Manchester Crane Survey 2022

Key headlines

The findings

Foreword

In the wake of the global financial crisis, construction activity across the Regional Centre accelerated at pace as Manchester established itself as one of Europe's fastest growing cities. Within the central areas of Manchester and Salford, almost 20,000 new homes have been built over the last 6 years, and 2021 has provided a second consecutive year of record housing delivery across the survey area. In addition, a consistent supply of new commercial development and high levels of foreign direct investment, have helped cement the city as the UK’s most important economic centre outside of London. Whilst there has been a pandemic induced reduction in construction levels during 2021, there remains a healthy pipeline of new offices under construction. As restrictions ease and businesses move away from home working to hybrid working models, momentum is building and the future pipeline is growing with a number of previously approved office schemes being revisited, and new office schemes being prepared, as the industry grapples with the future of work and ESG priorities in a post pandemic world.

The effect of Manchester’s rapid growth cannot be understated. New people in the city centre has supported investment in destination leisure, cultural and entertainment attractions, as well as neighbourhood focused retail and leisure as part of mixed use schemes. This has contributed greatly to the city’s attractiveness as a place to live and has also helped to offset well documented changes within mainstream high street retailing. For both residential and commercial developments, the quality of the retail and leisure offer has become increasingly important as a value driver, featuring heavily in their branding and place making strategies. This sector is being increasingly driven by innovation and new concepts, often led by independent operators.

Population growth in the core of the city has resulted in increasing demand for new areas of public space, including green space, and it is therefore very positive to see major investment in new public space this year, including Manchester City Centre’s first public park at Mayfield. New educational space completions were significant in 2021, including the vast Manchester Engineering Campus Development for the University of Manchester. Major projects across each of the city’s universities support cutting edge research in important economic growth sectors and are key to the attraction of talent as well as equipping that talent with the skills needed to support the city’s growing and diversifying economic base.

Overall, our latest results demonstrate that Manchester and Salford have been remarkably resilient during 2021 as the world entered its second year of the pandemic. Whilst there has certainly been some rebalancing of market activity over the last 2 years, overall construction levels are well above average for the city. Looking ahead, there are also plenty of new opportunities, with restrictions begin to wane and a healthy pipeline of new developments fuelled by a continued appetite for inward investment in the city. In addition, Government funding is already beginning to unlock a number of complex regeneration projects; however, this is just the start and we can expect to see an increasing focus as we move forward on private sector partners working in collaboration with the public sector to unlock funding and capitalise on the levelling up agenda.

