INDIA ECONOMIC OUTLOOK, JULY 2026

India’s trade deals will matter more than ever amid uncertainties

India’s growth outlook faces a volatile global environment, making free-trade agreements and industrial reforms crucial to continued economic resilience

India’s macroeconomic outlook seemed relatively favorable at the start of 2026: Inflation had moderated to 2.1%, its lowest level in years; the Reserve Bank of India (RBI) was contemplating further monetary easing; relief from higher US tariffs and supply-chain uncertainties had boosted investor confidence; and robust domestic demand and resilient growth prompted the RBI governor to describe India’s economic position as a “Goldilocks” phase.

The geopolitical arena has since become more complicated, with the Middle East conflict serving as the latest reminder that geopolitical tensions pose a key risk to global economic stability.

The hostilities underscored the fragility of the RBI’s macroeconomic assumptions, leading it to downgrade its growth projections and raise its inflation expectations, as higher energy prices and trade disruptions due to the blockade of the Strait of Hormuz trickle into the economy.

While the memorandum of understanding signed by the United States and Iran did reduce immediate concerns, structural vulnerabilities associated with an increasingly uncertain geopolitical environment persist. Despite entering the 2026 from a position of relative macroeconomic resilience, India now faces major global headwinds. Deloitte now expects a modest growth rate of 6.5% to 6.8% this fiscal.

But crises often present opportunities:

- The government will likely effect structural reforms to enhance India’s economic resilience, both externally and domestically. India’s recent free-trade agreements (FTAs) will form an important pillar of that strategy.

- Beyond improving market access, these agreements will seek to expand India’s export footprint in high-potential markets, diversify access to critical imports, and strengthen supply-chain resilience.

But these must be complemented by conducive industrial policy and an enabling ecosystem that can drive domestic value addition and progressively reduce India’s import dependence, given many of India’s strategic manufacturing sectors continue to rely heavily on imported inputs. The right industrial policy reforms can help the economy to integrate more effectively into global value chains while lowering its vulnerability to geopolitical and supply-chain disruptions.

