and construction spending, squeezing smaller contractors. By transforming macroeconomic uncertainty into a controllable variable, these organizations can model, hedge, and ultimately leverage tariff impacts for competitive advantage as trade policies evolve.

2. Shifting priorities: Growing focus on data centers and energy infrastructure to drive E&C’s next wave

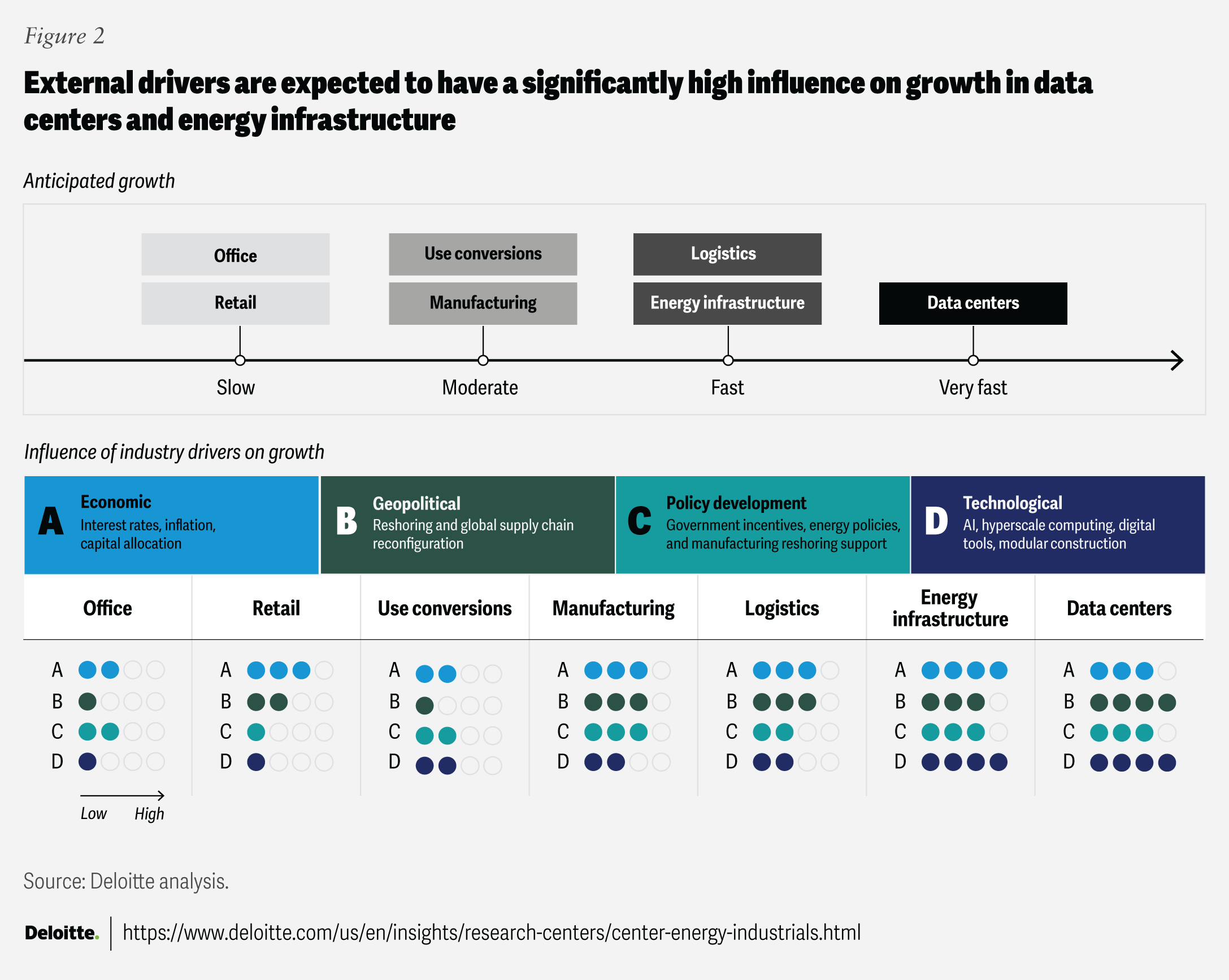

Construction priorities are undergoing a fundamental shift, driven by a dynamic mix of social, economic, technological, geopolitical, and policy developments, affecting both demand and project economics (figure 2). The focus has notably shifted from sustainable energy initiatives toward data centers and the infrastructure necessary to support them. This change is driven by the explosive growth in AI and hyperscale computing, which are altering labor and resource allocation across the industry.