Residential

Cooling down

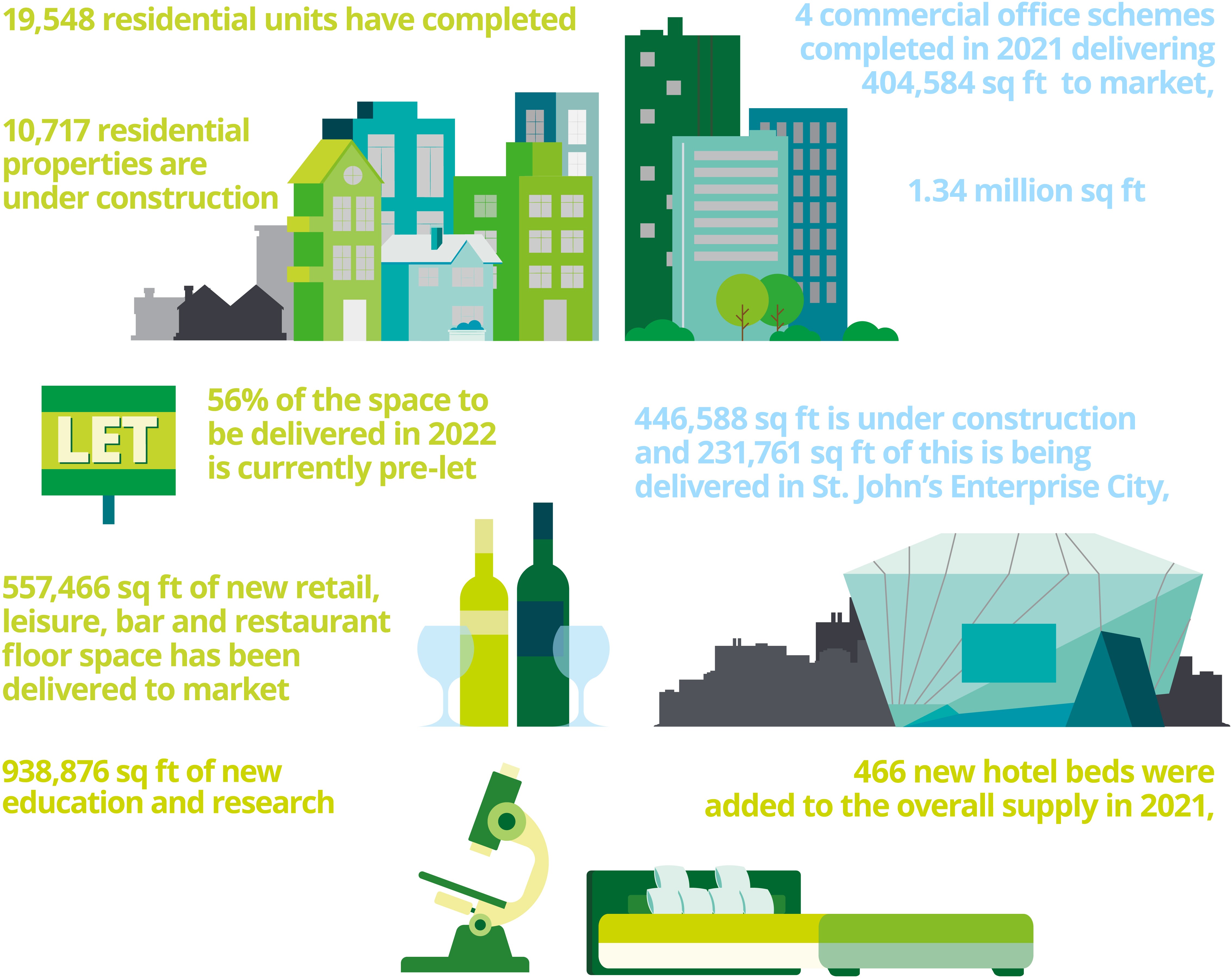

In 2021, 14 new residential developments started on-site, bringing forward the construction of 3,729 new homes. This represents a reduction compared to 2020, when 16 new schemes commenced to bring forward 4,698 new homes. Overall, the number of new homes under construction at year end 2021 was 10,717 across 40 sites, a reduction of 14% in comparison with the 12,322 units across 46 sites at year end 2020.

Whilst still achieving robust build-out rates for new residential developments, these figures suggest that the residential market is gradually cooling. The overall volume of residential properties under construction remains high but has been falling gradually from a peak of 14,480 at the end of 2018.

In part, the lower volume is a result of an increase in the number of residential schemes being completed each year. During 2021, 5,642 new homes for rent and sale were delivered to market – a second consecutive record year for delivery, and a 14% increase on the 4,914 new homes delivered in 2020. The delivery of residential units in the Central Salford area was higher than for any other Crane Survey sub-area, with 2,983 new homes, representing 53% of the total amount of residential development brought to market.

On many of the sites that completed in 2021, development has been at a relatively large scale. At 13 of these sites over 200 homes were delivered, which helps to explain the record-breaking figures for completions.

Residential placemaking and strong take up

The strong residential delivery in Central Salford is supported by new public realm and placemaking activity, and plans are being drawn up for investment in the railway viaduct archways that straddle Chapel Street, following their transfer from Network Rail to Trillium and the Arch Company in 2018. Similarly, Middlewood Locks nearby in Salford has a restored waterside offering in its first phase and looks set to continue this placemaking activity during 2022 in subsequent phases.

In Manchester, the most active area for residential completions is now in the heart in the City Core area, where 677 apartments were completed through Vita’s Affinity Living development alone. This new scheme sits on the edge of the newly-created Symphony Park, an 18,000 sq ft public space connected to Oxford Road hosting both an underground gym and a new Chinese and Vietnamese food market ‘Hello Oriental’.

Significant changes have taken place elsewhere in Manchester, particularly around the Gay Village. Apartments and commercial spaces for shops, bars and restaurants were delivered at Manchester New Square. Further north, Kampus has completed through the restored Grade II Listed Minto and Turner, which provides new apartments, retail opportunities, and pedestrian connections via Little David Street.

Further north, the 35-storey Oxygen development completed on Store Street; and Lampwick, the final plot of the first phase of Manchester Life regeneration, completed at New Islington. Plans were approved in 2021 for further Manchester Life and Great Places schemes as part of the masterplan for the ‘Back of Ancoats’ area. A number of these properties will be offered for affordable ownership: this is a trend that is starting to emerge in several projects led by the Manchester City Council (MCC) and from registered providers.

The Southern Arc, encompassing First Street and Great Jackson Street, had an unusually low number of completions (720 homes) given the sheer amount of development taking place there. Construction has commenced on the second of two towers (Three60) at the 855 apartment Crown Street Phase 2 scheme, which will also provide a new primary school and will be set within a new 0.5 hectare park. Funding for the new school was approved by MCC in October 2021 and will likely complete before 2025, along with the new public space. Further development is expected in Great Jackson Street through Plot F (currently lodged for planning) and Plot G (for which consent has been given): together these will add a further four 50+ residential towers and 1,037 new homes in the area.