Table of Contents

- Growth recap

- Seven headwinds shaping the outlook

- Free-trade agreements

Fiscal 2025 to 2026: A growth recap

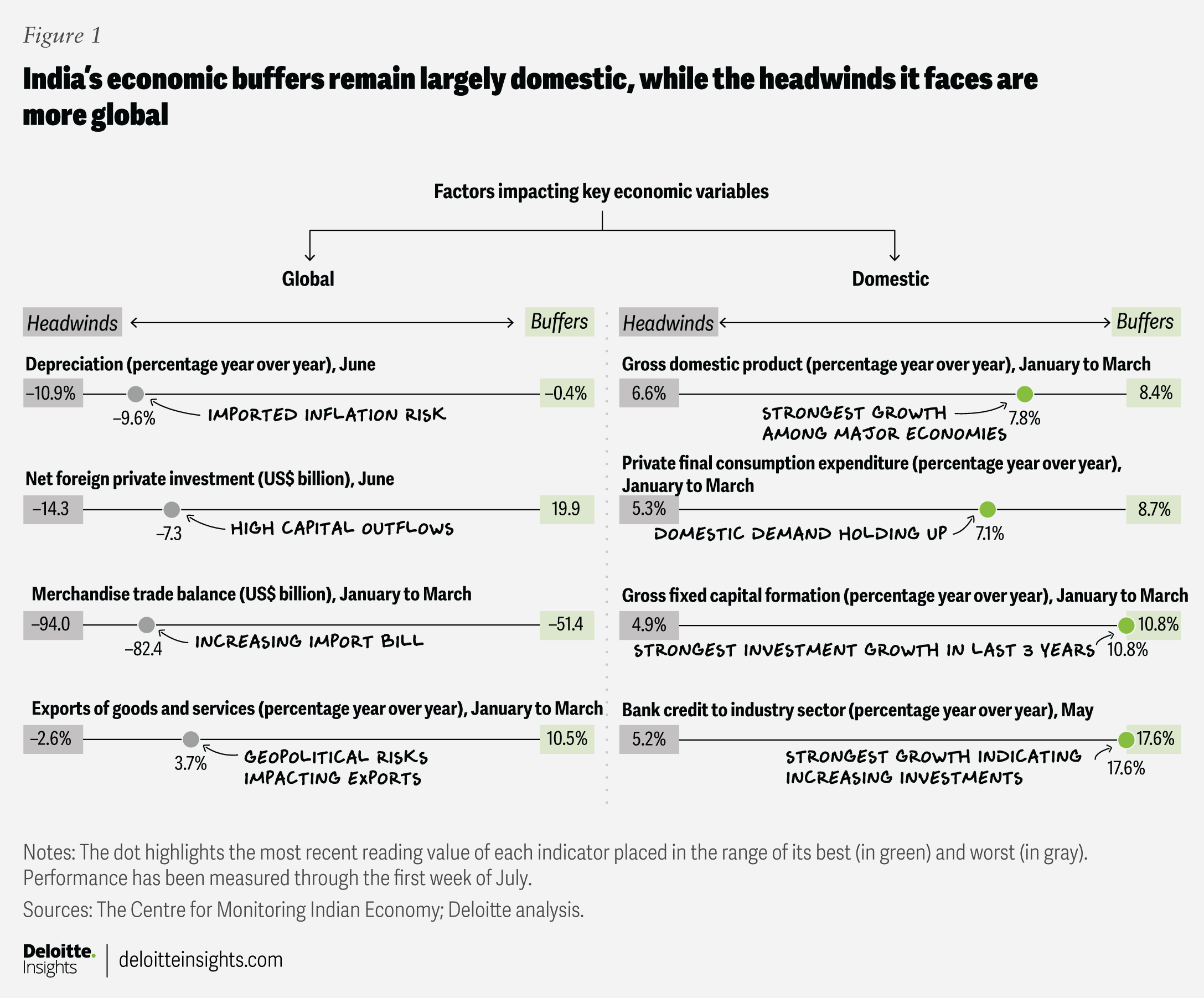

In the last fiscal,1 real gross domestic product growth stood at 7.7% year over year (figure 1), beating the government’s first advance estimate (7.4%).2 Growth remained robust in the final quarter (7.8%), indicating resilient domestic demand amid a challenging global backdrop. Real gross value added (GVA) expanded even faster (7.9%), pointing to strength on both demand and supply sides.

The expenditure side of GDP was largely driven by domestic demand.

- Private final consumption expenditure remained resilient, growing 7.1% in the last quarter of fiscal 2025 to 2026, with the Retailers Association of India reporting retail growth of 10% and 9% in March and February, respectively. For the entire fiscal, private final consumption expenditure grew 7.7%, supported by tax incentives, disposable income gains, and stronger purchasing power.

- Investment remained strong, with gross fixed capital formation rising 10.8% in the fourth quarter and 8.2% for the full year. Public capital expenditure did most of the heavy lifting here.

- Exports softened, rising by 3.7%, while imports were up 1.9% in the last quarter, as shipping disruptions due to the Middle East conflict weighed on economic activity in March. For the full year, exports were up 6.3% while imports rose 5.6%, helped by trade frontloading amid US tariff–driven uncertainty.

India’s merchandise trade deficit widened to US$776 billion, but services exports of US$421 billion and remittances worth US$143 billion helped cushion the overall external balance. India also retained its position as the world’s eighth largest services exporter in 2025.3

On the production side, growth was driven by strong performances in both manufacturing and services.

- Manufacturing showed strong performance through the year, with GVA rising 10.7% for the whole year, despite moderating to 7.3% in the fourth quarter.4 The index of industrial production pointed to strong growth in capital goods (11.8%) and infrastructure goods (9.2%).

- Services were the main growth pillar, with the tertiary sector growing the fastest—9.9% in the last quarter and 9.3% for the full year—driven by strong performances in trade, hotels, transport, and communication (11%).

- Growth moderated in the agriculture and allied activities sector, reaching 3.6% in the last quarter and 3% for the full fiscal. But this did not translate into weaker rural demand: Strong two-wheeler sales (up 13.2% year over year), tractor sales (up 19.2%), and growth in the fast-moving consumer goods sector (up 4.6% in rural areas versus 3.1% in urban areas)5 for fiscal 2025 to 2026 pointed to a healthy rural economy despite softer growth in agricultural GVA.

Inflation fell to a multiyear low as food and fuel prices eased, aiding consumer spending. This also resulted in a subdued GDP deflator, keeping nominal GDP growth at 8.9%.