Many large E&C companies are reassessing their project portfolios to align with these new priorities, investing in capabilities to compete for mega-projects such as data centers and advanced energy facilities. They are also looking to strengthen their insights and partnerships around emerging power-generation and cooling technologies, driving a competitive advantage as they engage with hyperscalers and data center developers.

They are increasingly leveraging digital tools, modular construction, and strategic partnerships to manage complexity and scale. Meanwhile, mid-market companies, which do not possess the scale or specialization to compete for large projects, are focusing on operational improvements, workforce development, and digital adoption to remain competitive. Recent spikes in commercial planning activity, following months of cautious inactivity, suggest that the market may be on the verge of moderate growth in construction spending despite ongoing uncertainty. In August 2025, commercial and institutional planning activity increased by 30% year over year.14

While overall commercial construction activity has slowed for much of 2025, data centers and energy infrastructure have surged. This boom is fueled by the rapid adoption of AI, increased demand for cloud services, and the exponential rise in energy needs for data centers.15 By 2035, Deloitte estimates that power demand from US data centers could grow more than fivefold, to 176 gigawatts from 33 gigawatts in 2024.16 AI data centers, with their commensurate power needs, will account for most of the increased demand—potentially growing more than thirtyfold, reaching 123 gigawatts. Government policies supporting the reshoring of US manufacturing have led to an increased focus on new manufacturing construction activity. Although several large projects have been announced, overall activity remains subdued as businesses weigh construction timelines, material costs, and the re-establishment of supply chains before making significant commitments. Office, retail, and mixed-use properties are expected to see moderate, regionally driven growth. Additionally, demand for property conversions—primarily from office to residential—remains strong in areas with high vacancy rates.

Looking ahead to 2026, the outlook for commercial construction activity is cautiously optimistic, with data center and energy infrastructure expansion providing continued momentum. Projects in early planning stages could be affected by signs of evolving government policies or economic slowdown. Interest rates, inflation, and consumer sentiment will likely be closely monitored by developers of manufacturing, retail, and office properties. Conversely, signs of rapid economic strengthening or targeted government incentives could accelerate activity.

3. Embracing digital transformation: Innovating to optimize capacity, cost, and competitiveness

The E&C industry is at a pivotal moment, facing surging demand across sectors like data centers, grid-modernization megaprojects, and advanced manufacturing.17 This growth, fueled by several major federal legislative initiatives and programs, along with strong private investment, presents significant opportunities and formidable challenges. Margin pressures from tariffs, volatile material costs, and ongoing supply chain disruptions are intensifying the potential need for firms to rethink traditional operating models.

E&C firms are increasingly leveraging advanced digital tools to boost productivity, protect margins, and adapt to rapidly changing market conditions. Leading organizations are deploying technologies such as AI-driven analytics, real-time project management platforms, and connected jobsite solutions to streamline operations, enhance decision-making, and stand out in a competitive landscape.

- Agentic AI: Many firms are piloting agentic AI systems to autonomously manage complex scheduling, coordinate workflows, and mitigate risk. These tools can help project teams anticipate disruptions and respond quickly to changing conditions.18

- Computer vision and safety analytics: The adoption of safety-focused computer vision technologies is transforming site safety. Many hazards can now be identified in seconds, improving compliance and reducing incident rates. Real-time safety analytics are becoming increasingly important, especially for firms competing for large federally funded projects.

- Building information modeling (BIM), 3D printing, and digital twins: Digital workflows, integrating BIM, 3D printing, and digital twins, are streamlining project delivery. These technologies enable more accurate project planning, minimize rework, and accelerate schedules, with timeline reductions of up to 20%.19

- Internet of Things devices: The integration of IoT devices, supported by 5G connectivity, is transforming asset tracking and predictive maintenance. Real-time equipment data helps minimize downtime and optimize resource allocation, especially on complex projects.

- Autonomous equipment and robotics: Autonomous machinery and robotics are moving from pilot programs to early-stage deployment. These technologies can help address labor shortages, improve safety, and automate repetitive or hazardous tasks, allowing firms to scale operations more efficiently.

Despite these advanced technologies, poor-quality data continues to frequently undermine the reliability of analytics and AI solutions,20 reducing the return on investment and limiting both operational and competitive advantage. Robust data governance frameworks can help organizations realize the full benefits of digital tools.

As E&C firms plan for digital initiatives through 2026, technologies like cloud-native digital twins and AI agents are expected to become standard. To fully capitalize on the digital dividend, firms should institutionalize data governance frameworks, invest in continuous workforce development, build ecosystem partnerships, and embed digital performance metrics throughout project delivery.