Development recommenced in 2021 on what was known as Angel Gate in the Northern Gateway, a site that stalled under previous ownership in 2015. Revised plans have been brought forward by the current landowner, the Far East Consortium, in an enlarged revision of previous proposals now referred to as Victoria Riverside. Along with site clearance and enabling works taking place in and around the River Irk, supported by the Housing Infrastructure Fund, this 634-home development marks the first meaningful new permanent development in the Northern Gateway, where there are plans to build a further 14,000 homes over the next ten years.

Much of this new development is supported by a buoyant rental market, where vacancy rates in new properties remain low. Data suggests that empty property exemptions from rates of about 1% in the city centre. Although this hasn’t changed significantly over recent years, it demonstrates a strong demand for housing in Manchester, even during the pandemic, and reinforces the need for further residential supply across diverse types and tenures.

Whilst we would expect growth in rented residential to continue over the coming years, recent planning applications from registered providers of affordable housing mark a step change in activity. Affordable housing is to be delivered by S106, new development models and government funding through Homes England, which is unlocking development on brownfield sites. Manchester City Council has also recently approved a further £33m of additional spending by the Council on affordable homes through ‘This City’, set up to deliver 500 affordable homes a year.

Office

Working hard

The total volume of office floor space on-site and starting construction in 2021 is similar to 2020, but the amount of floor space delivered to the market was 66% less.

1.34 million sq ft of office floor space is currently under construction across 12 schemes, this is broadly similar to the 1.29 million sq ft under construction across 11 schemes in 2020. The amount of new office floor space starting on-site during 2021 (400,000 sq ft) is also similar to the previous year. However this is spread across five schemes as opposed to three, indicating that new office starts are smaller on average compared to 2020. This shows that activity is has been declining from the second-highest figures ever recorded in the 2018 Crane Survey, when ten schemes started on-site.

St. John's Enterprise City and Central Salford have the highest amount of office floor space under construction. At Central Salford, Four and Five New Bailey will together ultimately deliver over 288,000 sq ft, and 483,000 sq ft will be delivered through as Manchester Goods Yard (320,000 sq ft.), Globe and Simpson (82,900 sq ft), and Old Granada Studios (80,000 sq ft) along with co-working space at Union’s co-living developments.

In 2020 the volume of office floor space completed was 1.2 million sq ft across 8 schemes, well above the annual average, and the second highest year on record (after the 1.4 million sq ft delivered in 2008). This was due mainly to the completion of several large schemes: Number 1 and Number 2 Circle Square; Hyphen; Landmark; and 125 Deansgate. In 2021, whilst 404,584 sq ft of office floor space completed construction across four schemes, 66% less than in 2020, this level of delivery is broadly consistent with volume of completions in both 2018 and 2019 and is only slightly below the average volume for completions each year since 2007 (523,120 sq ft).

The highest number of office completions was in the City Core, including the Lincoln (150,000 sq ft), 11 York Street (89,600 sq ft) and Tribeca House (25,941 sq ft). Three New Bailey also completed in Central Salford, which will provide the headquarters for HMRC’s 2,400 staff for the next 25 years. Looking ahead, the pipeline for completions suggests that an increased amount of amount 745,000 sq ft is set to be delivered to market in 2022 and 575,000 sq ft is in the pipeline for completion in 2023.

60% of schemes that were targeting completion in 2021 have extended their completion dates into early 2022.

For various reasons that affected all sectors to some extent, several schemes that were scheduled to complete in 2021 have been delayed into 2022. In a survey of 857 construction businesses in the UK 80% stated that their projects had been delayed as a direct consequence of COVID-19, with 70% of respondents unable to obtain the goods and services they needed to carry out work.

Offers you can’t refuse

Space delivered in 2021 remains unoccupied but 54% of the office floor space set to complete in 2022 and 30% set to complete in 2023 is already pre-let.

Of the 743,665 sq ft set to be delivered by the end of 2022, 402,900 sq ft is already pre-let to tech and digital businesses. The strong take-up of space at Globe and Simpson (82,900 sq ft) and Manchester Goods Yard (320,000 sq ft) is evidence of a solid appetite for commercial space at St John’s Enterprise City.

A recent Deloitte CFO Survey found that CFOs are placing greater emphasis on increasing capital expenditure now than at any time in the history of the Surveys, with 37% recognising it as a top priority, up from 20% pre-pandemic. This is pertinent to the take-up of office space. Many companies are seeking to understand what the future of work looks like, to help them invest in flexible floor space and leaseholds: for example, short-term office letting options are becoming increasingly popular.