Fiscal 2026 to 2027: Seven headwinds shaping India’s economic outlook

While India ended the last fiscal with strong momentum, vulnerabilities like capital outflows and currency depreciation persisted. Toward the end of the fiscal, these headwinds intensified due to the Middle East conflict.

Entering the new fiscal, India’s growth outlook is increasingly exposed to external headwinds and macro financial risks. Performance in fiscal 2026 to 2027 will likely be shaped by several key risks.

- Capital-flow volatility: In the last fiscal, India saw strong foreign portfolio investment outflows of around US$18 billion due to higher US tariffs and geopolitical uncertainties.6 Such outflows surged to US$21.6 billion between March and April 2026.7 We expect the volatility to ease, as reduced uncertainty partly improves investor sentiment, post the signing of the US-Iran agreement. While there might be intermittent disruptions to global supply chains, investors will increasingly factor them into their decision-making.

- Currency depreciation: A worsening payment balance (driven by capital outflows and a widening of merchandise deficit) weighed heavily on the Indian rupee, which depreciated by nearly 10% against the US dollar and over 15% against the euro during the last fiscal. Following the start of the Middle East conflict, higher oil import risks, the strength of the US dollar, and tighter global financial conditions caused the rupee to depreciate further, reaching an all-time low of 96.8 rupees per US dollar in May 2026.8 It has since regained some of its lost ground and is now hovering above 94 per US dollar. With capital flows expected to improve and the RBI building its foreign reserves, the rupee will likely remain in the range of 94 to 96 per US dollar till the end of the year.