4. Persistent talent shortage: Leveraging digital and workforce innovation to unlock opportunities

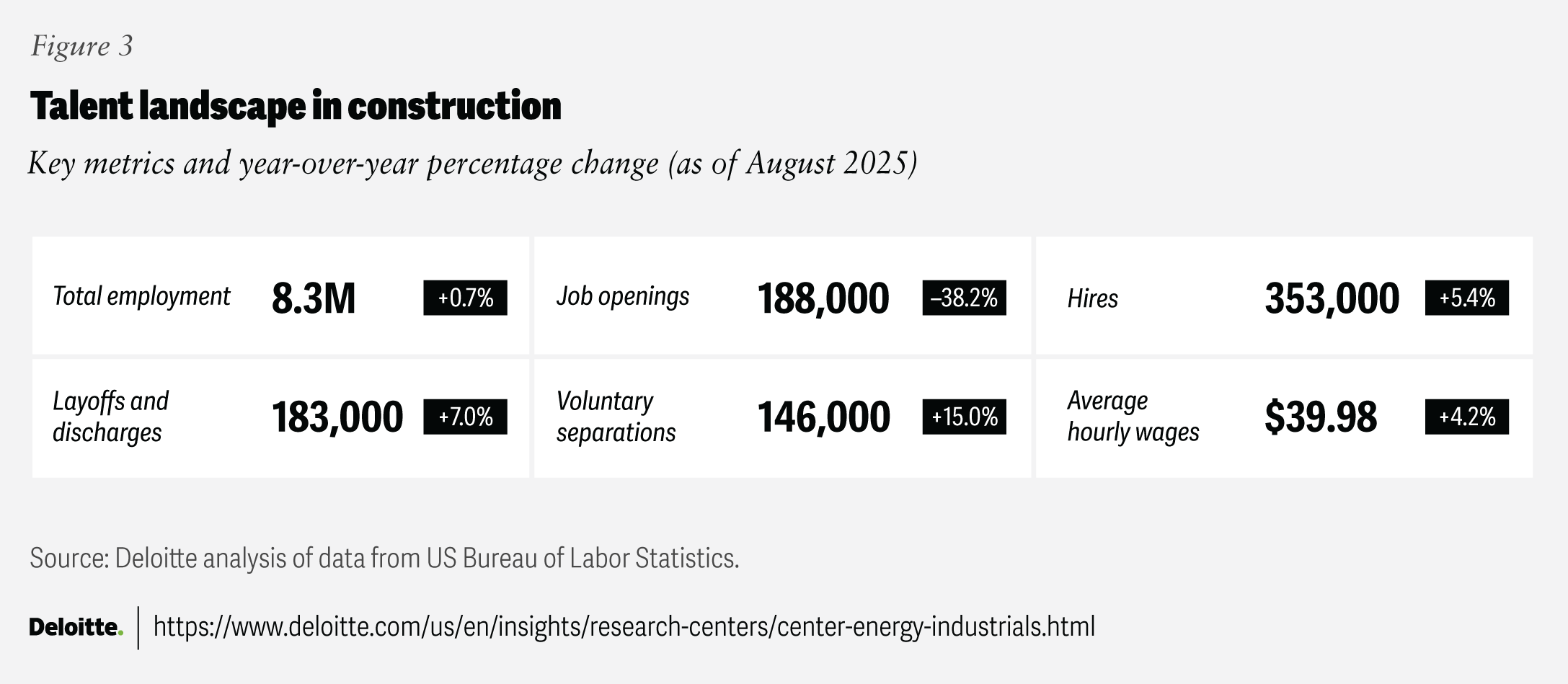

The E&C industry continues to face significant labor shortages, a challenge expected to intensify by 2026—with a projected need for 499,000 new workers, up from 439,000 in 2025.21 Without strategic initiatives to broaden and upskill the talent pipeline, the industry risks exacerbating project delays, cost overruns, and margin pressures.

The economic repercussions of labor shortages in E&C are already evident and expected to intensify (figure 3). Construction wages have increased 4.2% year-over-year as of August 2025.22 If the labor gap persists, the industry could potentially lose nearly US$124 billion in construction output due to unfilled positions.23

Structural factors continue to limit labor supply. By 2031, 41% of construction workers are expected to retire, while only 10% of current workers are under 25, signaling a critical shortage of younger talent entering the field.24 Interest in construction careers remains tepid, with only 7% of potential job seekers considering this field. Additionally, the migration of engineering talent to technology firms—driven by demand for tech-enabled skills—is intensifying competition for skilled workers.25

The surge in large-scale projects in sectors such as data centers, energy storage, and semiconductors will likely draw a disproportionate share of skilled workers, including electricians, welders, and heating, ventilation, and air conditioning technicians, further straining the labor pool.26 Projections indicate a potential shortage of over two million skilled craft professionals by 2028 if current trends persist.27 Monitoring the demand for electricians, welders, and design engineers across industrial, energy, and infrastructure projects can help identify scheduling bottlenecks and mitigate labor gaps.28

Immigration policies will likely remain a critical factor, as nearly 10% of construction and extraction workers are foreign-born, according to the US Bureau of Labor Statistics.29 Changes in visa regulations and immigration policies could further restrict labor availability in the industry.