Over 2.8 million sq ft of office floor space is planned to commence construction over the next few years

Other schemes may well commence in 2022 to boost the 21,000 sq ft already lined up to be delivered in 2024. There are a number of major office schemes with planning permission that should bring further office developments across the Crane Survey area over the coming years. These include: the Poulton and Republic at Mayfield (109,727 sq ft and 315,544 sq ft respectively), Electric Park, Pollard Street (505,667 sq ft across five office buildings); 2 and 3 Angel Square (201,356 sq ft and 252,952 sq ft), First Street Plot 9 (270,500 sq ft ), Kendal Milne building (248,775 sq ft) and the adjacent redevelopment of the multi-storey car park site (315,705 sq ft), the Former Rylands Debenham’s Building (297,901 sq ft); Number 3 Circle Square (216,000 sq ft) and The Island Site (88,800 sq ft).

Planning applications have also been submitted at Ralli Quays, New Bailey (190,543 sq ft) and at 50 Fountain Street (55,000 sq ft). Two further office developments, St. John’s Place and No.1 Grape Street, are planned to come forward at St. John’s Enterprise City. There are also emerging plans to develop a new innovation district of about 4 million sq ft of office space in the form of ID Manchester on the University of Manchester’s North Campus site, and plans for 1 million sq ft of office floor space at Central Retail Park.

Plans are also in hand for a new office, known as Alberton, as part of Viadux. Transactions have taken place for Albert Bridge House and New Victoria to support new office schemes being brought forward. Overall, that’s over nine million sq ft of commercial office floor space anticipated for the centres of Manchester and Salford in the coming years, equivalent to 15 years at the average annual delivery since 2007.

The higher number of new starts could be evidence of a greater confidence from developers in the speculative office development market, when compared to 2020

Flexibility in recovery

More than a third (37%) of developers expect homeworking to have no impact on the demand for leasing, three times more than in winter 2020 (12%). Furthermore, only 24% of UK businesses have expressed an intention to increase homeworking going forward. The proportion of individuals only working remotely has also been falling since the 2021 high of 37% in February, dropping by 12 percentage points to 25% in May 2021.

At the same time, 85% of individuals currently working from home have indicated that they would like to use a ’hybrid’ approach in the future, combining both home and office working. The number of days in the offer or at home will vary greatly from employee to employee, however. Evidently, the way in which office space is used has changed and is likely to continue to change, requiring office buildings to be as flexible as possible. Any new regulatory guidance and restrictions on working in the office would inevitably have an impact.

In response to these changes, during the past year there have been initiatives by corporates and office occupiers to improve the employee experience, to attract the best talent. A recent Deloitte survey found that 61% of executives now focus on reimagining work compared to only 29% before the start of the pandemic. Moving forward, we can expect offices to offer more in the way of on-site facilities and amenities to improve employee well-being such as gyms, eateries, roof terraces, and collaborative and entertainment space.

Whilst it may take further time to understand the full implication of demand for office space, it should be recognised that Manchester has a strong economy, with existing and growing clusters of businesses in key sectors.

Manchester is a rapidly expanding tech hub and currently 28% of jobs in the city are within this sector: this is reflected in office take-ups. The average take-up of office space in the tech sector between 2016 and 2020 was 73% higher than the five-year average between 2011 and 2015. The strong take-up of floor space by tech-based companies at St. John's Enterprise City and at Circle Square is testament to the strength of the sector.

With the ever-increasing importance of sustainability and the city’s targets for net-zero by 2038, there is an increasing appetite for both refurbishment and for maximising flexibility and adaptability in new builds.

ESG and the office

Climate change is a core issue for the development industry. Construction, demolition and excavation generated around three-fifths (62%) of total UK waste in 2018, and for new buildings, the emissions from construction can account for up to half of the carbon impacts associated with a building over its lifecycle. In a recent Deloitte CFO Survey, the long-term effects of climate change were ranked by CFOs in the UK as the fourth highest risk to business (after labour shortages, COVID-19 and inflation/bubbles in global asset prices).

Whilst sustainability and the net-zero agenda have jumped up the priority list for potential occupiers, there is also a shift among developers and finance providers. A quarter of developers now expect all their new developments to be net zero by 2024, and 45% expect to achieve this between 2025 and 2029. Only 5% of developers consider that a lack of funding is a problem for the transition to net-zero: a greater problem is lack of support and guidance on how exactly to achieve it.