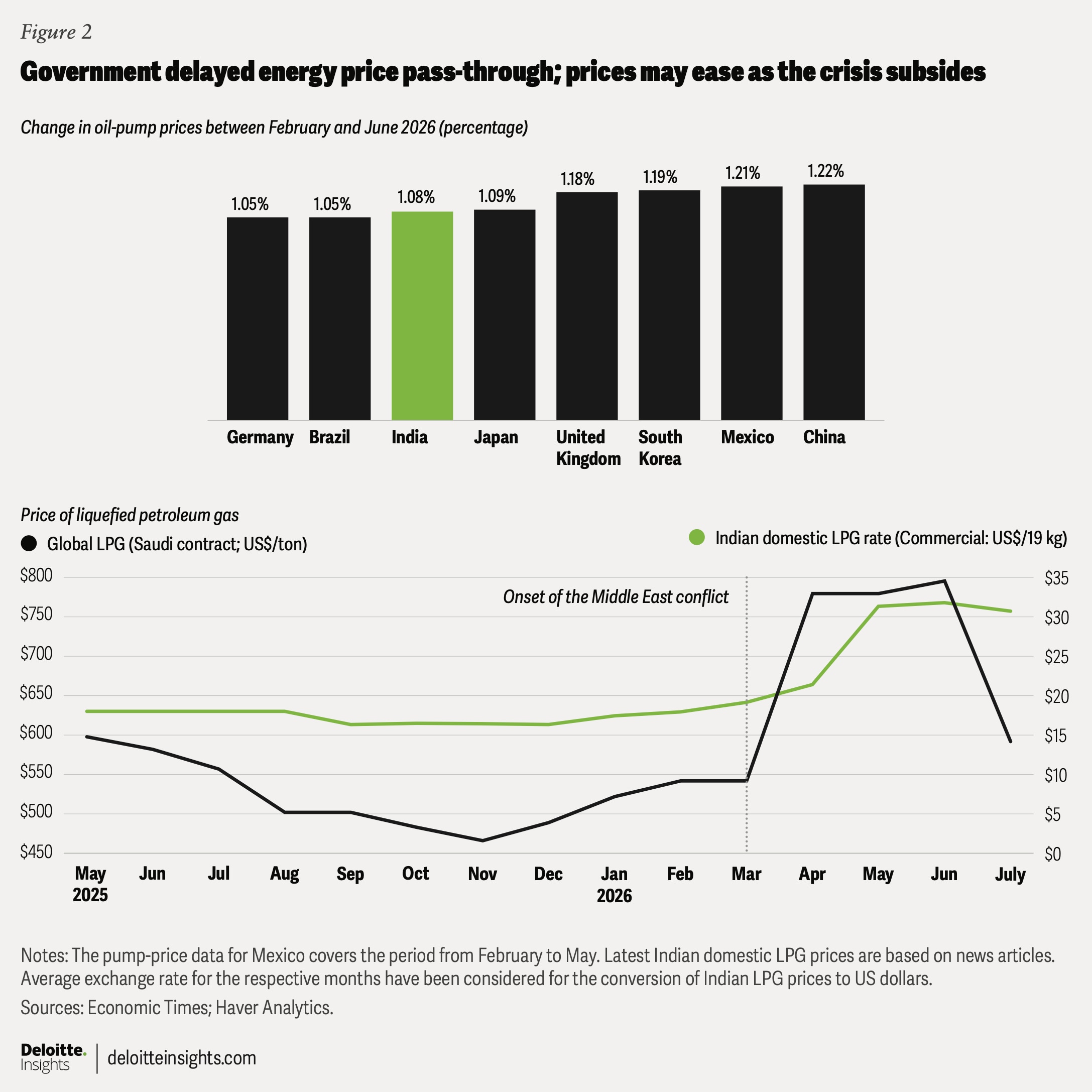

- Inflationary pressures: Rising prices of crude oil, essential minerals, fertilizers, and palm oil, combined with a depreciating currency, added to costs for India’s agricultural and industrial sectors. Government partly cushioned the domestic economy through fiscal measures, including delayed fuel-price pass-throughs, higher fertilizer subsidies, and support for essential inputs like liquefied petroleum gas (figure 2).

Despite these measures, the wholesale price index inched up to 8.2% in June due to higher fuel, freight, and input costs, while the consumer price index rose to 3.9%. While many of these concerns may subside post the US-Iran peace agreement, the impact of El Niño on food supplies and prices could prove to be a significant shock, as the monsoon rainfall deficit reaches a record high at 43%.9

With inflation having moderated to 2.1% in the last fiscal, a low base effect is expected to push it up to 5.5% in fiscal 2026 to 2027, before it eases to 4.2% the following fiscal. - Fiscal pressures: Government interventions have helped contain inflation and support consumer spending but also shifted part of the external shock burden onto public finances. Subsidy spending rose sharply, accounting for 23% of the annual budget allocation between January and March 2026, highlighting the growing trade-off between macroeconomic stability and fiscal prudence.10 The new year began with continued stress on the government’s balance sheet as revenue expenditure reached 18% of the budgeted allocation in April and May 2026, compared with 13% a year earlier.

Higher subsidies for food production and farming, along with lower revenue buoyancy due to cuts in customs taxes this year, may cause the fiscal deficit to remain elevated. We expect it to be slightly higher than the targeted deficit of 4.3%, although this is unlikely to compromise capital expenditure.

5. Potential delays in the US-India trade deal: The US-India trade deal is in its final phase and will likely help to bring down tariffs on Indian exports to 10%. However, till it is concluded, uncertainty will likely persist. Besides, implementing the arrangement will take time, and it may not come into full effect until the next fiscal.

6. Elevated global inflation and tight monetary policy: Tensions in the Middle East and intermittent disruptions to key trade corridors will likely keep input costs high. Even if freight and insurance markets normalize over the next few quarters, global prices are likely to remain elevated, leading to higher policy rates set by central banks in the West. For example, the European Central Bank announced a rate hike at its June meeting.

7. The RBI’s monetary policy trade-offs: The RBI faces a tough balancing act between promoting growth, maintaining price stability, and keeping currency steady. In June, the RBI kept policy rates unchanged to support credit growth, which has lately improved by 17.7%, the highest level since May 2024, providing a buffer at a time when access to external financing is constrained.

At the same time, the RBI announced five measures to encourage capital inflows, including incentives to attract FCNR(B) deposits11 and exemptions from capital gains tax on government securities. According to a study by the State Bank of India, these measures could bring in US$40 billion to US$45 billion over the next few months and support additional bank deposits of around INR4.5 trillion, thereby boosting banks’ willingness to lend.12

In fact, overseas investors invested a record US$4.2 billion in Indian government bonds in June, marking the strongest inflow into debt instruments since August 2024.

However, if inflation rises due to El Niño effects, the RBI may have to tighten its policy stance. Besides, measures to attract foreign capital will affect the balance sheet, adding risks to liquidity management and long-term financial stability.

Hence, in fiscal 2026 to 2027, economic performance will largely depend on how Indian policymakers navigate an increasingly uncertain external environment without compromising on domestic growth momentum.