In response to mounting challenges, firms are expected to accelerate investments in digital tools and automation, including autonomous equipment, robotics, AI-powered scheduling, and prefabrication where feasible.30 These technologies are rapidly permeating engineering functions, where AI-driven design tools and augmented reality field instructions facilitate “learn-as-you-install” workflows.31 While such tools can help reduce reliance on manual labor, they are also increasing demand for skilled talent such as data scientists, digital engineers, and specialists capable of managing AI-driven insights.32 This rising need for highly skilled digital talent is forcing firms to compete with each other as well as with technology companies.

The current administration has announced plans for workforce reform33 and is directing all federal workforce programs to modernize, integrate, and realign to address critical workforce needs in emerging industries.34

Moreover, as the E&C workforce requirements shift from traditional craft roles toward factory-based technicians and digitally skilled operators, firms may need fresh human resources strategies, ranging from rethinking onboarding and retention models to redesigning career pathways.35 Without sustained action, labor constraints may limit the industry’s capacity to deliver on critical infrastructure, data center, and housing projects in the coming years.

Thriving through transformation: Building resilience and agility for 2026

Looking ahead to 2026, the E&C industry faces a dynamic mix of challenges and opportunities. Persistent labor shortages, rising material costs, and economic uncertainty continue to challenge firms’ resilience. However, organizations willing to adapt and innovate may be well positioned to thrive. Embracing digital transformation can help firms overcome inefficiencies and labor constraints, improving project delivery and operational performance.

Financial agility will be equally integral to strategy. Firms that maintain liquidity, manage debt wisely, and leverage legislative incentives will be better equipped to respond to market shifts. Strategic M&A, especially those that strengthen digital capabilities, offer additional pathways to growth and competitiveness.

Success in 2026 will likely depend on resilience against market volatility, flexibility toward changing priorities, and commitment to innovation.

Future in focus: AI’s transformative impact on engineering and construction

Although the E&C industry has historically been conservative in adopting new digital technologies, AI is expected to drive a profound transformation over the next few years. This shift will redefine how work is delivered, moving from a labor-intensive, fragmented industry to a digitally enabled and augmented ecosystem.

AI-driven tools will optimize designs, automate calculations, and manage schedules in real time, enabling smarter and faster project outcomes. On construction sites, automation will become increasingly visible, partially addressing labor shortages, enhancing safety, and improving performance. As AI integrates into everyday workflows, firms can see improvements in cost estimation, risk management, and decision-making, helping them to anticipate and resolve issues before they escalate. This technological adoption will potentially redefine the competitive landscape: large enterprises may benefit from scaling digital capabilities into their operations, while mid-market firms can thrive through agility and strategic partnerships. However, those slow to adapt risk rising costs, shrinking margins, and strategic irrelevance.

Access the archive

- 2025 Engineering and Construction Industry Outlook

- 2024 Engineering and Construction Industry Outlook

- 2023 Engineering and Construction Industry Outlook

- 2022 Engineering and Construction Industry Outlook

- 2021 Engineering and Construction Industry Outlook

- Midyear 2020 Engineering and Construction Industry Outlook

- 2020 Engineering and Construction Industry Outlook

Continue the conversation

Meet the industry leaders

Steve Shepley

Michelle Meisels

Kate Hardin

By

Michelle Meisels

Patricia Henderson

Sami Alami

Kate Hardin

Scott Welch

Kruttika Dwivedi

The authors would like to thank Anuradha Joshi for her key contributions to this report, including research, analysis, and writing.

Deloitte advisory board: Anand Desai, Hogan Miller, Jeffrey Kummer, Kuttayan Annamalai, and Victor Reyes

The authors would like to acknowledge the support of Clayton Wilkerson for orchestrating resources related to the report; Kimberly Prauda and Neelu Rajput, who drove the marketing strategy and related assets to bring the story to life; Alyssa Weir for her leadership in public relations; and Pubali Dey, Harry Wedel, Anu Augustine, and Aparna Prusty from the Deloitte Insights team who supported the report’s publication.

Cover image by: Pooja Lnu

Visit the Deloitte Center for Energy & Industrials

Access more insights for the aerospace & defense, chemicals & specialty materials, engineering & construction, mining & metals, oil & gas, power & utilities, and renewable energy sectors.