Although most on-site office schemes are new builds, in 2021 there were three on-site office refurbishments: Calico (11,421 sq ft); the refurbishment of the former Renaissance building on Deansgate; and a warehouse-to -office refurbishment as part of Glassworks. When looking at the pipeline for office developments that are yet to start construction, further office refurbishment schemes are planned by Bruntwood Works at Mosley Street and Pall Mall Court; Thackeray’s 7-9 Piccadilly scheme; and the re-purposing from department stores to offices of the Rylands and Kendals buildings, both Grade II listed.

Since the completion of One Angel Square in 2013, the first BREEAM Outstanding building, several offices in the Crane Survey area have acquired BREEAM Excellent status or better, including Landmark, No. 1 Spinningfields, New Bailey, Circle Square and First Street. Five buildings at MediaCityUK owned by Peel L&P have also been the first to achieve verified operational net zero status.

Demonstrating its commitment to decarbonisation, Manchester City Council has established a new sustainable power network across several buildings in the city centre. The ‘Tower of Light’ is a symbol of this network and MCC’s commitment to reducing carbon emissions and supporting the transition to net-zero by 2038. There are also plans to make Central Retail Park the first net-zero commercial district in the city.

In Manchester developers are working with net zero organisations to establish new policies, and are setting their own objectives and targets. Critically, a universal definition of net zero needs to be adopted and steps must be taken toward improving the energy performance of our existing buildings. The cleanest energy is energy that isn’t consumed.

Hospitality and the visitor economy

Retail and Leisure

The volume of retail/leisure floor space brought to market each year continues to rise, but the total volume on-site is levelling out from the volume in 2019.

A total of 447,588 sq ft of retail and leisure floor space is currently on-site as part of mixed-use schemes across the Crane Survey area. This is only a 7% decrease from the amount on-site year end of 2020, when 481,800 sq ft was under construction. Both years remain well above the annual average since 2007 (160,000 sq ft).

Of the total floor space under construction, 26% (totalling 116,280 sq ft) started on-site in 2021. A substantial proportion of this (29,945 sq ft) is to be delivered through the refurbishment of Islington Mill, creating an art gallery and events space and café. The conversion of New Century Hall into a creative college, with a 1,000-capacity flexible events space and a food hall located on the ground floor, will also deliver 23,322 sq ft of retail/leisure floor space.

The number of retail and leisure completions continues to rise, with 143,848 sq ft of retail and leisure floor space completed in 2021, an increase of 35% from 2020 (106,700 sq ft) and well above the average annual level since 2014 of 64,673 sq ft.

The largest amount of retail / leisure floor space delivered to market in 2021 was within the City Core at developments including The Lincoln (10,000 sq ft), Circle Square (33,000 sq ft) and Kampus (49,000 sq ft). In Central Salford, retail units have been delivered to market at completed residential schemes, including Atelier, The Filaments, and Embankment West, and these will support the large influx of residents to the area in the coming years.

The pipeline for the delivery of further retail and leisure floor space to the market also looks strong with 205,802 sq ft expected to be delivered in 2022, with a further 190,807 sq ft in 2023 and 50,978 sq ft in 2024.

As expected, the area with the largest amount of new space to be delivered in 2022 is also the City Core with 76,318 sq. ft. of retail floor space at developments including London Road Fire Station (37,254 sq ft), Hotel Du Vin (4,232 sq ft) and Maldron Hotel (7,308 sq ft).

St John’s is also set to deliver 60,950 sq ft of new retail and leisure floor space in 2022. With office pre-lets already secured and a strong future pipeline of office and residential development in St. John's, this retail and leisure floor space will provide local amenities to support the creation of a 15-minute city and a vibrant new city centre neighbourhood.

76-82 Oldham Street (20,000 sq ft) will add to the vibrant retail and leisure provision in the Northern Quarter and give confidence to new opportunities in emerging areas like New Cross. In Salford, the delivery of Four New Bailey in 2021 will also provide further ground floor retail (6,028 sq ft) when completed.

Online spending increased from around 9% of total retail sales in September 2011 to about 19% in September 2019 and rose still further during COVID restrictions to 34.5% in March 2020 and then 37% in March 2021. Although the level has fallen as restrictions to shopping in store have eased, online sales have remained high, at 28.1% of all retail sales in September 2021. In response, the redevelopment of department stores offers the potential for renewed and reformatted in-store retail activity at ground floor level, and also provide space for office, hotel, residential and even educational uses. A sustainable and vibrant city is one that is adaptable to change.

However, high streets and town centres are about more than just shopping. Spending on leisure, eating and drinking out is increasing as restrictions are eased, up 6% on the start of 2021 and by 35% from Q3 2020 to Q3 2021. At the same time, there is an increased focus among consumers on localism and supporting independent businesses. This is in evidence at Kampus, Circle Square and Deansgate Square, where many such lettings have been secured by Manchester-based companies, or businesses that have started their journey in Manchester or Salford.