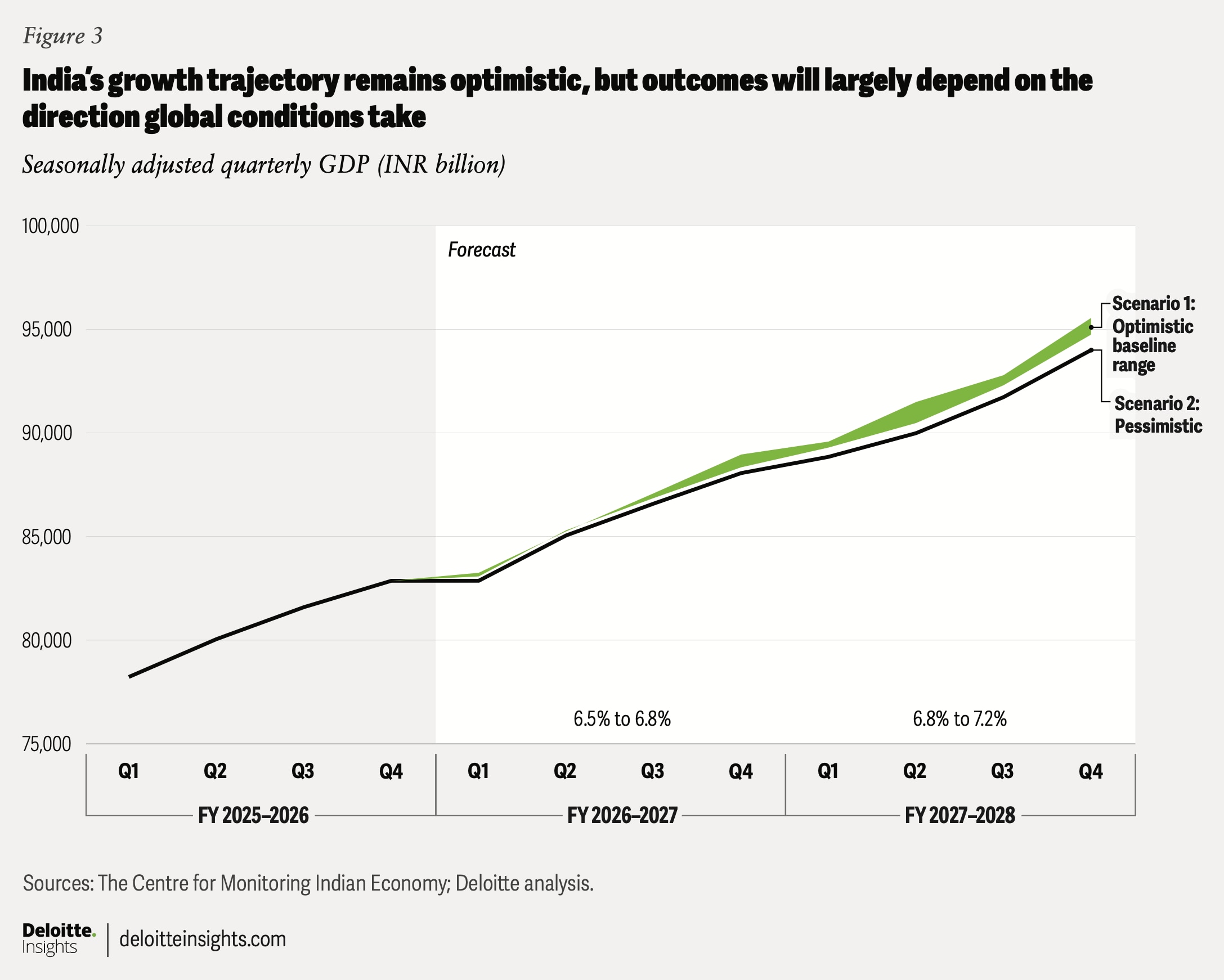

We expect economic growth to remain modest in the first half of the year and pick up in the second half, driven by a demand surge during the festival season (October to December) and the gradual easing of geopolitical uncertainties. Trade deals with the United States, United Kingdom, and the European Union are expected to usher in trade and private investments from 2027 onward.

In Deloitte’s optimistic scenario (see “Key assumptions for Deloitte’s projections” for all scenarios), growth in fiscal 2026 and 2027 is likely to range between 6.5% and 6.8% (figure 3), before crossing 7% in the next fiscal year.

