The future of GST - taxable supply information

Tax Alert - September 2022

By Jeanne du Buisson & Haidee Watkin

The latest Tax Bill includes a number of further remedial tidy-ups to the major changes around GST tax invoicing that were in the Taxation (Annual Rates for 2021-22, GST and Remedial Matters) Bill and which largely come into effect on 1 April 2023. We've set out below the updated position that will apply from 1 April 2023, assuming, of course, that the updates contained in the latest Bill are enacted as proposed. Deloitte will be making submissions to try and make a number of the changes more practical. This area is still a bit of a moveable feast, and it will be important that businesses ensure they are aware of the final position before the new rules apply on 1 April 2023.

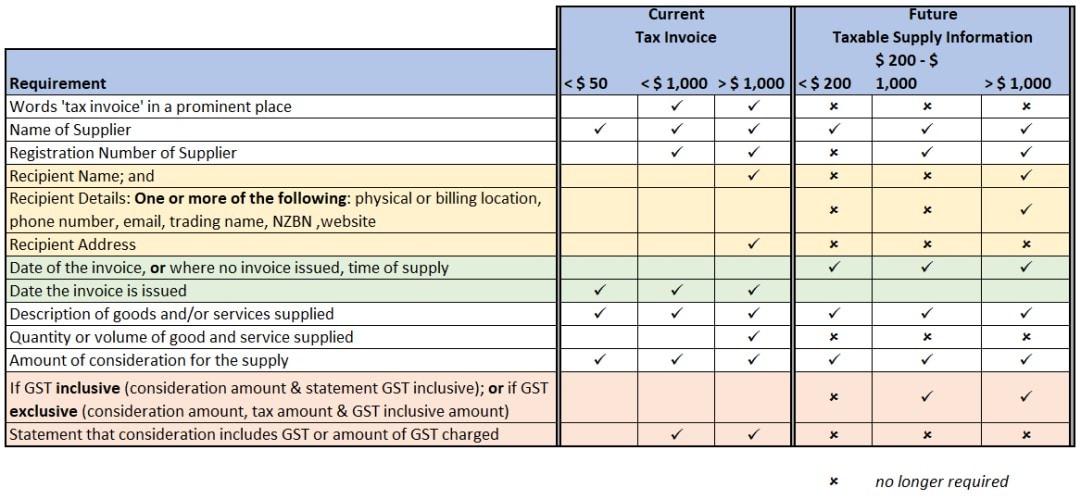

The existing mandatory requirement to hold a ‘tax invoice’ to claim an input tax deduction has been replaced with a requirement to ‘hold’ business records showing that GST has been borne on the supply. These information requirements no longer need to be contained in a tax invoice and can be contained in a variety of business records such as documents containing contractual information, systems and databases holding key supplier/customer information or sales and purchasing documentation issued. As an aggregate, these documents may already exist in organisations' systems and provided they met the minimum information requirements, become taxable supply information.