The vibrant independent retail offerings in Ancoats and New Islington will be further supplemented by the completion of units at Lampwick and Mansion House, where all retail units are let to independent occupiers. Elsewhere in the city, road closures and extended outdoor seating in restaurants and cafés has helped to establish concepts such as Freight Island and Ramona.

Hotels and travel

Compared with construction in the previous year there was a 17% decrease in the total number of hotel beds on-site in 2021

There were 1,975 hotel bedrooms on-site in 2021 across eight schemes, a 17% decrease from last year’s volume under construction of 2,397 beds across ten sites. Many of these 2021 hotel schemes are located within City Core, where there are six schemes on-site comprising 1,525 hotel beds in total.

175 hotel beds are on-site at St John's at Old Granada Studios and a further 275 hotel beds are on-site near Manchester Piccadilly Station at the Leonardo Hotel on Adair Street. The largest hotel scheme on-site comprises Motel ONE and Wilde Aparthotel at St Peter’s Square, which is set to complete in early 2022. This is a dual-operated hotel block, which will be split between 328 rooms operated by Motel ONE and 262 studios and one-bedroom aparthotel units operated by Wilde Aparthotels (part of the StayCity brand).

Two new hotel schemes started on-site in 2021, both located within the City Core: the Treehouse Hotel (216 beds) at the former Renaissance site on Deansgate, and Hotel Du Vin (70 beds). Although these schemes will boosted the supply of new hotel rooms to Manchester beyond 2022 and into 2023, the overall volume of new hotel beds on site has fallen by 34% from 2020.

Both these new schemes are refurbishments by new hotel providers. The Treehouse Hotel will not only provide a new brand into Manchester City Centre but will promote sustainability through both the refurbishment of the existing building (as opposed to full demolition), the use of recycled materials, rainwater harvesting, bee hotel and rooftop garden.

The relatively low number of new hotel schemes means that new supply of accommodation, following five-years of increases in the volume under construction up to 2019, is diminishing. This should be viewed against a large uplift in supply in 2017 and 2018 when five new schemes started construction in each year.

Even so, the 1,759 hotel beds expected to be brought to market in 2022 will exceed the highest-ever previously recorded, which was in the 2018 Crane Survey when 840 hotel beds were completed. Completed hotel schemes during 2021 provided 261 beds at Yotel at John Dalton House, 41 beds at Cotton Yard on Chorlton Street and 164 beds at the Moxy Hotel in Spinningfields.

Overall, the number of hotel schemes which started construction in 2021 is only slightly below the average number since 2007 (2.5 schemes), whilst the pipeline for delivery of hotel beds to the market in early 2022 is very strong.

These hotels are advertised as supporting the ‘millennial traveller’, with Yotel and Moxy brands positioned as high-quality and stylish, yet affordable hotel accommodation and with Cotton Yard providing a flexible aparthotel offering.

As in the rest of England, hotel occupancy rates in the North West fell dramatically from 81% to 48% in 2020. Prior to COVID-19, Manchester had consistent hotel occupancy of over 80%, which supported the appetite for hotel delivery in the region. Although demand is still relatively subdued, occupancy levels bounced back to 76% in September 2021.

Unsurprisingly, the UK’s airports have suffered due to a lack of visitors, but figures from October 2021 indicate that passenger numbers have been increasing gradually. Traffic was at 51% of the pre-pandemic (October 2019) level, due to the easing of travel restrictions and regulations.

In a further boost to tourism, in April 2021 Manchester was voted the best UK city to staycation for summer, and with 37% of people still planning to holiday within the UK in 2022 and more people taking shorter holidays, there should be cause for optimism about attracting visitors. Manchester was also named as the third-best city in the entire world in 2021, behind San-Francisco and Amsterdam. Looking at what makes these cities the best in the world - diversity, culture, and creativity - Manchester has in abundance.

Spending on cultural activities continues to rise and retail, leisure and hotel developments under construction will further support growth in the city’s hospitality offerings and its visitor economy.

Overall spending on cultural activities in Q3 2021 was higher by 29% on Q3 2020 figures and 11% on Q2 2021, while the return of live stadium audiences for football boosted spending on live sports events by 9%. The completion of Factory in 2022 and the Co-op Live Arena at the Etihad Campus will add to the City’s existing excellent culture and sports offering and support a vibrant city centre. Additional supply of hotel bedrooms is needed to support demand for overnight stays during events at major visitor destinations, both existing and under construction.

Public realm

As major schemes complete, new ‘pocket-parks’ are adding green space to the city and improving the pedestrian environment. Pedestrianisation plans will also link these spaces and further improve the city centre environment, supporting business and contributing to the net-zero target.