Free trade agreements: Domestic resilience to external resilience in the long term

The recent US-Iran agreement may likely ease pressure on commodity prices and stabilize investor sentiment, but the conflict has drawn attention to the challenges posed by disruptions in geopolitically sensitive trade corridors.

Building durable external resilience will, therefore, require more than just strong domestic demand—it will also require a stronger trade architecture. In this context, India’s recent FTAs and ongoing trade negotiations assume greater significance.

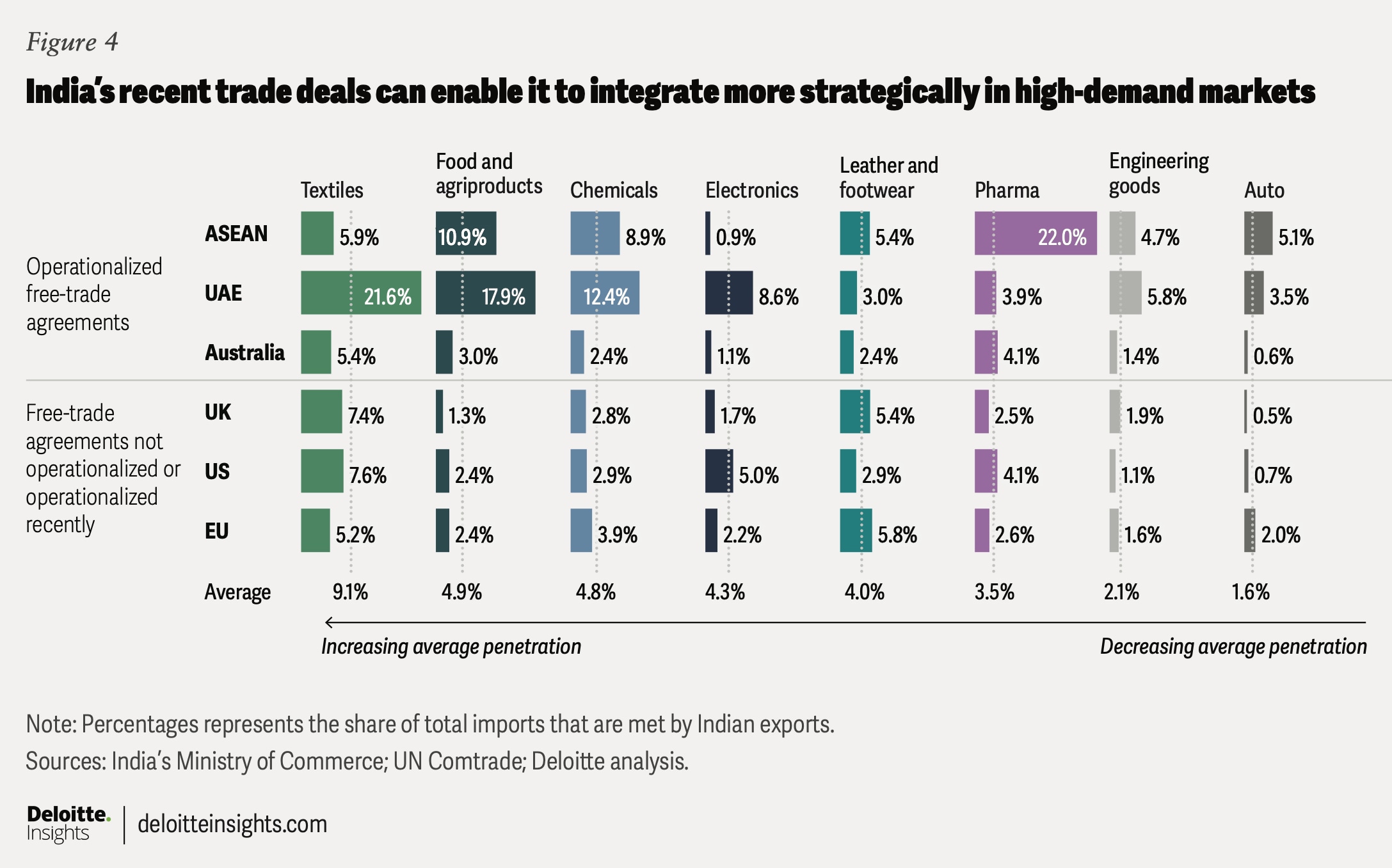

Over the past two decades, India has signed 22 FTAs, eight of them in the last six years, reflecting a more strategic approach to trade policy. The newer agreements, built on lessons learned from the earlier ones, are not just about market access. They also aim to expand exports, strengthen supply-chain resilience, and diversify trade. But India also needs the right industrial policy reforms to remain competitive as it integrates with global supply chains.

1. Strengthening India’s export footprint strategically: The newer FTAs seek to align India’s competitive strengths with high-demand markets where its export presence remains limited. Successful partnerships with the United Arab Emirates and Mauritius helped secure a larger share of their import demand, suggesting that tariff preferences, policy certainty, and deeper commercial integration can help players expand their presence over time. Trade with Australia has doubled since the FTA was signed, even though cross-sector penetration remains low due to geographical distance and low economic growth.

India is now seeking to replicate this success with countries whose agreements are yet to become operational or have only recently become operational (figure 4). The agreements with the United Kingdom, the United States, and the European Union could create opportunities in electronics, engineering goods, pharmaceuticals, chemicals, textiles, and auto components—sectors where India has growing capabilities but relatively low market penetration.

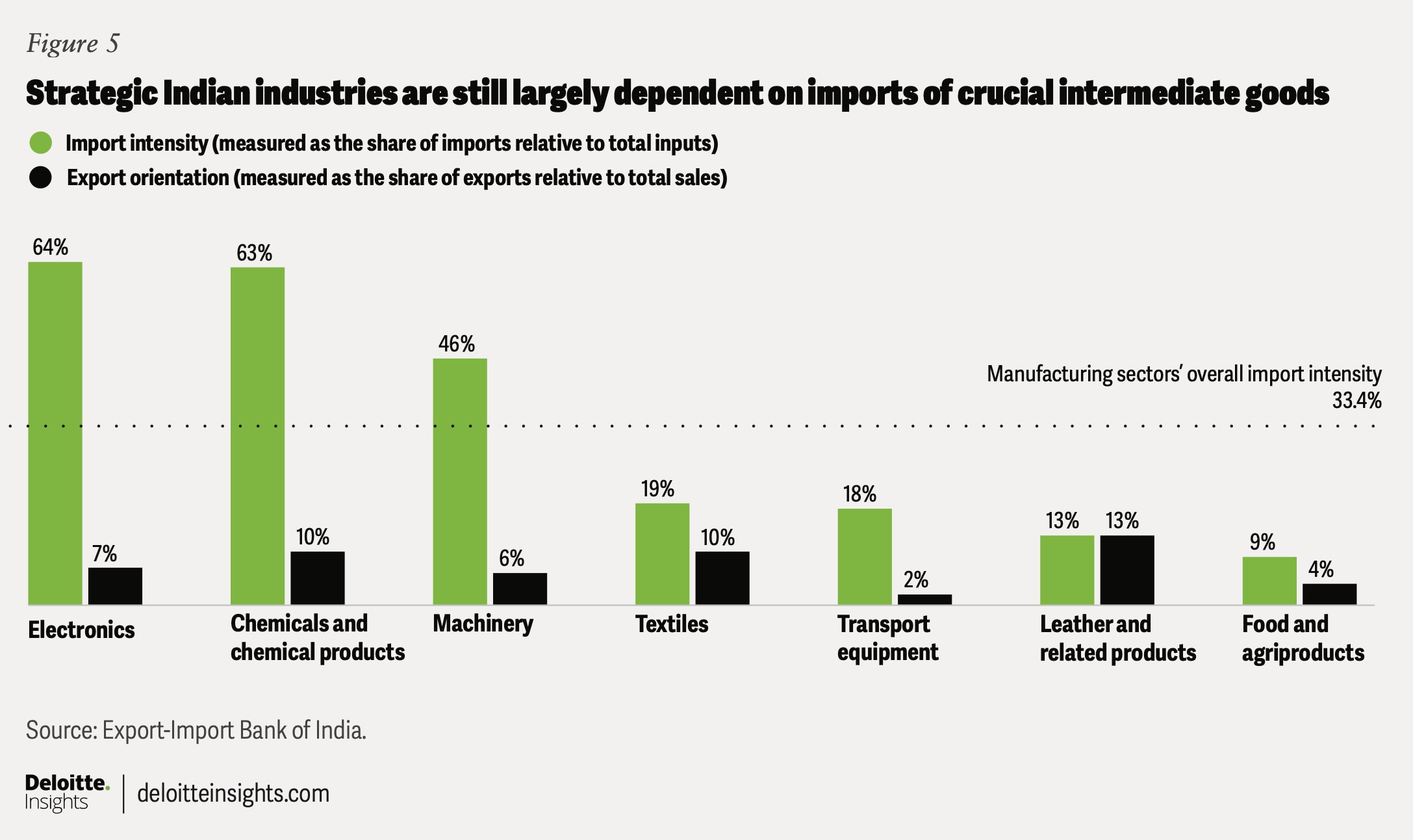

2. Enabling competitive and resilient value chains through strategic imports: India’s FTAs are often criticized for widening trade deficits (for example, the ASEAN agreement saw imports rise faster than exports over time).13 But these concerns do not fully capture the role imports play in modern manufacturing: Sectors like electronics, machinery, chemicals, and transport equipment depend heavily on imported intermediate inputs and subcomponents and currently have higher import intensity than the manufacturing average (figure 5).

For these, FTAs can help secure diversified access to critical inputs, reduce dependence on concentrated sourcing geographies, and strengthen resilience against geopolitical, trade, and logistical disruptions. These agreements complement industrial initiatives such as the phased manufacturing program. Expanding India’s network of sourcing partners will help enable firms to integrate into—and move up—global manufacturing value chains.

3. Reducing import dependence through complementary industrial policy and a supportive ecosystem: Greater import resilience should not be confused with continued import dependence. Over the long term, India’s competitiveness will increasingly depend on reducing import intensity through higher domestic value addition, stronger supply ecosystems, and tech- and innovation-driven improvements in manufacturing capabilities.

o Industrial policy must complement trade policy: FTAs will help integrate India more deeply into global supply chains and diversify access to critical inputs. At the same time, industrial policies such as production-linked incentives, infrastructure development, and domestic capability creation will enable India to gradually substitute imported intermediates with competitive domestic production.