In the City Core, enhancements to Lincoln Square are creating public realm that will provide fully pedestrianised links between Deansgate, Queen Street, John Dalton Street and Albert Square. Albert Square is being transformed into ‘one of the finest civic spaces in Europe.’ The first phase of works is due to complete in 2022 and involves the closure of roads to the south and west and extension of the Square.

A riverside park with improved civic space next to the Cathedral will provide further public realm enhancements in the Medieval Quarter. This also includes the recently opened Glade of Light, a memorial to those who tragically lost their lives in the Manchester Arena attack in May 2017.

Also in the City Core, 5.7 acres of new public realm has completed in and around Symphony Park at Circle Square, providing green space for residents and workers in this new mixed-use city centre neighbourhood. New public realm has also been delivered at Kampus and Manchester New Square.

Further space is also under construction at Mayfield, providing a brand new 6.5 acre park in the City Centre prior to the first phase of commercial development being progressed. In the Southern Arc, the All Saints campus area of Manchester Metropolitan University is to be upgraded, providing an improved green space and pedestrian environment at the gateway to the Oxford Road Corridor. Overall, over 25 acres of new and improved public space has been, or is due to be, completed in Manchester city centre by the end of 2022.

Looking forward, a competition has been launched to redesign Piccadilly Gardens alongside separate plans by the National Trust to develop a New York style ‘high-line’ on the Castlefield Viaduct.

Planning has been accelerated to remove through traffic in Manchester city centre and to improve facilities for cyclists. Restaurants were forced by COVID restrictions to spill into streets to remain open, and there is recognition of the opportunity for a café culture across the streets of cities and town centres.

Government lockdown restrictions for COVID-19 have demonstrated the value of local open spaces and green infrastructure, with 46% of people saying they have spent more time outside during the pandemic than before. The delivery of green space and more pedestrian-friendly network of streets continues to be important for creating an attractive city centre to visit, work and live. Overall, the creation of a more locally-focused and independent-driven consumer economy, where all necessary amenities are within easy reach without the use of cars, will be a critical element in ensuring the transition of the region towards net-zero by 2038.

Students, eduacation and research

Education and research

A fall in the volume of education and research floor space on-site can be attributed largely to a 143% increase in the volume of floor space completed, and to a slowdown in the delivery of new schemes to site.

In 2021, three schemes were under construction providing 518,836 sq ft of education floor space, including 200,000 sq ft at The Manchester College next to Victoria Station that is due to complete in April 2022. The remaining floor space is being delivered across two further schemes that started construction in 2021: a creative college at New Century Hall (12,818 sq ft) complementing the range of uses in NOMA; and the Manchester Metropolitan University Science and Engineering Building (306,018 sq ft) located between First Street and Circle Square.

There are two fewer schemes on-site overall compared to 2020. This represents a drop of 53% from the 1.1 million sq ft under construction, but the level of completions in 2021 far exceeds the figures in the years before 2020. In total, 938,876 sq ft of education and research floor space completed in the Crane Survey area across three schemes:

- Manchester Metropolitan University Institute of Sport (46,876 sq ft)

- Manchester Metropolitan University School of Digital Arts (SODA) (56,000 sq ft)

- The University of Manchester MECD (840,000 sq ft).

Looking ahead, the delivery of the Manchester College development in 2022 will provide a hub for digital media, computing and visual arts, which will complement the region’s strengths within the creative and tech sectors. It will also provide a stepping-stone to regeneration within the Great Ducie Street Strategic Regeneration Area. Manchester Metropolitan University’s Science and Engineering Building will accommodate research in areas such as health and wellbeing, computing, smart cities, ageing, and climate change. It will also make effective use of a gap site between First Street and Circle Square on the University's existing John Dalton complex.

840,000 sq ft of education floor space completed at MECD in 2021, a scheme the size of eleven football pitches.

The lower construction volume in 2021 can be attributed partly to the high volume of education floor space that was completed by the University of Manchester at MECD, which now caters for 6,750 students. The £400 million MECD is the largest home for engineering in the UK and the biggest construction project ever completed by a higher education institution. The building, committed to achieving BREEAM Excellent, will ensure that the University of Manchester, and Manchester more widely, is at the forefront of engineering and sustainability globally. It will provide world-class sustainable research facilities to sit alongside two flagship centres of excellence – the Henry Royce Institute and the National Graphene Institute, the UK’s national institute for advanced materials research and innovation.

The City’s Higher Education institutions are key economic assets within the Oxford Road Corridor and the continued development of these assets is paramount to achieving the vision for the Corridor and the City in general.

Leaps and bounds

Of the developments that have completed, all are part of the cluster of research and education sites within the Oxford Road Corridor. The scientific pioneering activity within the Corridor had beneficial effects on construction practices in 2021. The first commercial use of concretene at Mayfield - a blend between concrete and wonder material graphene - provides a more environmentally-friendly version of concrete. The link between engineering solutions and the commercial economy will become increasingly critical for addressing the challenges of climate change

Higher education and research and development institutions have a key role to play in innovation for climate change action.

The Manchester Metropolitan University Institute of Sport will seek to capitalise on the city’s existing strengths, providing a world-class institute for sports research. It will build on the city’s pre-eminence in sport, represented by the presence of two major football teams in England and the Etihad Campus, which is also home to the National Cycling Centre, National Squash Centre, the GB Water Polo Team, the GB Taekwondo team and the Manchester Institute of Health & Performance.

School of Digital Arts (‘SODA’) is a purpose-built building to support Manchester Metropolitan University’s ambition to be a world-leader in digital arts, providing a digital and creative skills powerhouse with space for collaboration and innovation. It will provide space for those specialising in film, animation, UX, design, photography, sound design, gaming, and artificial intelligence. To showcase these skills, the building features an exciting changeable LED façade.

There are few research and education schemes with planning permission, but there is clear ambition to develop further the education, research and innovation offerings in Manchester and Salford. In Salford, plans are in the pipeline for the creation of a new innovation district at Salford Quays, to capitalise on the existing presence of media and technology, and also for the proposed redevelopment of the University of Salford’s £800 million ‘EcoCampus’.

A partnership announced between the University of Manchester and Bruntwood SciTech will enable progress in Manchester towards the delivery of ID Manchester, a £1.5 billion innovation district envisaged for a key City Centre site between Mayfield and Circle Square. This internationally significant project will ensure that Manchester is at the forefront of innovation in the science and technology sector. It has been designed specifically to maximise the economic impact of the existing research and development institutions within the Oxford Road Corridor, including the National Graphene Institute, the Graphene Engineering Innovation Centre, the Henry Royce Institute, the Manchester Institute of Biotechnology, and the Christabel Pankhurst Institute for Health Technology.

Within the Oxford Road Corridor Innovation District, the city’s strengths in science and technology are to be further improved with the delivery of Citylabs 4.0, which will add to the world-class hub for health innovation and precise medicine within the Manchester University NHS Foundation Trust (MFT) campus, the UK's largest NHS Trust.

Student accommodation

In total only two purpose-built student residential developments are on-site in the Crane Survey area, 84 Cambridge Street (62 beds) and Echo Street (242 beds). 84 Cambridge Street, located in the Oxford Road Corridor, is the only scheme to start construction in this sector during 2021. The development is small scale compared to other student residential developments that have come forward in the area in recent years and is due to be completed in 2022.

In terms of completions in 2021, Archway Halls was the only scheme to be delivered to market. This scheme, brought forward by Manchester Metropolitan University, delivered an additional 492 student bedspaces within the Oxford Road Corridor and the Southern Arc, between the Birley Fields and All Saints areas of their estate.

The development pipeline for student accommodation in 2021 is 65% smaller than in the previous year, when the highest level of delivery since 2012 was recorded. This reduction is the result of the delivery of major schemes in 2020, including Artisan Heights (603 beds) and River Street (807 beds).

Manchester has one of the largest student populations in Europe with an average of over 100,000 students in the region and 70,000 students in Manchester itself

The higher education institutions in Manchester and Salford are important to the local economy and benefits extend well beyond formal education. £5.3 billion was generated for the UK by Manchester’s universities in 2018/19, with £1.2 billion of this benefiting Manchester directly.

During 2020 and into 2021 there were some concerns regarding impact of the pandemic on the student intake at Manchester and Salford’s higher education institutions, due to uncertainty over student experience and financial stability. This could explain why across the UK in general, planning activity has been subdued within the student accommodation sector as developers hold off from starting on-site until demand became more predictable.

In the event, student enrolments for both Manchester Metropolitan University and the University of Manchester for 2020/2021 were higher than for 2019/2020, at 73,906 students in total. Admissions for the 2022/2023 student intake expected to increase further. In view of the developments referred to previously, such as the Manchester Engineering Campus, School of Digital Arts and Manchester Institute of Sport, it is evident that the higher education institutions are investing heavily in the development of their estates to support students and to continue to attract the best talent from across the UK and internationally.

With the higher education institutions focused on key sectors of the economy, companies are attracted to locate in Manchester and Salford, and students are choosing to stay in the area after graduation, with around 36,000 graduates annually entering the labour market in the region and 10,000 in Manchester itself. The provision of student accommodation within the city centre and Oxford Road Corridor is a key part of the education, research and innovation investment cycle.