o A stronger enabling ecosystem to effectively implement FTAs: This would require improving the ease of doing business, easier compliance, awareness of the provisions, and efficient logistics to ensure the FTAs that India signs are implemented and utilized to their full potential.

In short, FTAs can help India sell more to the world and buy more securely from it. But trade agreements must go hand in hand with industrial policy and effective implementation. With preferential market access now spanning 38 countries, India has an unprecedented opportunity to leverage this new trade architecture to create economic advantage.

Key assumptions for Deloitte projections

The Deloitte assumptions used in this analysis can be grouped into two scenario buckets—optimistic and pessimistic—with the former being more likely.

Optimistic scenario

The US-Iran agreement helps improve trade and boosts the global economy. With the Strait of Hormuz open, oil and other essential commodity prices ease to prewar levels by the third quarter of fiscal 2026 to 2027. Trade deals with the European Union and the United States become operational by early 2027. El Niño affects agriculture, but not enough to weaken overall output or drive inflation into a spiral.

The other assumptions are:

- The US Federal Reserve keeps policy rates steady and may implement one rate hike by the end of the year. The US economic outlook remains largely positive.

- Various trade deals worldwide bring more clarity around global trade.

- Brent crude falls below US$80 per barrel in the next two quarters and eases further to between US$65 and US$70 thereafter.

- The rupee remains steady against the US dollar at around 94 to 96, reducing import-price pressures and inflation expectations.

Pessimistic scenario

The US-Iran agreement improves trade only marginally as the region continues to experience intermittent escalations and supply-chains disruptions. Regions with ongoing conflicts face prolonged economic uncertainty. Global inflation spikes, compelling the United States and the European Union to go ahead with several policy rate hikes.

Trade-related uncertainty continues, and India’s trade deals with Europe and the United States are delayed. As a result, exports decline rapidly, while supply-chain shocks raise costs and disrupt production. Monetary policy remains tight in both the West and India.

By

Dr. Rumki Majumdar

Debdatta Ghatak

Editorial (including production and copyediting): Arpan Saha, Preetha Devan, and Anu Augustine

Design: Harry Wedel

Knowledge services: Rohan Singh

Visit the Deloitte Global Economics Research Center

Access more insights for the consumer spending, housing, business investment, globalization & international trade, fiscal & monetary policy, sustainability, equity, & climate, labor markets and prices & inflation sectors.